Developed Countries

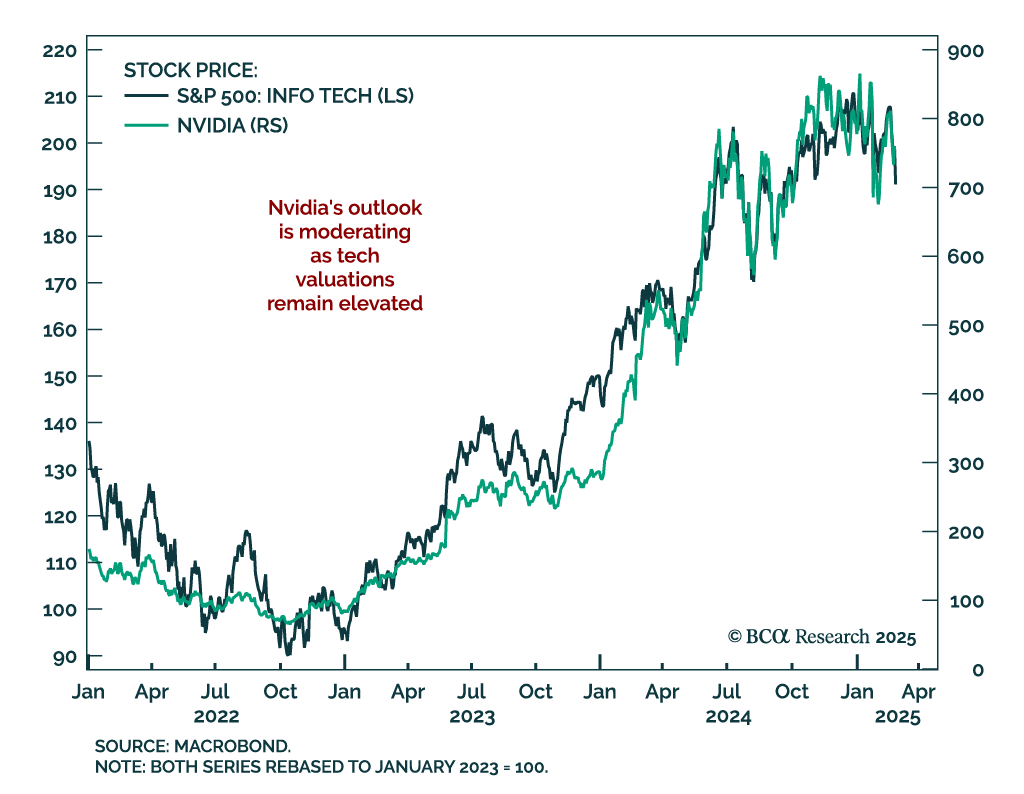

Nvidia announced good results, but Q1 sales guidance fell short of expectations. The numbers point to growth normalization as investors have been accustomed to blowout numbers. Nvidia’s meteoric rise means investors think about the company in exponential…

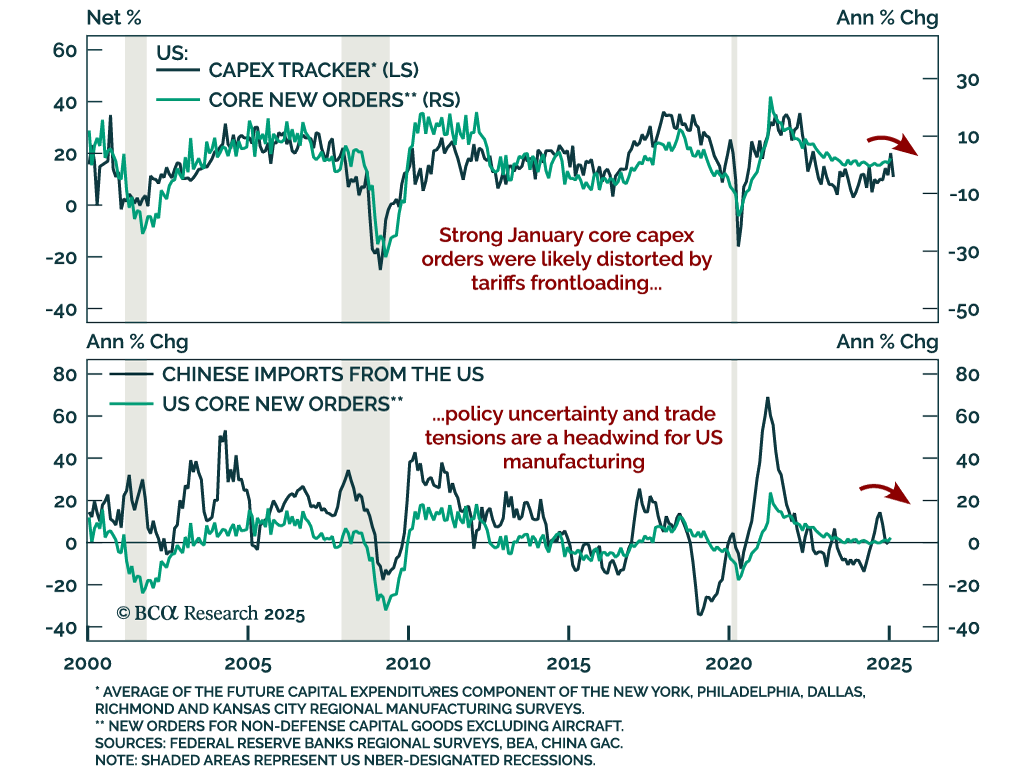

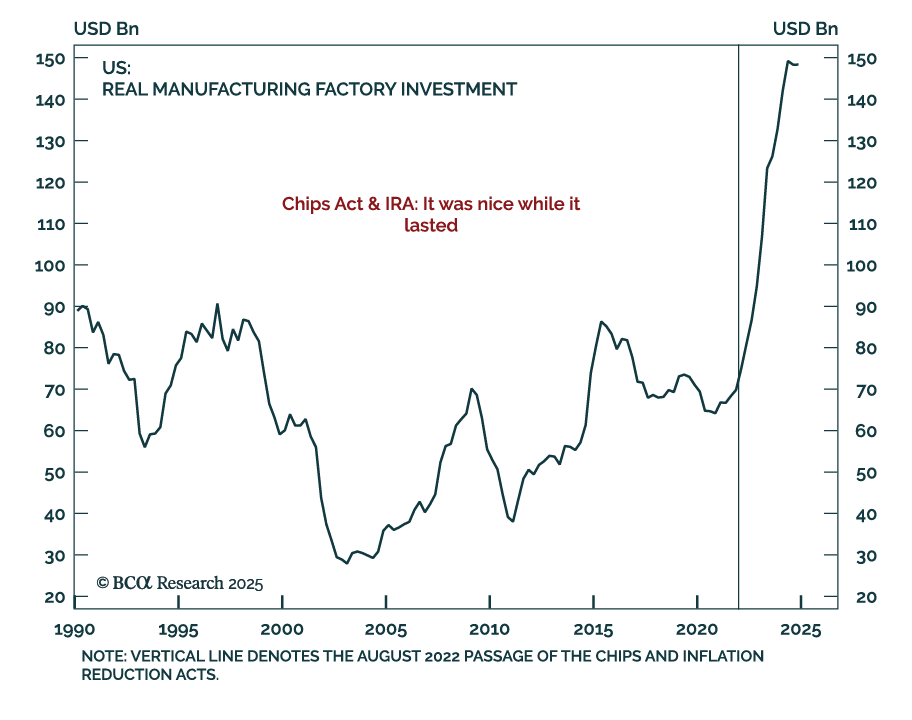

US January core new orders beat expectations, rising 0.8% m/m, an acceleration from 0.2% in December. This measure, which excludes defense and aircraft from capital goods, is used as a proxy for business investment. Core shipments however decreased…

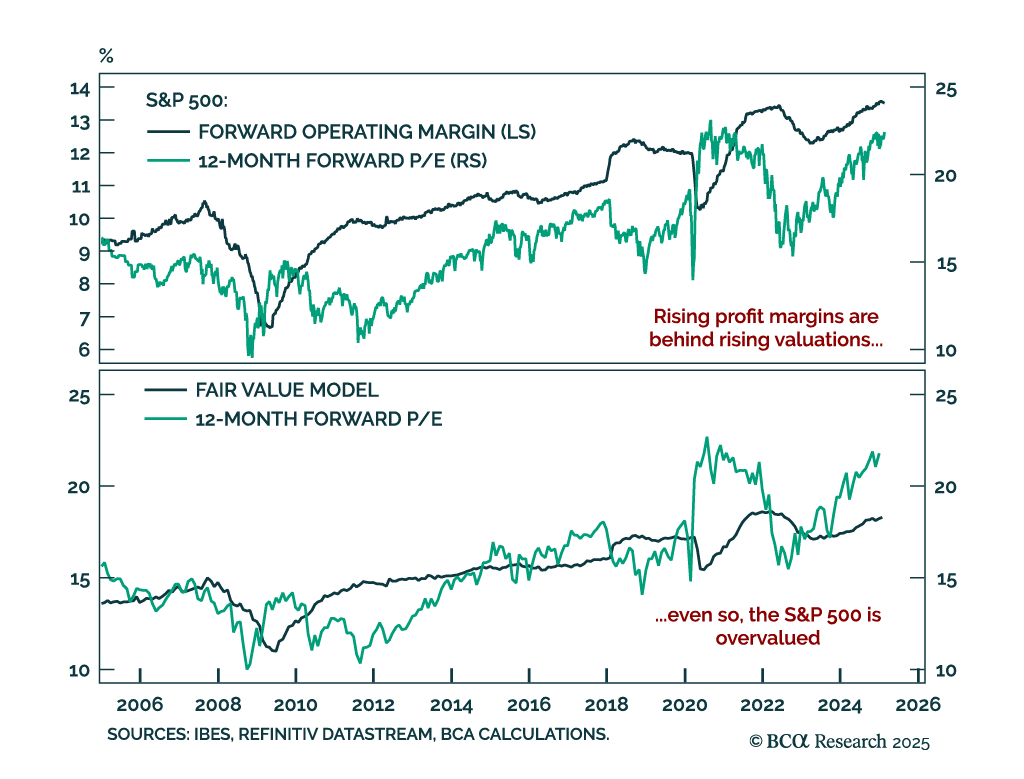

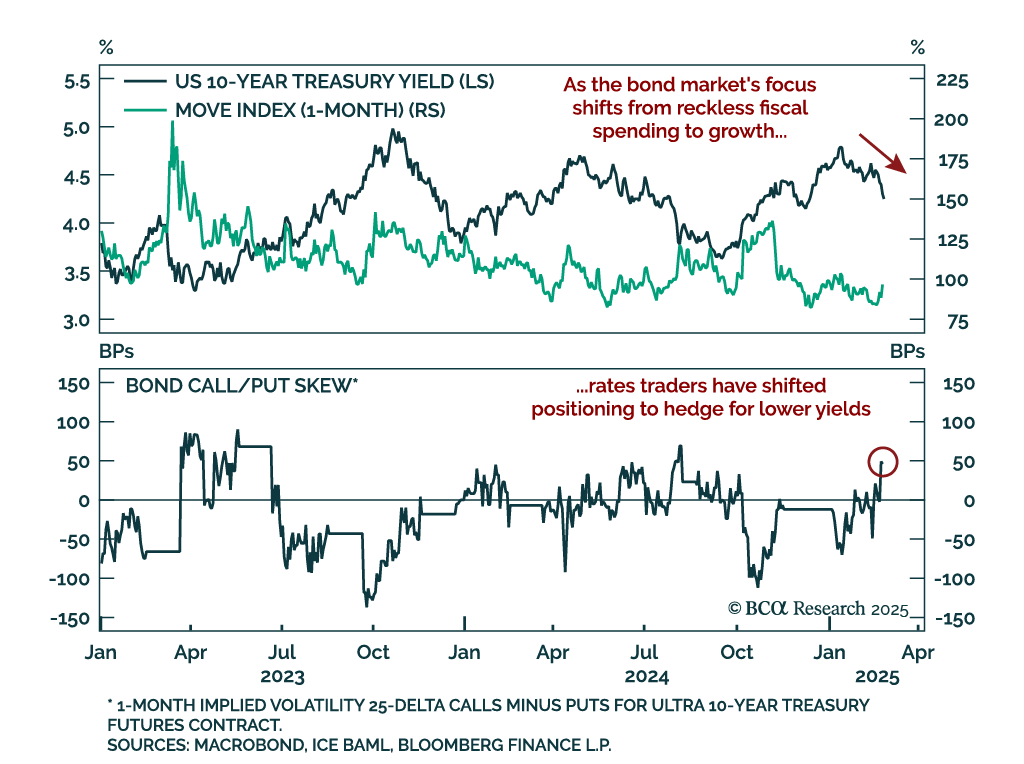

Our US Equity strategists held a roundtable, which led to many client questions addressed in the team’s latest report. Long-term interest rates will decline if disinflation persists, deficits shrink, or economic growth slows, though each scenario…

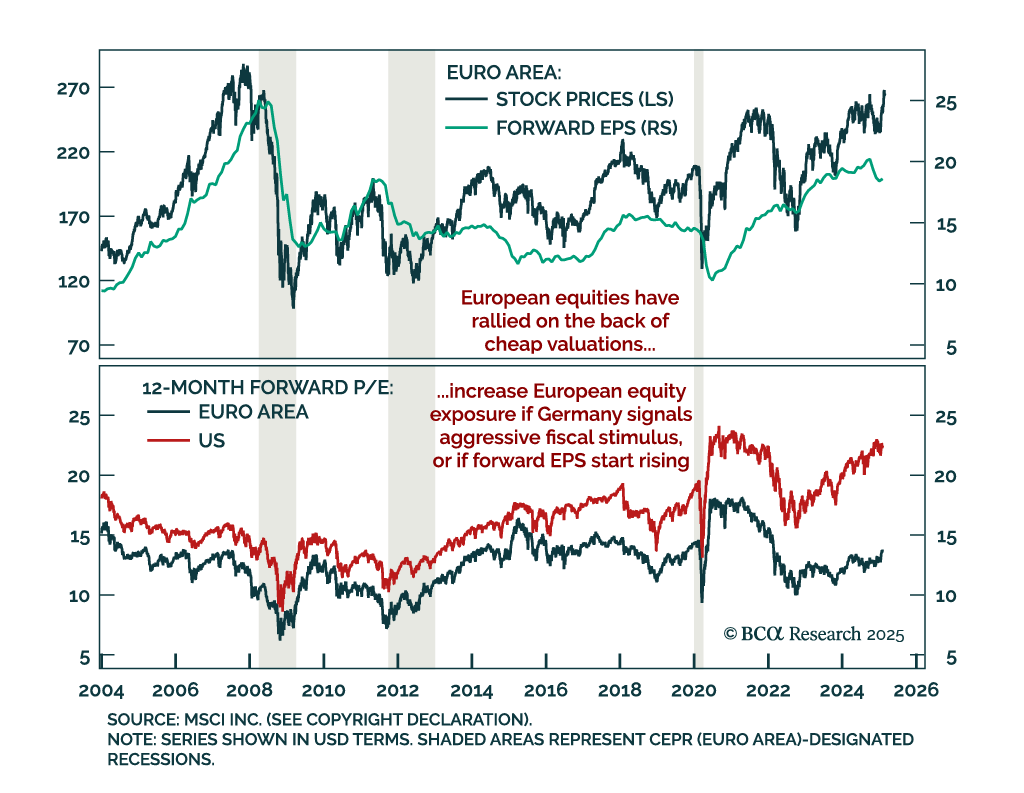

European equities have outperformed the US so far in 2025, especially after Euro Area economic surprises started outperforming as the US is starting to disappoint. The current leadership change between US and European assets reflects extremely one-sided…

The House of Representatives passed a Budget Resolution bill that adds $2.8tn to the deficit by 2034. Our Geopolitical strategists highlighted during our BCA Live & Unfiltered meeting that the Senate is likely to modify it by increasing tax cuts and…

Our US Investment strategists visited Midwest clients, and provided a summary of their discussions with investors. Despite solid data, investors should focus on where the economy is headed rather than where it has been. Excess savings have been spent,…

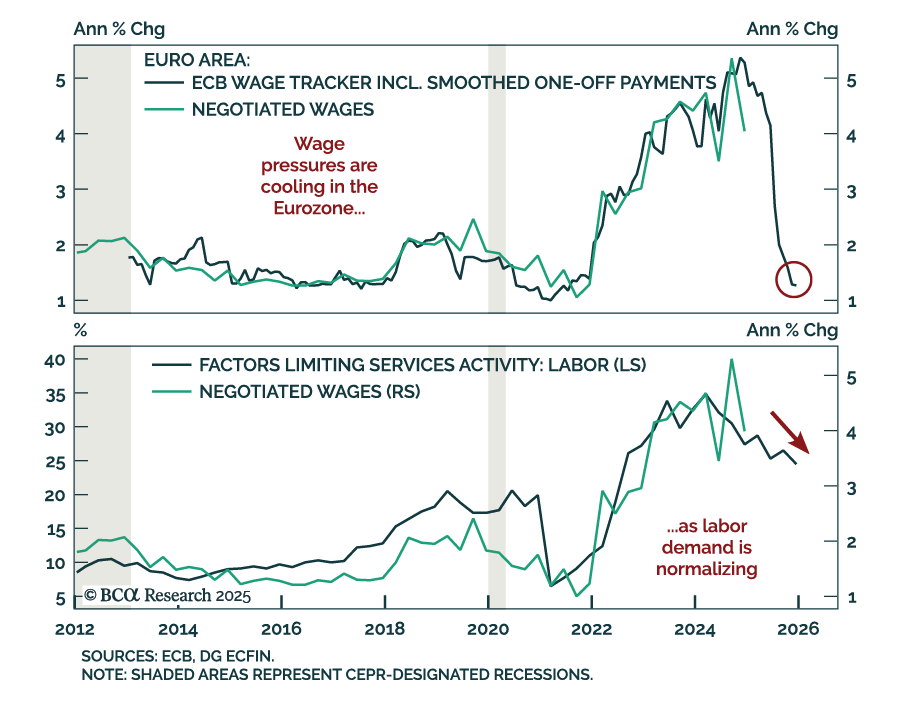

Fourth-quarter European negotiated wages growth cooled to 4.1% y/y, down from the 5.4% peak seen in Q3. The cooling is in line with the ECB’s Wage Tracker showing wage growth decelerating to 1.3% by the end of the year. Labor demand is easing in Europe,…

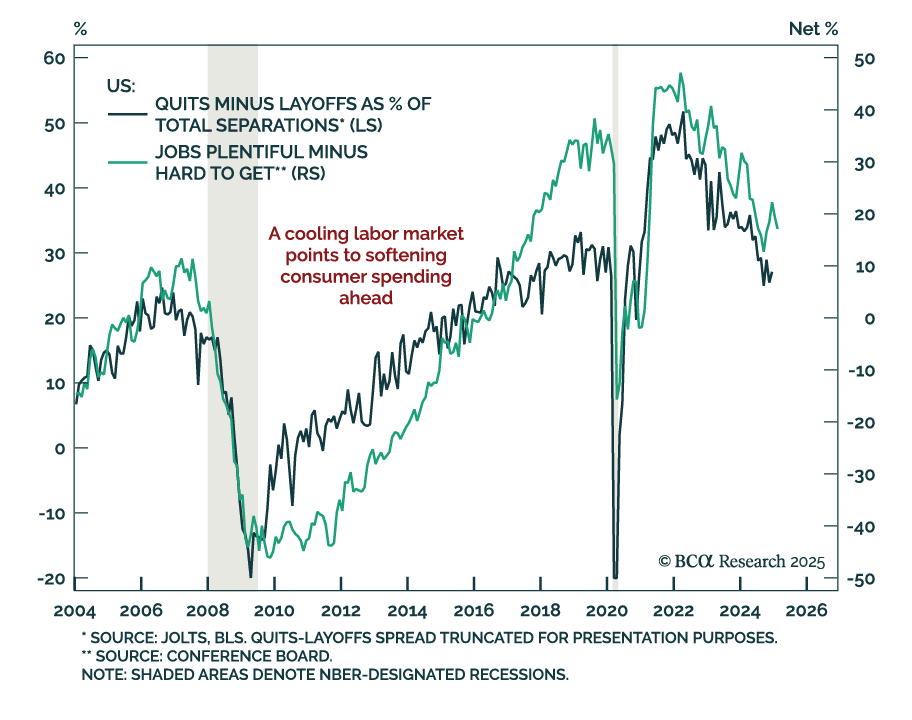

The February Conference Board Consumer Confidence index missed estimates for the third month in a row, falling to 98.3 from 105.3. Consumers’ assessment of both their current situation and their expectations worsened, with the latter falling close to 10…

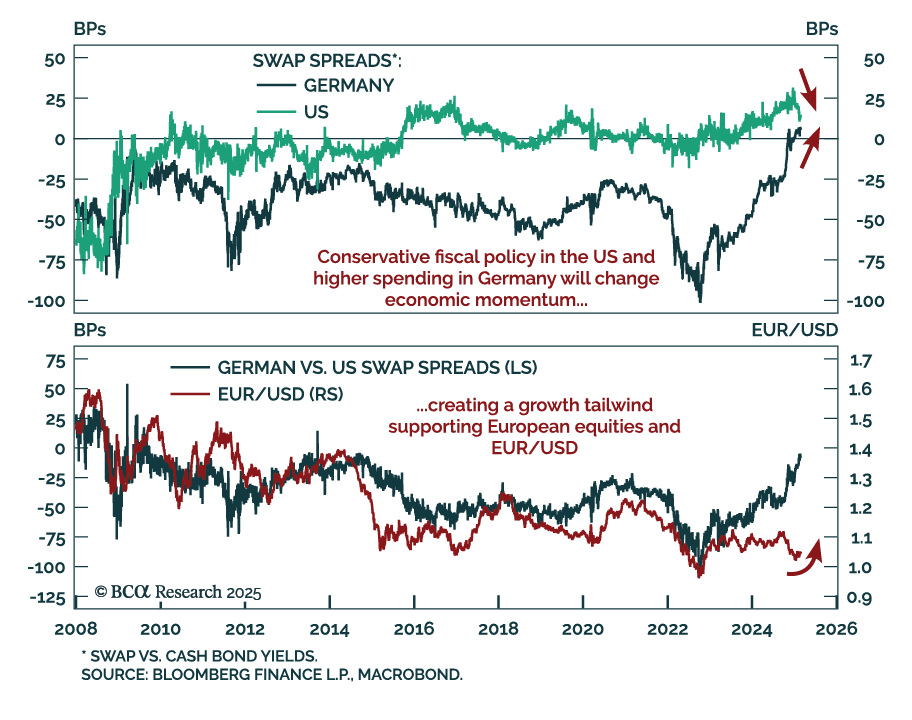

German election results were roughly as expected, but Europe’s biggest economy suddenly just got more interesting. While the details of the governing coalition have yet to be finalized, Chancellor Merz has floated options to ease the “debt brake”, which…

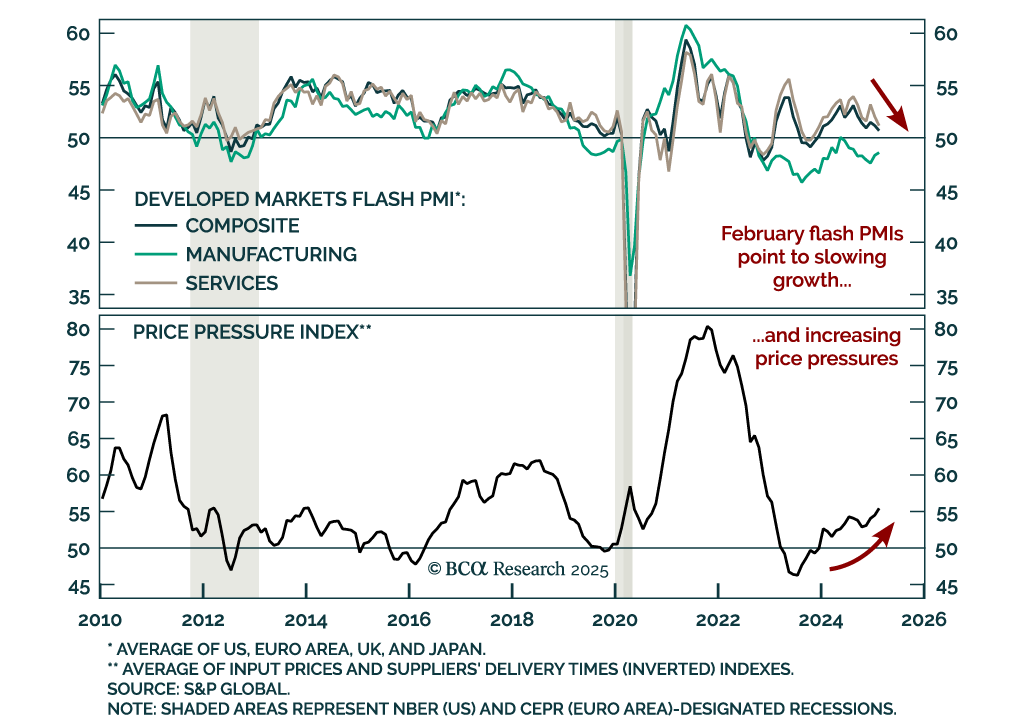

February’s flash PMIs for the major developed markets showed softening growth, and rising price pressures. The US composite index missed estimates and decreased to 50.4 from 52.7 in January. Services were a big contributor to the decline, with the index…