Economy

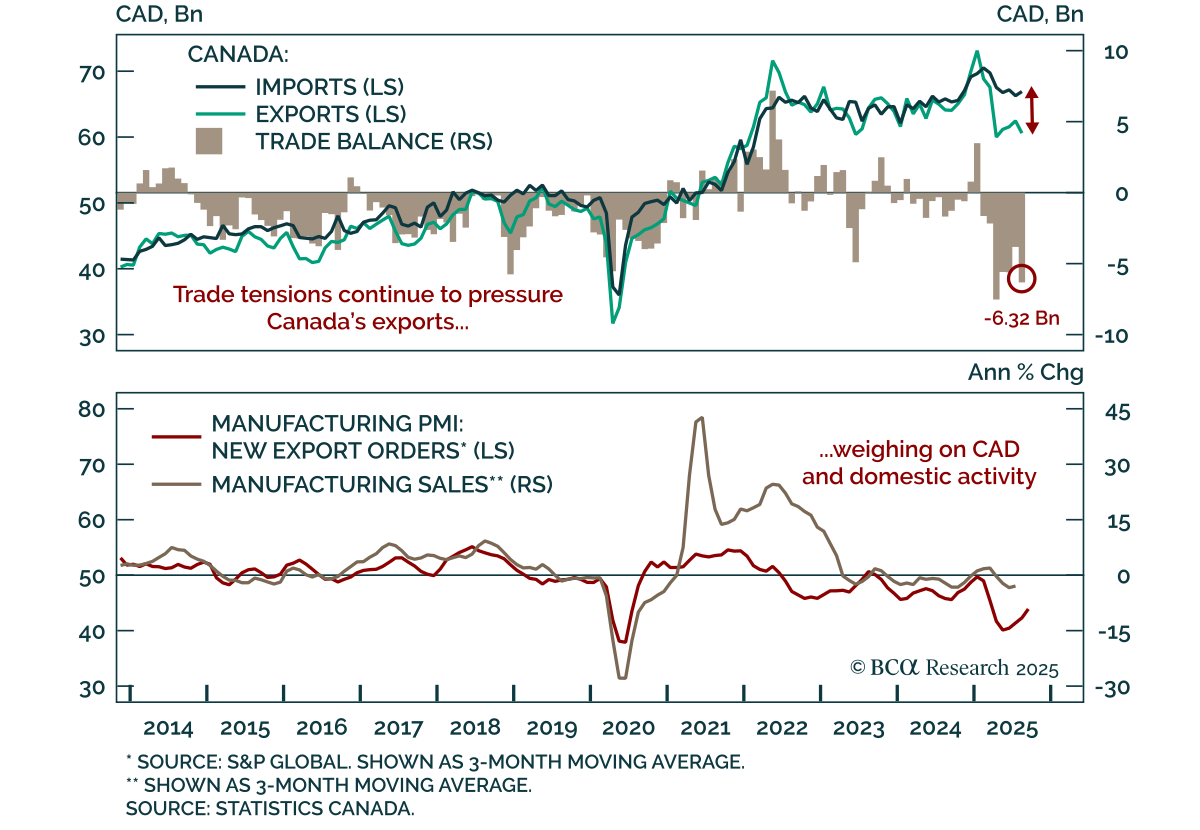

Trade concerns continue to weigh on Canada, reinforcing a cautious macro outlook with near term downside for bond yields and the CAD, though the currency selloff is getting stretched and could soon present an attractive entry point.Canada’s goods trade…

The K-shaped economy aptly describes the bifurcation between low- and high-end households but it’s not something investors should celebrate if they want the expansion to continue.

Our Portfolio Allocation Summary for October 2025.

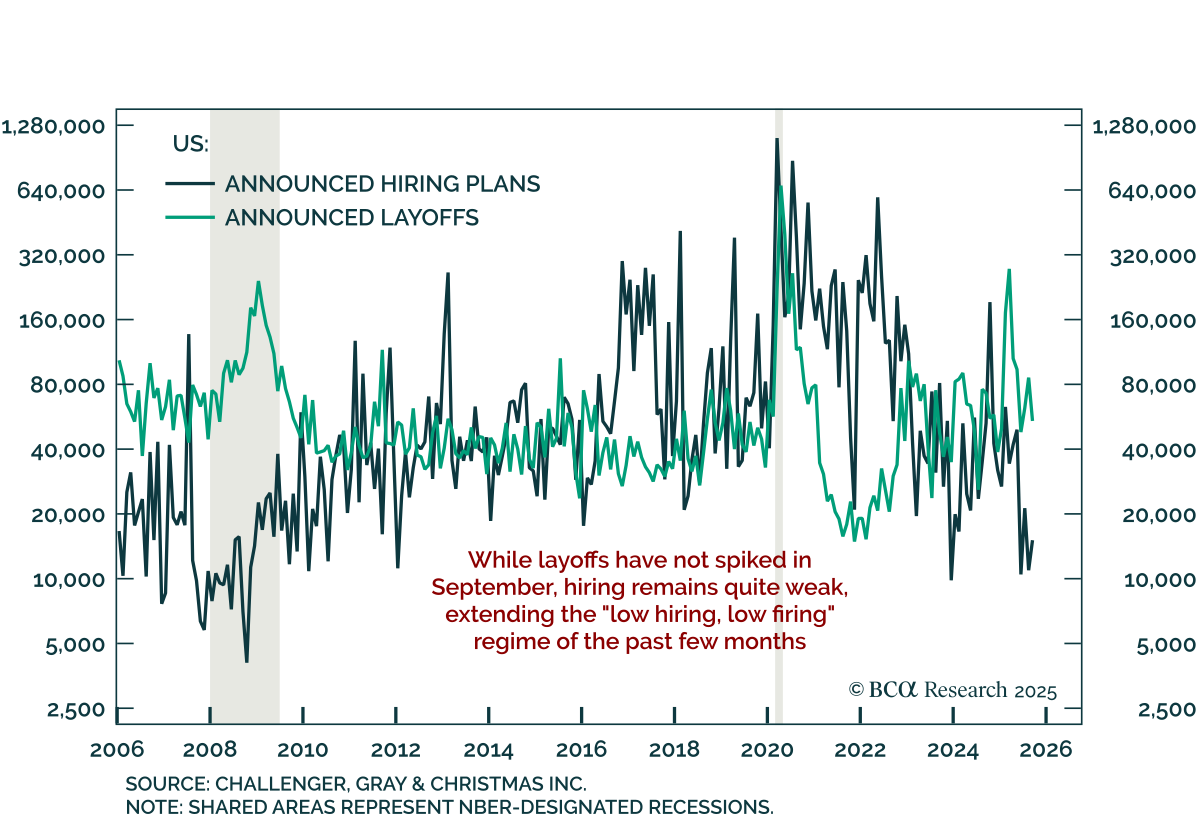

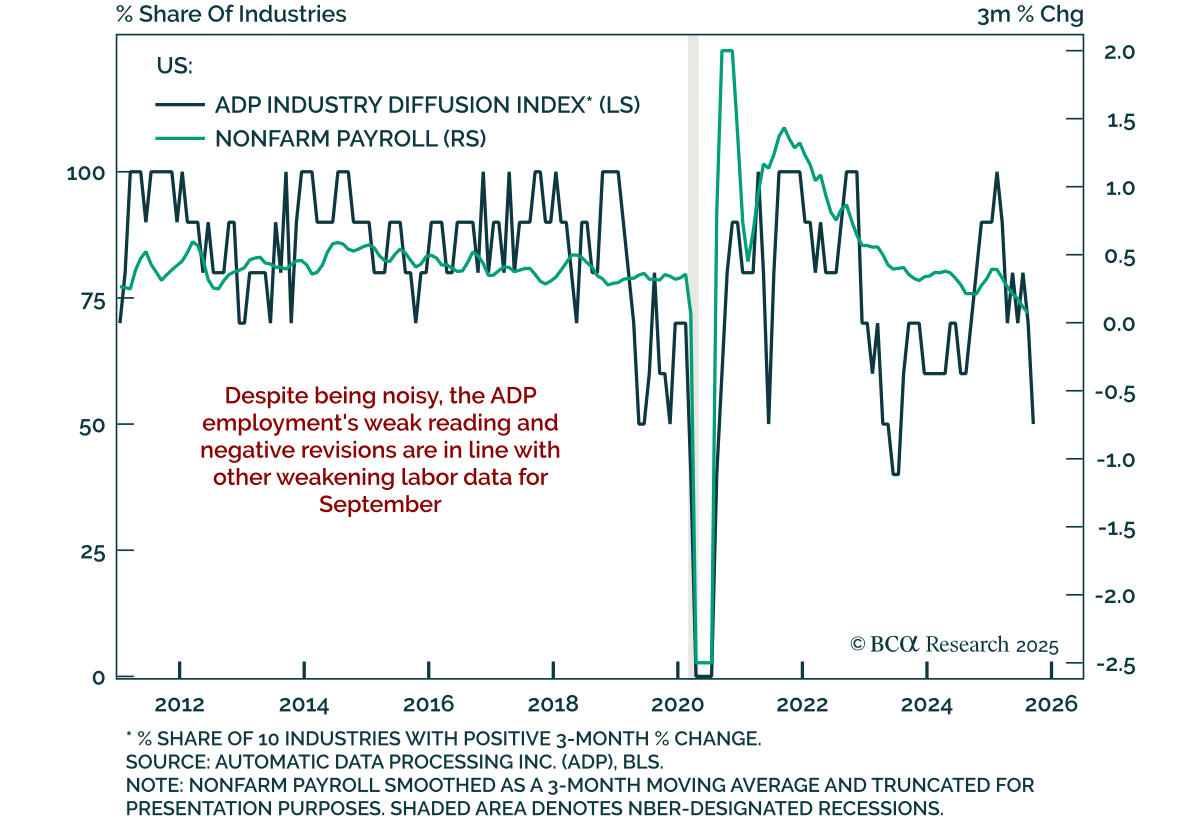

With the government shutdown delaying jobs data, alternative indicators point to a marginally weaker US labor market in September. The absence of the monthly employment report and weekly initial claims leaves us reliant on other sources. The September…

The September ADP report contracted by 32k jobs, missing expectations and extending the trend of weakening employment. August was revised lower to a 3k contraction, marking two consecutive months of decline after also contracting in June. The report was noisy…

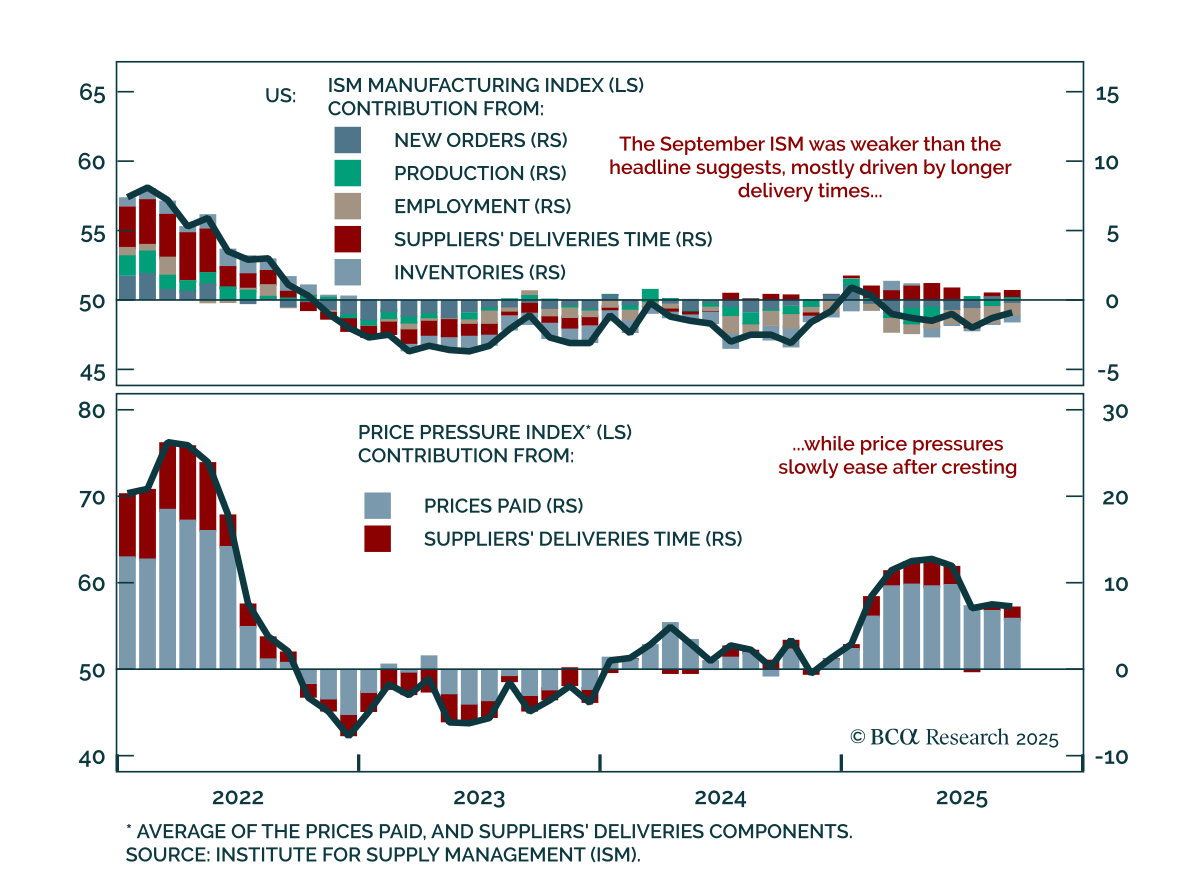

The September ISM Manufacturing index beat expectations at 49.1, but details confirm weak momentum and tariff-driven pressures. The headline improved from 48.7 in August, its second consecutive monthly gain, but the uptick came mainly from longer supplier…

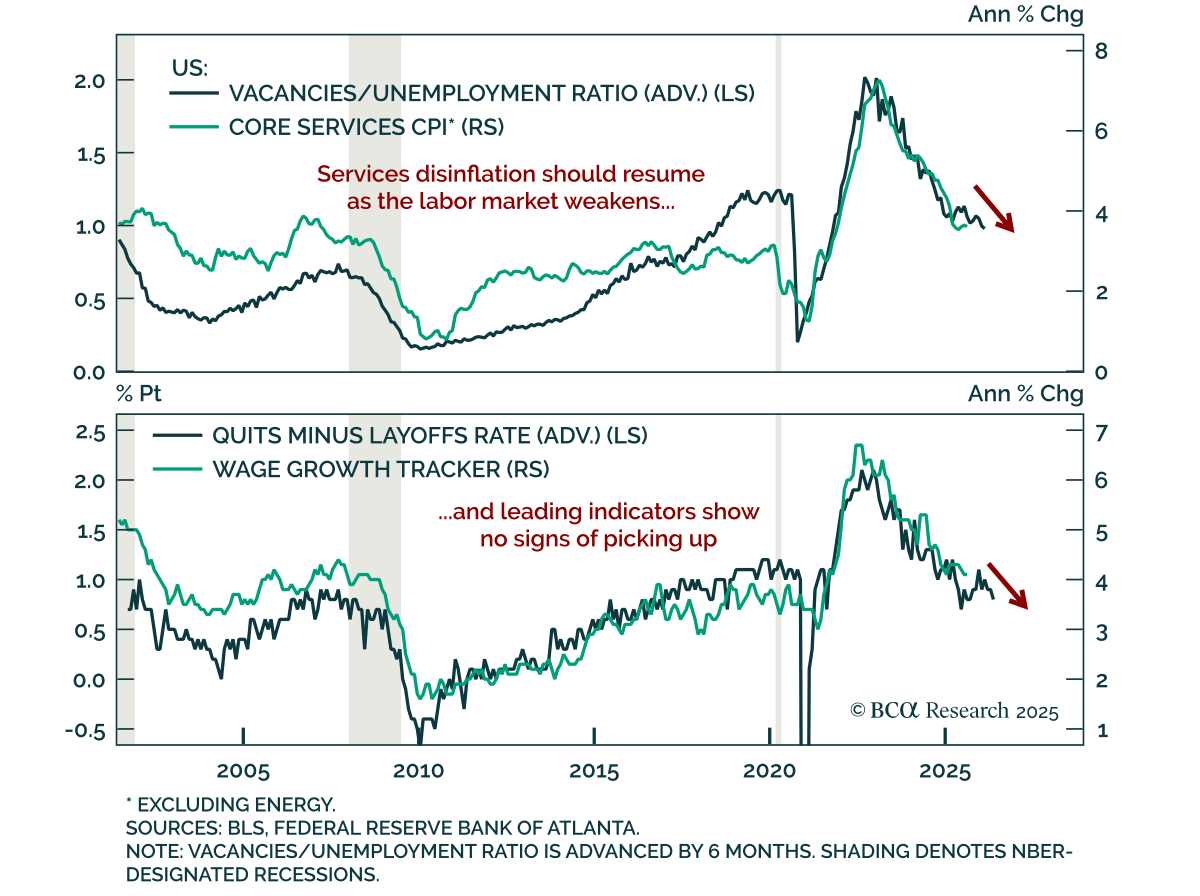

August JOLTS data confirm a loosening labor market, reinforcing a modestly defensive allocation stance. Job openings ticked up to 7.23m from 7.21m, yet gains came from non-cyclical sectors. Quits fell to 3.09m from 3.17m, pushing the quits rate down to 1.9%…

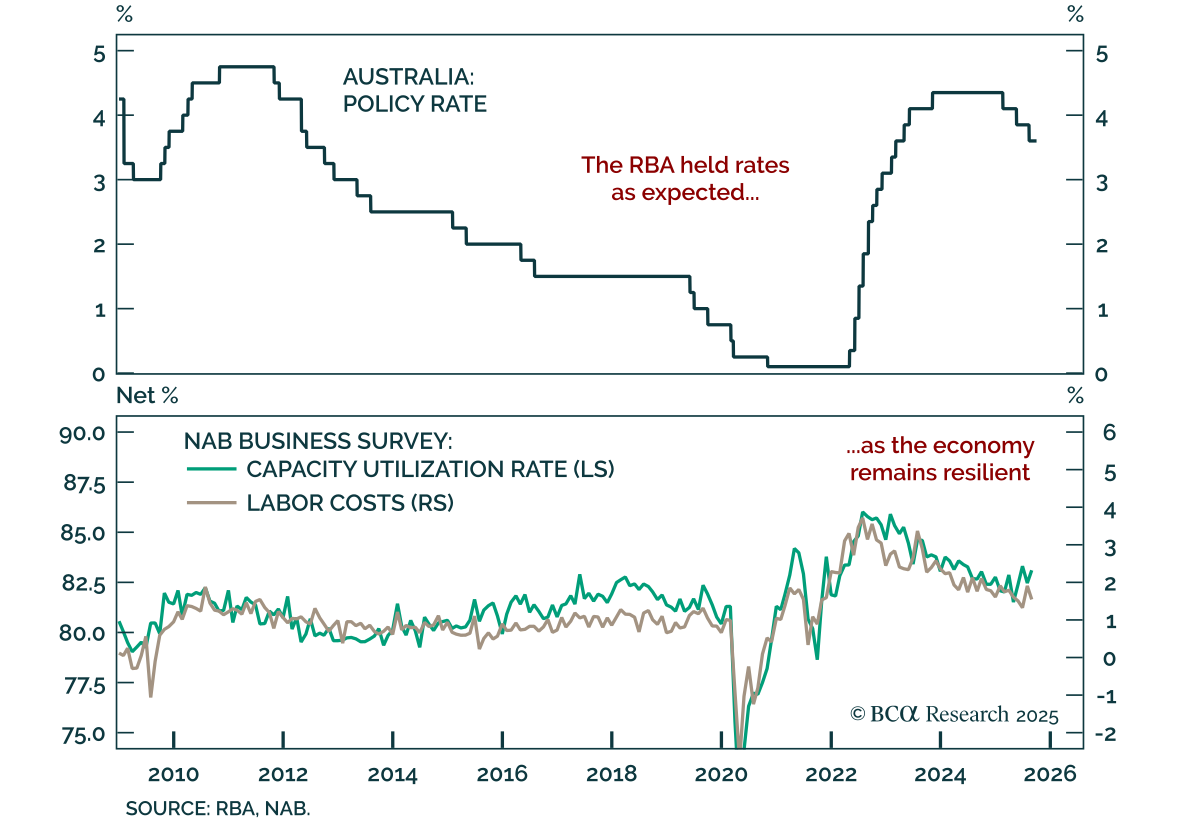

The RBA held rates at 3.6% as expected, maintaining caution as inflation could prove stronger than expected. Policy remains slightly restrictive, and at most one additional cut is on the table as the central bank has achieved a soft landing. While the RBA has…

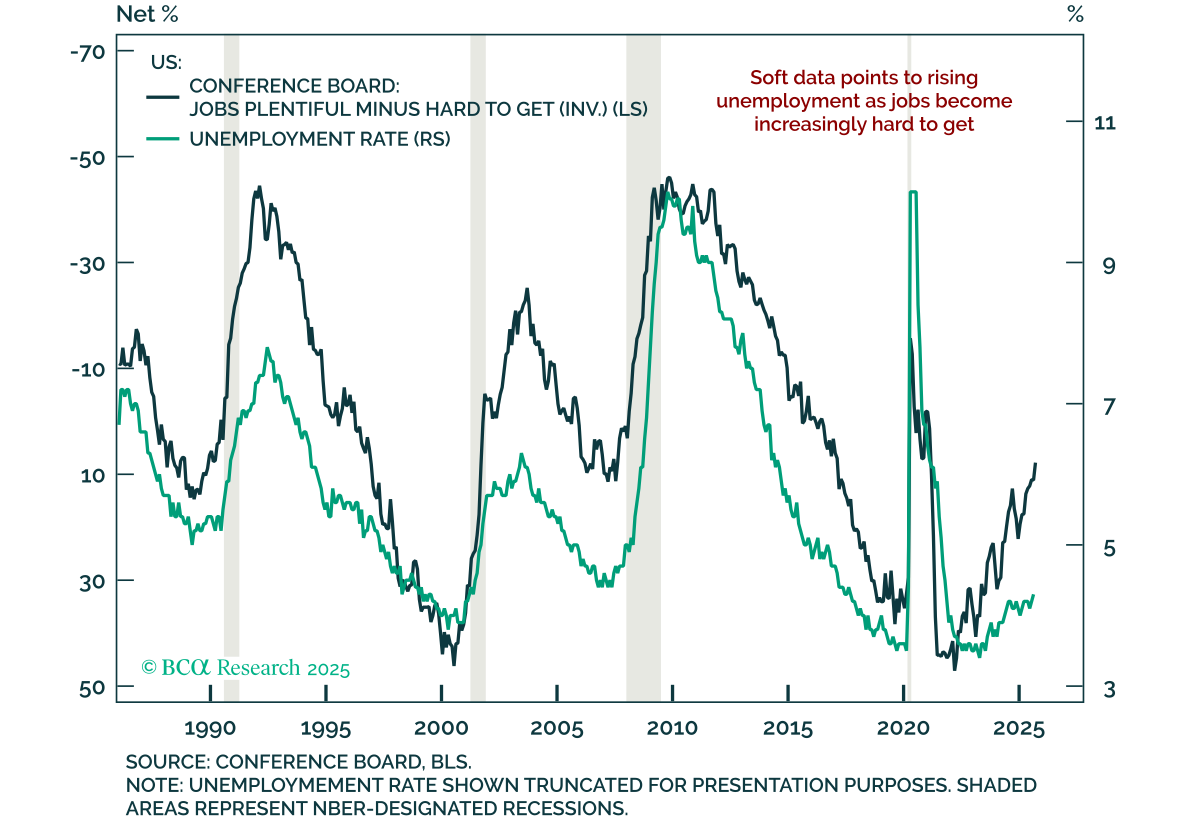

Consumer confidence fell further, reinforcing weakening labor signals and supporting a long duration stance. The September Conference Board Consumer Confidence Index dropped to 94.2 from 97.8, missing estimates. Both present situation and expectations…

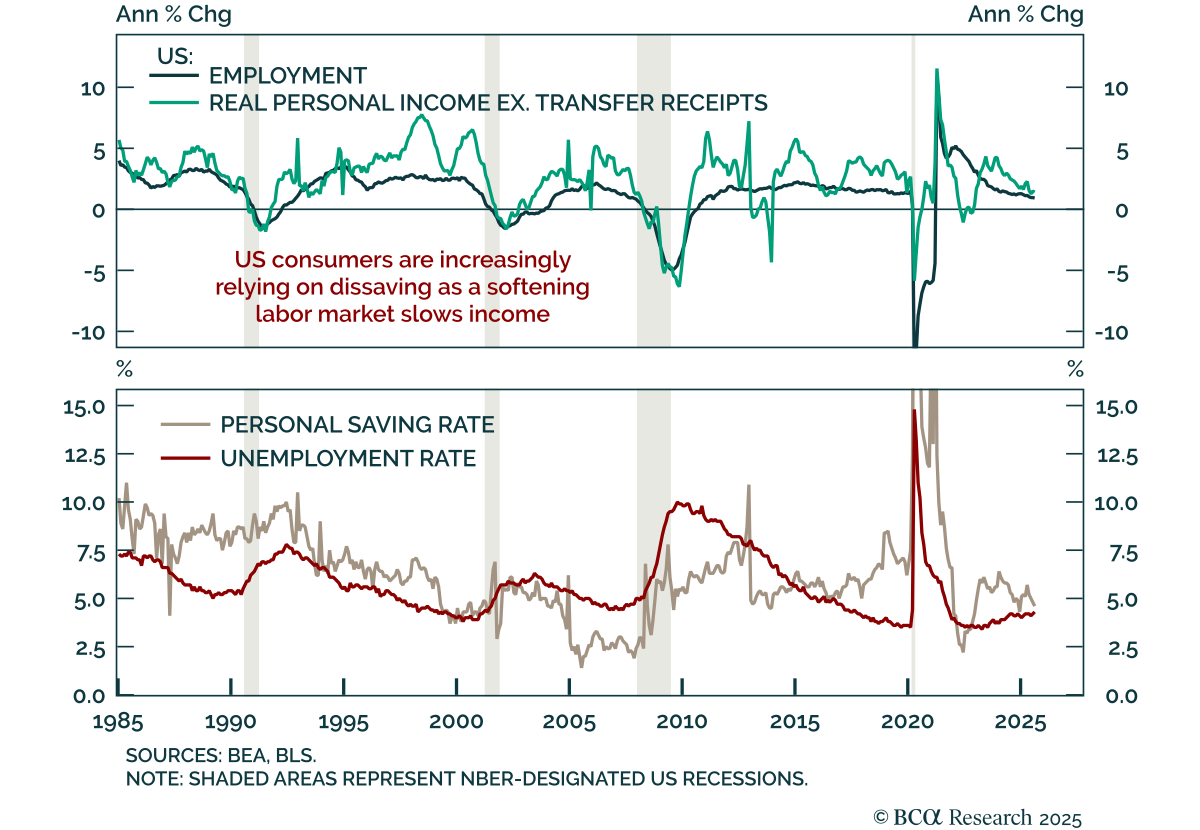

September consumption and income data beat estimates, showing a resilient US consumer but leaving the outlook fragile. Personal spending rose 0.6% m/m, outpacing income at 0.4%, pushing the saving rate down to 4.6%, its lowest level this year. Adjusted for…