Economy

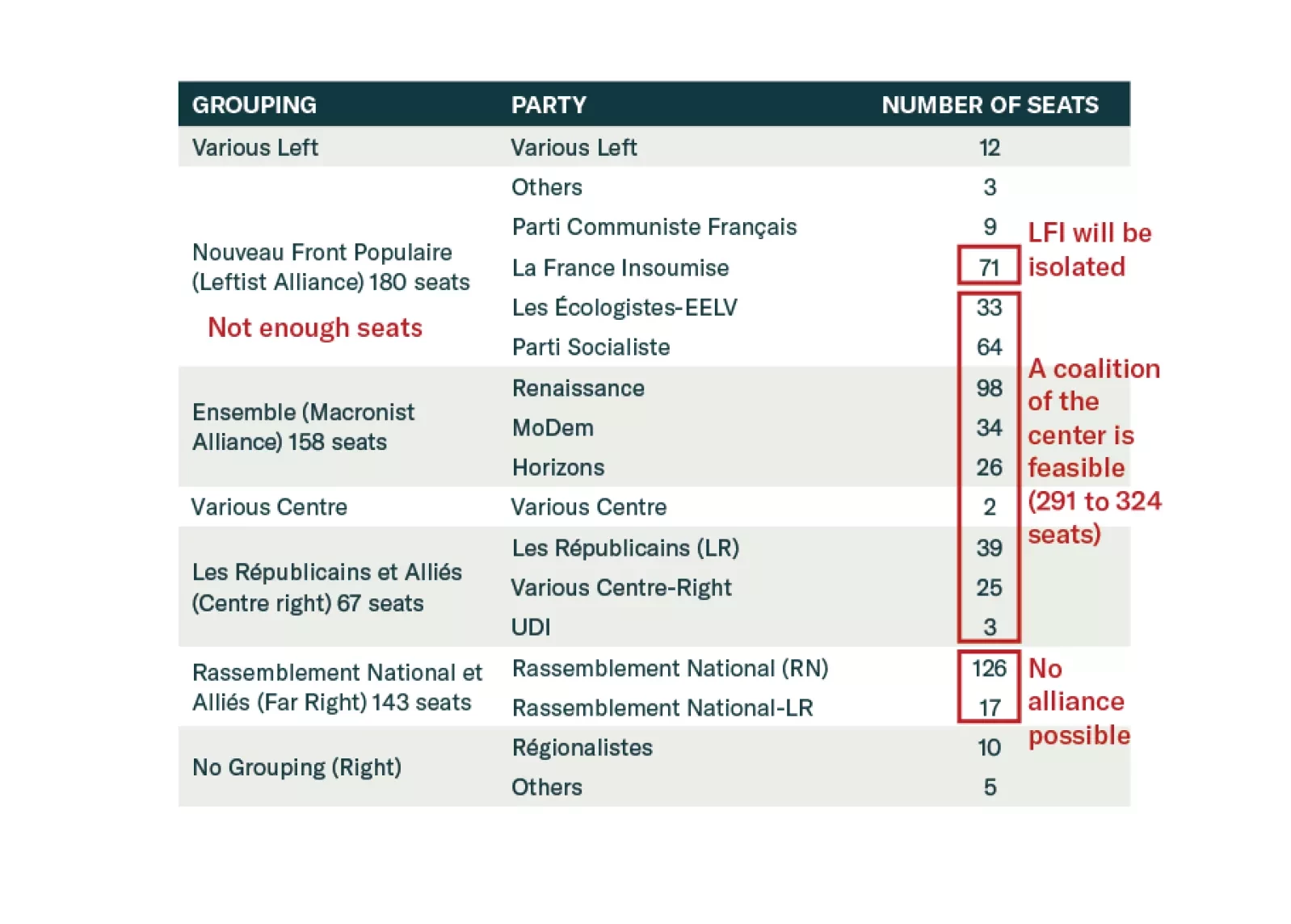

At first glance, France has moved to the far left. However, this coalition is fragile, and Macron’s allies still hold the balance of power. What are the assets that will benefit from this new political setup, and those that will not?

Although we ticked a second box on our checklist, the incoming data still do not indicate that a recession is imminent. We remain tactically equal weight equities with a strong bias to underweight them, but we’re not exiting the party just yet.

Is the RMB cheap or expensive? Based on trade accounts, the yuan is inexpensive, but the RMB is vulnerable due to capital outflows. Yet, Beijing will not resort to a rapid devaluation for now, and the option of floating the currency is improbable. The PBoC will allow a gradual depreciation of the yuan versus the dollar, say around 5%, in the next six months.