Economic Growth

US job openings declined from a downwardly revised 7.91 million to 7.67 million in July, the lowest level since 2021 and well short of expectations of 8.1 million. The downward revision indicates that labor demand actually declined in June, when it was…

In a widely expected move, the Bank of Canada (BoC) cut interest rates by a quarter of a percentage point for a third consecutive month in September, lowering the benchmark overnight rate to 4.25%. Policymakers also signaled further easing ahead. Both the…

Both leading PMI measures painted a sluggish picture of China’s economic conditions in August. The NBS composite PMI suggested that overall activity barely expanded (50.1) and that the manufacturing sector’s contraction unexpectedly accelerated (49.4 to…

The Q2 2024 earnings season is drawing to a close with 93% of S&P 500 companies having reported results as we go to press. Nearly 80% (60%) of companies have topped earnings (sales) expectations in Q2, according to Factset. Excluding Materials and Real…

The ISM manufacturing PMI improved in August, from 46.8 to 47.2, but remained below expectations of 47.5 and extended a five-month contraction streak. Production declined at a faster pace (45.9 to 44.8) and both new orders and new export orders contracted…

The 2Y/10Y segment of the yield curve is flirting with un-inversion. Aggressive rate cut expectations have largely driven its steepening, with the 2-year Treasury yields falling nearly 100 bps over the past couple of months. Our colleagues at the Bank…

Significantly stronger-than-expected consumer spending growth led to an upward revision to US GDP growth in Q2. That said, gross domestic income (GDI) has been lagging behind GDP. It increased 1.3% q/q in Q2, at the same rate as in Q1, and well below Q2’s…

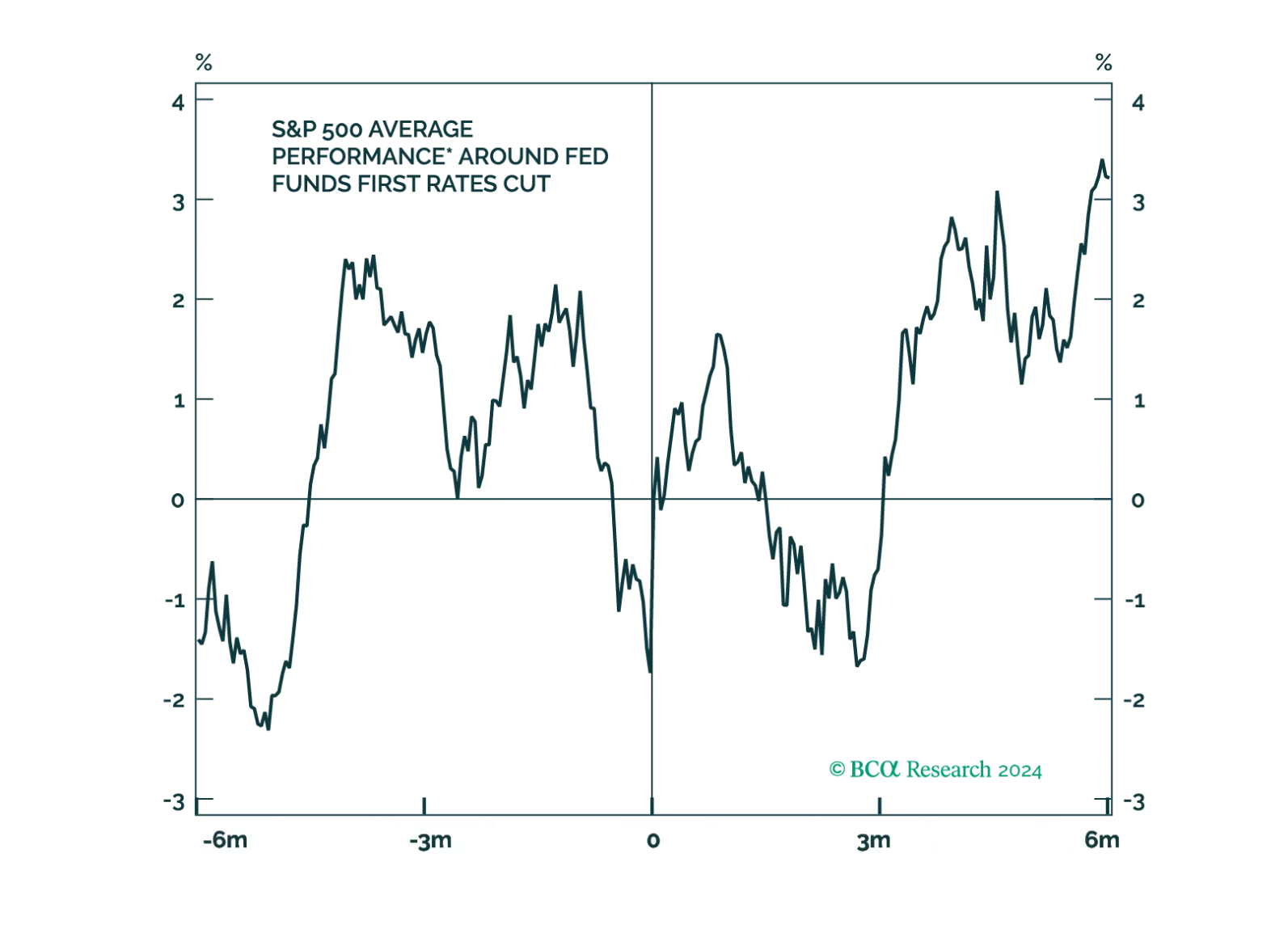

Even after the Fed cuts rates, policy will remain restrictive for some time. Moreover, in history, stocks have tended to fall around the first rate cut. We remain cautious on the outlook for the economy and risk assets.

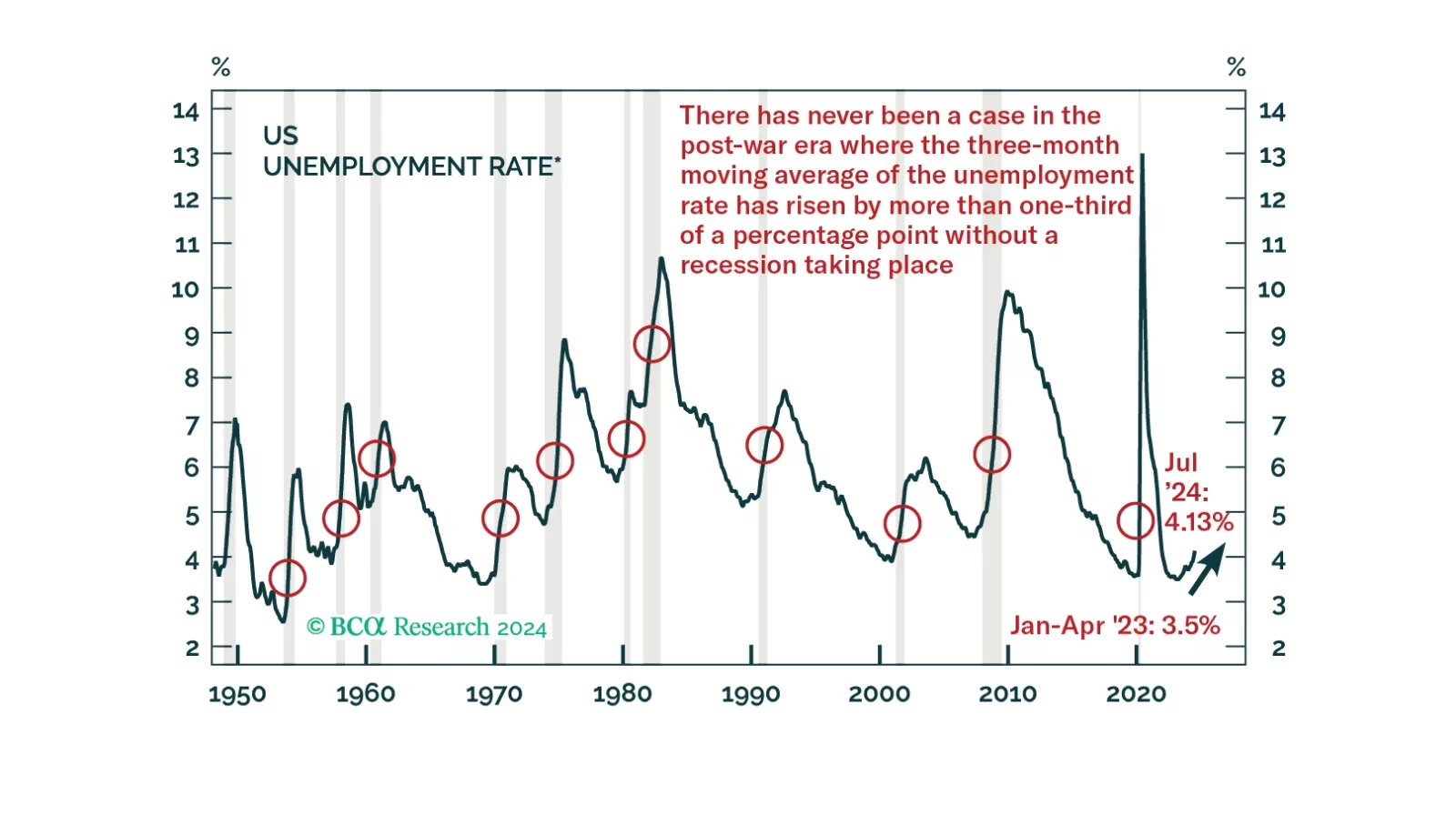

Our annual end-of-summer chartbook report traces the labor market deterioration that led us to downgrade equities at the beginning of August. It also highlights the soft-landing expectations that the credit and equity markets are discounting. We like the risk-reward profile of our newly defensive stance.

After surprising to the upside in July on higher energy costs, Eurozone CPI resumed its deceleration in August. Headline and core CPI declined from 2.6% y/y to 2.2% and from 2.9% to 2.8%, respectively. Energy prices contracted 0.3% y/y from July’s 1.2%…