Economy

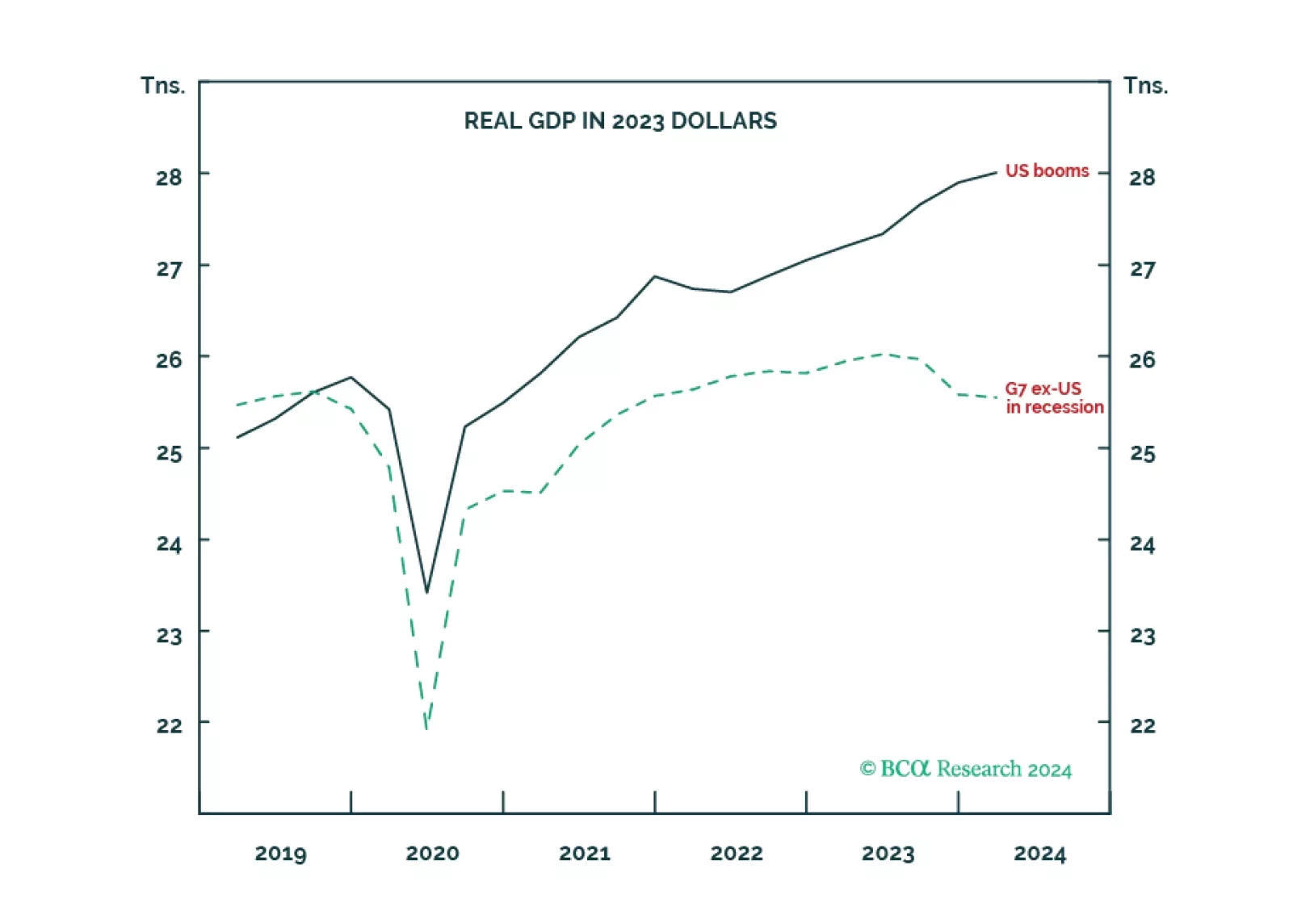

The economic schism in the world economy, between the non-US developed economy in recession and the US in strong growth, is unprecedented during our lifetimes. Now the schism will continue in reverse, as the non-US developed economy rebounds while the US fades. There are important implications for rates, the dollar, and sector and regional equity allocation which we discuss. Plus: base metals are a tactical short.

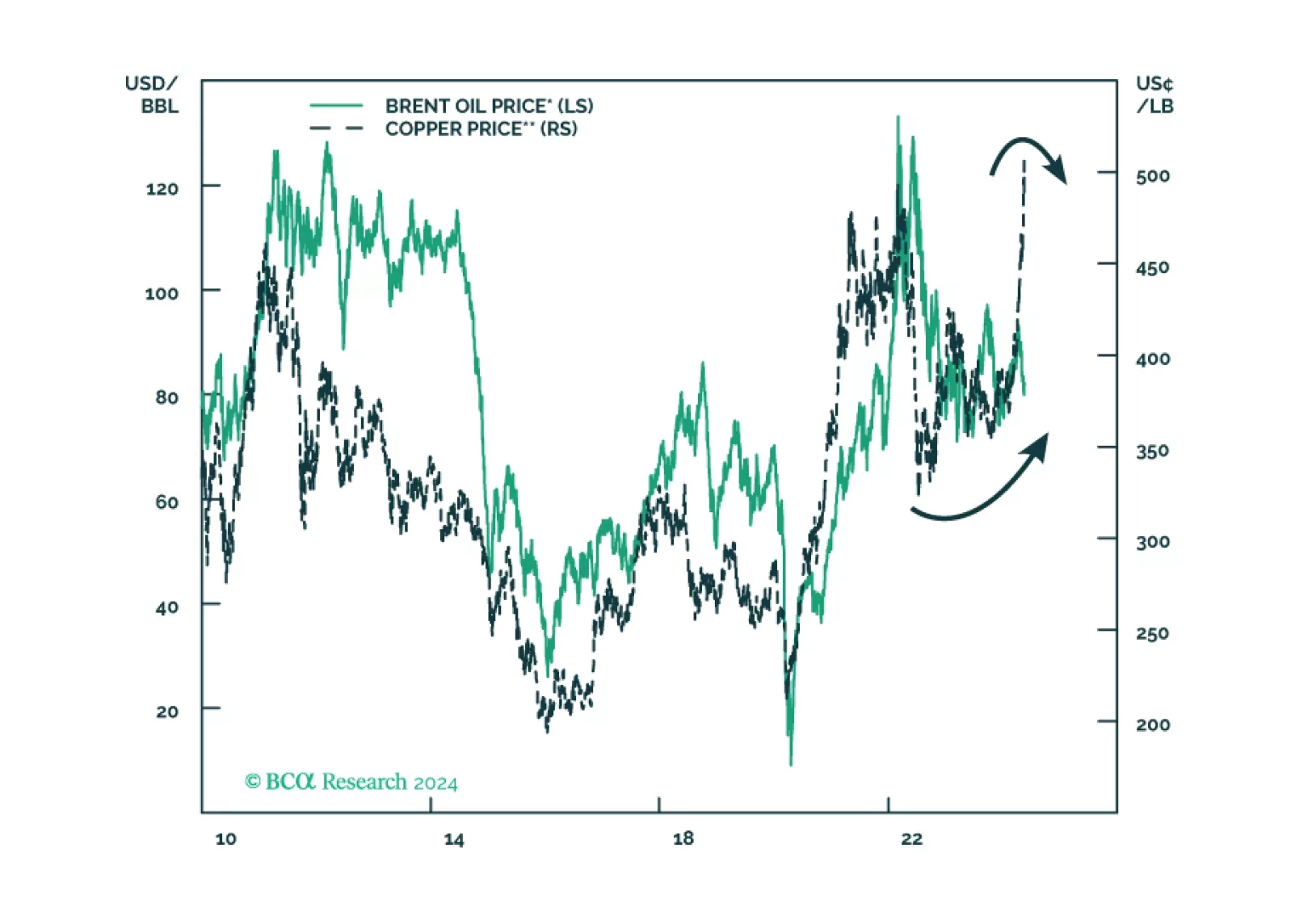

The death of the Iranian president reinforces our base case view of Middle Eastern instability and at least minor oil supply shocks. Rapid geopolitical developments in recent weeks are pointing to a new bout of global instability. The US is hobbled by its election. Conflicts with Russia, China, and Iran are all now escalating at the same time, at least marginally. Investors should reduce risk and shift to more defensive assets, markets, and sectors.

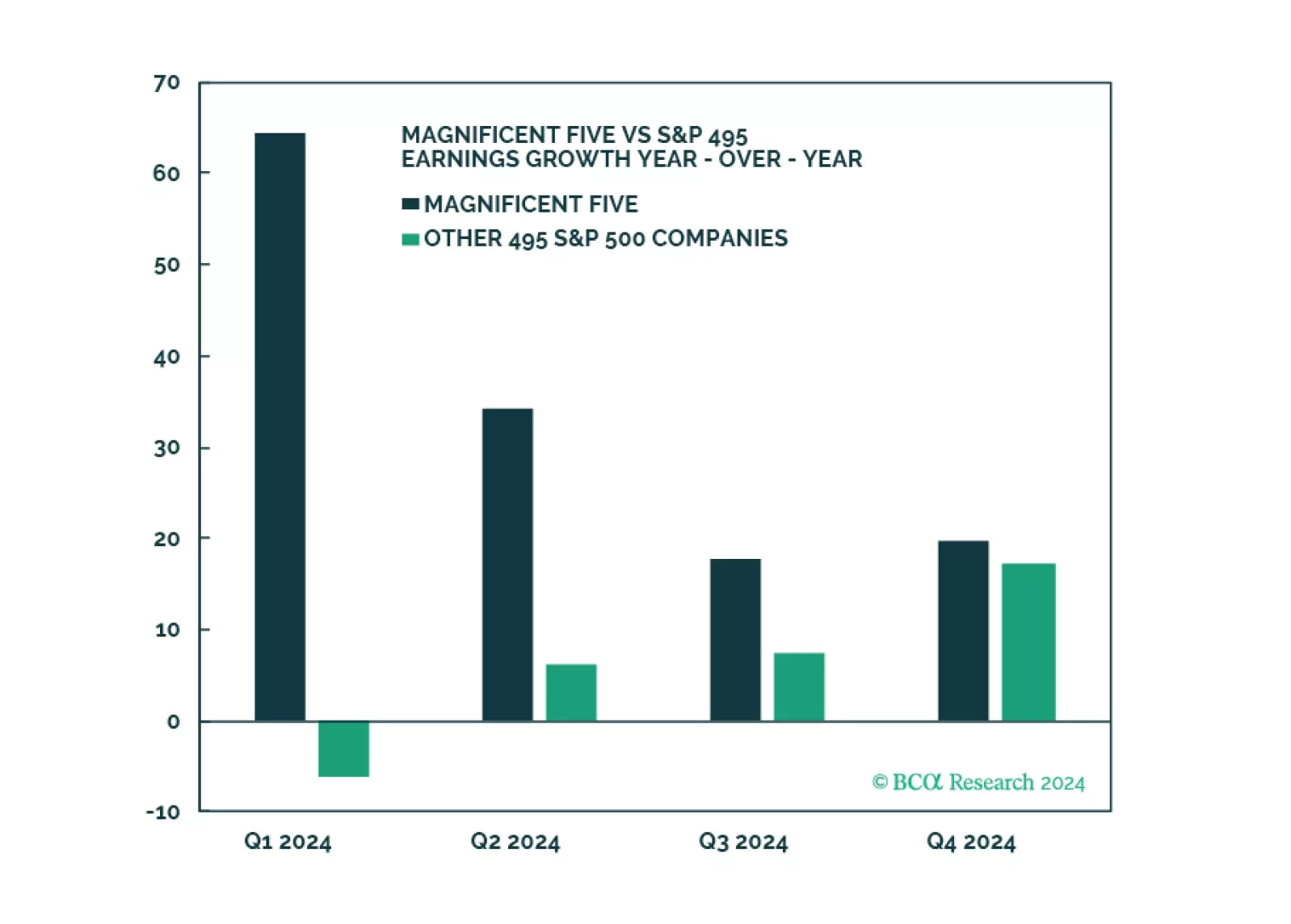

Q1 Earnings and sales growth were strong, but the devil is in the details: Without the Magnificent Five, earnings growth for the index would have been negative. On a positive note, margins have stabilized, and earnings growth is expected to broaden into yearend. Companies are optimistic about the economy. Development of AI applications is in full swing, but few companies are monetizing them yet. Consumer spending is strong but is slowing. We reiterate our underweight of consumer sectors, and overweight of Software and Services as the “don’t fight AI” adage holds.