Economic Growth

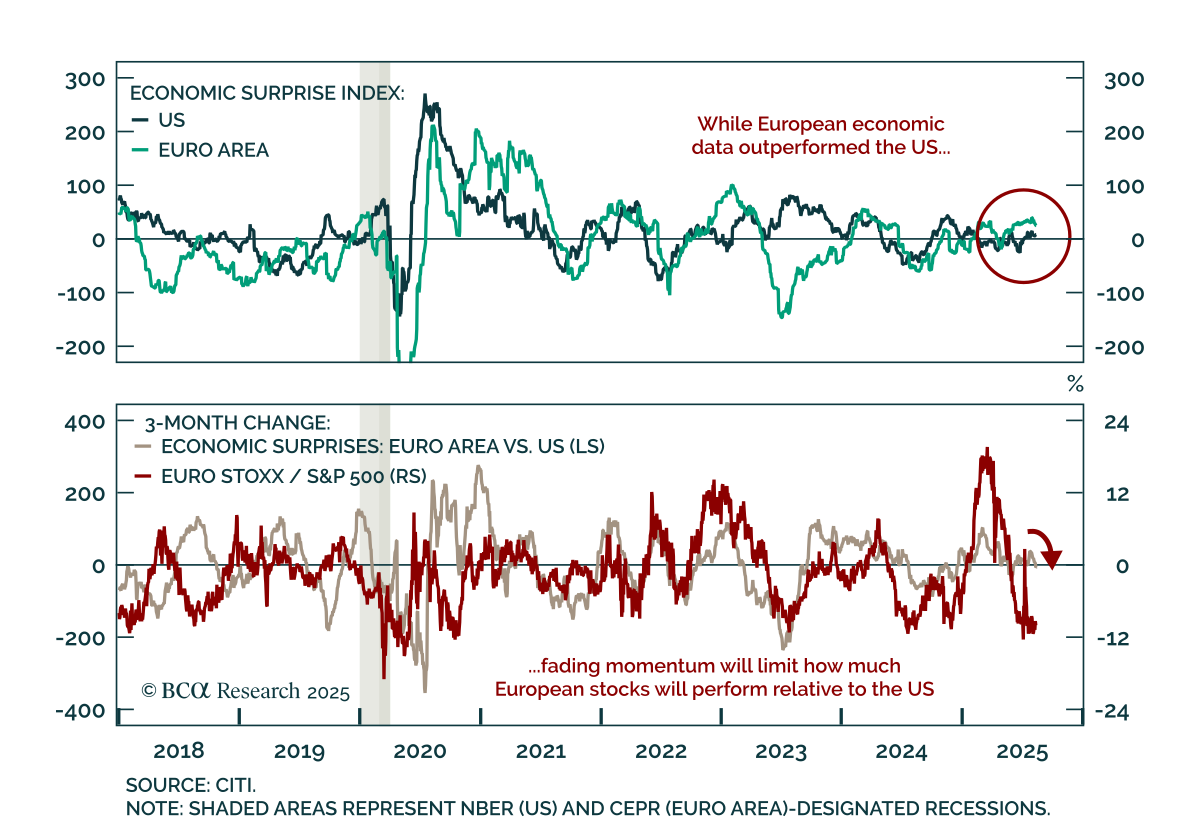

US equities are set for tactical outperformance versus Europe, but dips or underperformance in European assets remain entry points for long-term investors. European stocks have stalled below prior highs, while the S&P 500 has rebounded to record levels…

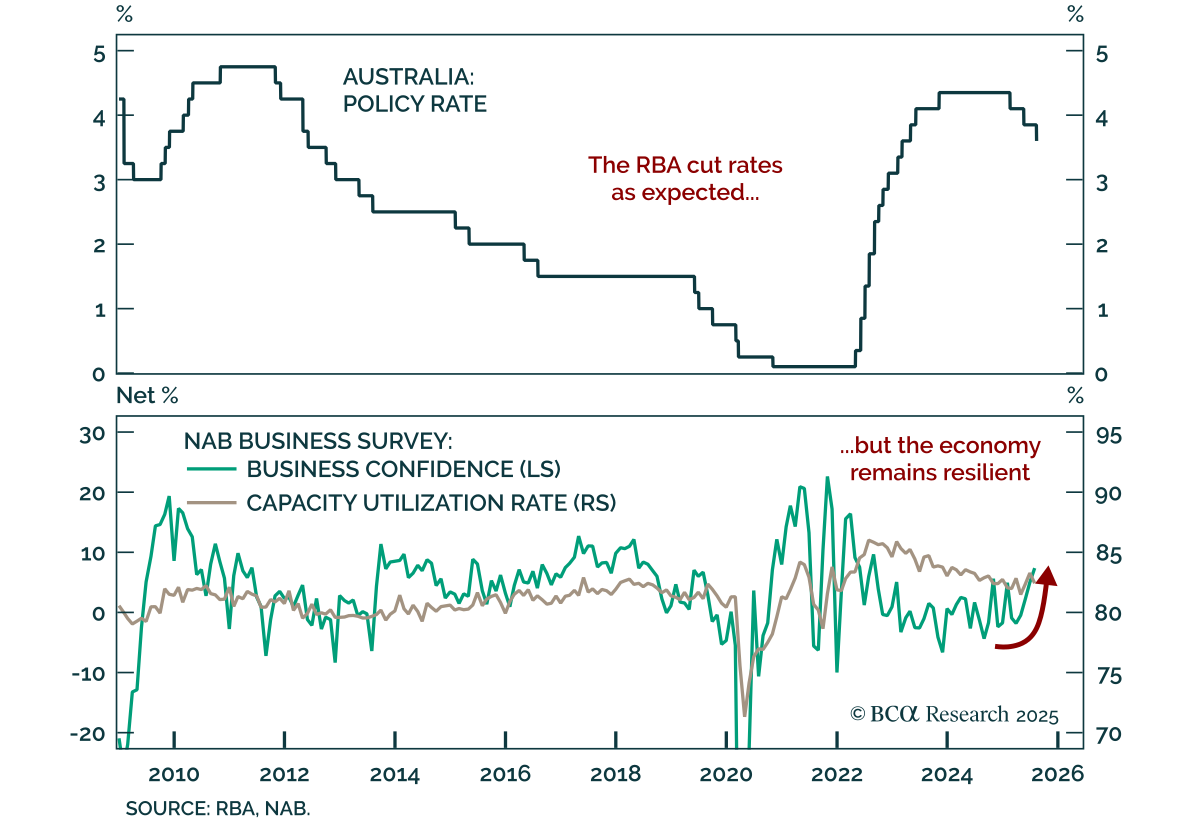

The RBA delivered a widely expected cut to 3.6%, but resilient data warrant an ACGBs underweight. The 25 bps cut was the third this year and Governor Bullock’s guidance was consistent with a cut every other meeting, keeping ACGB yields roughly…

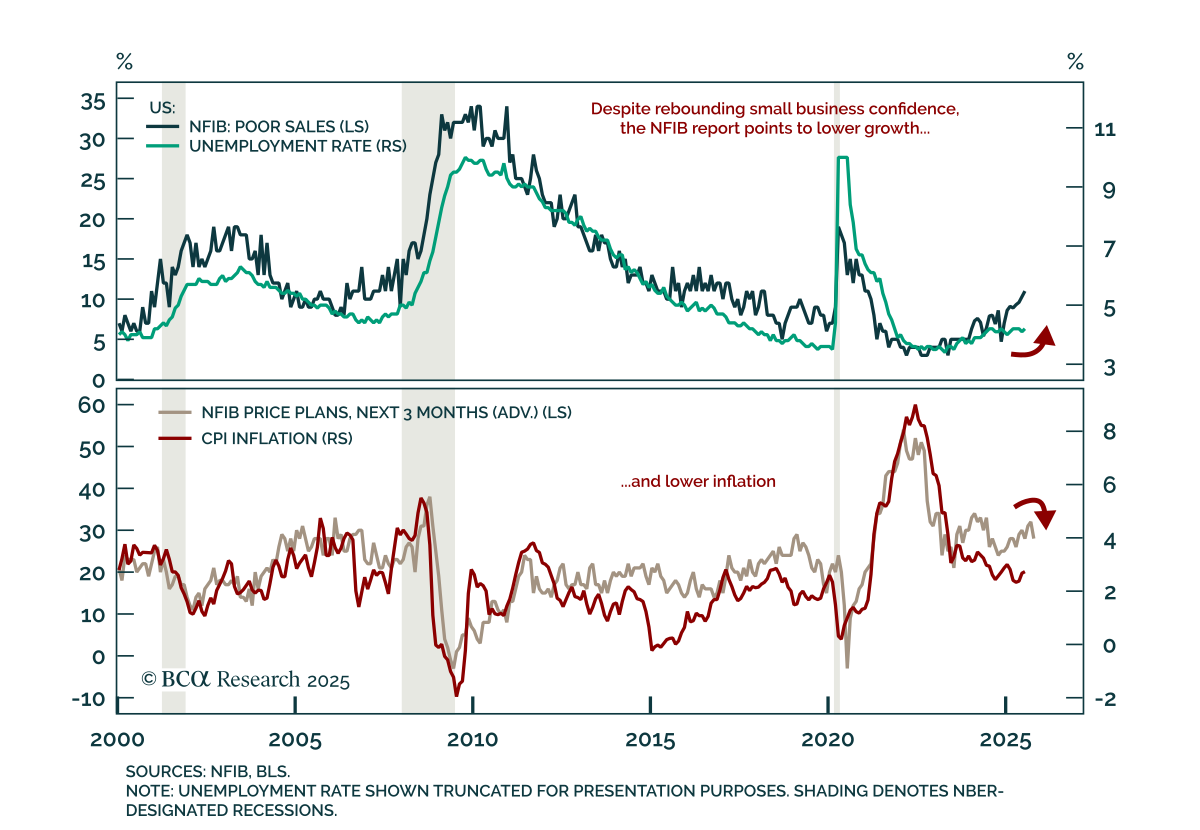

The July NFIB survey showed a rebound in expectations, but underlying weakness reinforces left-tail risks and supports a moderate risk-off allocation. The headline index rose to 100.3, a five-month high, but remains below December 2024 levels. The…

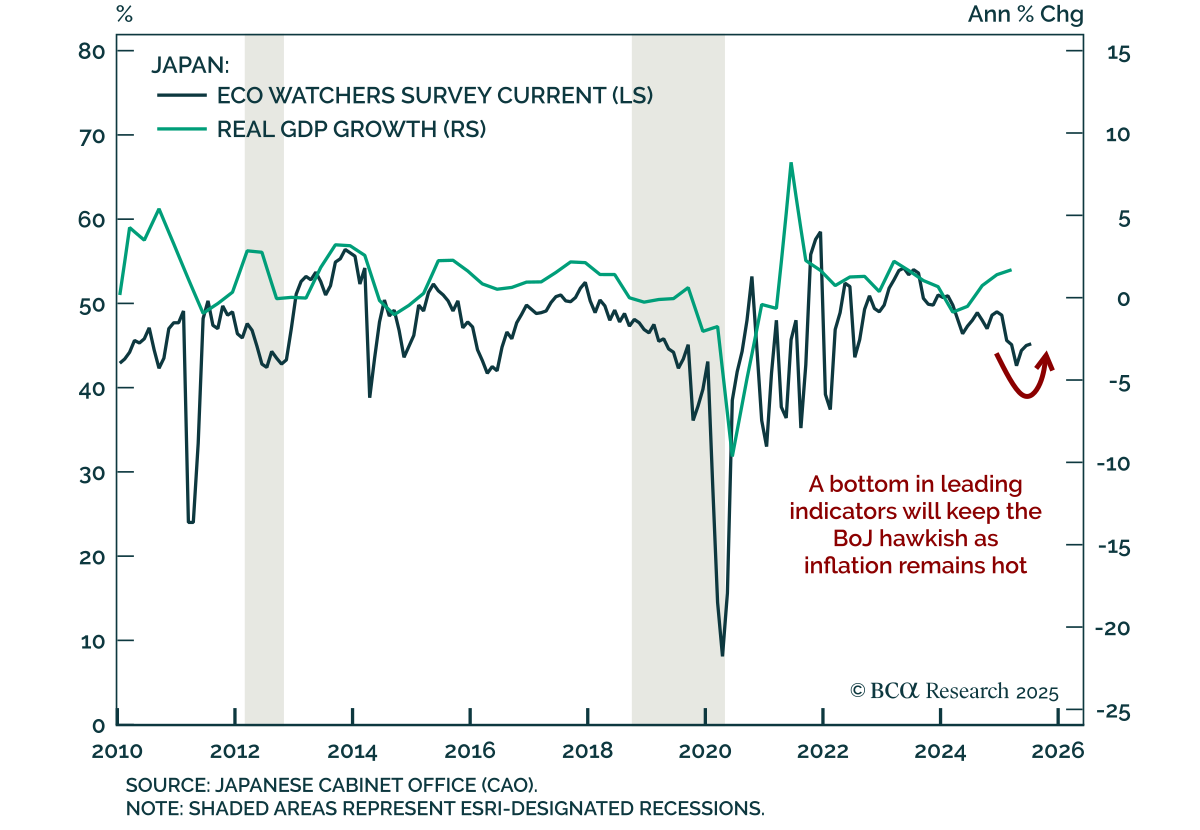

Japan’s Eco Watchers survey suggests growth has troughed, making JGBs vulnerable in both global slowdown and reacceleration scenarios. The July survey showed current conditions ticking up to 45.2 and expectations improving to 47.3. While both remain…

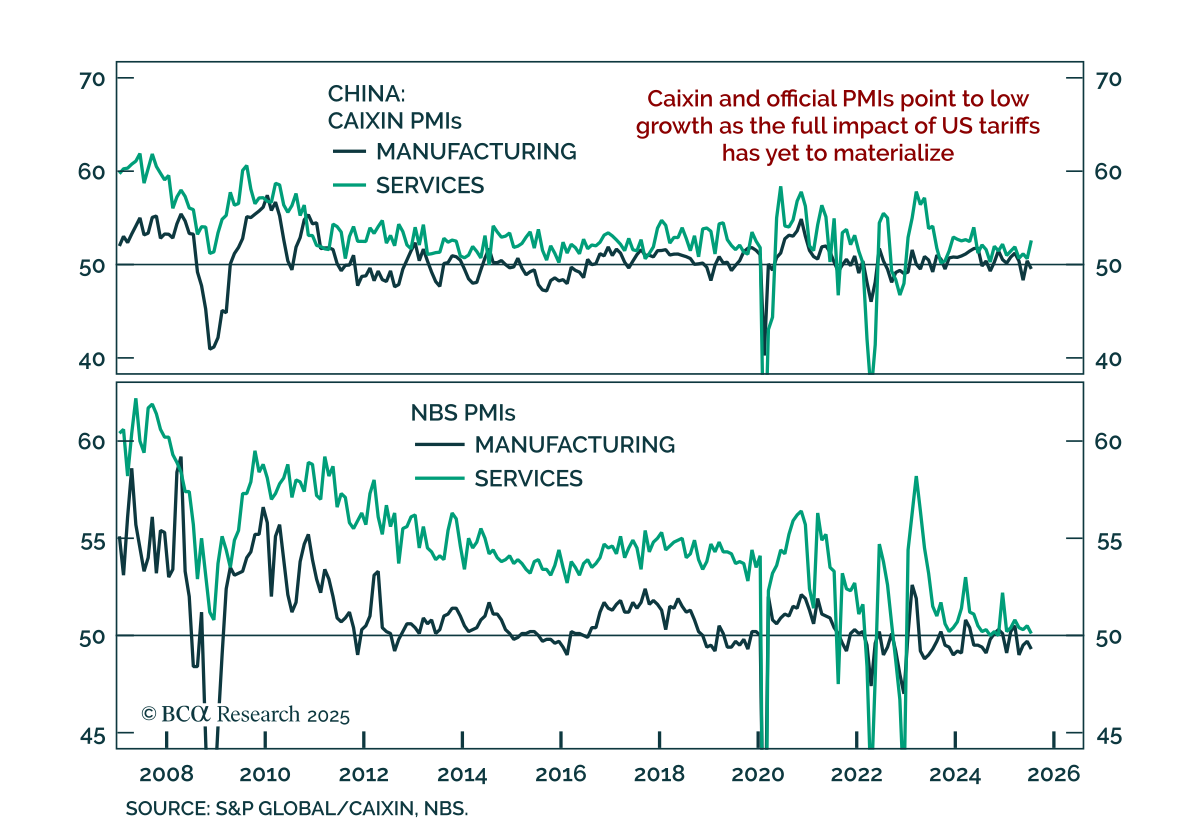

The July PMIs and inflation data confirm that China faces a persistent low-growth, deflationary backdrop, with weak demand and tariff risk warranting defensive equity positioning. The Caixin manufacturing PMI fell to 49.5, while services ticked up at 52.6.…

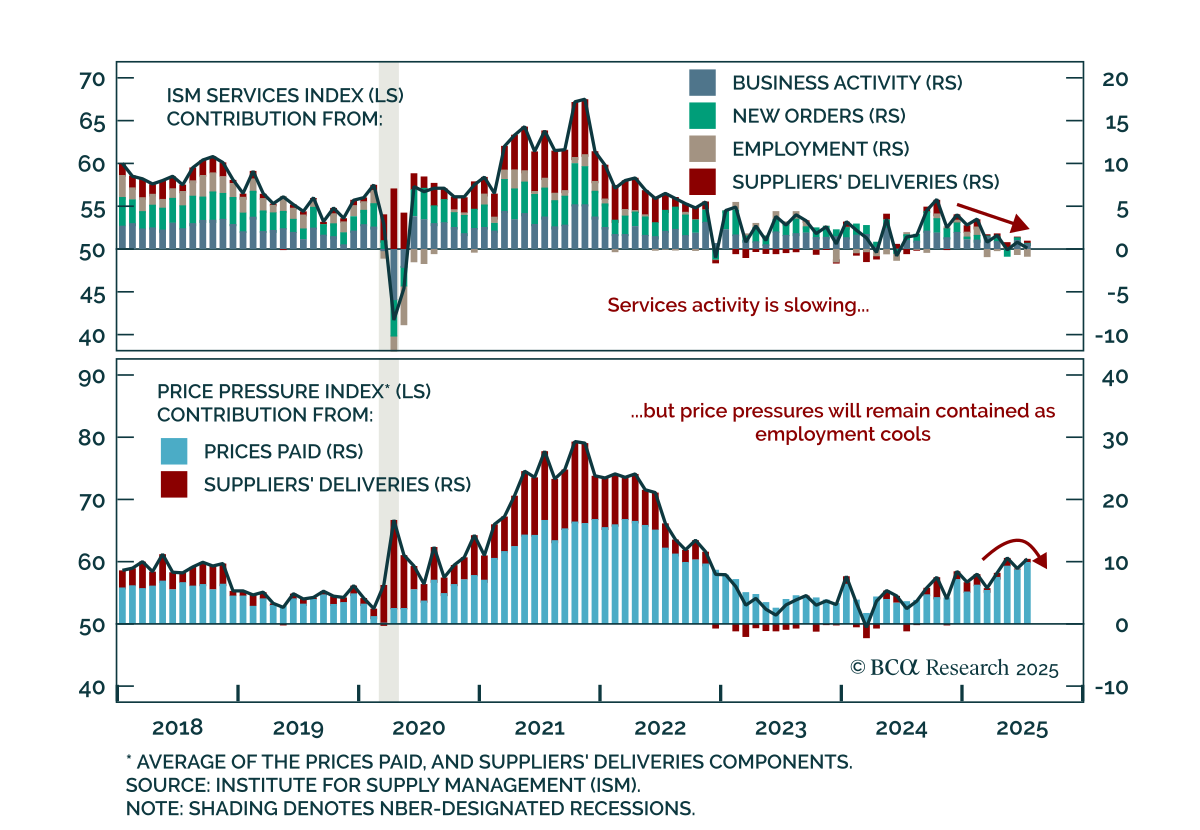

The July ISM Services report showed a stagflationary impulse, but soft labor momentum reinforces the view that price pressures remain contained. The headline index fell to 50.1 from 50.8, missing expectations. New orders softened to 50.3, while employment…

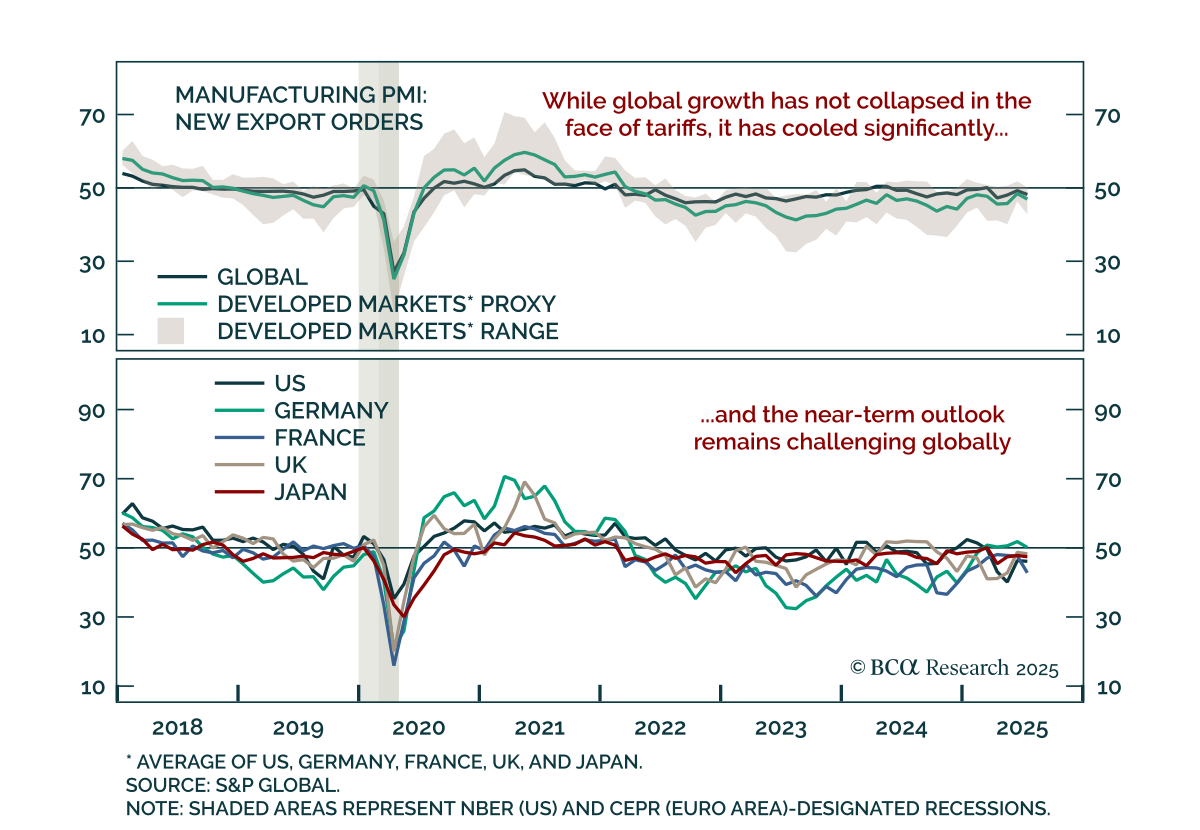

In response to trade uncertainty, global growth is cooling but not collapsing, supporting a cautious near-term view on risk assets. Trade disruption earlier this year raised fears of a global recession, but the data so far point to deceleration, not…

Our Commodity strategists recommend staying short LME copper outright and long gold/short LME copper on a cyclical basis. The unwind in copper, set off by the US tariff exemption on refined metal, is not yet complete. An inventory overhang in the US will…

The S&P 500 recently breached new highs, but narrow leadership and a slowing labor market reinforce caution on risk assets. Equities rebounded from their post-Liberation Day lows, but the rally has been led mostly by the tech sector. The equal-weighted…

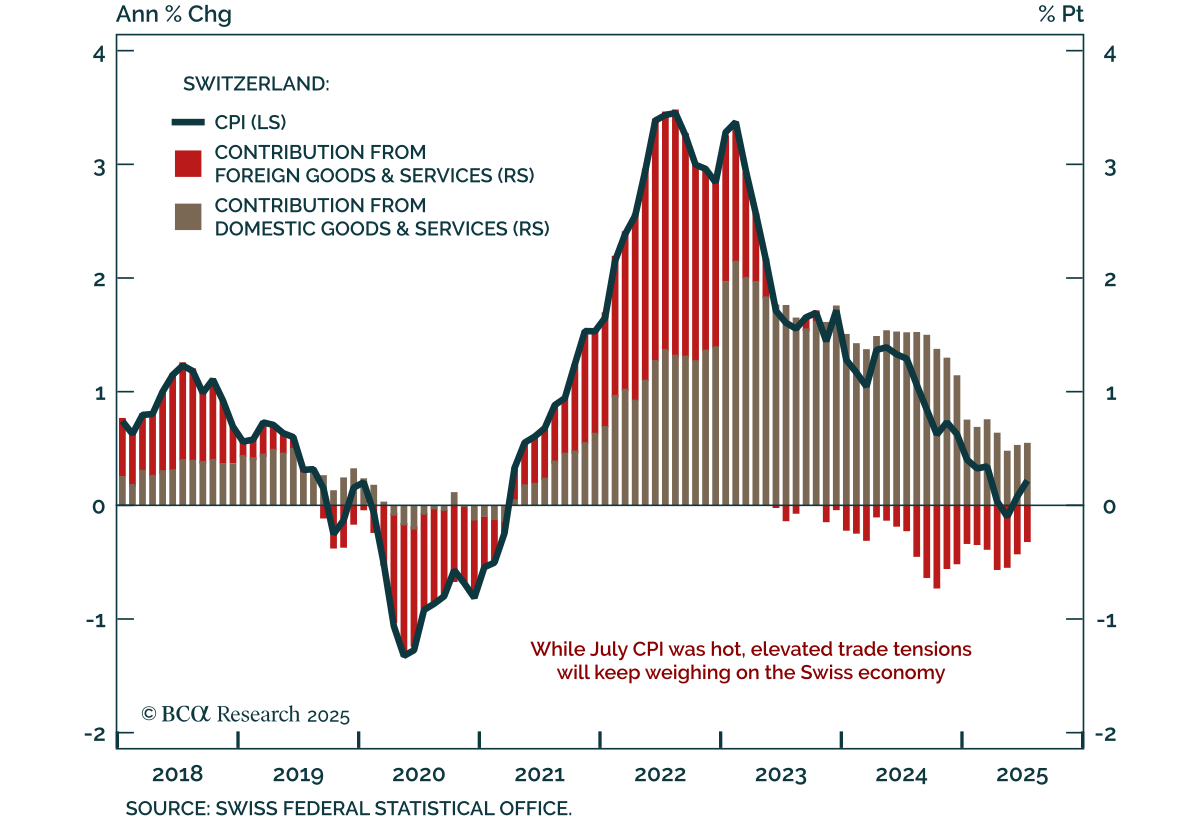

Hot July inflation does little to alter Switzerland’s near-term deflationary outlook, as soft data and trade risks support a defensive stance and preference for bonds over equities. CPI ticked up to 0.2% y/y from 0.1%, with core rising to 0.8%, both…