Economy

US retail sales were mostly unchanged, growing by a mere 0.1% m/m in May, short of the expected 0.3% monthly increase. A 2.2% m/m decline in gasoline stations’ sales weighed on the overall result, though retail sales excluding autos and gas disappointed by an…

The Reserve Bank of Australia kept its cash rate at 4.35% at its policy meeting on Tuesday, in line with market expectations. Australia’s monthly measure of headline inflation came in at 3.6% in April, still considerably above the midpoint of the RBA’s 2-3%…

Singapore is a small open economy sensitive to global trade dynamics. Its non-oil exports (NODX) are thus a good bellwether for global growth conditions and they surprised to the upside in May. Notably, electronics exports, which are particularly sensitive to…

The equity risk premium (ERP) allows investors to assess the additional compensation they are offered as an enticement to assume equities’ incremental risk. The ERP measures equities’ excess return by deducting the inflation-linked 10-year yield from the…

Chinese retail sales grew 3.7% y/y in May, from 2.3% in April, upending expectations of a more muted 3.0% increase. The government appliance trade-in program has likely boosted these figures. Sales of home-related goods such as communication appliances,…

Housing is the most interest-rate-sensitive sector of the economy. Yet, the very aggressive monetary tightening cycle has only had a muted effect on home prices. While recent housing market data have been mixed, prices have not tumbled. Indeed, a tight…

Declines in Chinese new and used home prices accelerated in May to 0.71% m/m and 1.00% m/m respectively, and the contraction in residential investment deepened to 10.1% YTD y/y. These figures come on the heels of relaxed purchase and mortgage rules, as well…

Eurozone equities sold off 7% from their June 6 highs, according to MSCI indices. The surprise French legislative elections and renewed fears of populism and European Union exits are spooking investors. Yet, our European Investment strategists argued that…

According to BCA Research’s Geopolitical Strategy service, the South African election presents a window of opportunity for productivity-boosting structural reforms, such as privatization, to coincide with monetary and fiscal easing necessary to fend off…

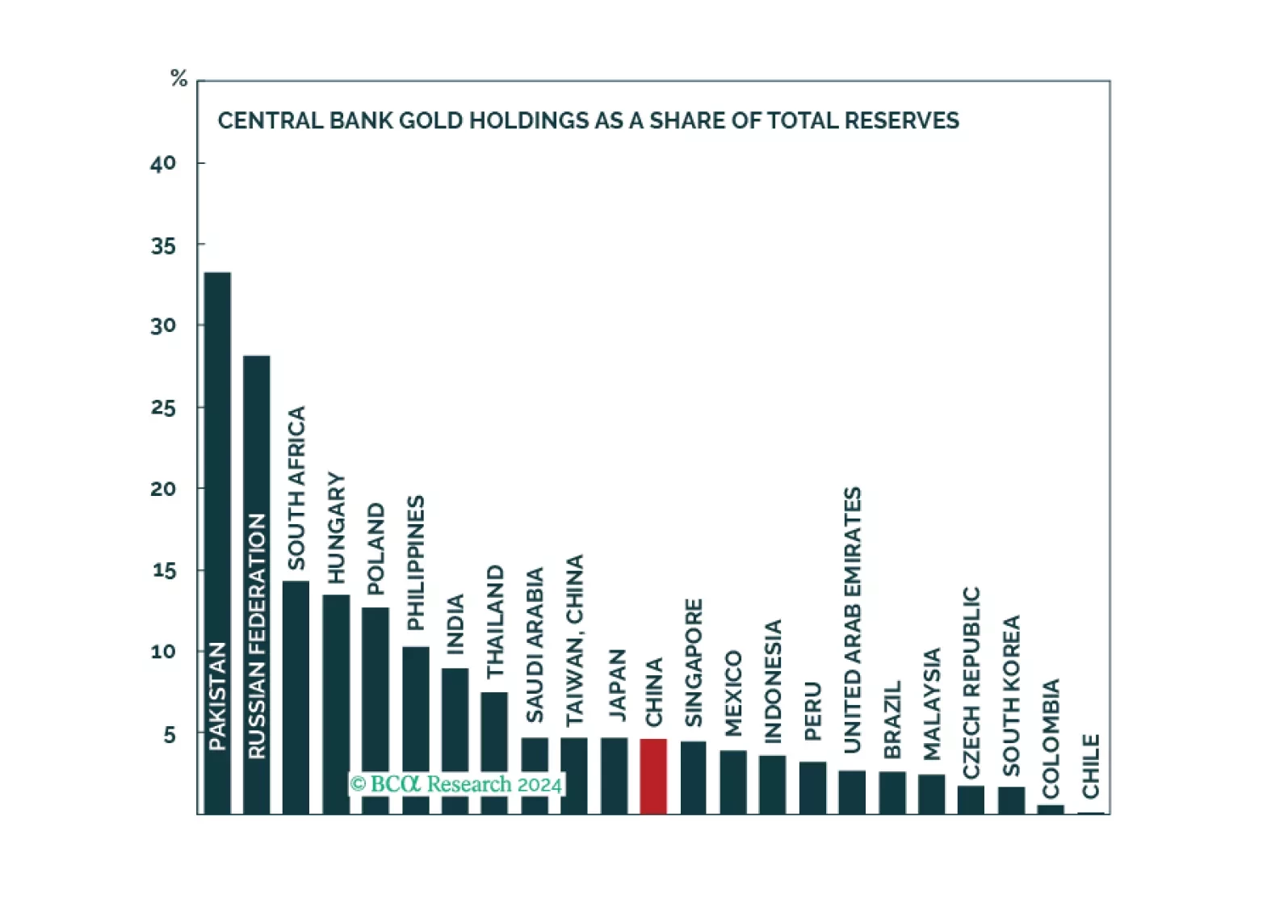

Gold prices might experience a correction or consolidation over the near term. However, cyclical and structural forces will ultimately cause the yellow metal to trend upwards.