Economy

The Caixin Chinese manufacturing PMI reached a two-year high in May, expanding at a larger-than-expected rate from 51.4 to 51.7. The Caixin figure thus contrasts with the alternative NBS manufacturing PMI, which unexpectedly contracted in May. The Caixin…

The Swiss KOF Barometer is a composite leading indicator of the Swiss economy. It surprised to the downside in May, coming in at 100.3 from 101.9, below expectation of an acceleration to 102.1. Switzerland’s economy is highly pro-cyclical and…

According to BCA Research’s Commodity & Energy Strategy service, the oil demand forecasts from the IEA, EIA, and OPEC are too optimistic. The IEA, EIA, and OPEC all anticipate oil demand growth to slow this year following a robust post-pandemic…

Our Portfolio Allocation Summary for June 2024.

The US economy is in the “Overheating” phase, so stronger growth brings higher inflation. Tight monetary policy means recession is still likely over the next 12 months. Stay defensive.

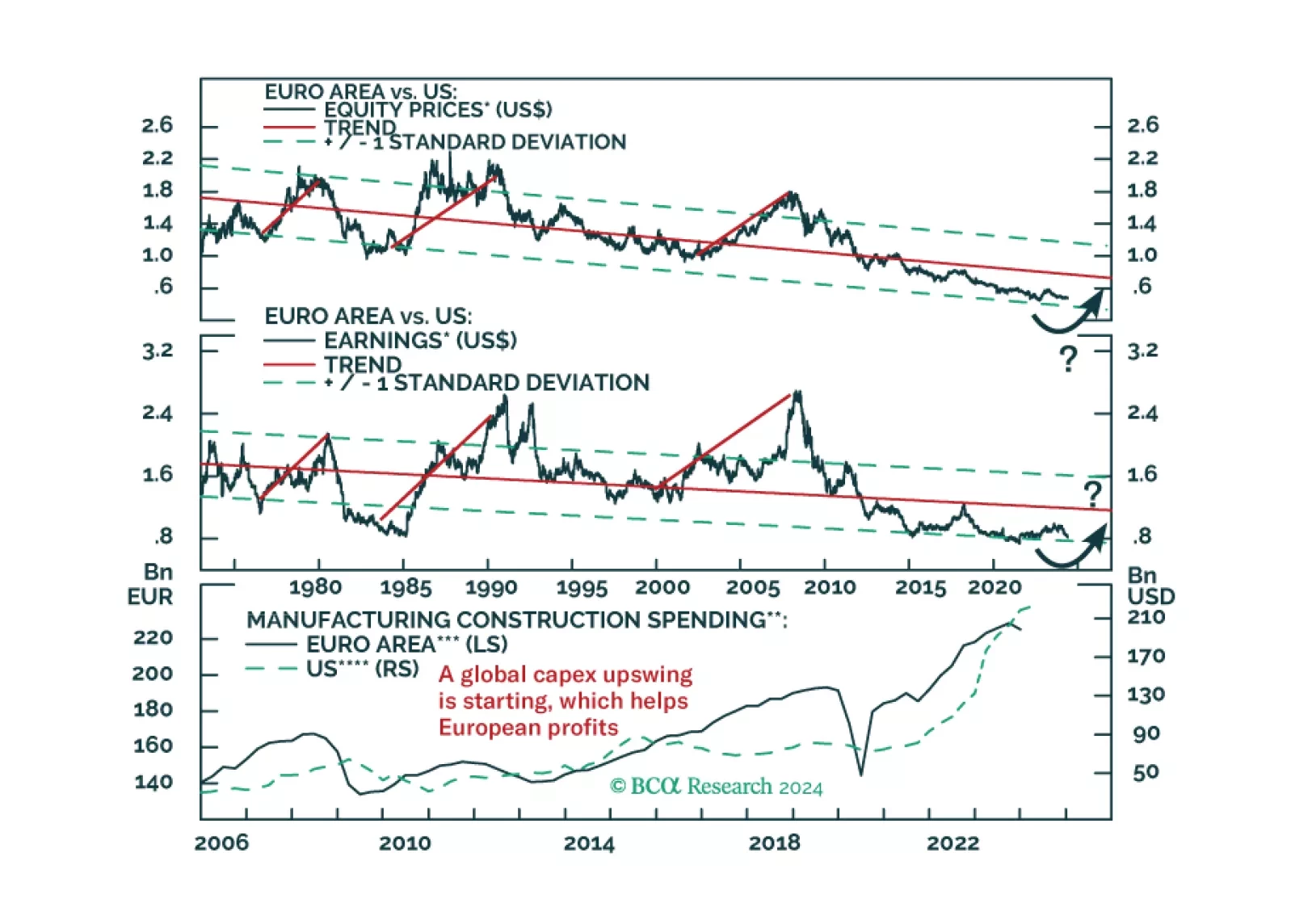

European stocks have massively underperformed US ones since the GFC. Demographics and productivity say this trend will continue, but is that really so?

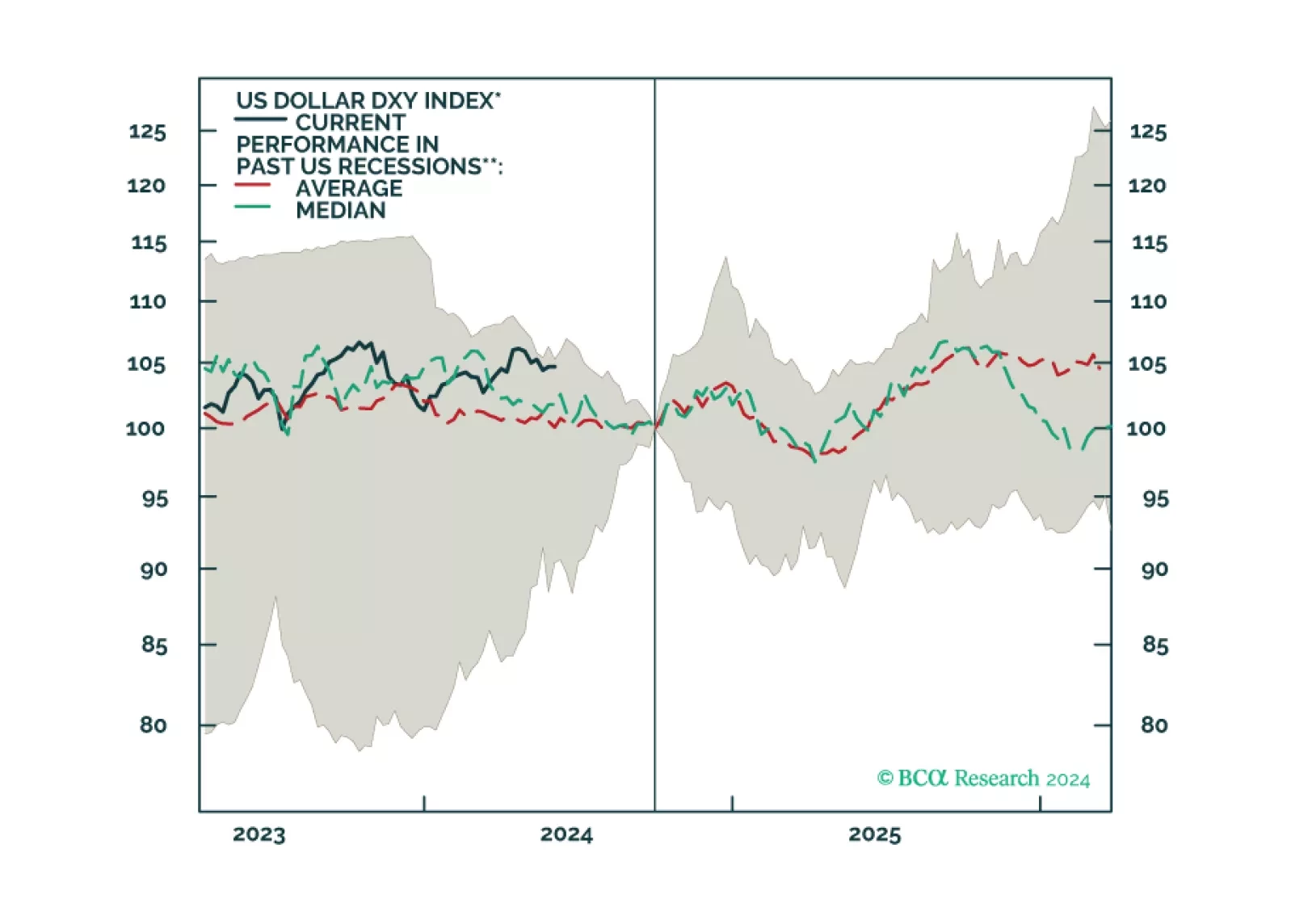

In this report, we gauge the outlook for the dollar given client visits in Africa.

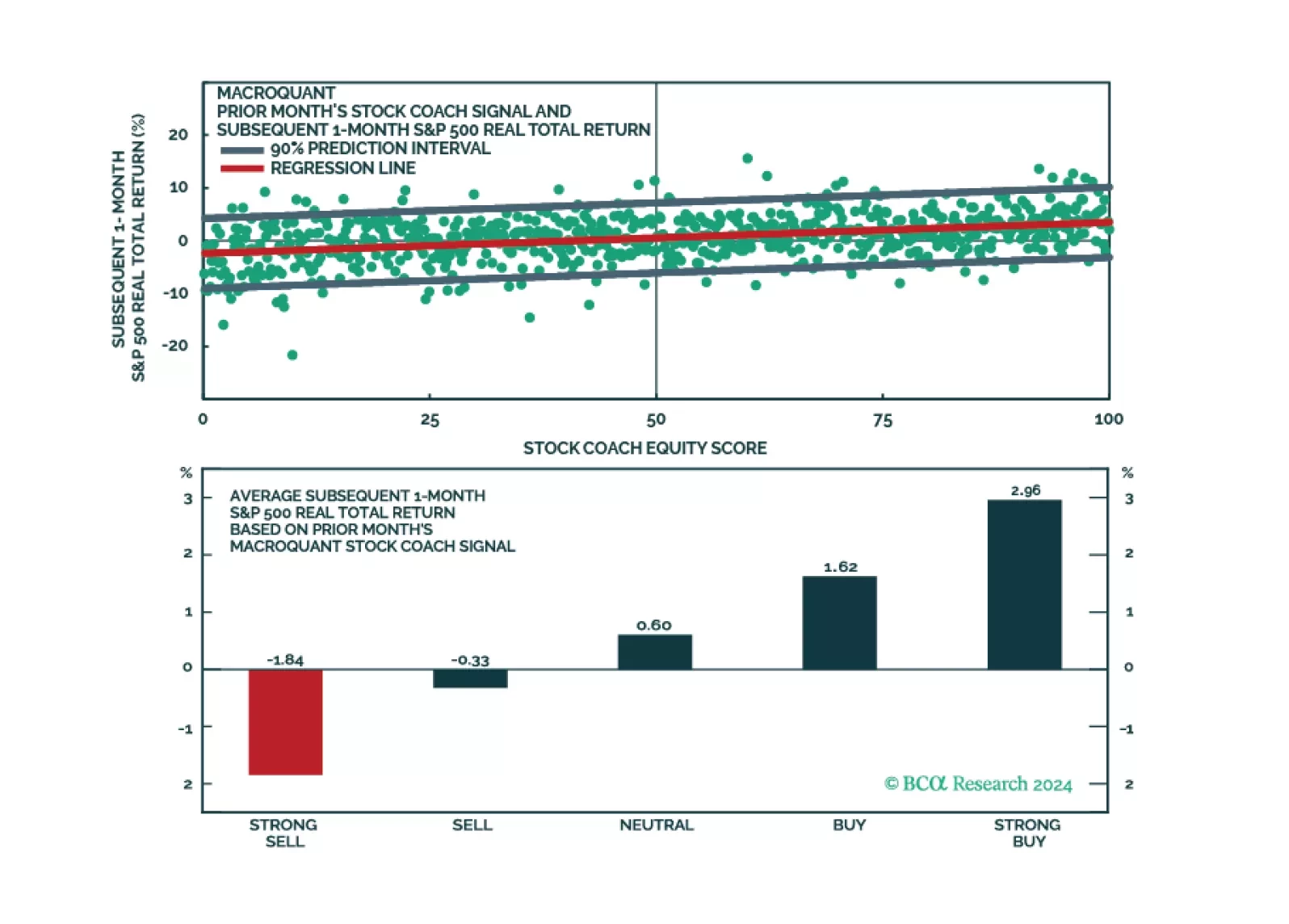

MacroQuant sees significant downside risks to stocks over a 1-to-3 month horizon and suggests increasing allocation to long-term bonds. The model favours defensive equity sectors but is also hedging its bets by overweighting materials.

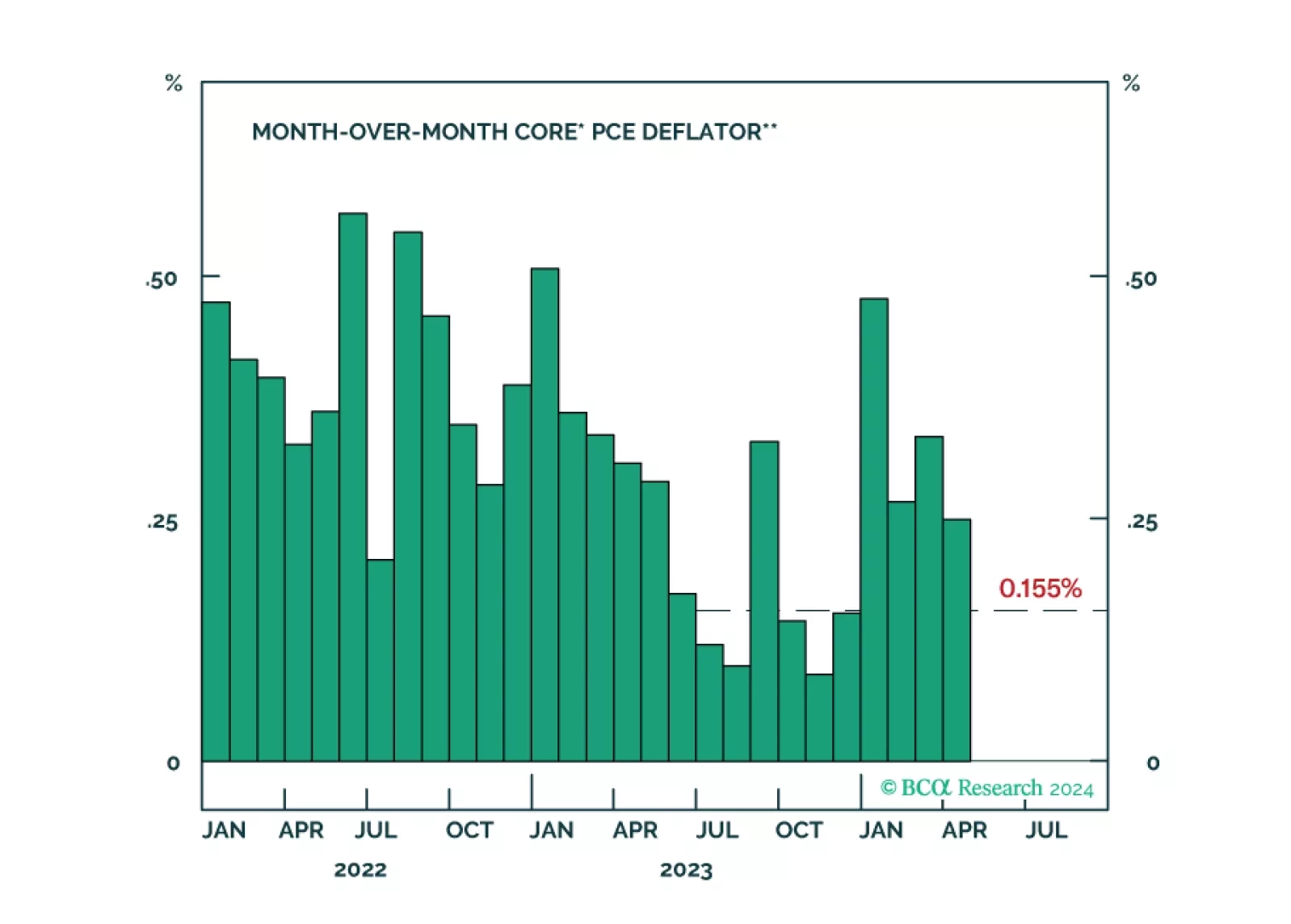

US nominal personal income growth decelerated from 0.5% m/m to 0.3% m/m in April, in line with expectations. However, nominal personal spending surprised to the downside, and contracted 0.1% m/m in real terms. Core PCE – the Fed’s favored inflation gauge –…

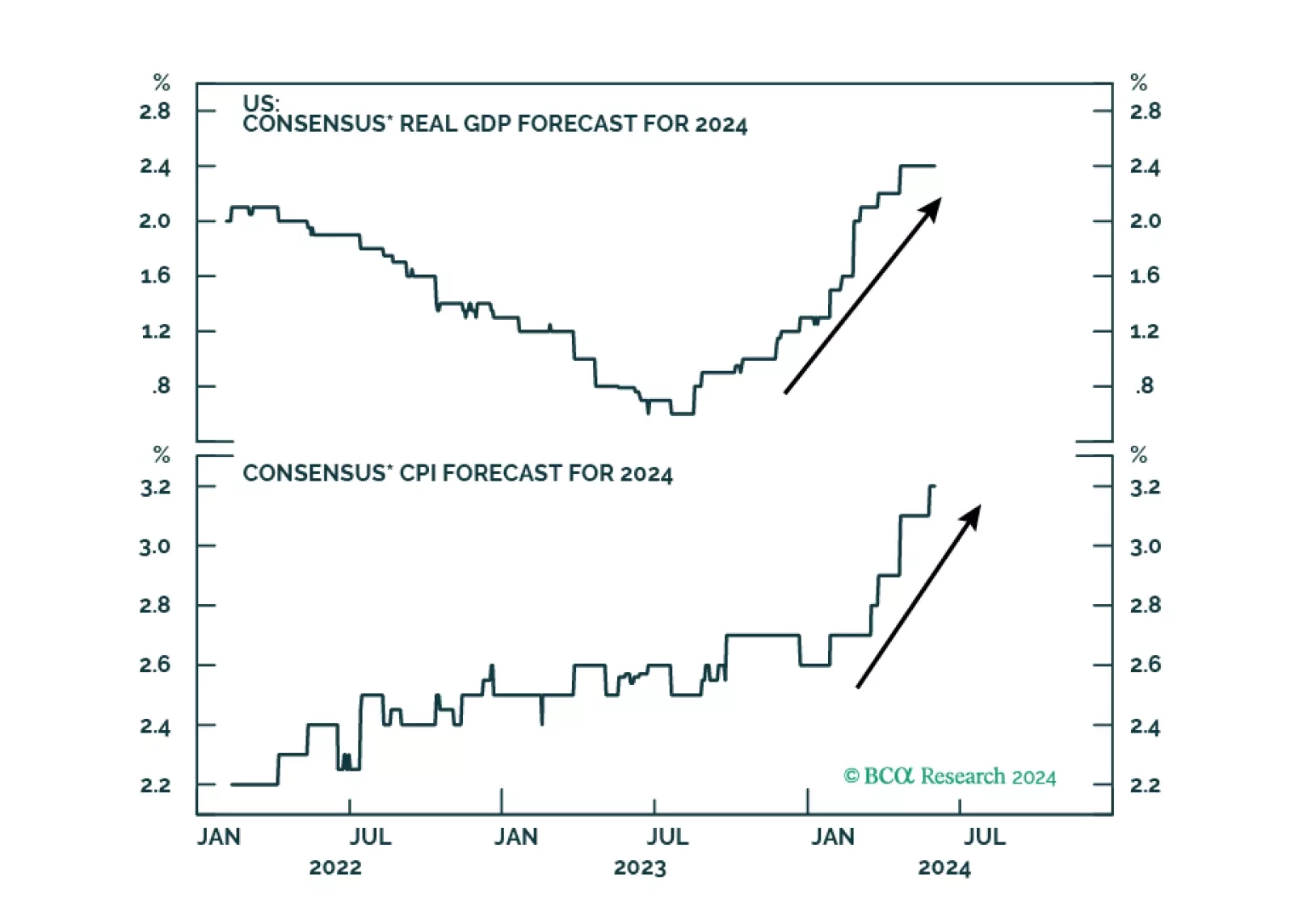

US Q1 GDP was revised lower from 1.6% q/q annualized to 1.3%. Notably, the downward revision to personal consumption was higher than expected, from 2.5% q/q annualized to 2.0%. Investment and government spending were revised higher. Real final sales to…