Developed Countries

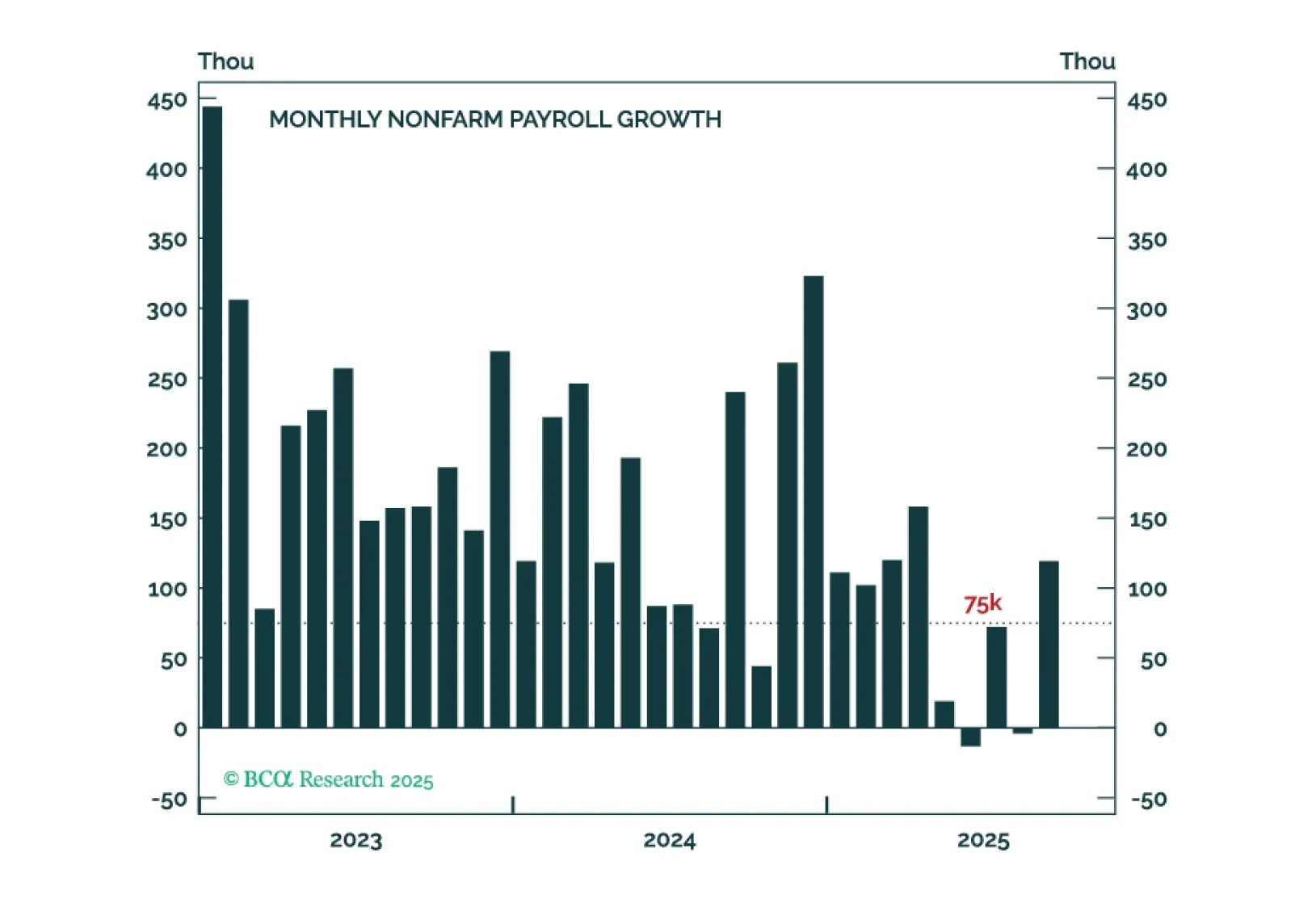

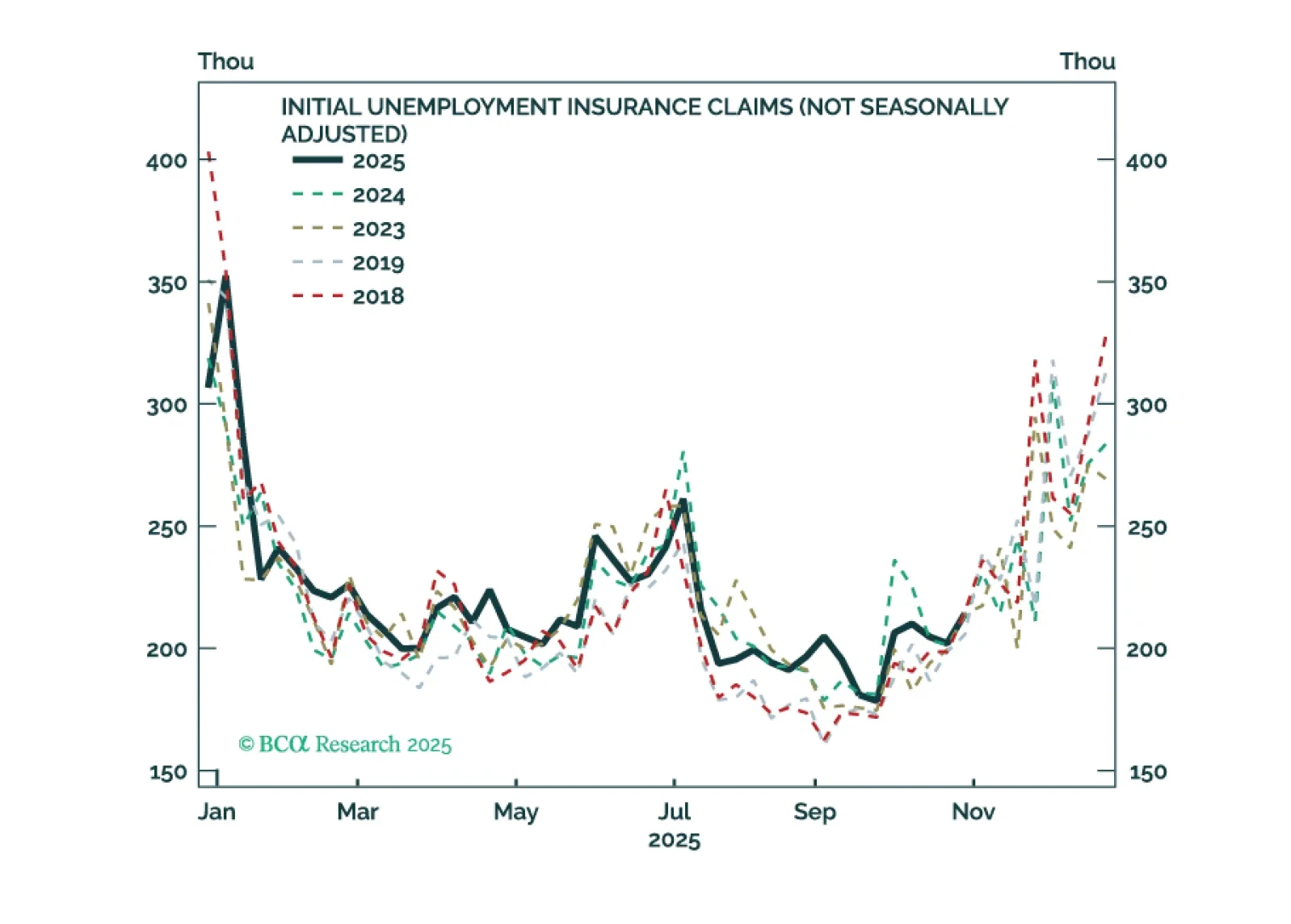

The September employment report probably won’t convince enough hawks to vote for a rate cut in December.

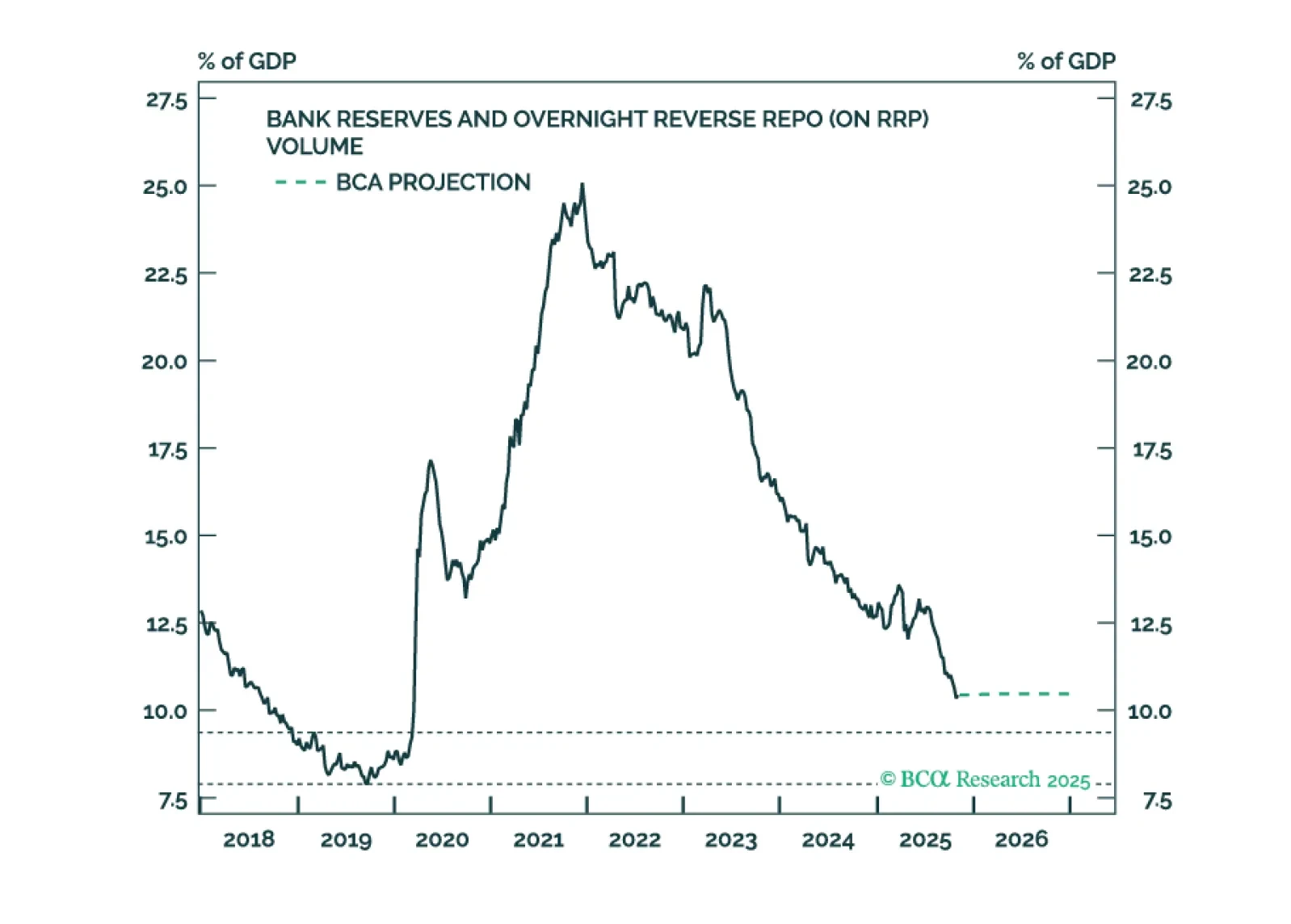

This Special Report outlines the Fed’s balance sheet strategy and the rationale behind it. We also provide updated projections for the major asset and liability line items on the Fed’s balance sheet.

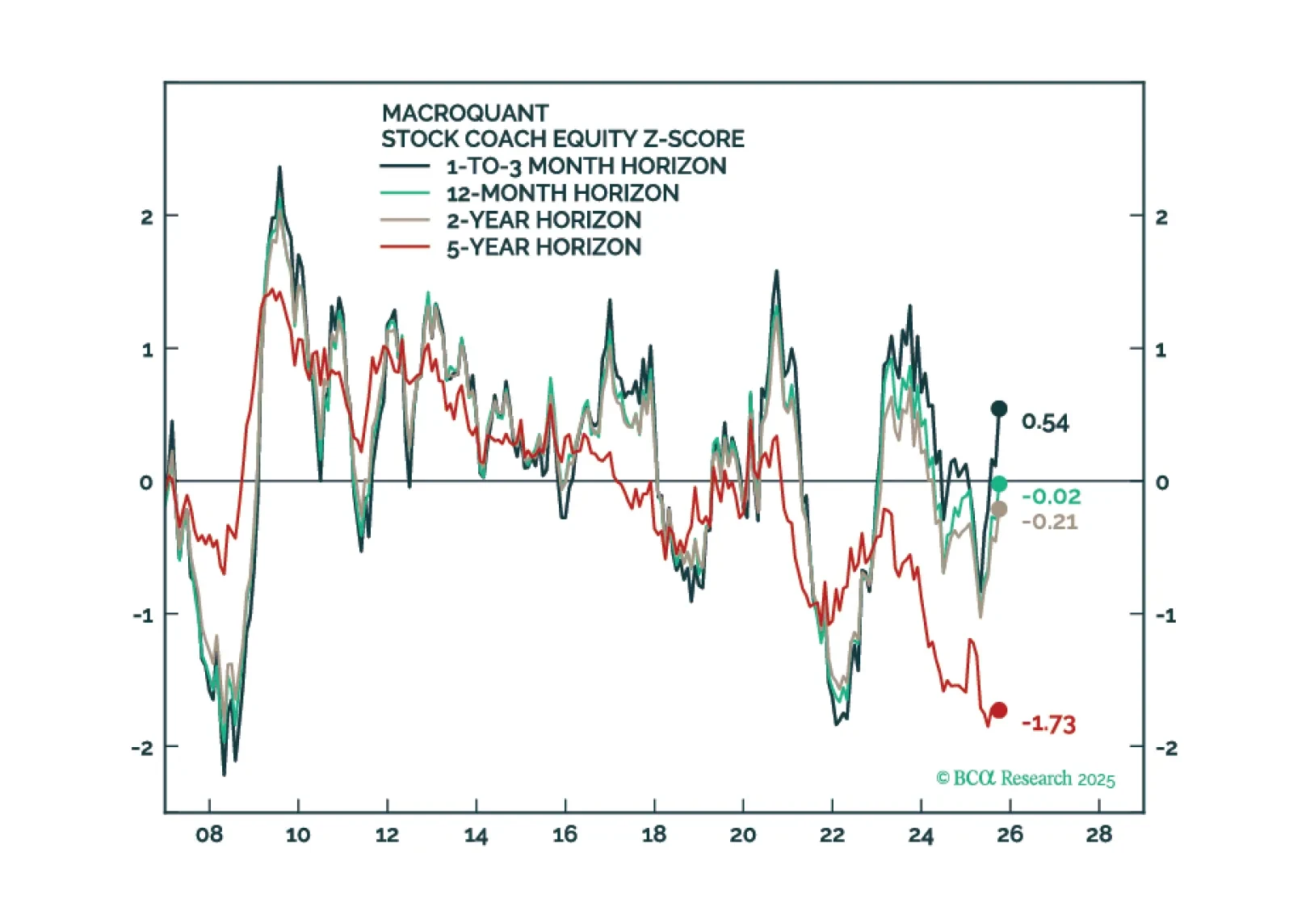

Our Portfolio Allocation Summary for November 2025.

MacroQuant is tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold and copper.

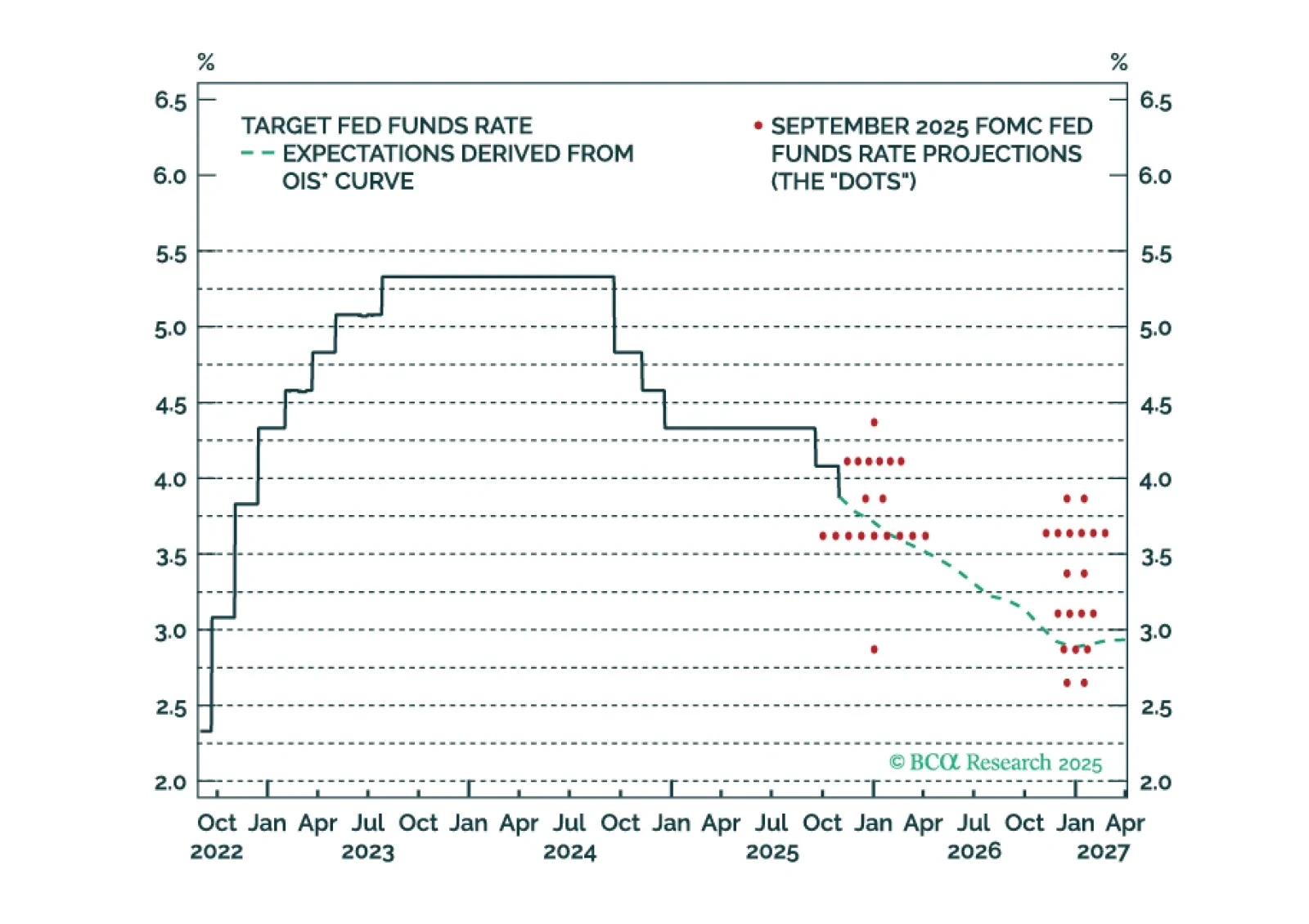

The Fed cut rates today, but a follow-up rate cut in December is uncertain. It will depend, in large part, on who wins a debate about the neutral rate of interest.

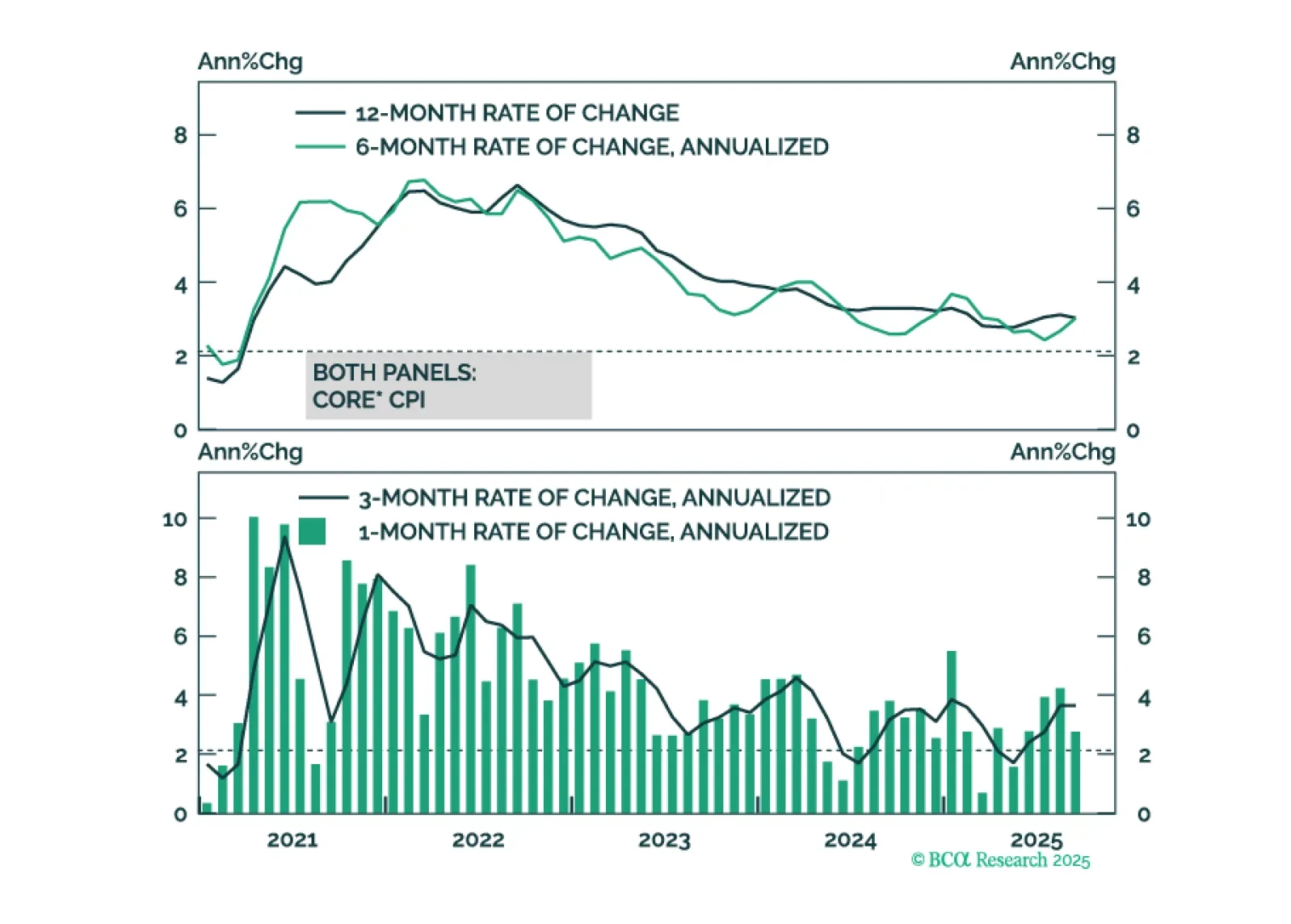

US inflation data continue to show no signs of price pressures beyond a near-term tariff effect.

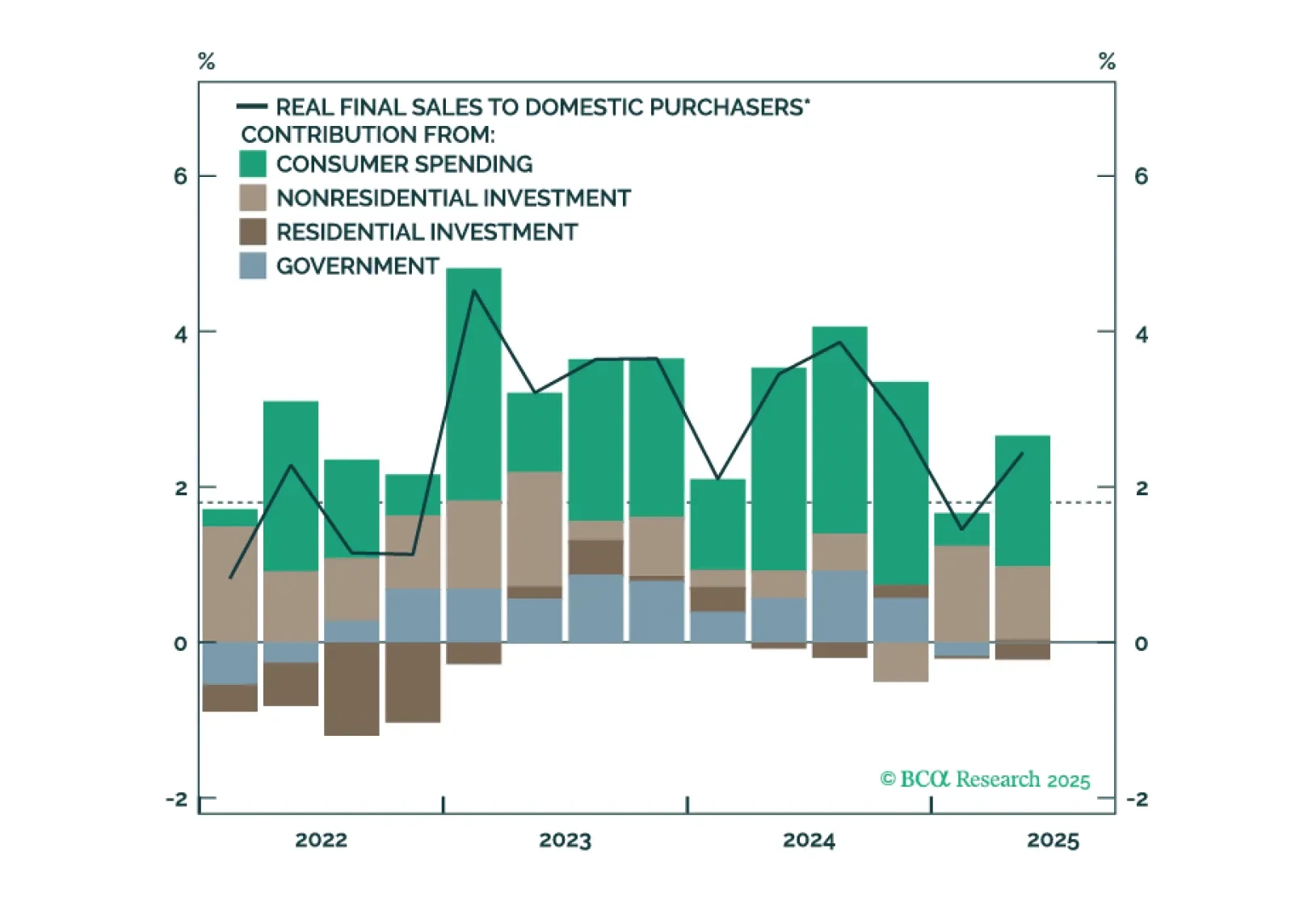

The Fed is poised to deliver a 25-basis-point rate cut this month, but a follow-up rate cut in December will depend on how the divergence between strong consumer spending and weak employment growth is resolved.

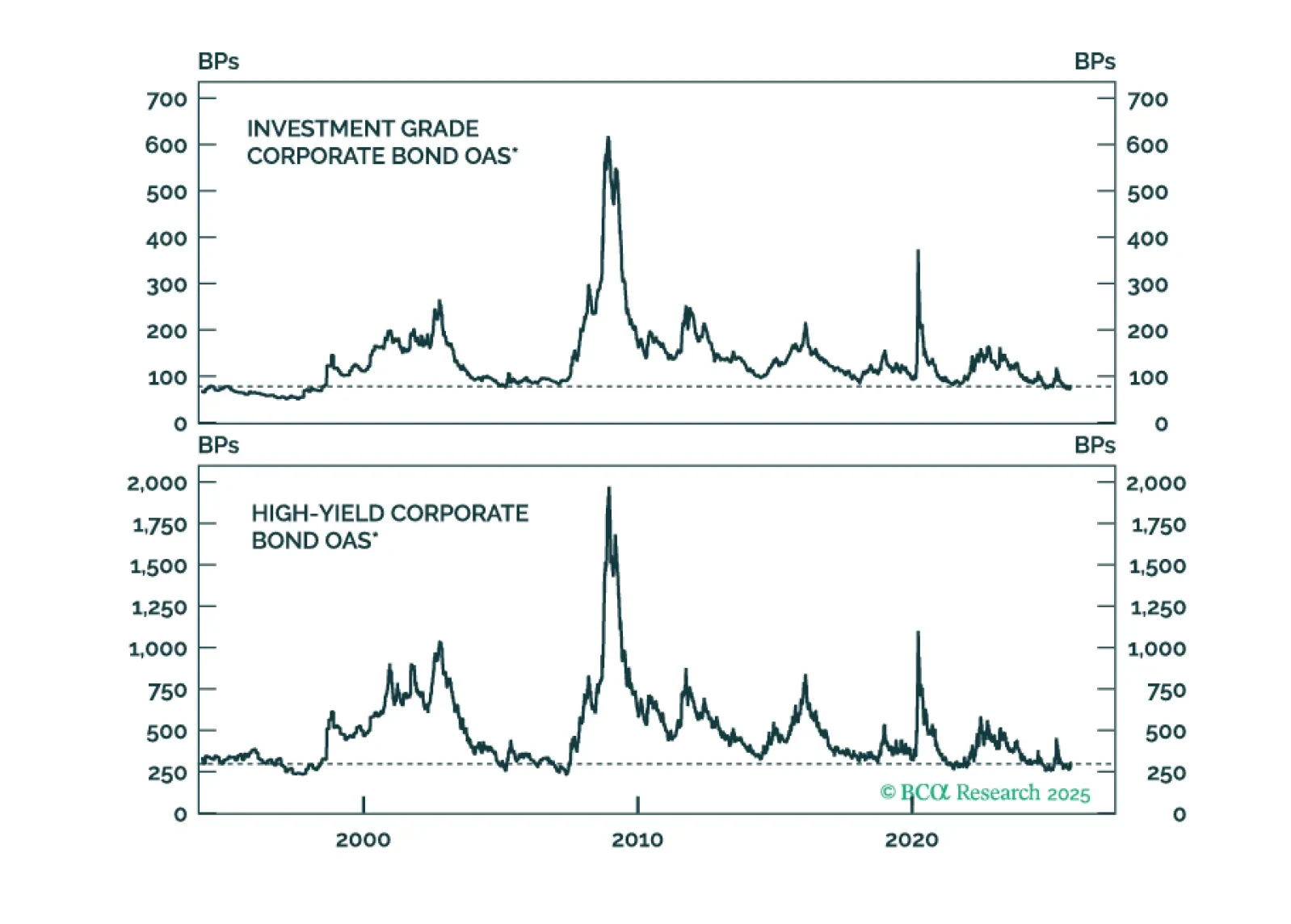

This week’s Special Report evaluates the reward and risk in corporate bonds. We address the question of whether low expected excess returns today are justified by low risk or an example of overvaluation.