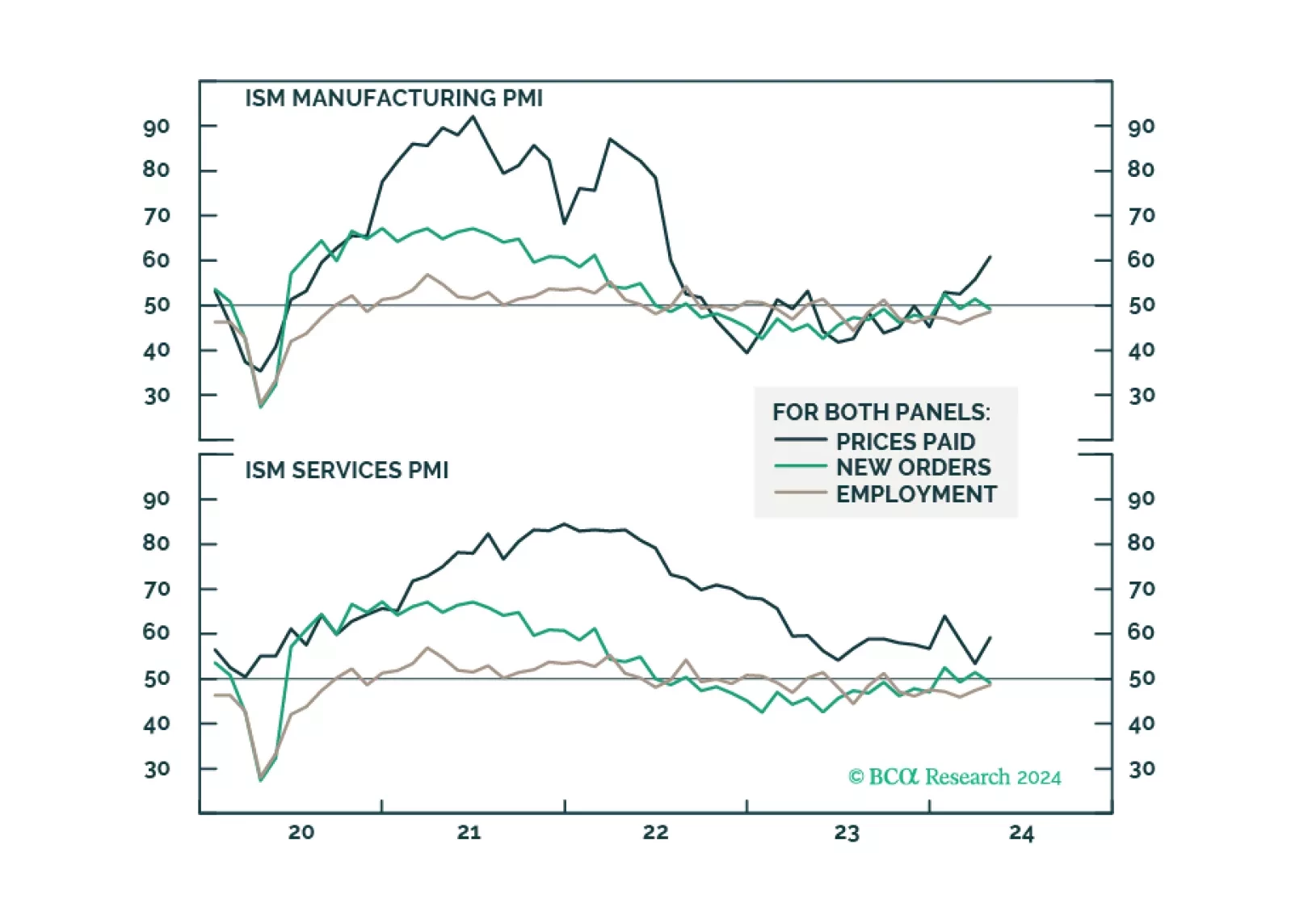

Economy

The broad market took a significant step backward in April, as market jitters gripped investors, stoking fears of higher for longer monetary policy. However, our roundtable investor poll has demonstrated that the majority remain constructive on equities, and have plenty of cash ready to be invested, which could prolong the rally. Economic data is deteriorating while inflation is stubborn. However, so far, bad news is good news as many believe that a “Fed put” is still on.

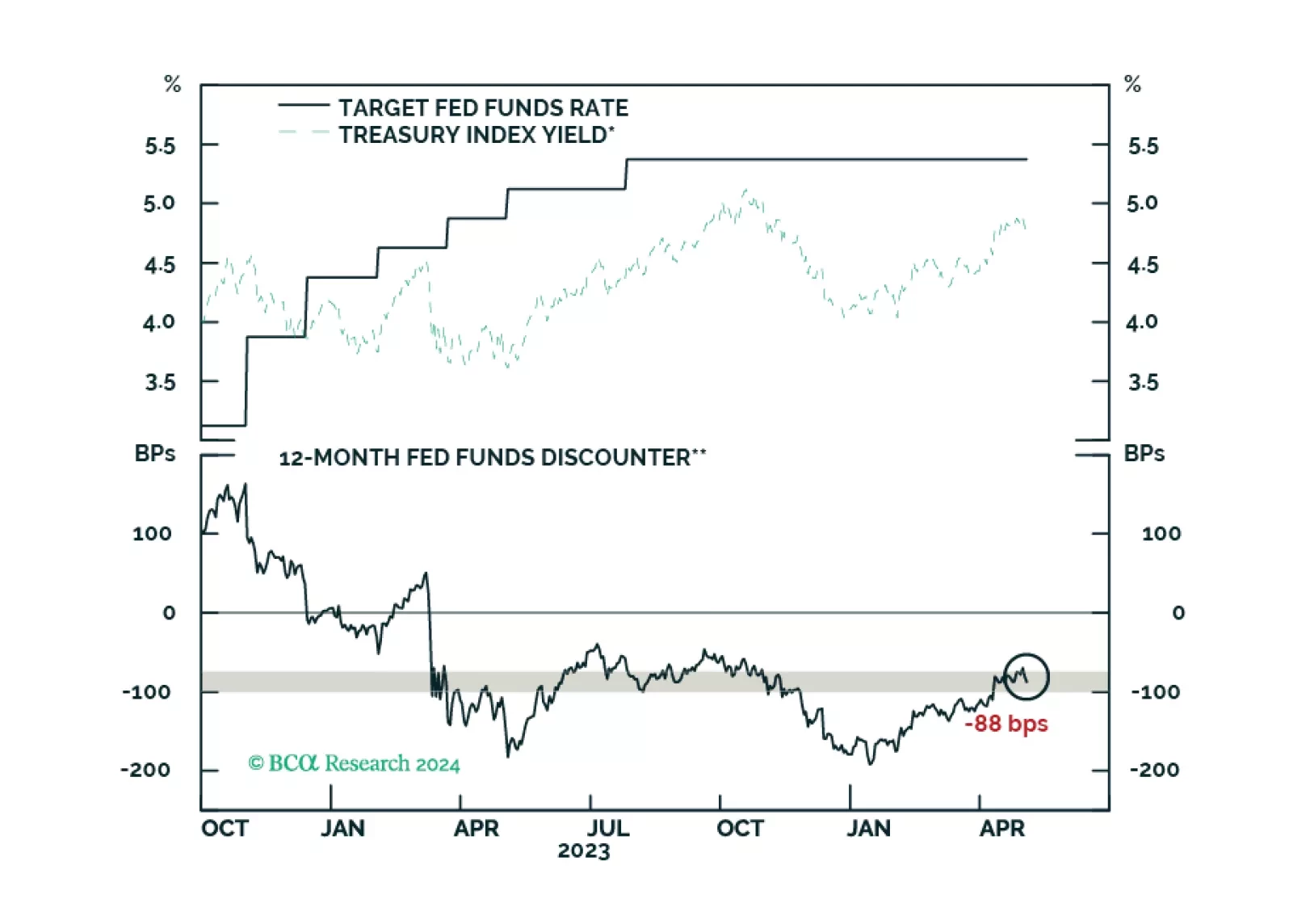

Some thoughts on this morning’s employment report and recent trends in US economic data.

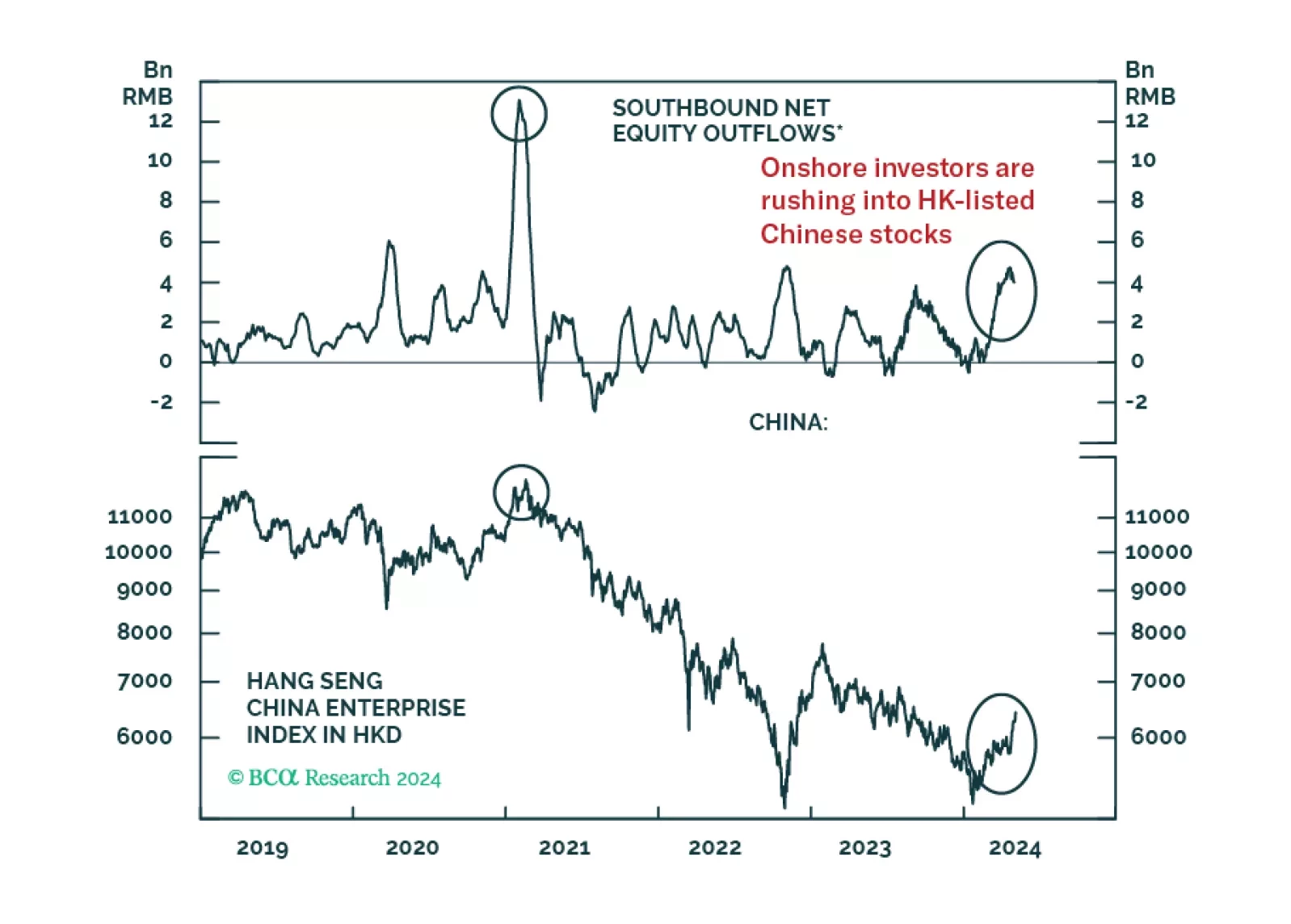

Mainland residents’ investments in gold, other metals, and Hong Kong-traded stocks are a form of capital outflow. Chinese authorities will counter any excessive capital flight with stricter administrative controls. Thus, markets benefiting from these flows will likely be hurt.

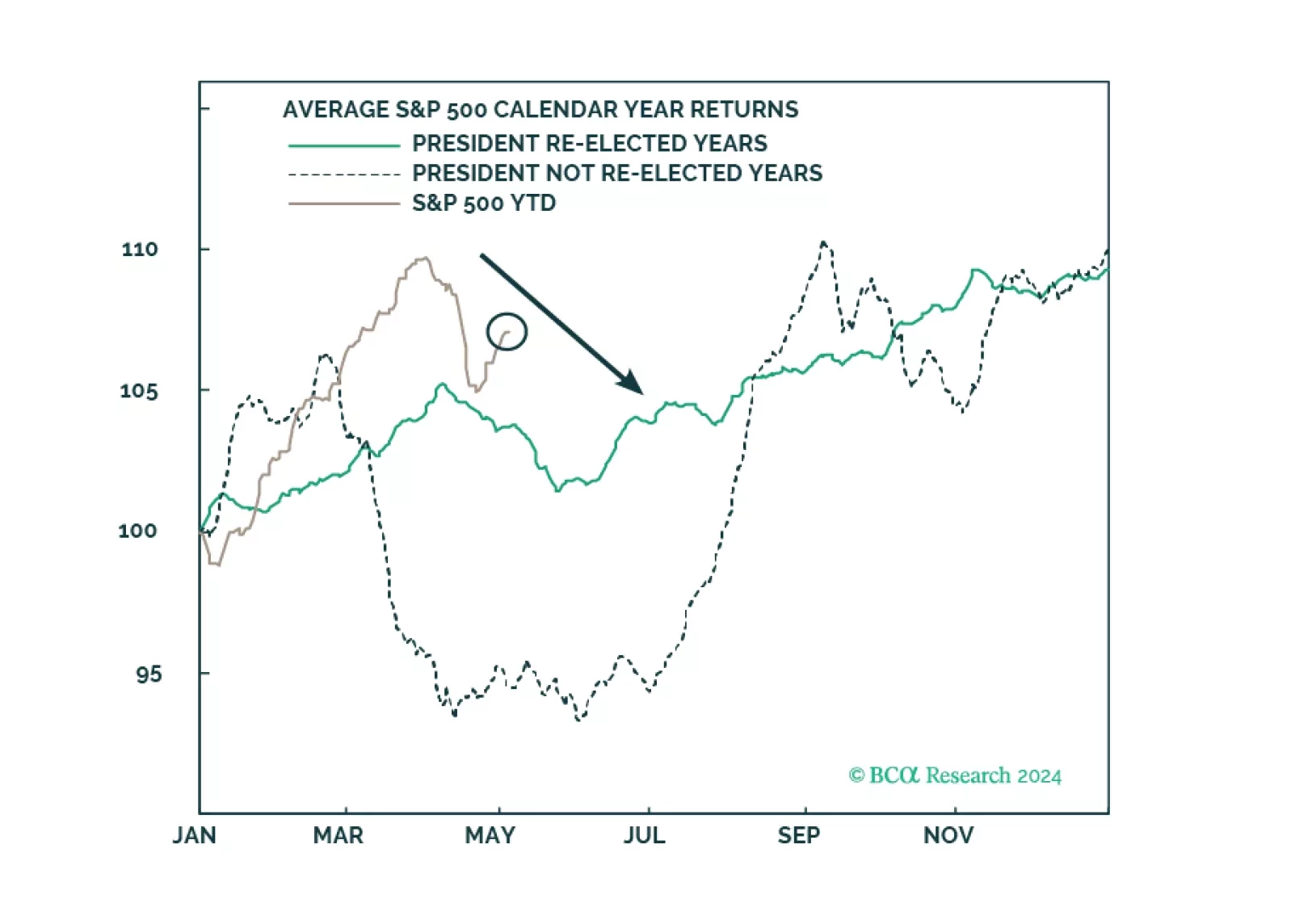

Investors should prepare for economic data to weaken even as policy uncertainty and geopolitical risk skyrocket ahead of the US election.