Economy

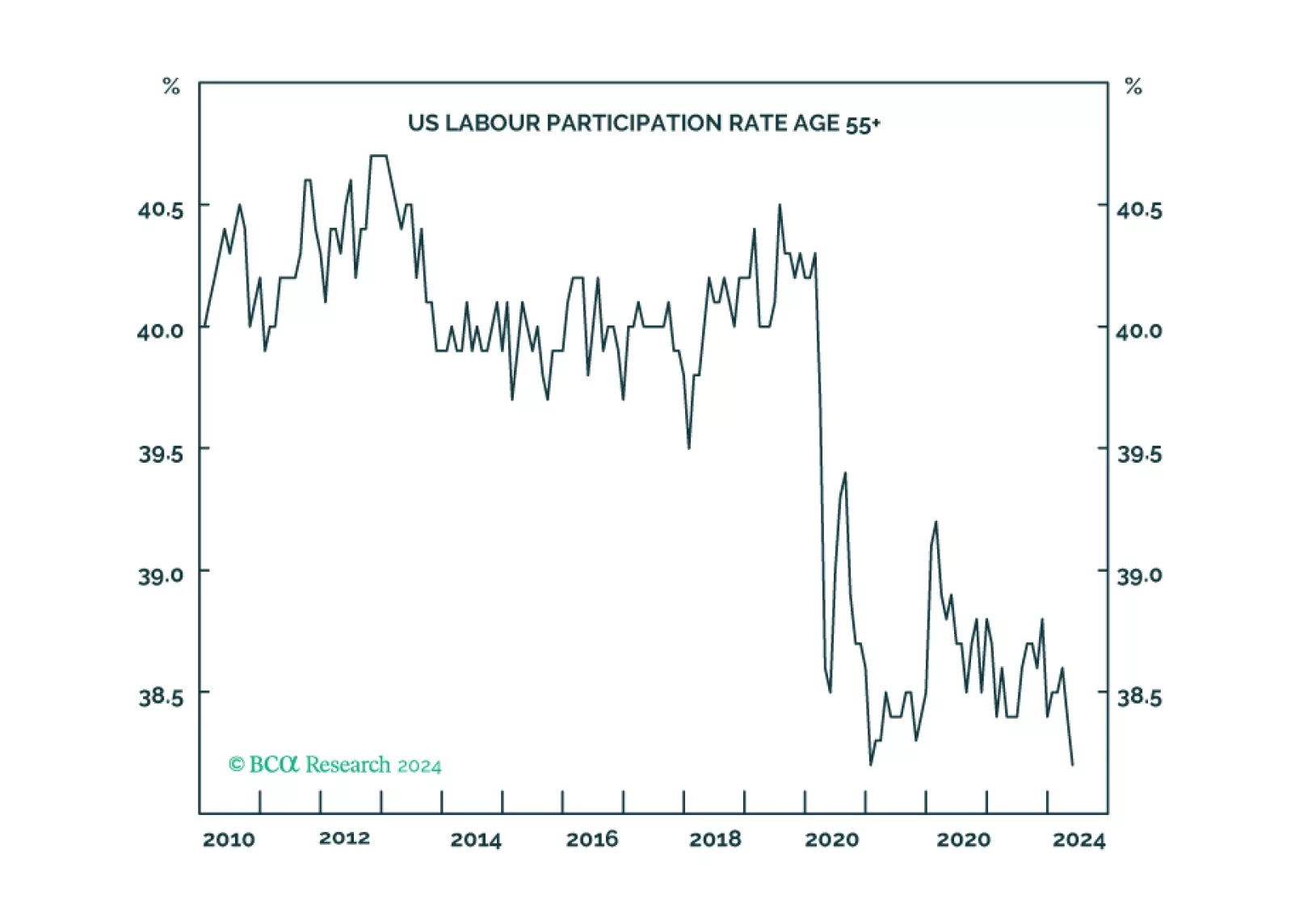

According to BCA Research’s Counterpoint service, job losers not on temporary layoff (‘bad’ unemployment) will need to rise further for the Fed to reach its 2 percent inflation target. Although prime-age participation has surged, the participation of older…

We continue to expect a recession by early 2025 but assign non-trivial odds to growth surprising to the upside until then. Our Global Investment Strategy team thus recommends investors adopt a barbell equity strategy as a hedge for the second half of 2024,…

Our reaction to this morning’s CPI report and this afternoon’s FOMC meeting.

On Wednesday, the European Commission announced it would impose tariffs ranging between 17% and 38% on imports of Chinese EVs starting next month. These duties will be applied on top of existing 10% across-the-board tariffs on all Chinese EV imports, and…

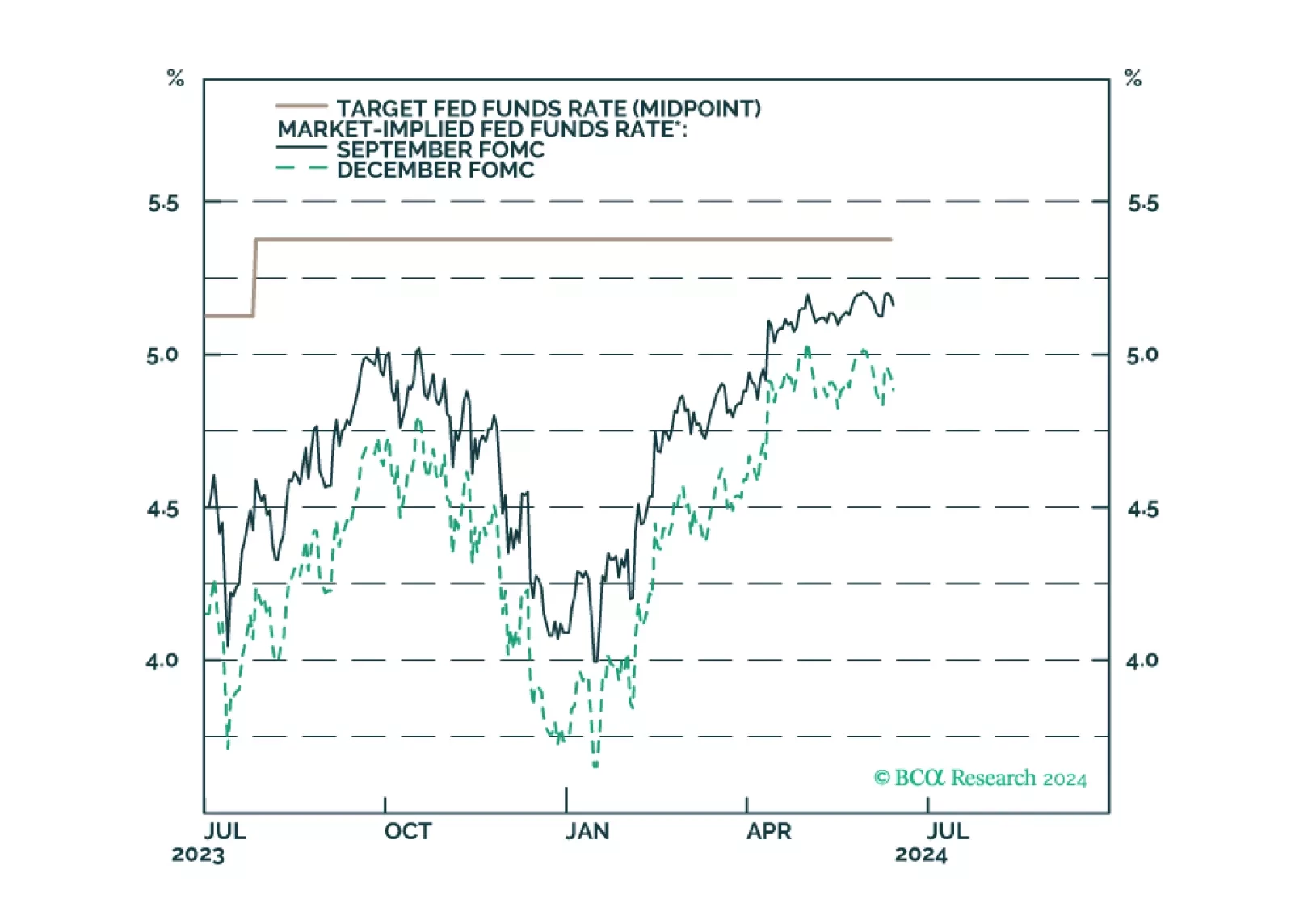

In a widely expected move, the Fed kept its policy rate unchanged within a 5.25%-5.5% range following its June 11-12 meeting. However, the median dots have moved higher for both 2024 and 2025. The median FOMC member now expects to cut only once this year…

US CPI inflation continued to ease in May. Headline CPI stagnated on a month-on-month basis (3.3% y/y) in May, down from April’s 0.3% m/m (3.4% y/y), and below expectations of a more muted rate of growth. Core CPI also slowed more than expected, rising…

The Bank of Japan exited negative interest rate policy in March, but subsequent softer-than-expected CPI inflation prints have complicated its path towards tightening. The central bank is widely expected to stay put when it meets this week. Governor Kazuo…

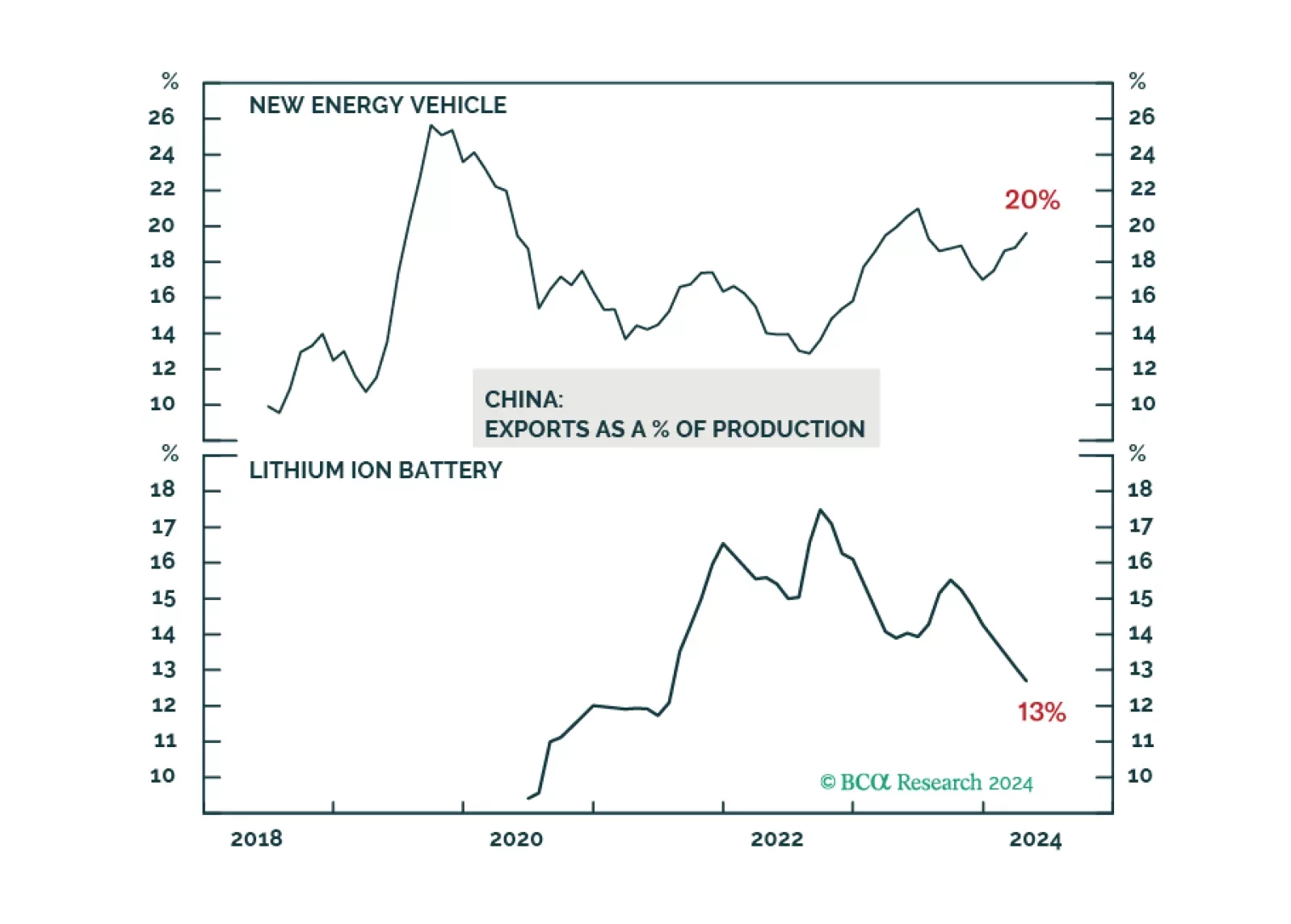

According to BCA Research’s China Investment Strategy service, it is an overstatement to assert that China’s subsidies are the main driver of its green energy industries’ competitiveness. It is commonly perceived that China heavily subsidizes its industry…

1 in 17 older Americans workers have gone missing either through ‘excess retirements’ or ‘excess mortality’. The consequent dislocation of the labour market means that the Fed’s work is not yet done. We go through some investment implications. Plus: the China and Japan rallies are exhausted.

The issue of "industrial overcapacity" in China may be a misconception. Overcapacity in the old-economy sectors has largely diminished, while China's dominance in the global green-energy market reflects its technological advancements and innovations.