Economy

According to BCA Research’s Commodity and Energy Strategy service, soft oil demand growth raises the likelihood that OPEC+ will back down from its plan to begin unwinding some of its production cuts later this year. However, investors should not read this as…

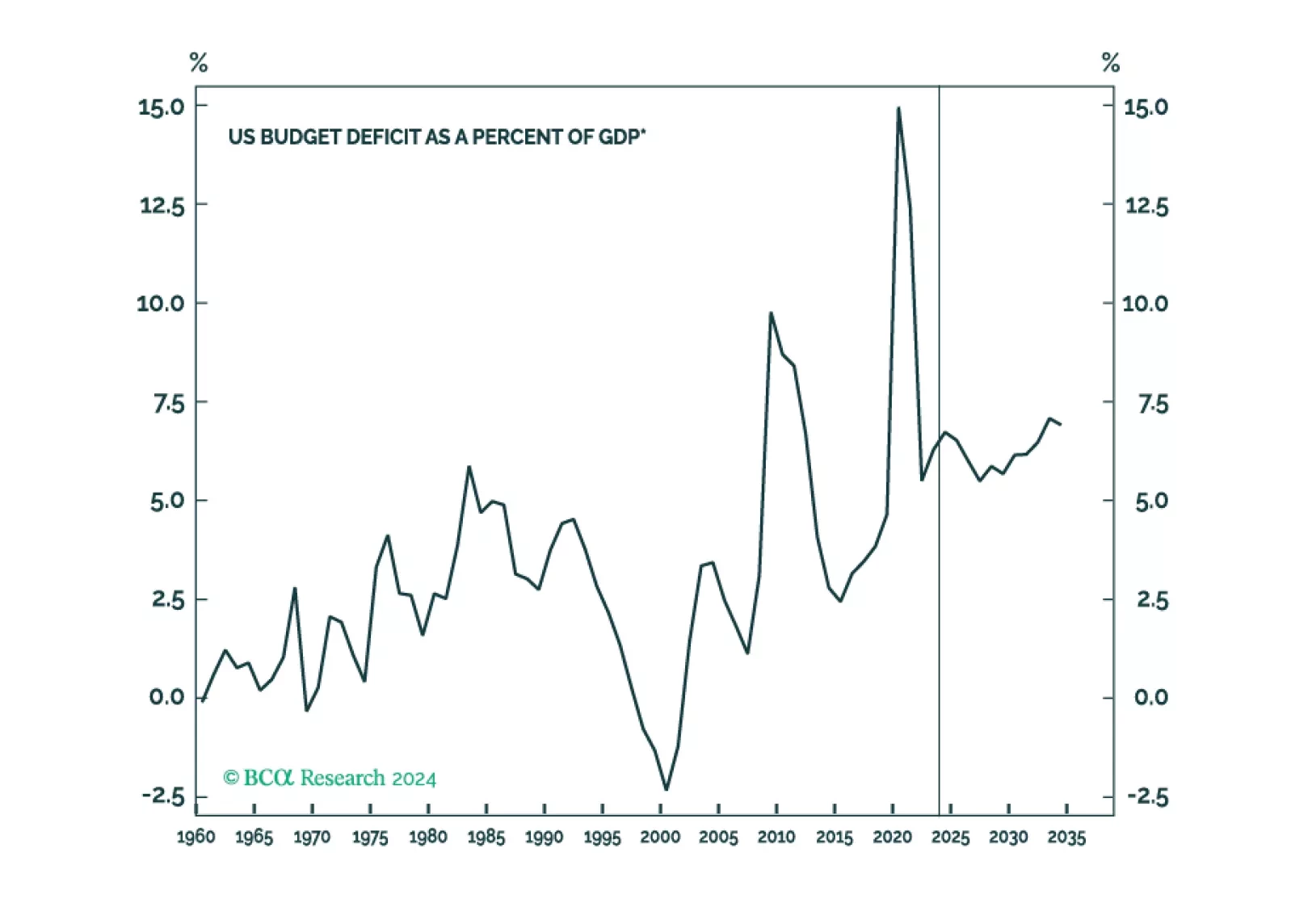

The US fiscal outlook is more unappetizing than it was before the pandemic, but we are not convinced that a difficult day of reckoning awaits. A Treasury market crisis is conceivable, but it is far from inevitable.

Housing starts and permits both disappointed in July. New construction contracted 6.8% m/m, from a 1.1% expansion in June. Permits, which typically lead housing starts, declined 4.0% m/m in July from 3.9% growth in the previous month. Concurrently, the NAHB…

The US unemployment rate has clocked in below 4.5% for 33 consecutive months. However, this historically low rate camouflages nascent cracks in the US labor market. Ahead of recessions, firms usually reduce the pace of hiring before they start…

Preliminary estimates suggest that although consumers’ perceptions of current economic conditions unexpectedly deteriorated in August, they are becoming increasingly optimistic about the future. The University of Michigan current conditions gauge dropped…

Singapore is a small open economy sensitive to global trade dynamics. Its non-oil exports (NODX) are thus a good bellwether for global growth conditions. They rebounded sharply in July from a previous contraction, largely exceeding expectations. Notably,…

According to BCA Research’s GeoMacro Strategy service, while the idea that Donald Trump would allow China to build factories in the US does not mesh with the contemporary media narrative, it would fit the historical track record. The last time that the US had…

What do the mixed signals sent by the UK economy mean for the Bank of England, and what are the implications for Gilts and the British pound?

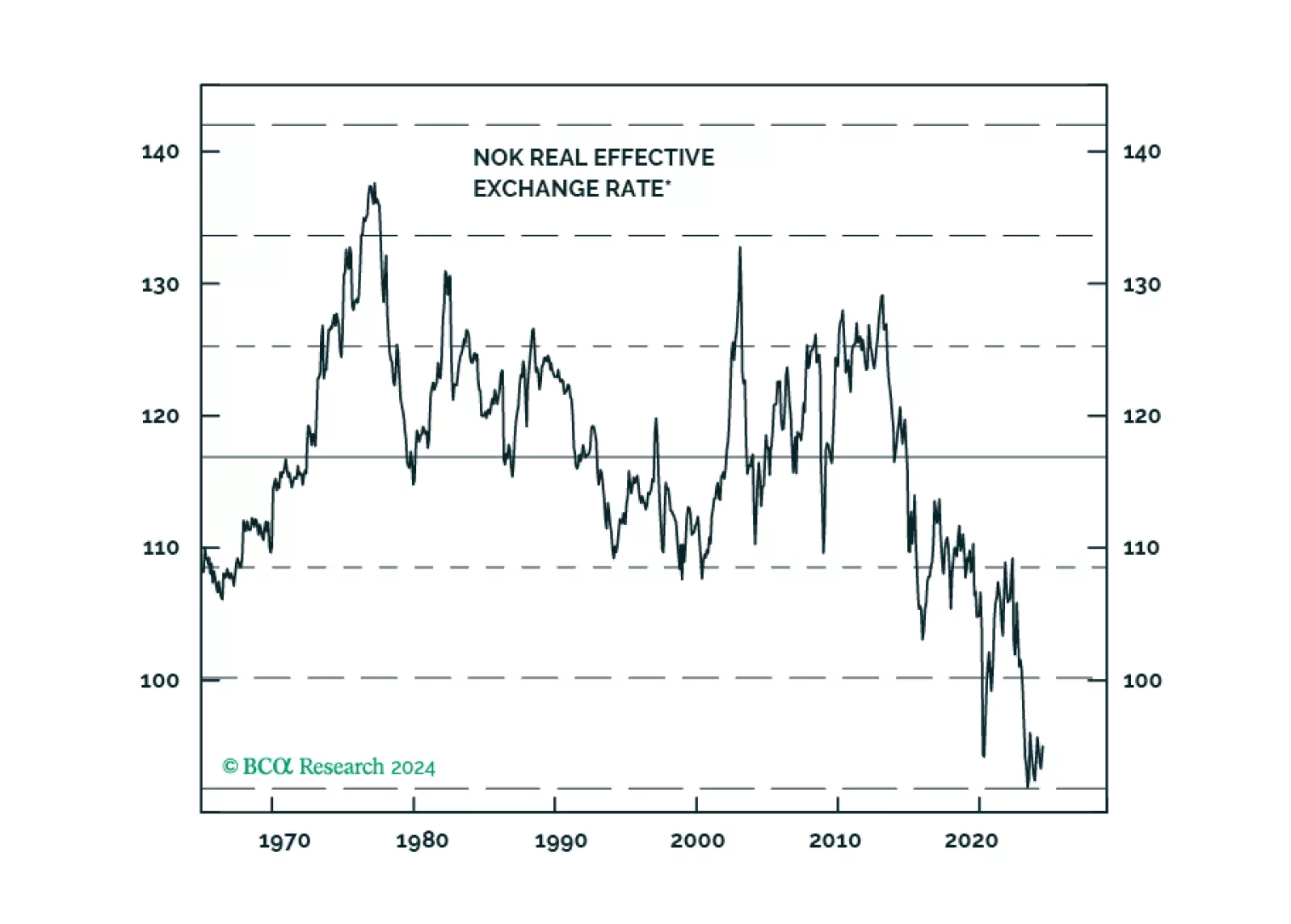

In this report, we gauge the reasons behind the persistently weak Norwegian krone, despite what appears to be benign domestic economic conditions.

China’s economic malaise extended through the month of July. The contraction in property investment worsened (-10.2% YTD y/y) and disappointed expectations of a slower pace of decline. Residential property sales remained dismal (-25.9% YTD y/y). Industrial…