Economy

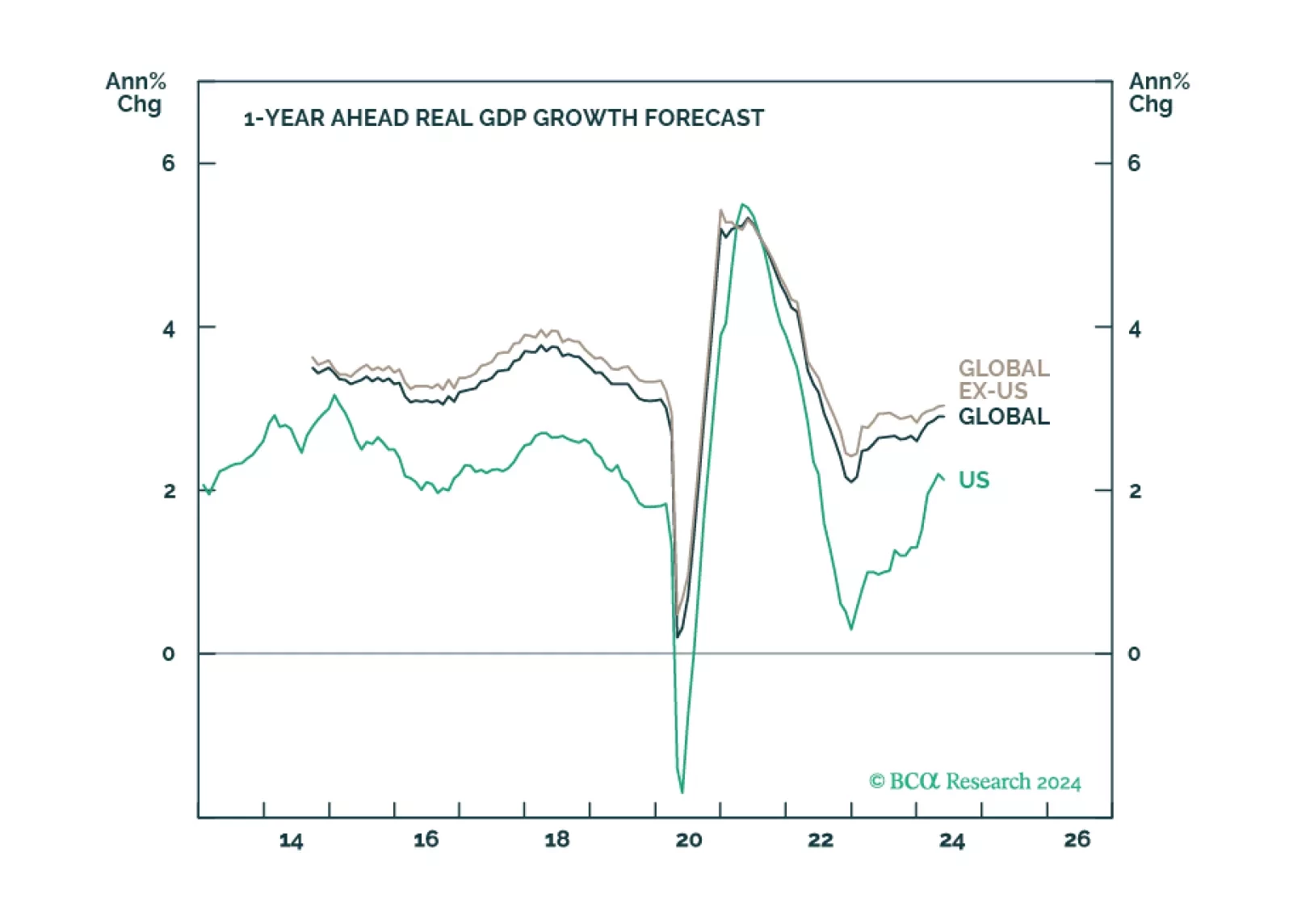

Looking at economic activity, global monetary policy seems restrictive, however, the behavior of financial markets tells a different story. What gives?

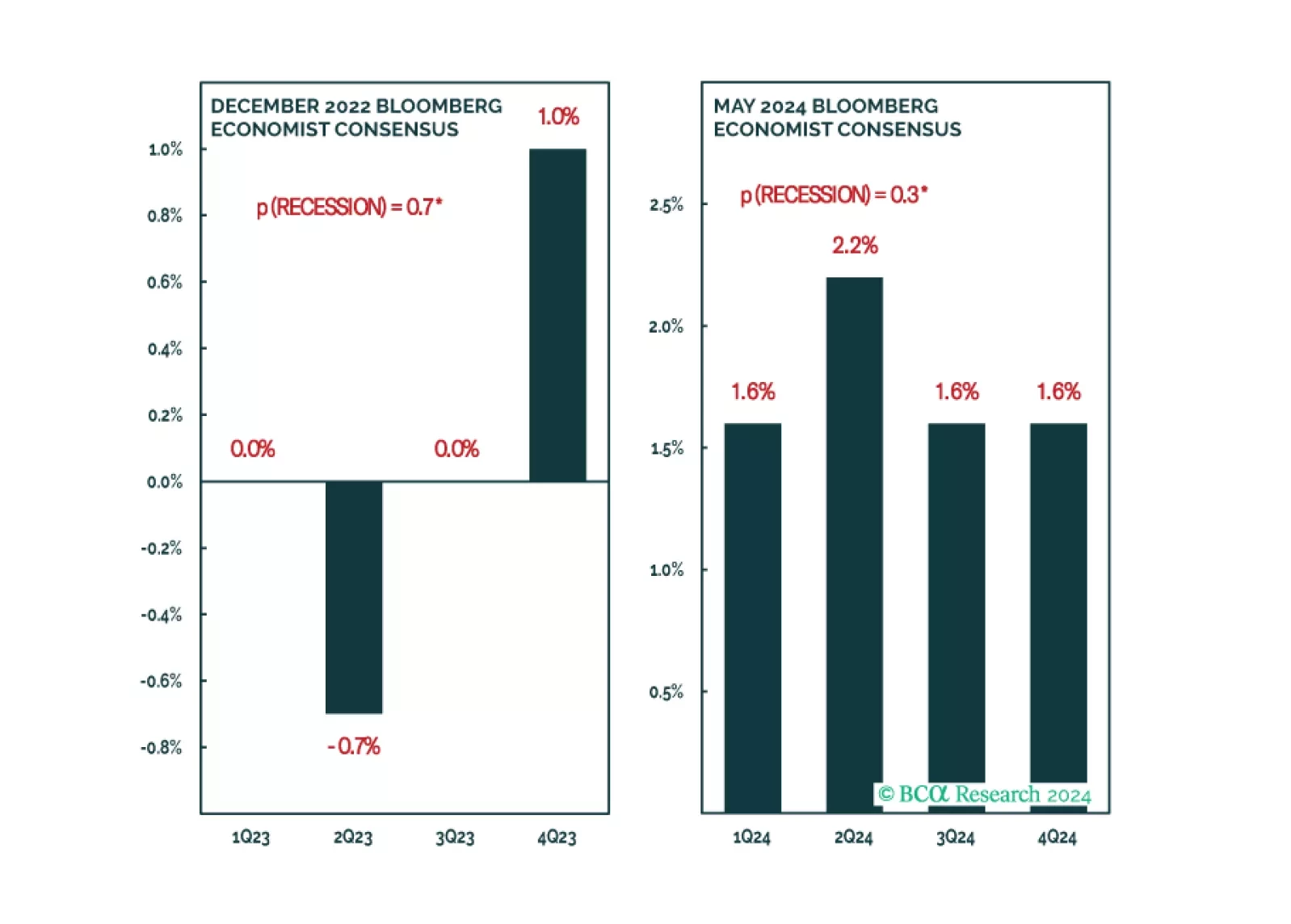

The signs of an approaching recession are starting to emerge. We will turn tactically defensive once they all fall into place.

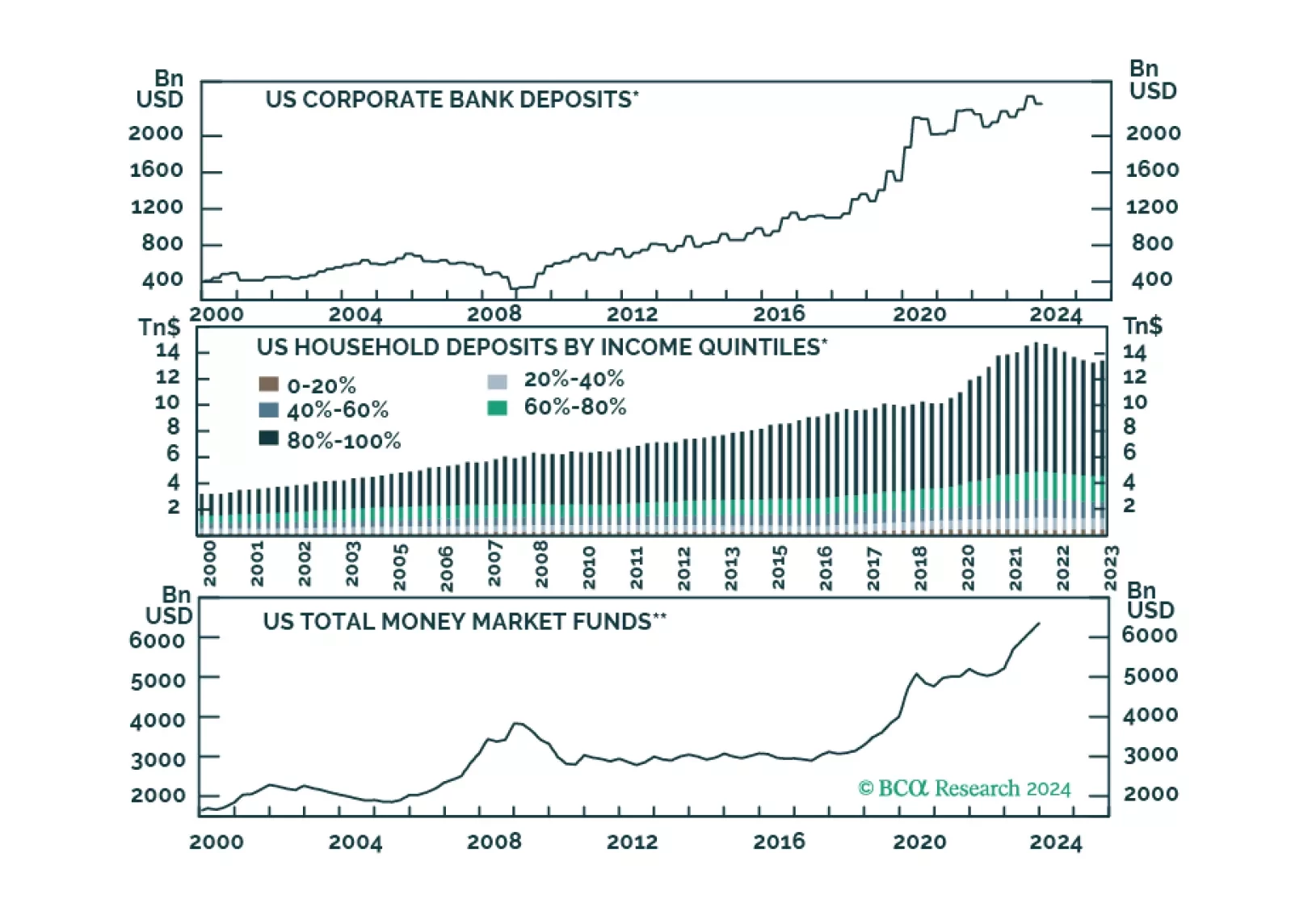

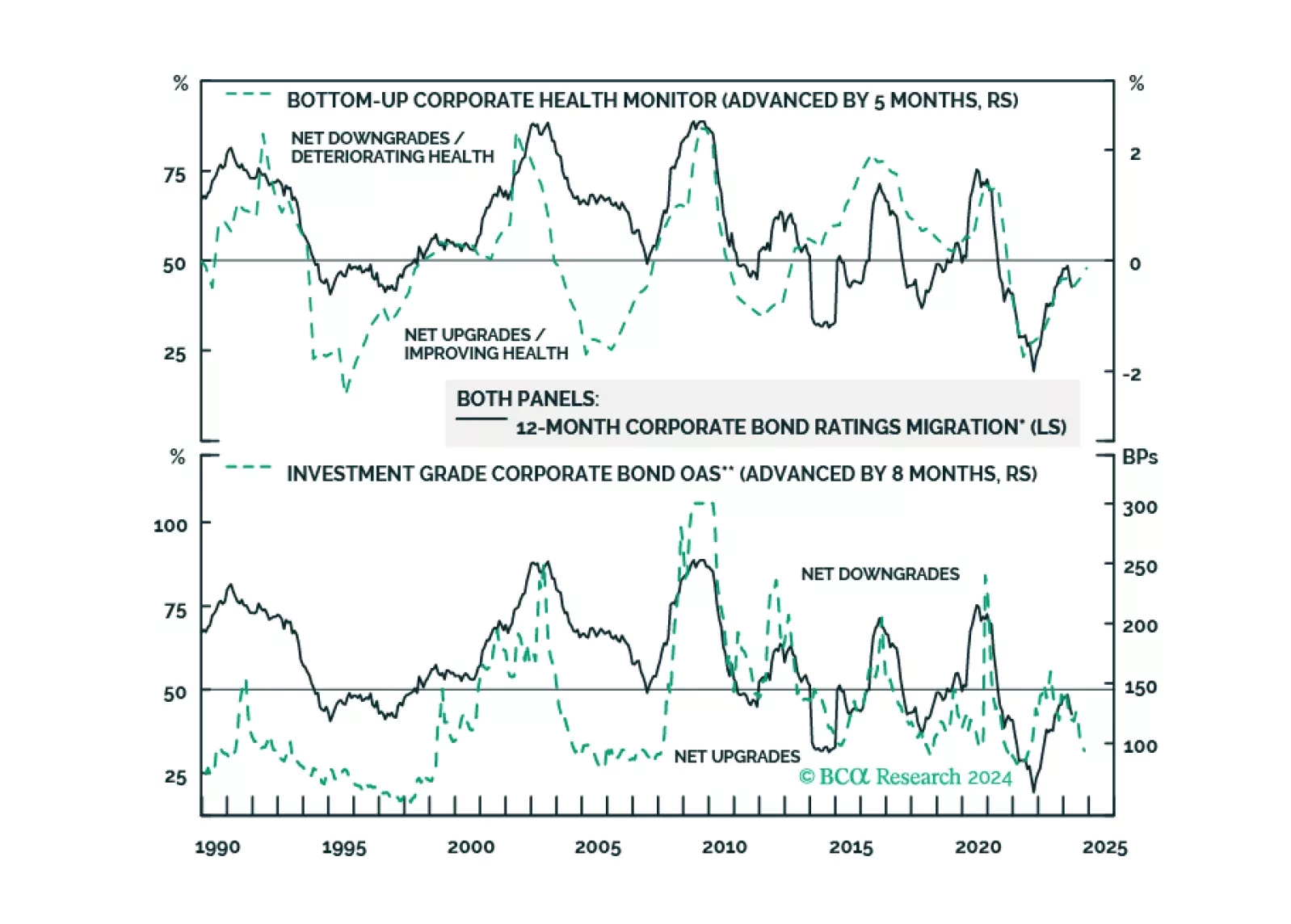

Nonfinancial corporate balance sheets are generally in good shape, but there are signs of deterioration at the bottom-end of the credit spectrum. We present evidence showing that credit deterioration at the bottom-end of the credit spectrum has a habit of migrating upwards.

There is a path to a soft landing, but it is a narrow one. We estimate that there is only a 20% chance that the US will avoid a recession before the end of 2025. We are currently neutral on global equities, but expect to downgrade stocks to underweight during the summer.