Economy

The pro-cyclical Eurozone economy is highly exposed to a global downturn, which we expect will materialize by early 2025. The ECB is behind the curve and we thus expect it to ease more aggressively than markets expect next year. A dovish surprise in 2025…

According to BCA Research’s Commodity & Energy Strategy service, central banks will continue to be a key source of gold demand. Central bank purchases in the first half of this year exceeded first-half purchases in every year they’ve been tracked going…

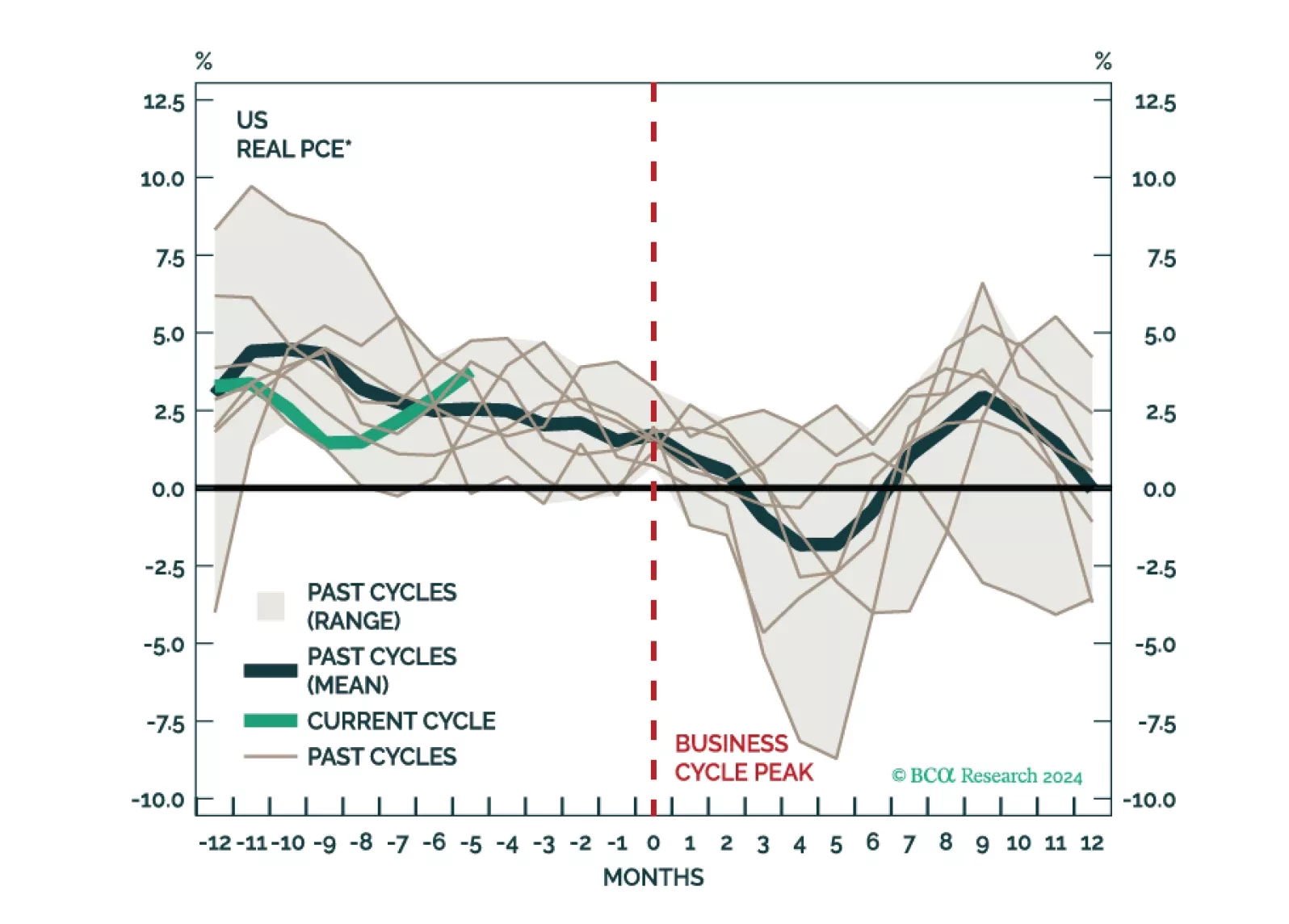

This morning's employment report, particularly the downward revisions to prior months, strengthens our conviction that the US economy is headed for recession.

In this Special Report, we analyze the behavior of economic data leading up to US recessions and discuss some common patterns.

Our Portfolio Allocation Summary for September 2024.

The ISM services PMI remained mostly stable in August, extending a second consecutive month of modest expansion. The headline index ticked 0.1 point higher to 51.5. However, although new orders continued to expand, new export orders fell a whopping 7.6…

The Fed’s Beige Book compiles qualitative input sourced from business and other organizational contacts in each of its 12 Districts. It precedes FOMC meetings by a couple of weeks and is meant to help participants trace the evolution of economic conditions. …

Many currencies have registered sizable gains against the US dollar over the last two months. Most notably, the yen has been one of the best G7 performers since the greenback began depreciating. It now trades at 143 against the US dollar, marking a 11% gain…

There has been a decoupling within the global semiconductor industry. Demand for AI and advanced chips has been booming. Yet, sales of legacy and non-AI semiconductors have failed to recover. Given their spectacular run-up, share prices of high-end and AI-chip producers might continue selling off even if their sales continue to grow rapidly.