Economic Growth

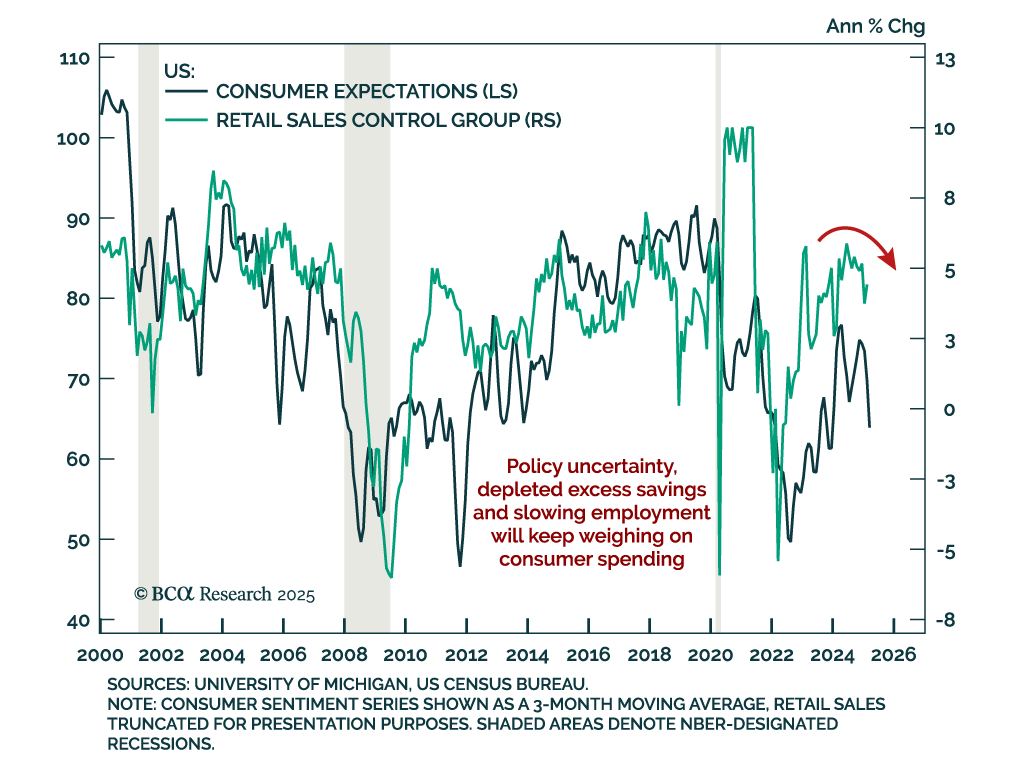

Households’ healthy balance sheets do not square with the rise in credit cards and auto loans delinquencies. The tailwinds that have supported higher-income cohorts’ spending have faded, presaging broad-based deterioration in credit performance.

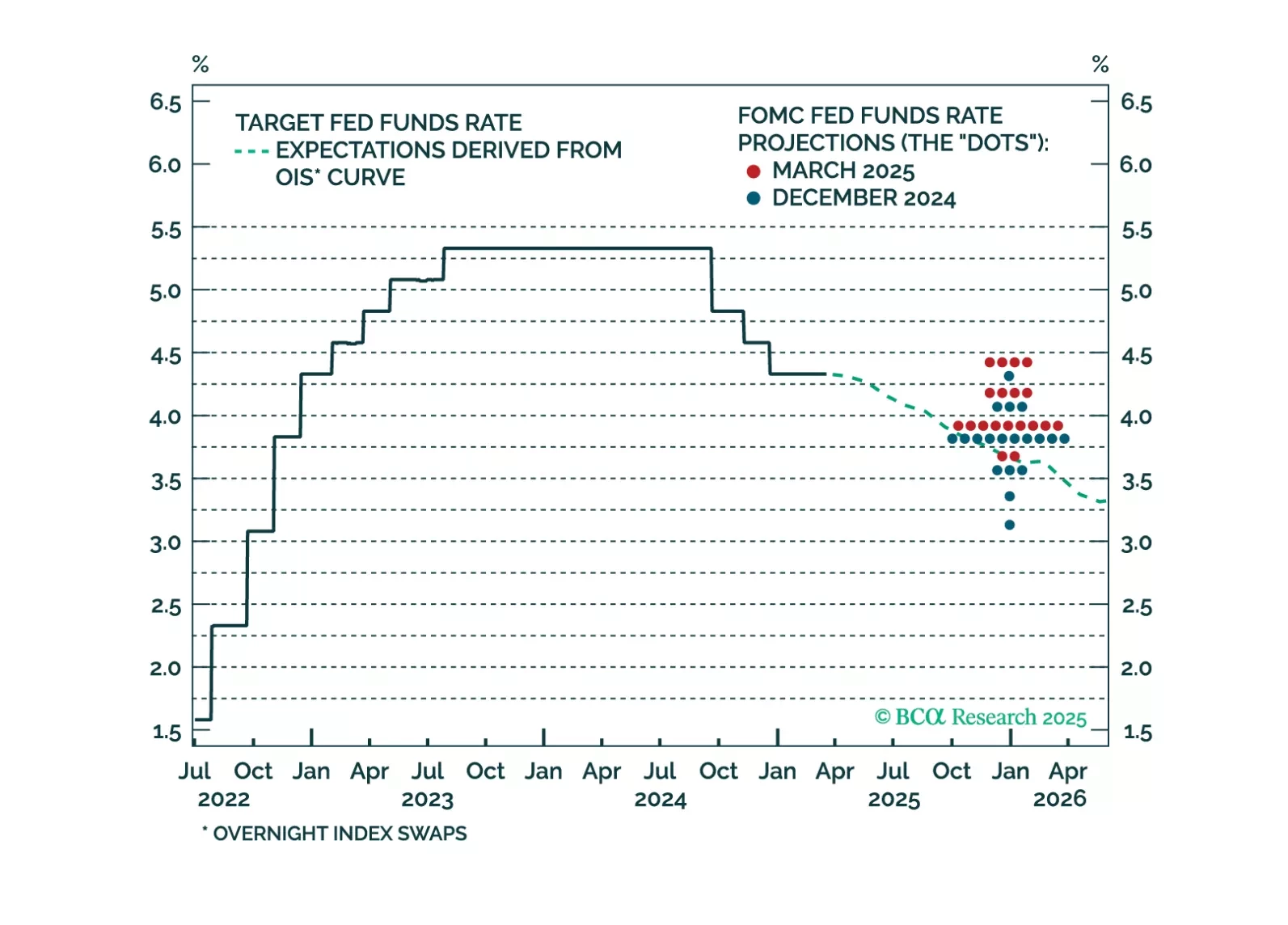

The market reaction to this afternoon’s Fed meeting looks overdone. Investors could be in for a hawkish surprise when it becomes apparent that the Fed won’t ease policy into higher tariff-driven inflation prints.

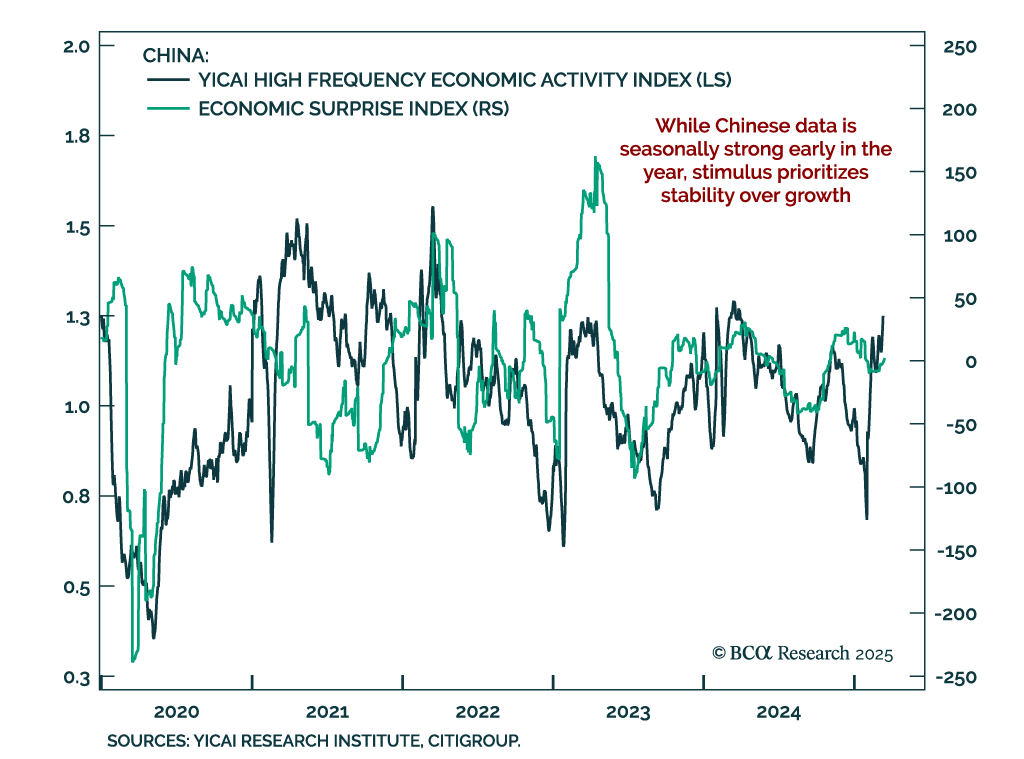

Notwithstanding periodic short-term rebounds, the path of least resistance for global share prices remains down. The resilience of European and Chinese stocks in the face of the US equity selloff is unsustainable. These economies will deteriorate as US demand – the sole pillar of global growth in the past two years – vanishes and tariffs bite. A new currency trade: go long MXN / short an equal-weighted basket of CAD and the euro.