Economic Growth

We enter 2024 as we were across the last four months of 2023, tactically equal weight across the board until the S&P 500 rally is complete and we gain a better entry point for underweighting equities and overweighting fixed income.

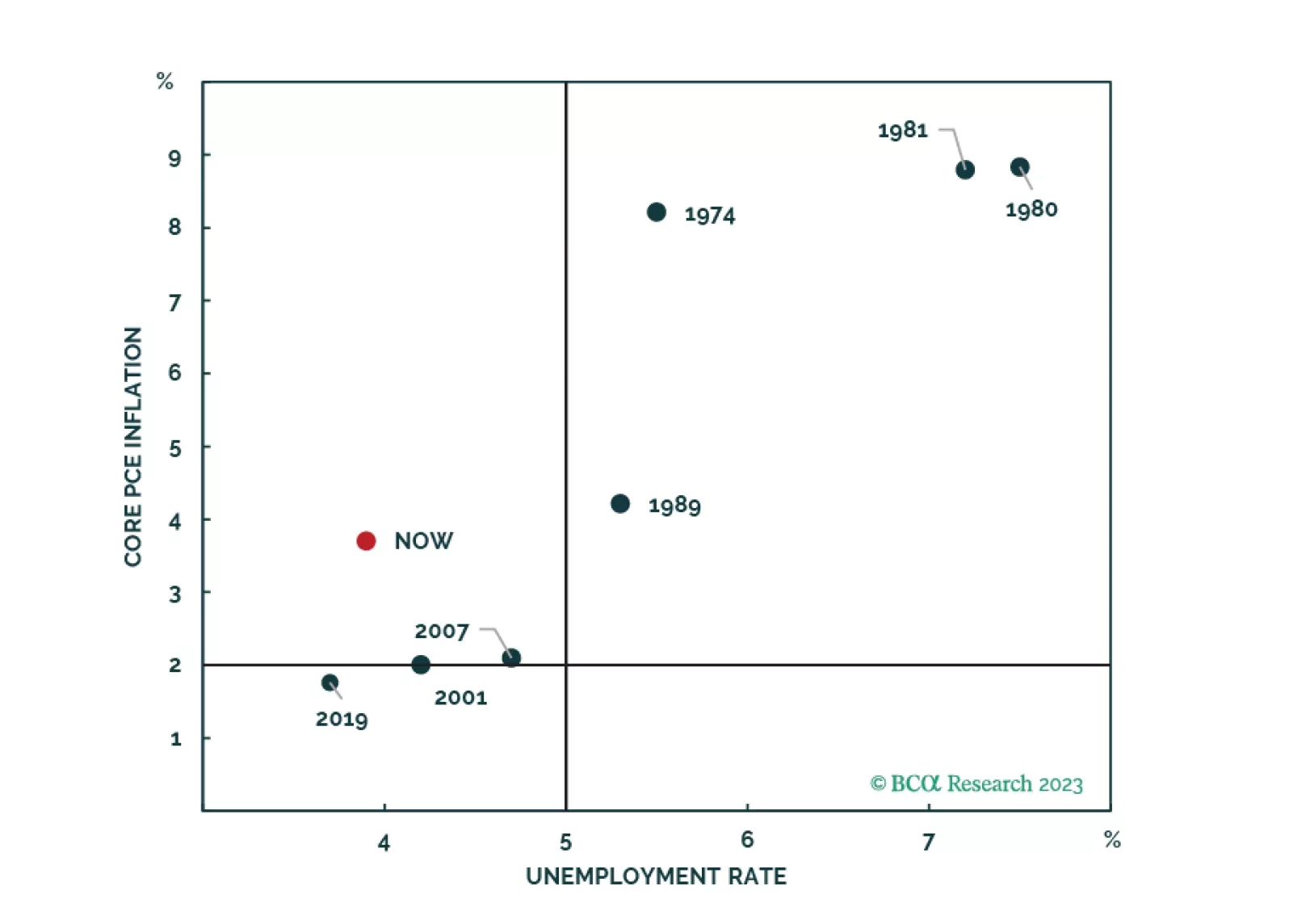

Inflation won’t fall fast enough for the Fed to cut rates preemptively before recession arrives. The risk/rewards balance is unfavorable for risk assets. Stay overweight bonds versus equities.

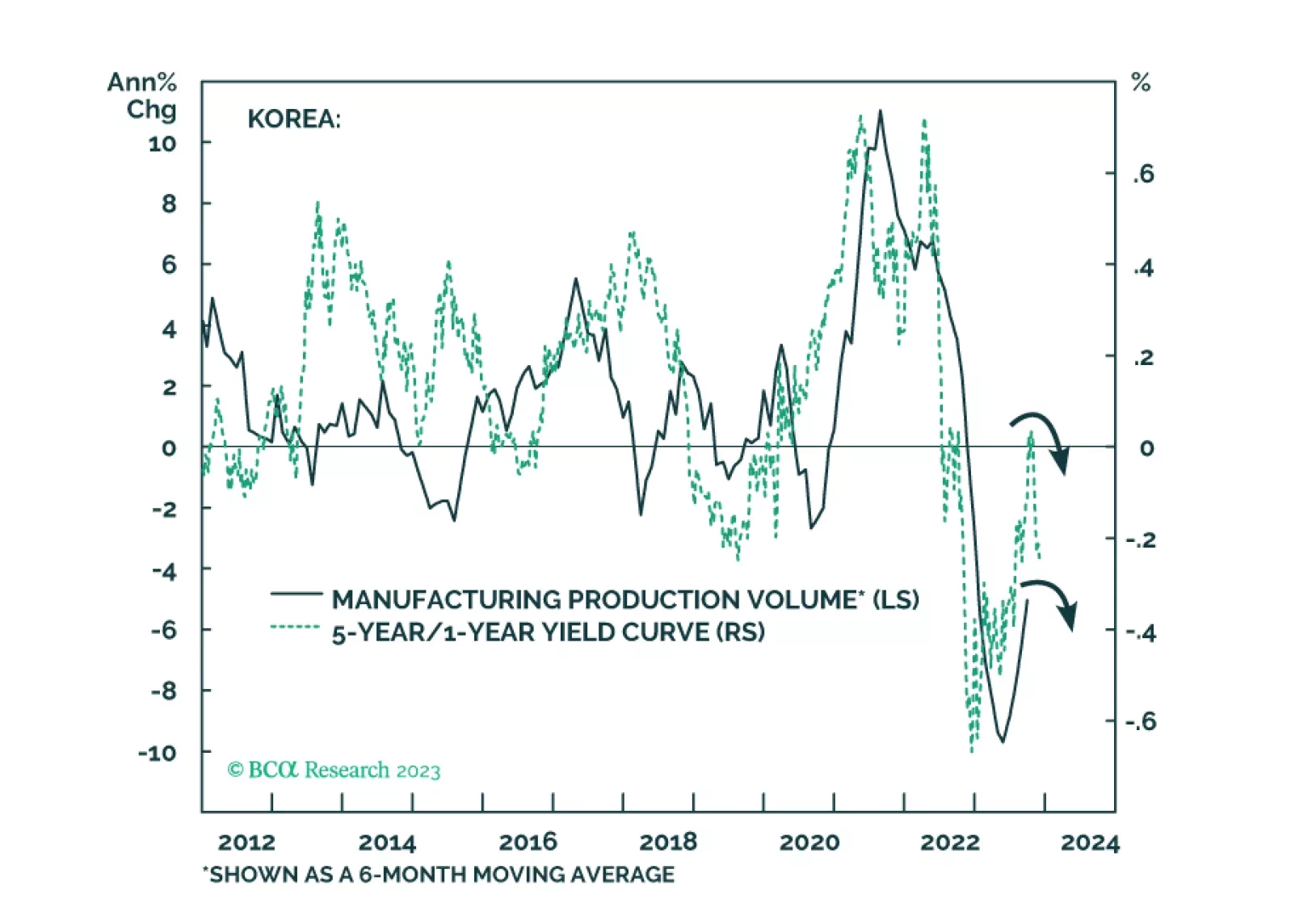

The recent increase in Korean exports will likely prove to be a mid-cycle rebound within a cyclical downtrend. Korea’s households and enterprises are among the most indebted globally, and their debt service ratio is among the highest in the world. Korea’s 10-year bond yields have peaked. We discuss opportunities in Korean stocks as well as in fixed income and currency markets.