Domestic Politics

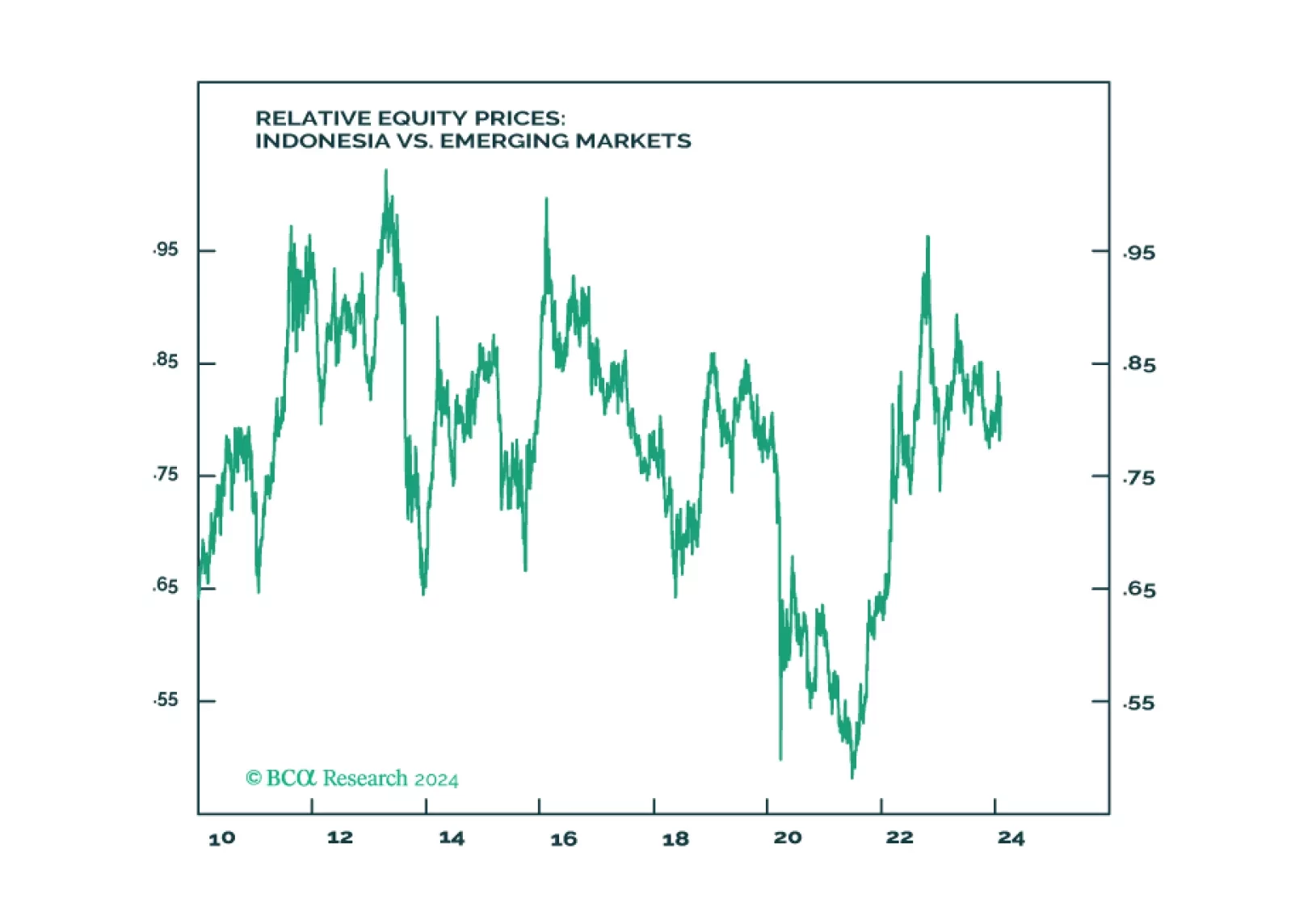

Indonesia will not revert to dictatorship. Yet the guardrails against authoritarianism are also constraining the actions of the next government in tackling near term domestic and regional challenges. For long-term positioning, use potential selloff from a “dictatorship scare” to build position as structural outlook for Indonesia is positive due to the China-West divorce and the global energy transition.

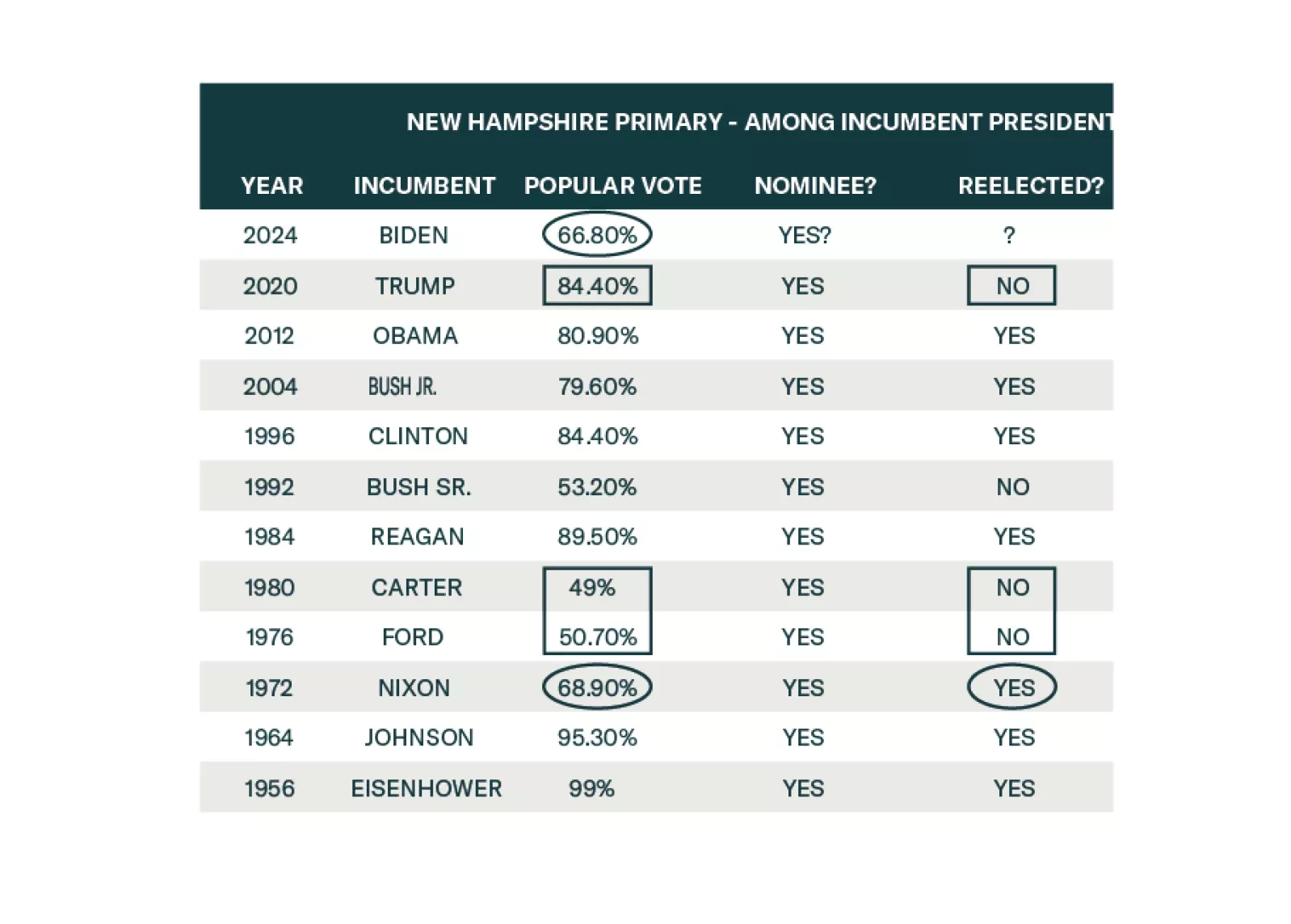

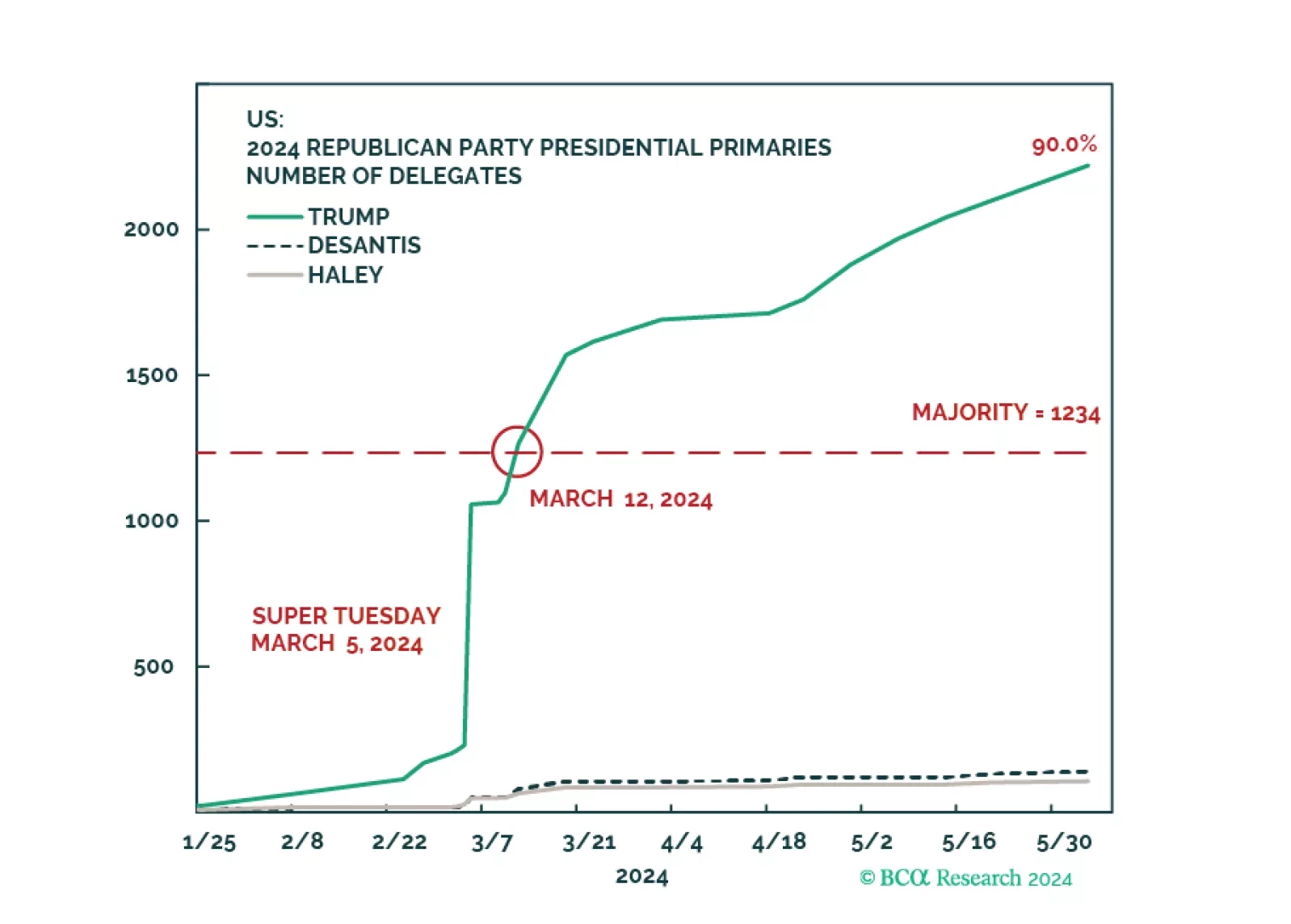

The US primary election is effectively over. The Biden-Trump rematch – our base case since 2022 – is all but set in stone. Only a health issue or freak incident could change that now.

Middle East conflict, extreme US policy uncertainty, Chinese economic slowdown, US-Russian proxy war, and Asian military conflicts do not create a stable investment backdrop for 2024. Our top five “black swan” risks may be highly improbable, but they stem from these underlying trends.

The market will eventually be forced to react to rising odds of a sharp US national policy reversal. Investors should overweight government bonds and defensive equity sectors.

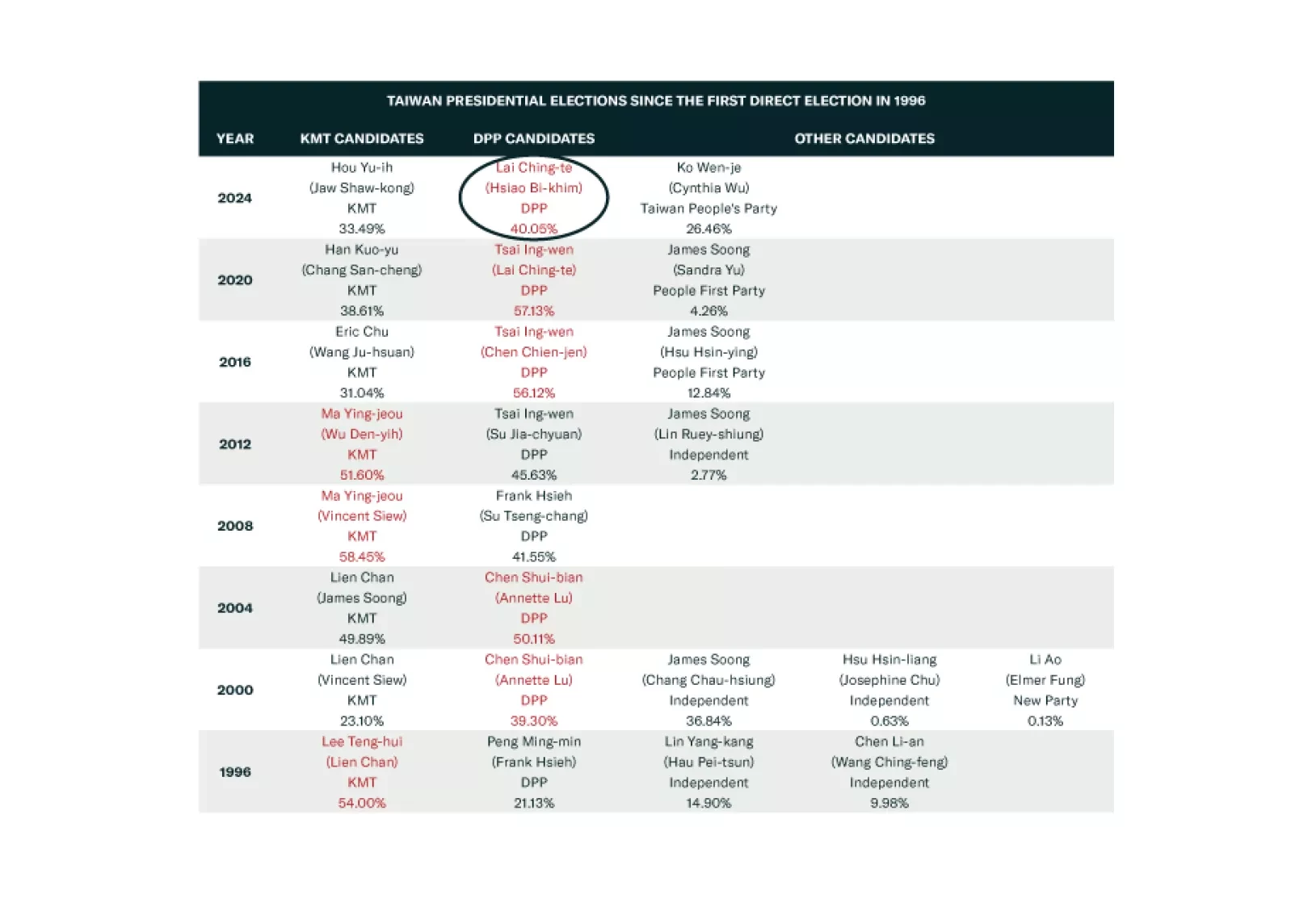

Taiwan’s election will lead to serious Chinese military and economic pressure but not full-scale war. War is a long-term concern. Investors should short TWD-USD.

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.

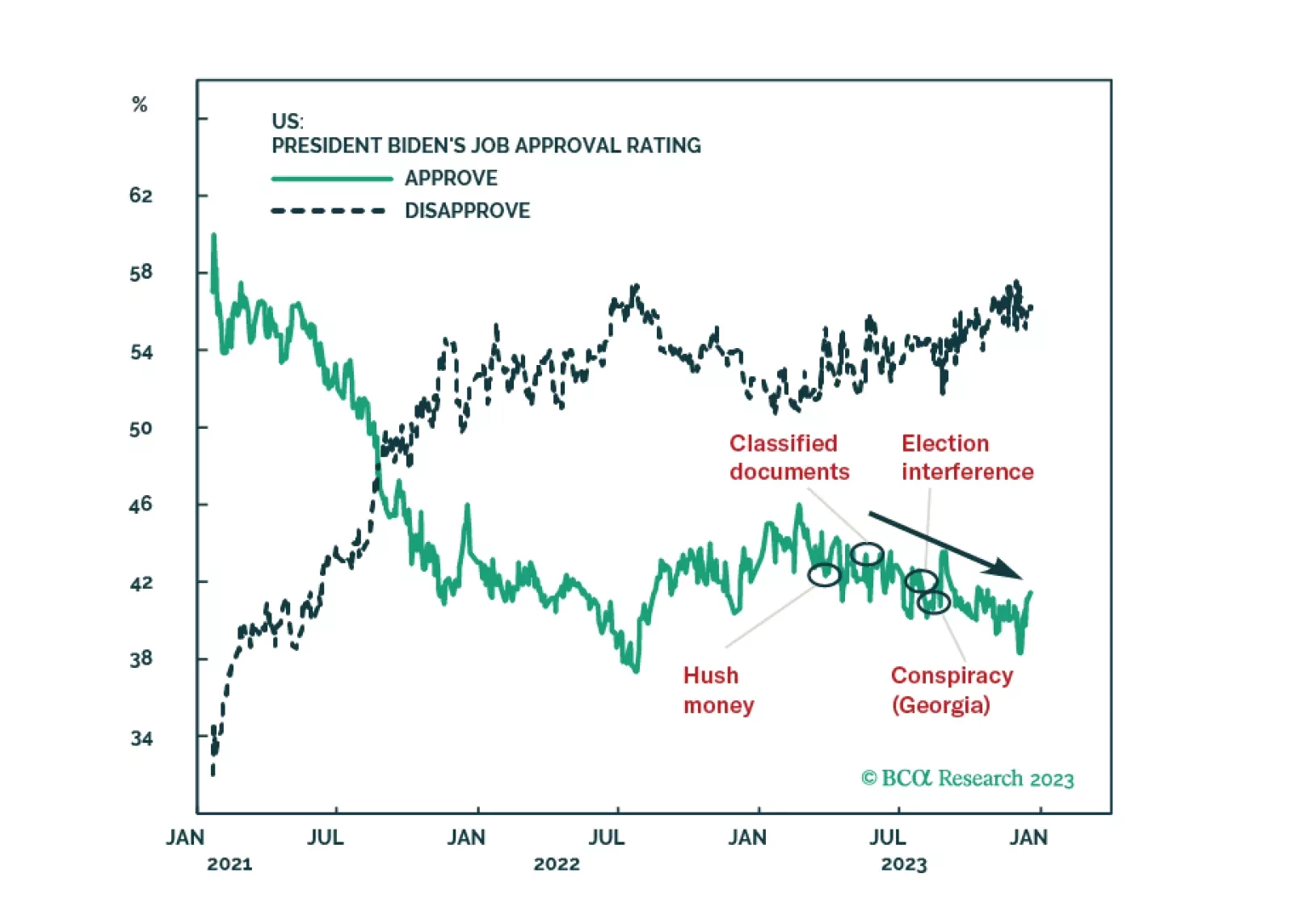

The Republican Party’s odds of winning the 2024 election will benefit, if anything, from state courts’ attempts to exclude President Trump from primary or general election ballots. Higher odds of a change of ruling party will increase stock and bond market volatility.