Developed Countries

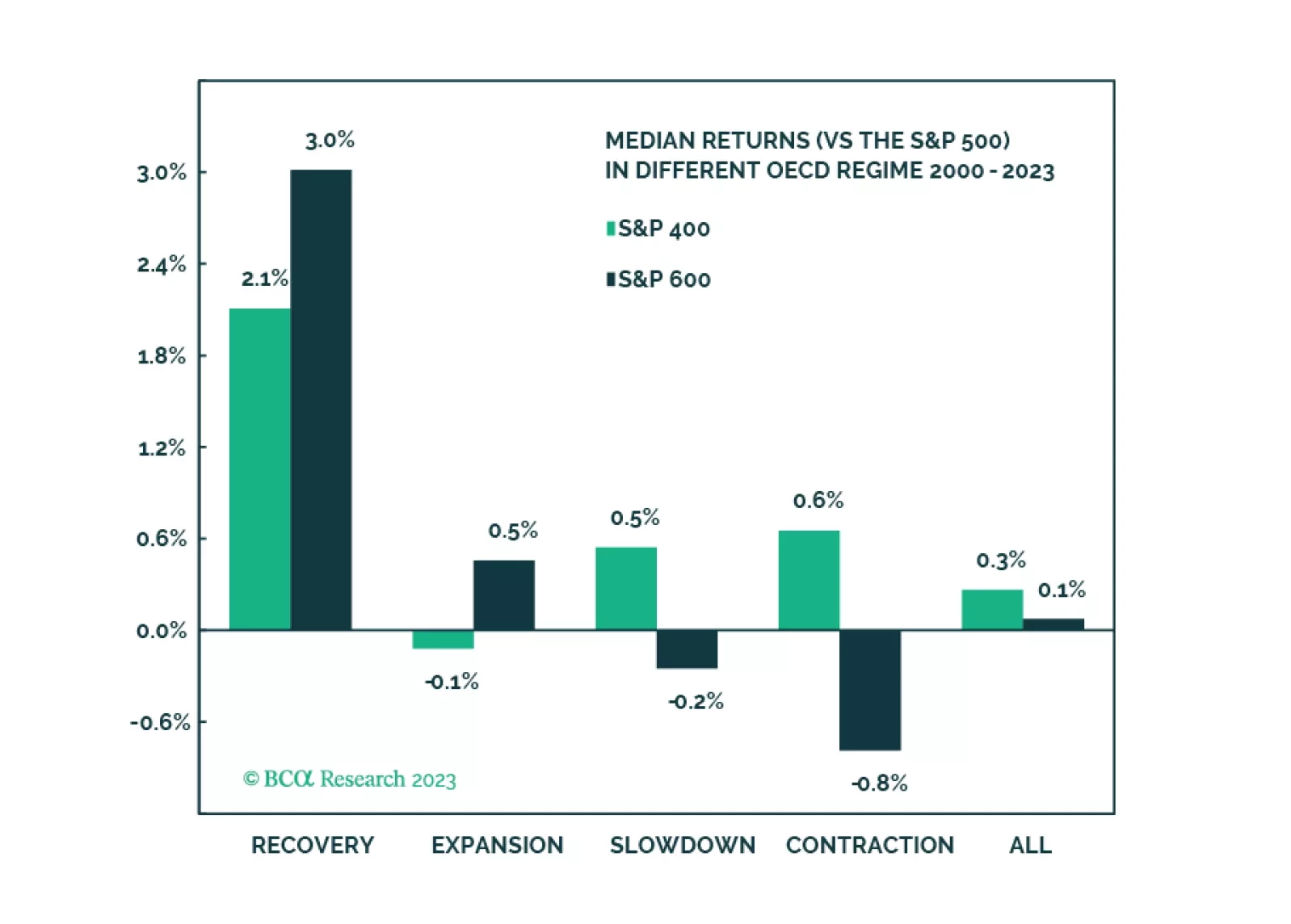

Mid-caps are the best of both worlds and are an excellent strategic overweight thanks to their size premium, but also better financial quality and higher dividend yield than Small. We are bullish on Mid near term and believe that this may be a great trade. We will initiate a position in the S&P 400 as a tactical overweight but will monitor it very closely.

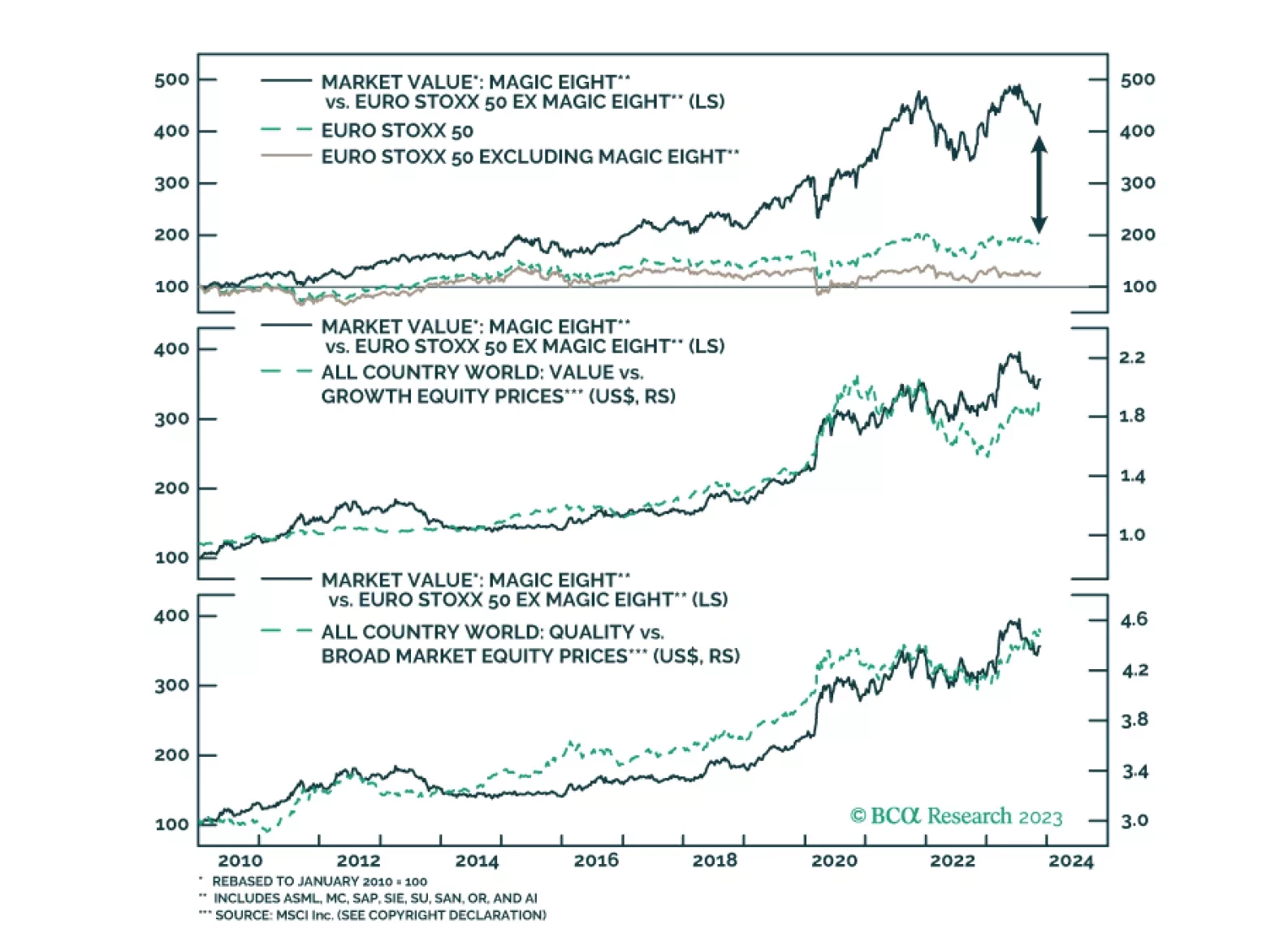

The US has the Magnificent Seven, Europe has the Magic Eight. What drives the performance of those eight stocks crucial to the European market?

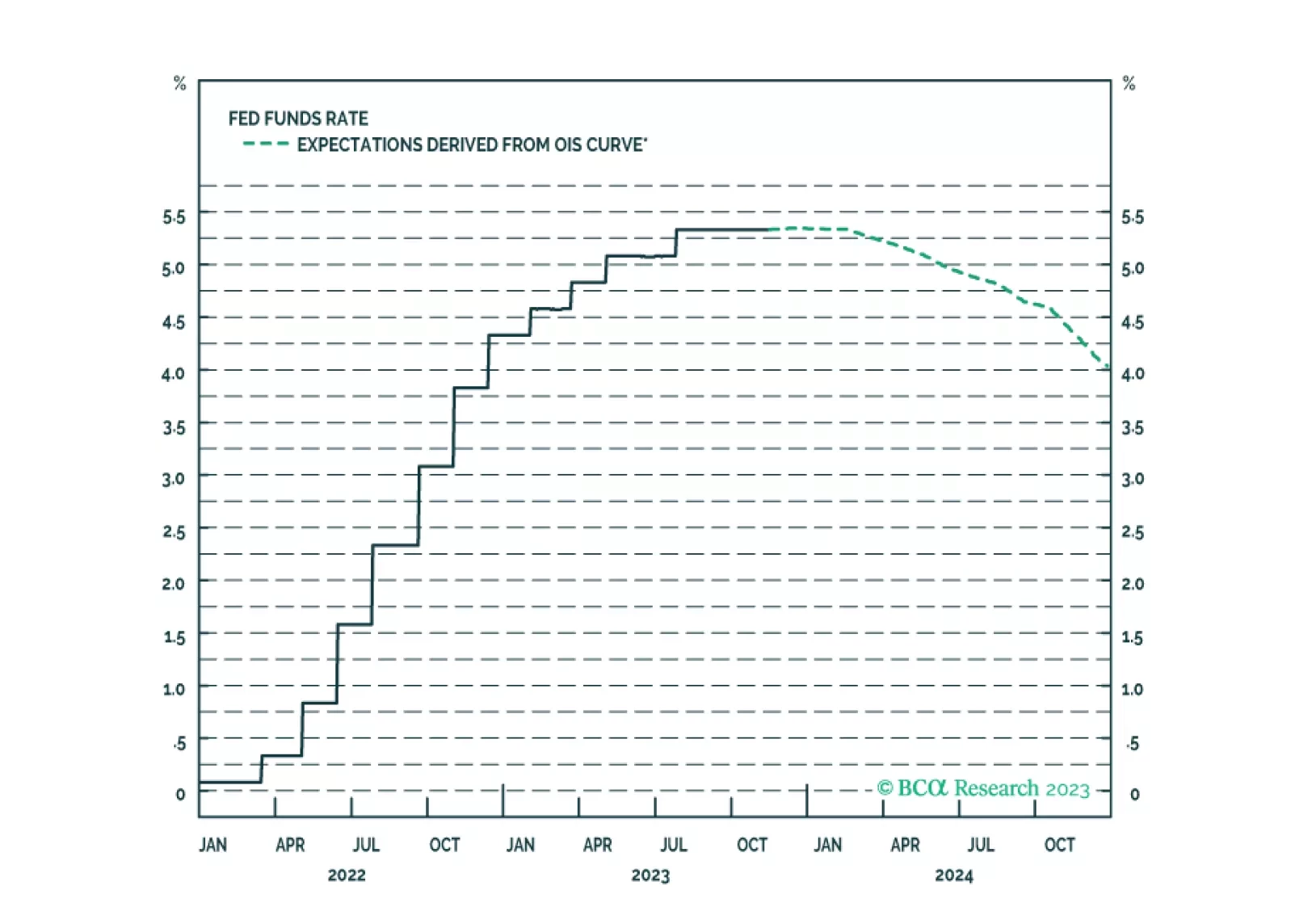

The soft-landing narrative has gotten nowhere at BCA but appears to be making some headway with broker-dealers and investors. We are preparing to lean against it once it pushes equity prices a little higher.

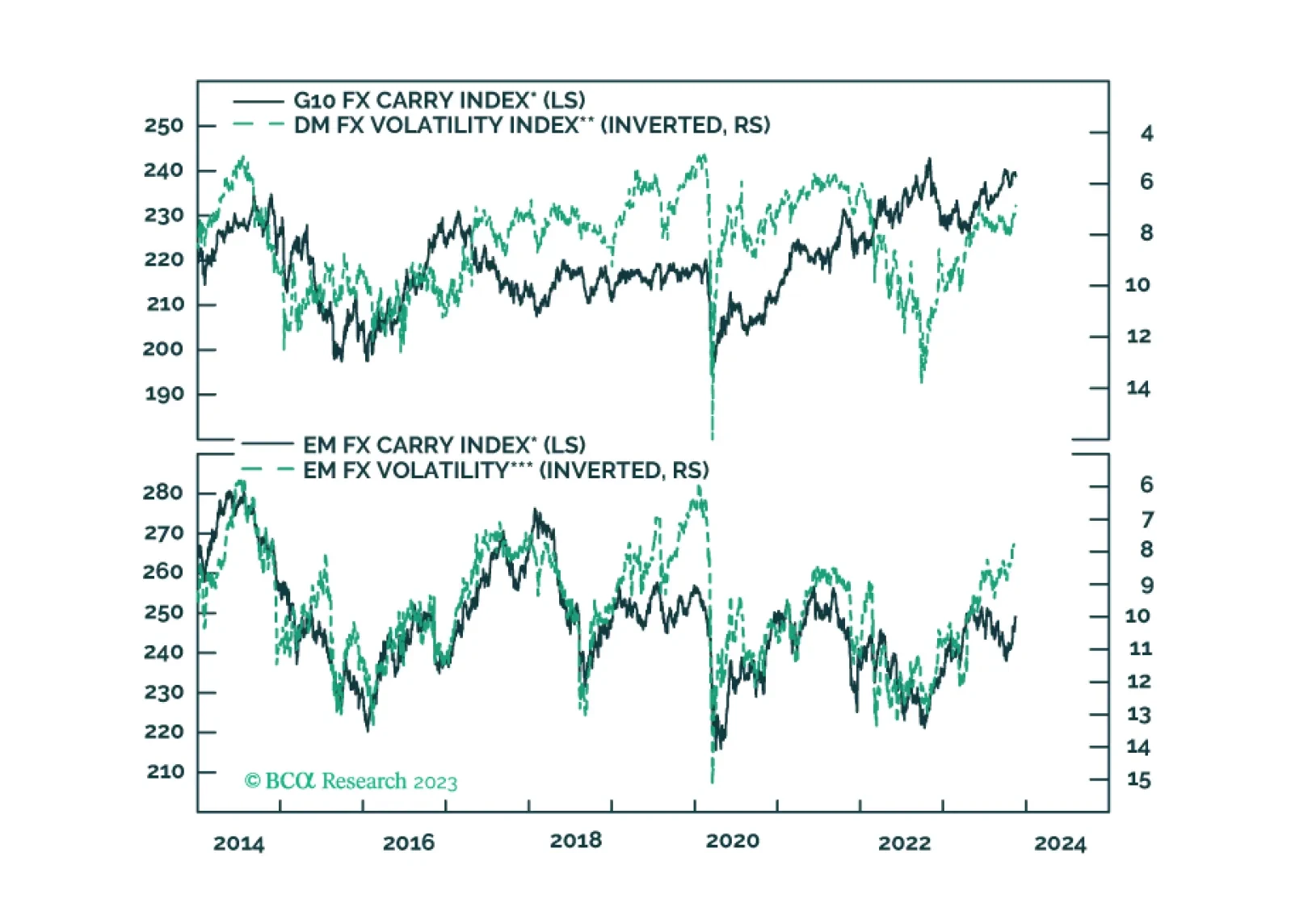

In this report, we evaluate the risk to carry trades in the coming months.