Developed Countries

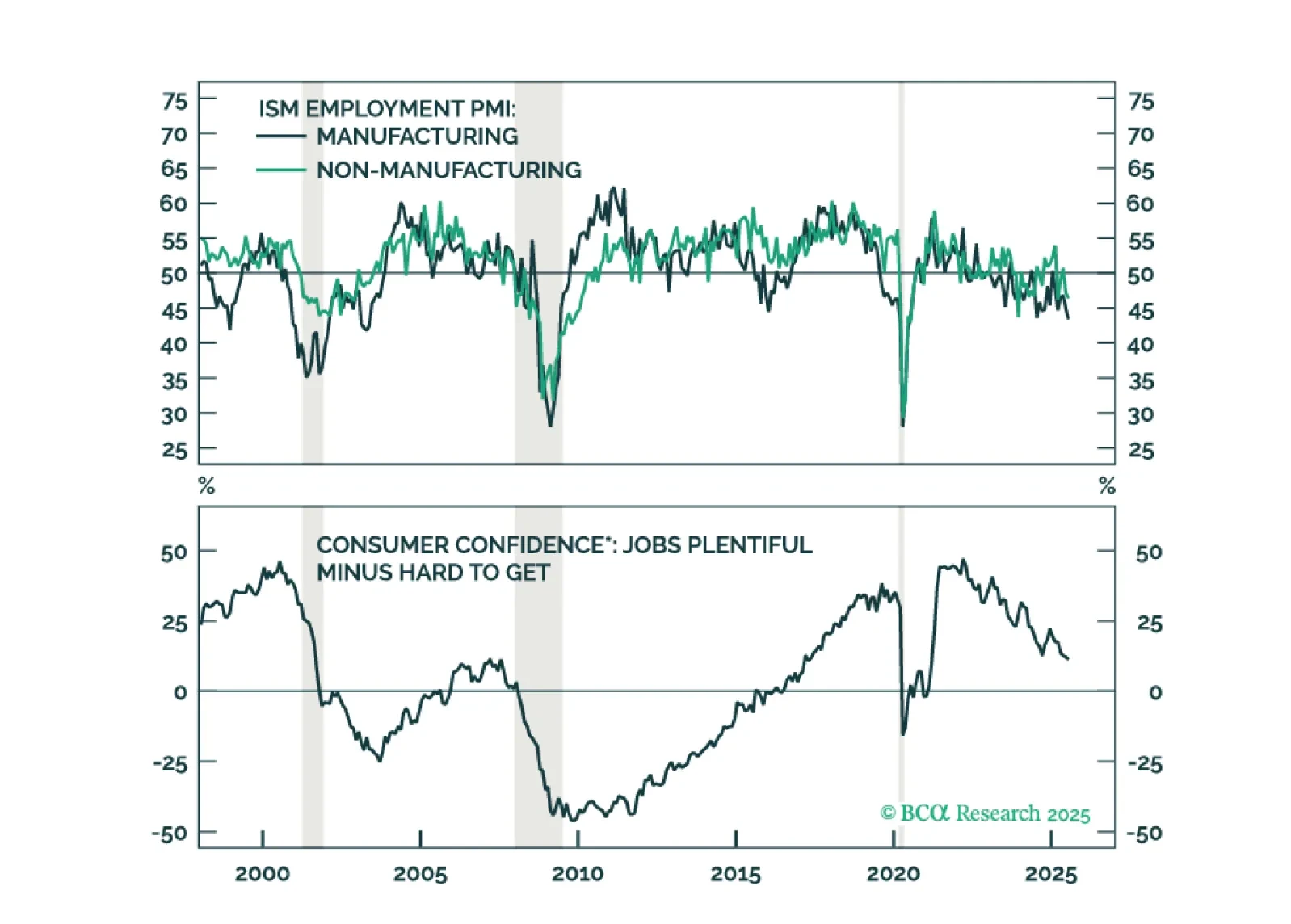

The August employment report showed a modest increase in labor market slack, enough to cement a 25-basis-point rate cut this month.

Our Portfolio Allocation Summary for September 2025.

MacroQuant sees downside risks to stocks over a long-term horizon but is not yet saying that we are at imminent risk of an equity bear market.

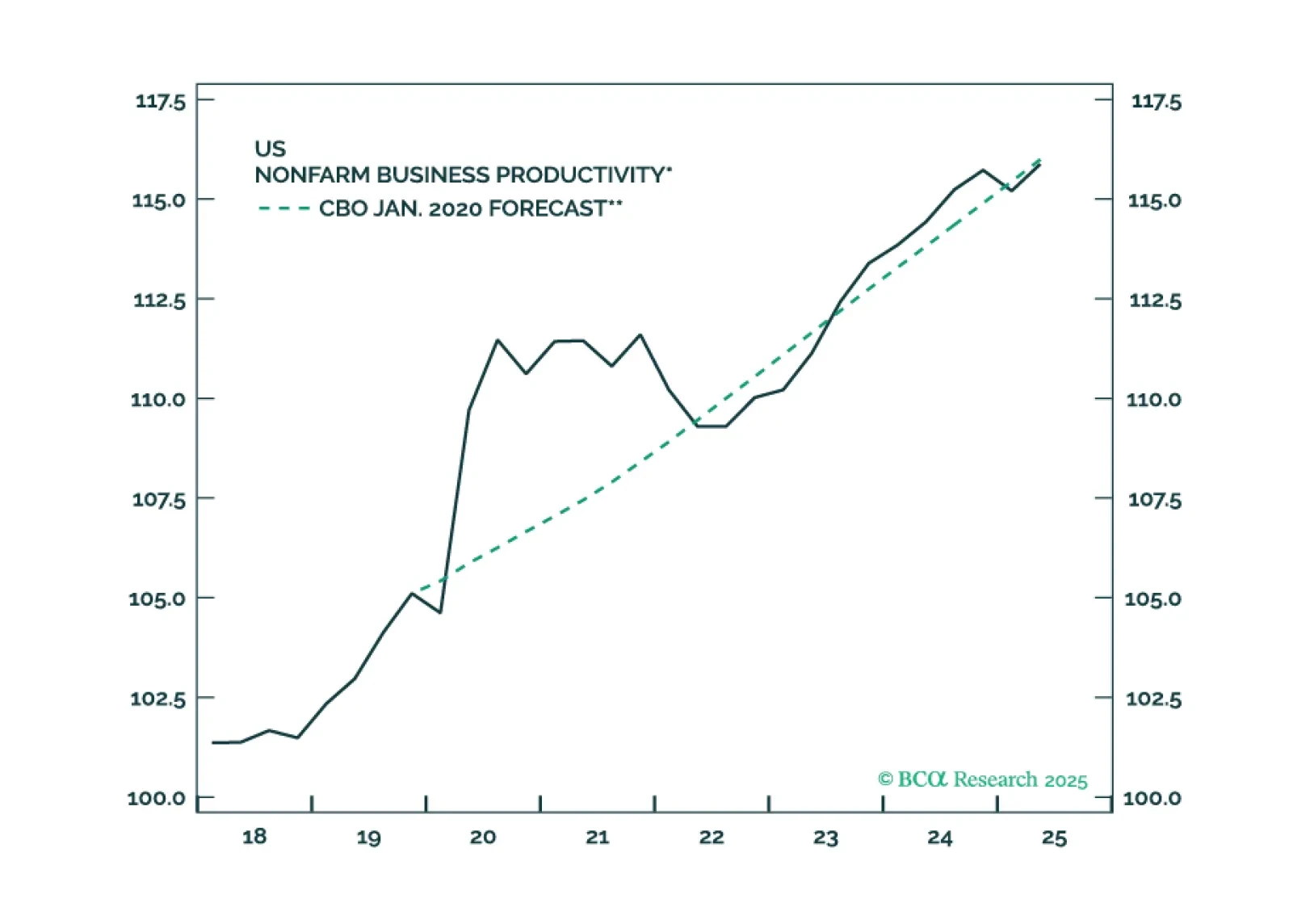

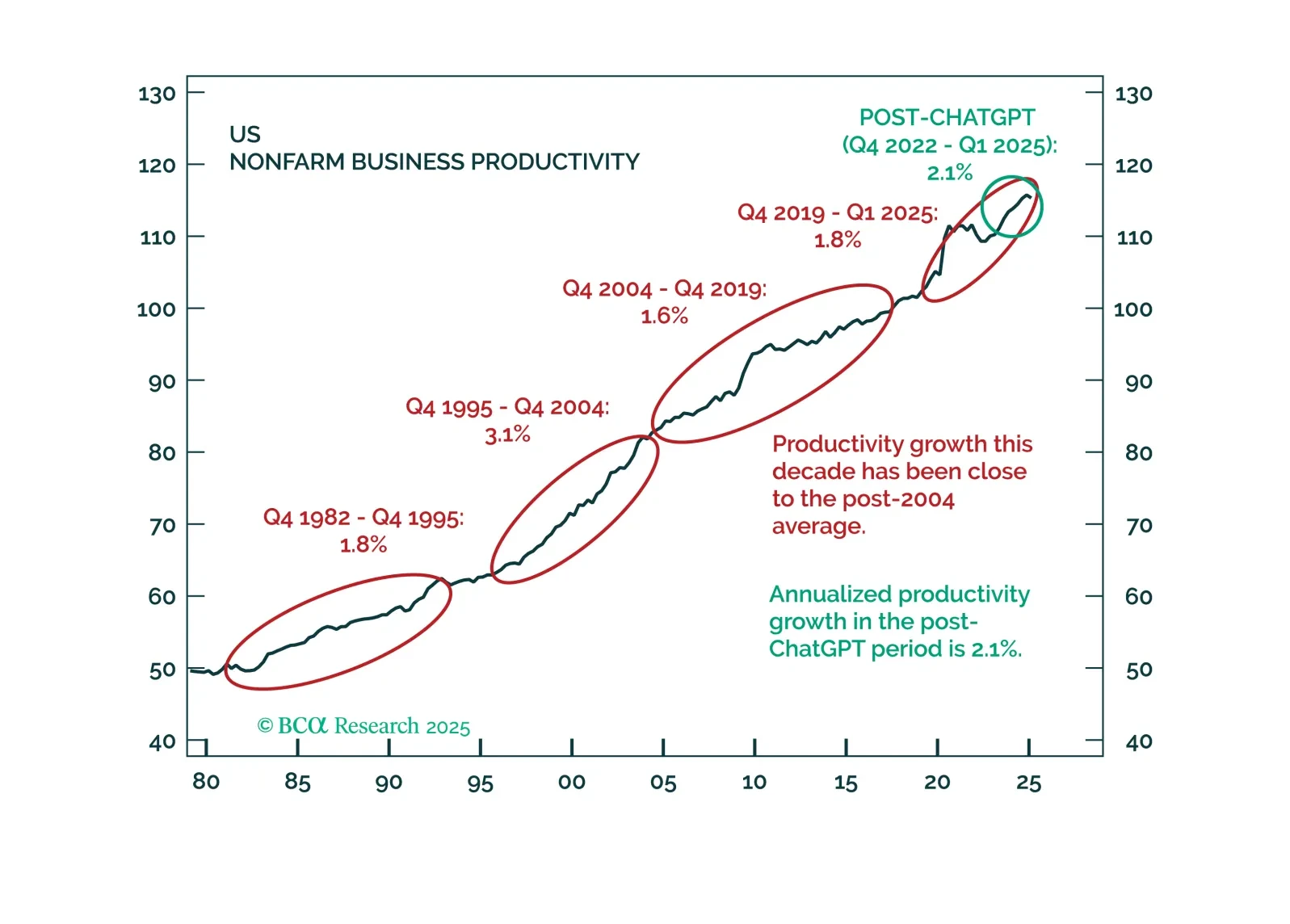

The AI boom has had less of an impact on the economy than widely believed. This may eventually change, but the risk is that investors grow impatient before it does.

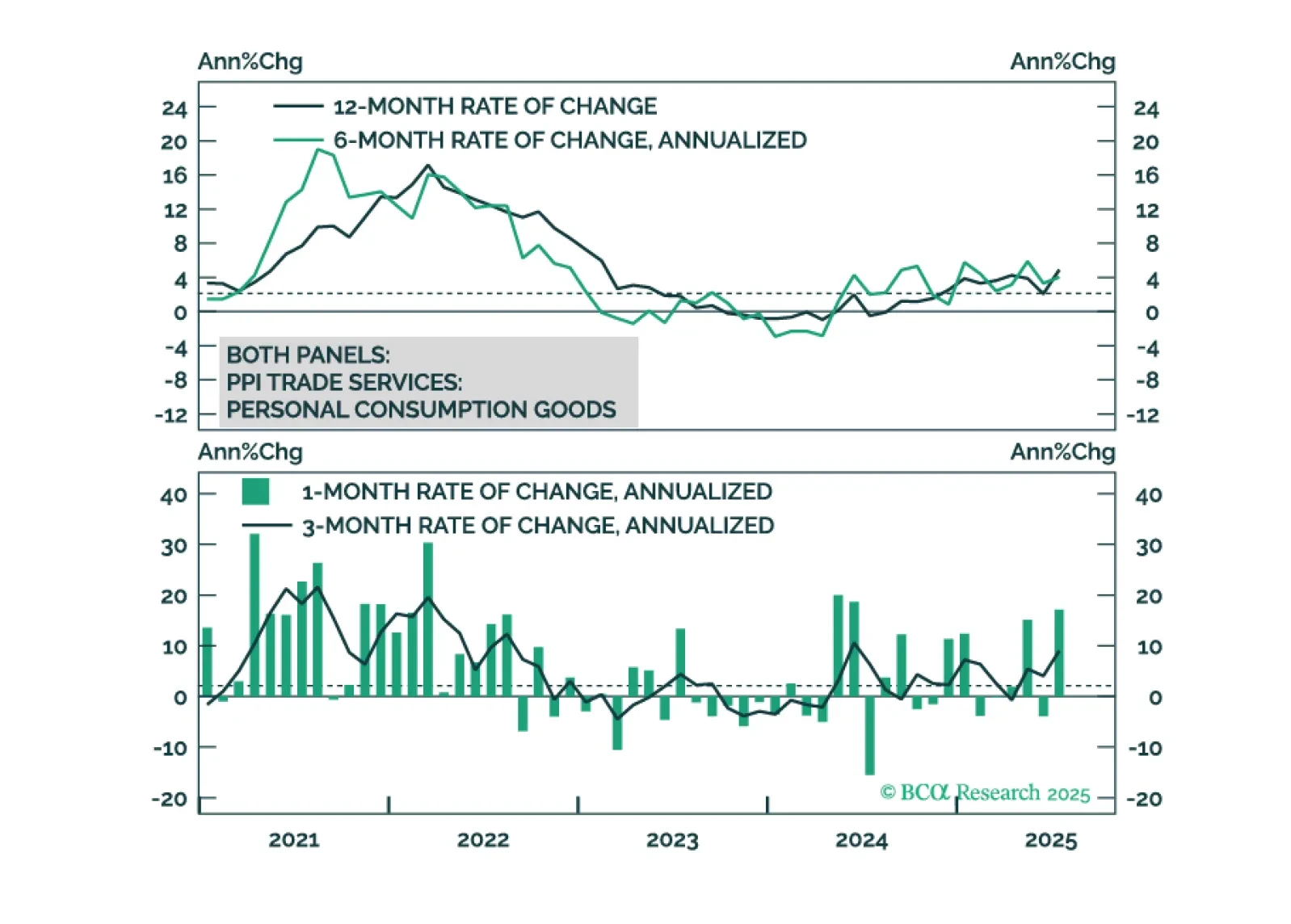

The cost of tariffs is falling on the US consumer, not foreign exporters or US firms.

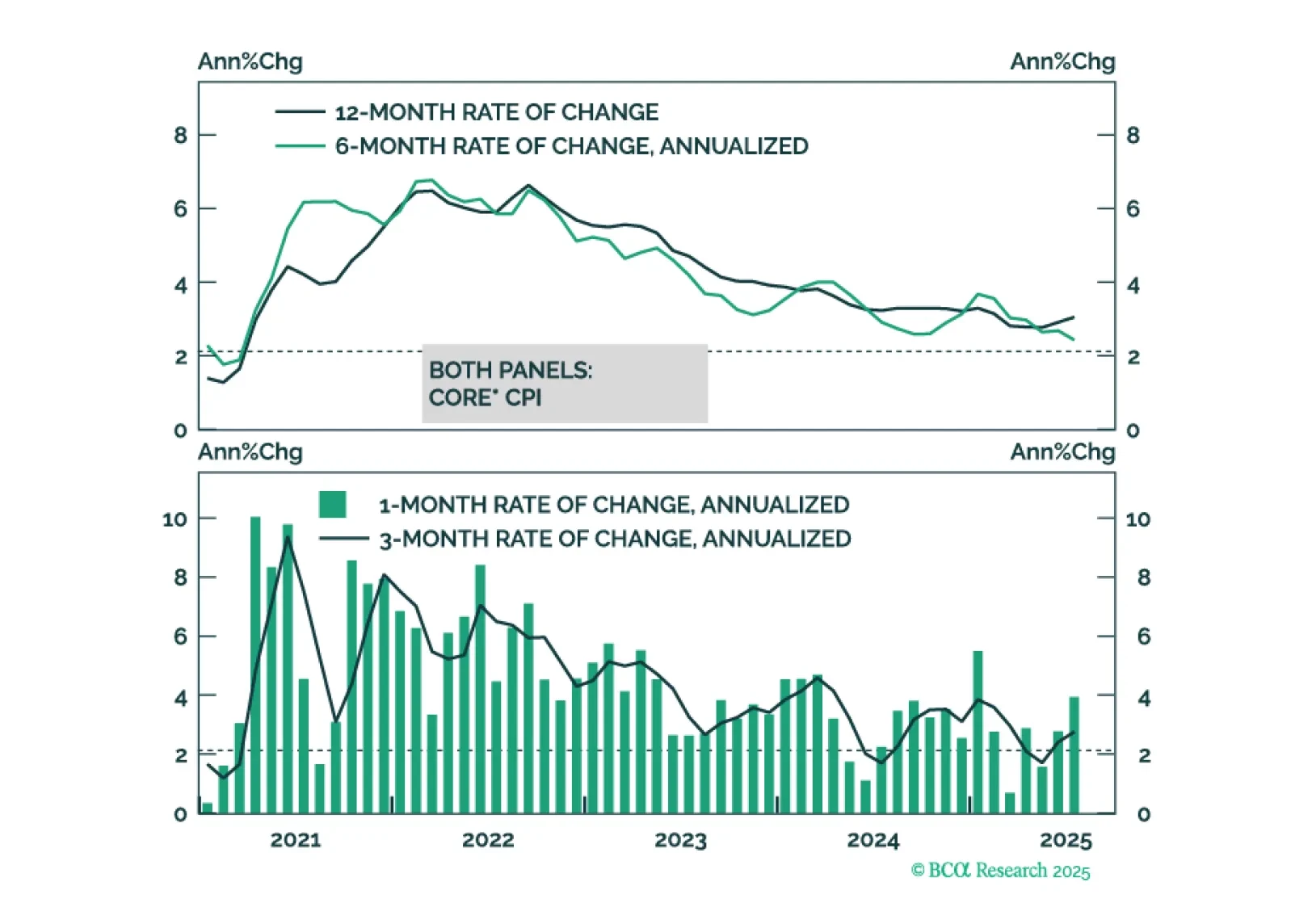

This morning’s CPI report marginally tips the scales in favor of a September rate cut.

Our Portfolio Allocation Summary for August 2025.

We maintain our 12-month US recession probability at 60%. However, until the “whites of the recession’s eyes” are more clearly visible, we would refrain from moving to a fully defensive stance.