Developed Countries

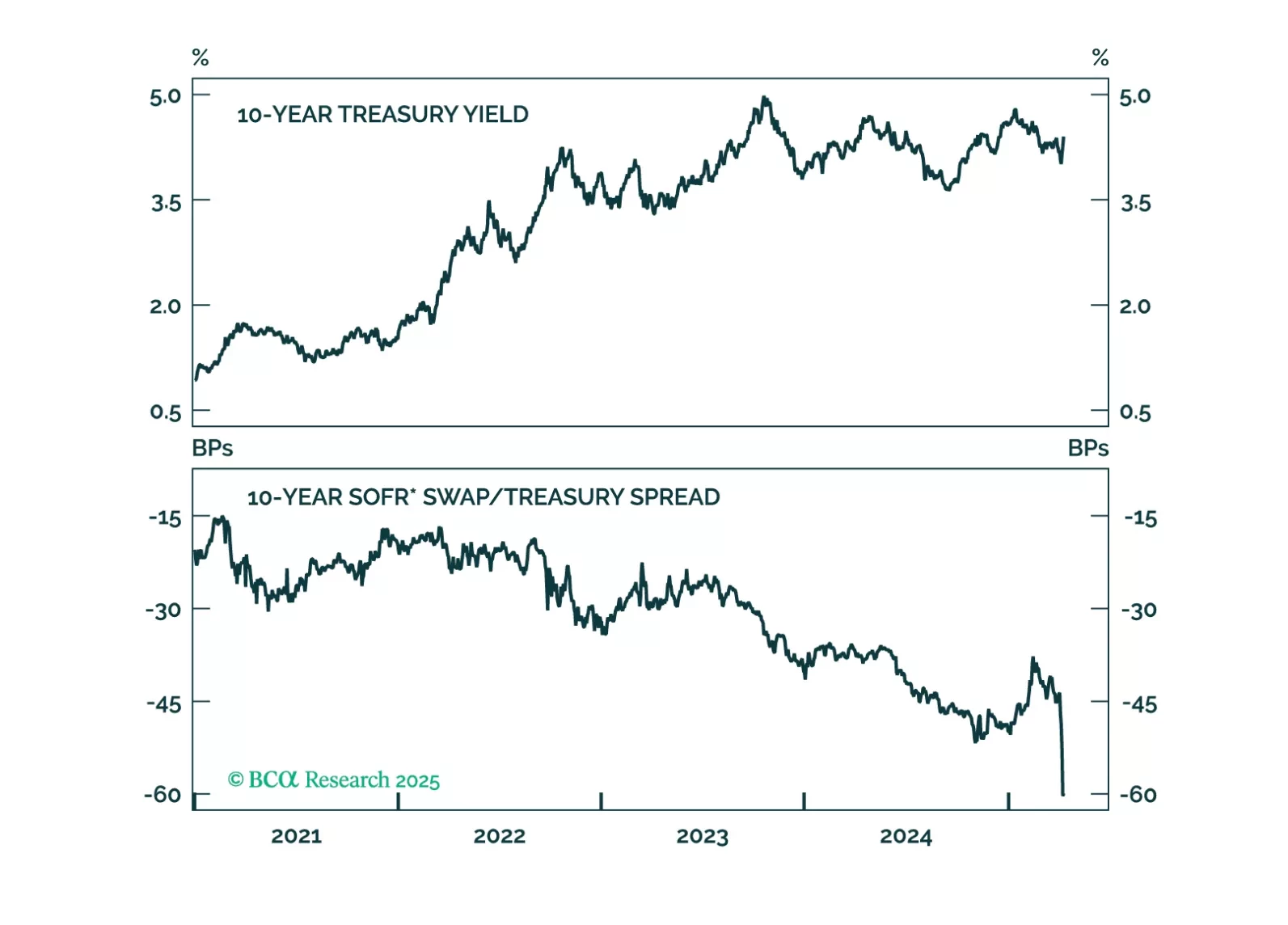

The combination of dollar weakness and rising US yields suggests global investors are questioning the safe-haven status of US Treasuries.

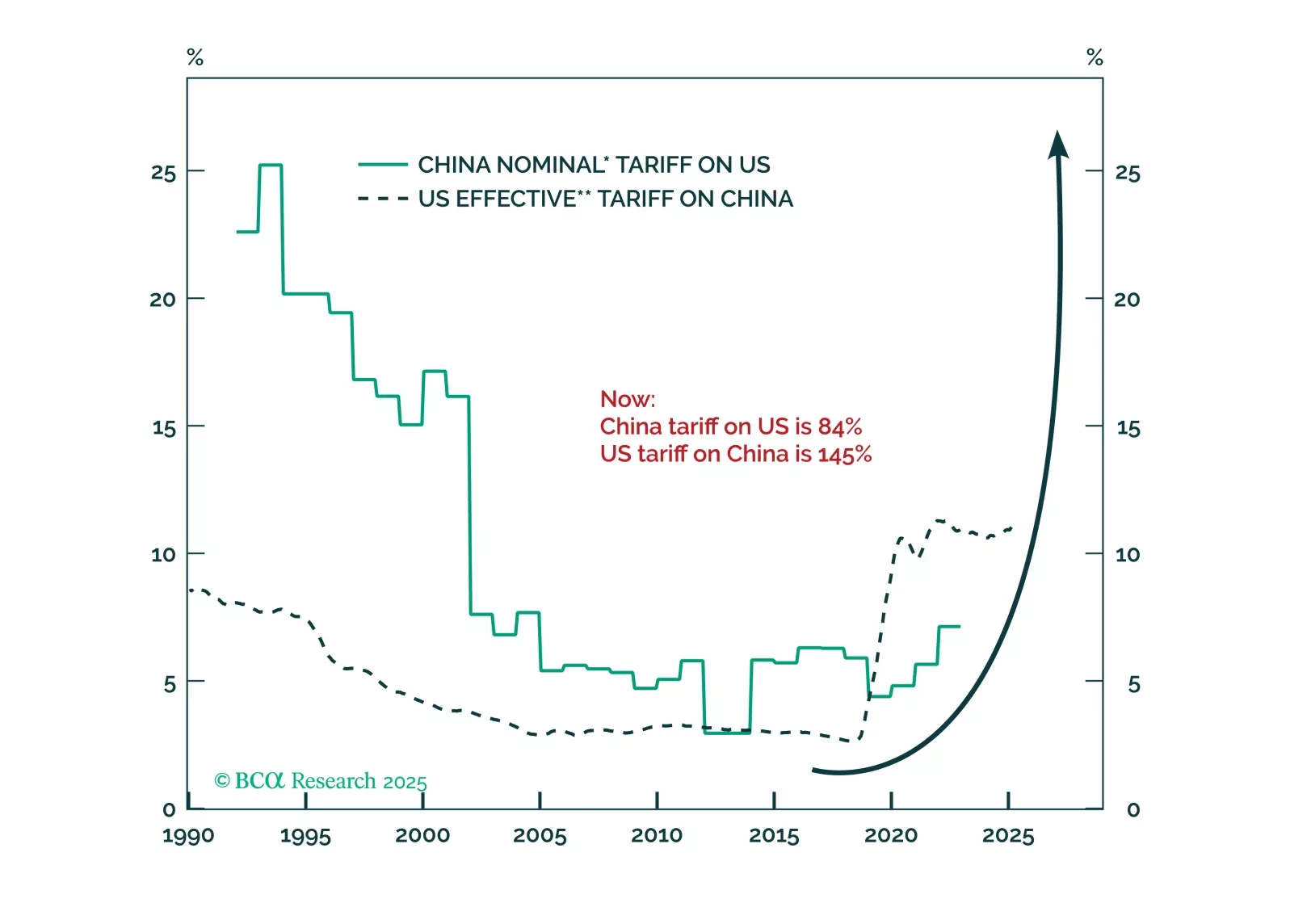

China prepares to devalue the yuan in response to US tariffs. Our Emerging Markets strategists recommend shorting CNH, downgrading offshore Chinese equities, and staying bearish on global risk assets. Beijing sees the tariffs as a declaration of economic war,…

Dips in European assets remain long-term buying opportunities, even though short-term risks abound. A notable feature of the recent selloff is that US safe havens failed to rally. In a global growth scare, both the US dollar and Treasuries typically benefit.…

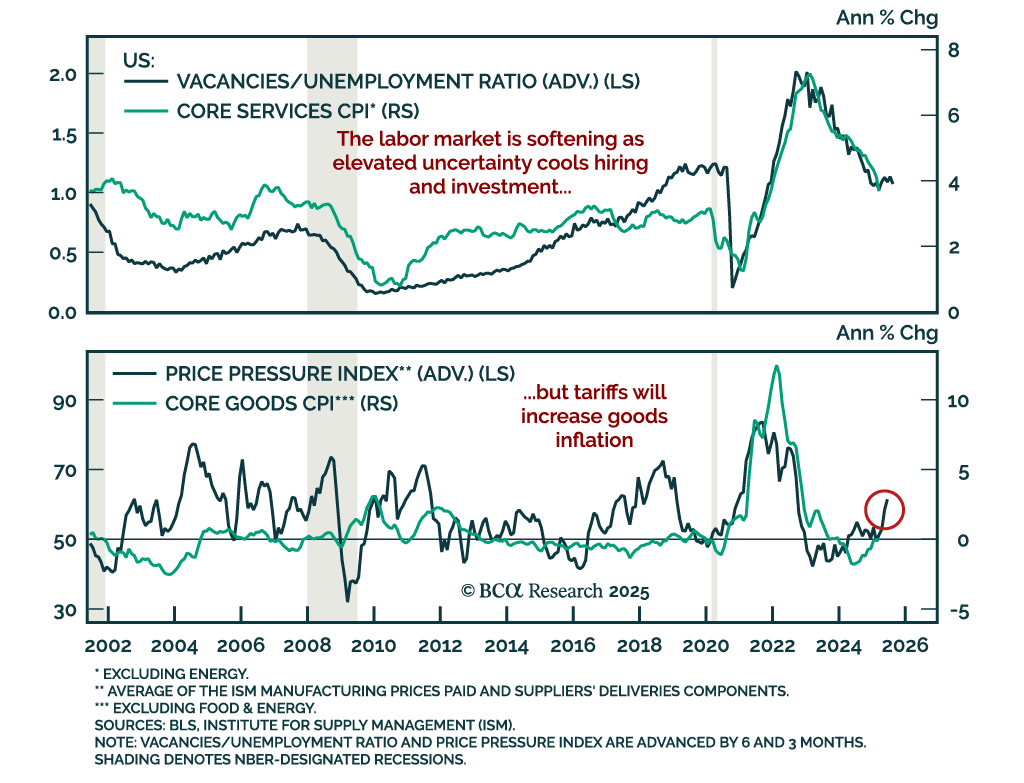

March’s cooler CPI print reinforces our defensive positioning as it points to softening growth that the Fed cannot address yet. Headline CPI came in at -0.1% m/m (2.4% y/y), and core rose just 0.1% m/m, slowing to 2.8% y/y from 3.1%. Core services inflation…

Will US-China Trade War Escalate To Real War?

China’s aggressive retaliation against U.S. tariffs will enable President Trump to shift from punishing allies and redirect the trade war toward China. If Beijing does not react to the latest tariffs by doubling its fiscal stimulus, it indicates they are planning something different, as China will encounter economic destabilization. The likelihood of a hybrid military pressure on Taiwan will rise.

Our Global Fixed Income strategists continue to recommend long duration exposure, curve steepeners, and an underweight in corporate bonds relative to government bonds, as global recession risks rise. The trade war has increased the odds of a downturn, but the…

We maintain an overweight in government bonds, as recent yield spikes appear technical and unsustainable. US 10-year Treasury yields have surged even as global markets were selling off on growth fears. The move has spread to higher-yielding DMs like the UK,…

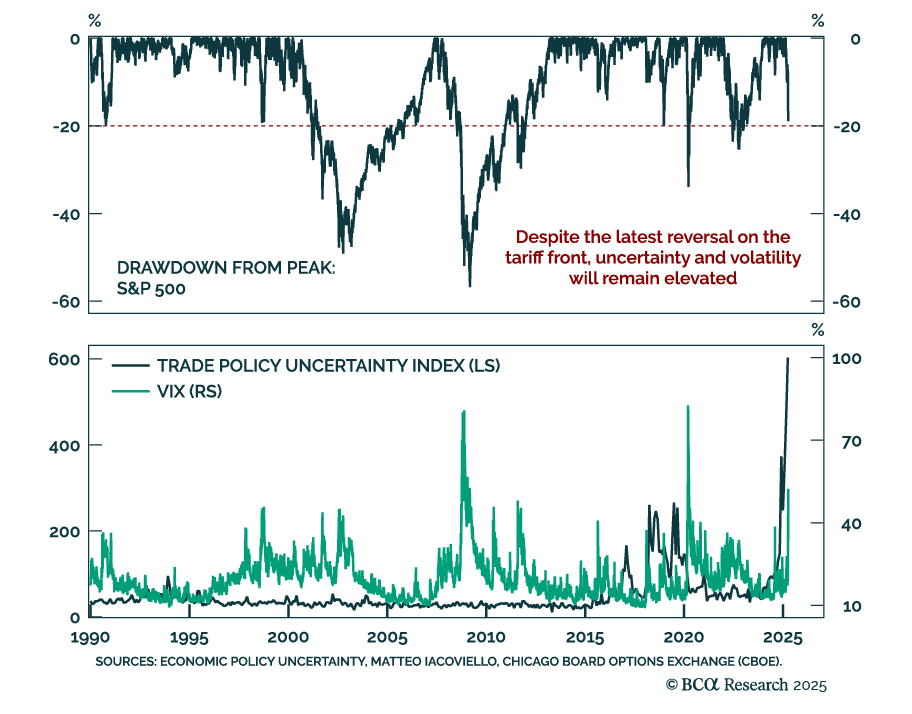

We maintain a defensive asset allocation, as the hit to confidence will linger even if tariff tensions ease. The past few days have seen sharp volatility, with trade headlines swinging markets between despair and euphoria. At the time of writing, President…

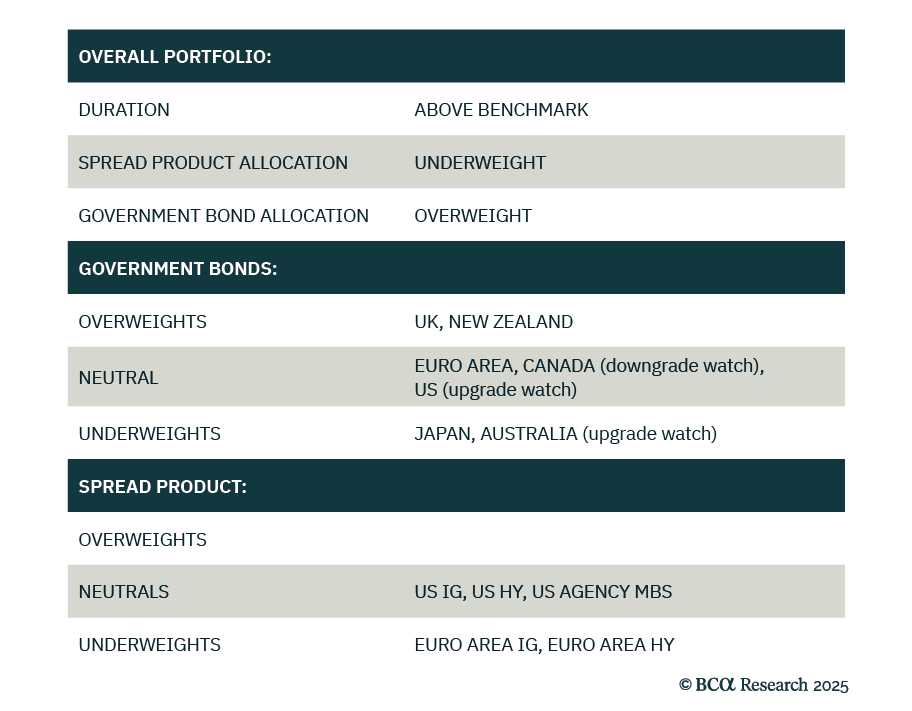

Our Portfolio Allocation Summary for April 2025.

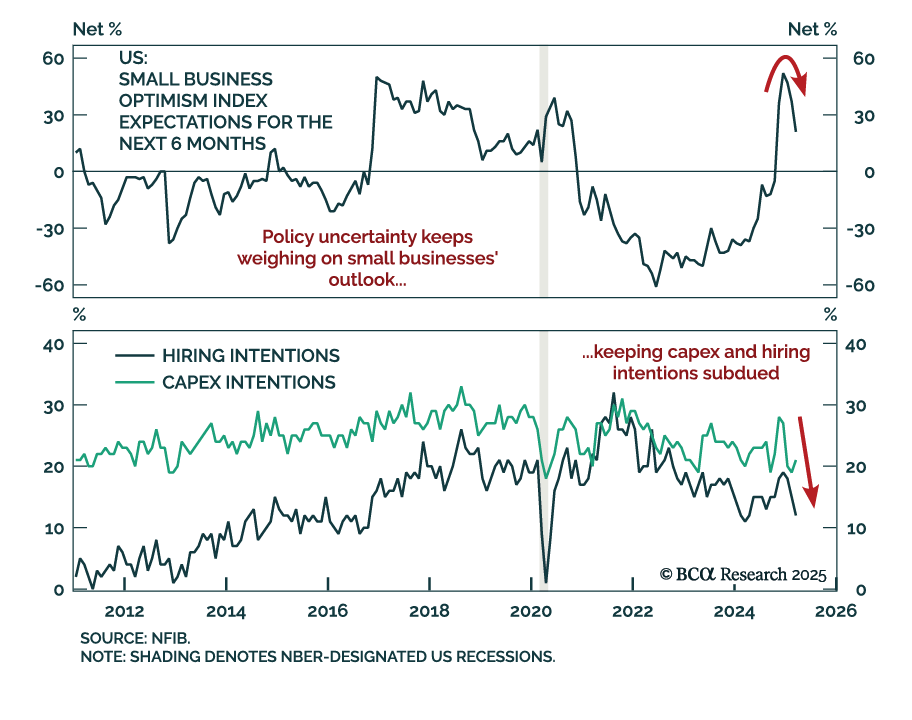

The sharp drop in March’s NFIB survey reinforces our defensive asset allocation, as small business sentiment weakens amid rising policy uncertainty. We remain overweight government bonds and underweight risk assets, while tactically shorting the January 2026…