Economy

As expected, the Governing Council of the ECB kept interest rates unchanged on Thursday. In its statement, the ECB reiterated that most measures of underlying inflation were easing, wage growth was moderating, and firms were absorbing the rise in labor costs…

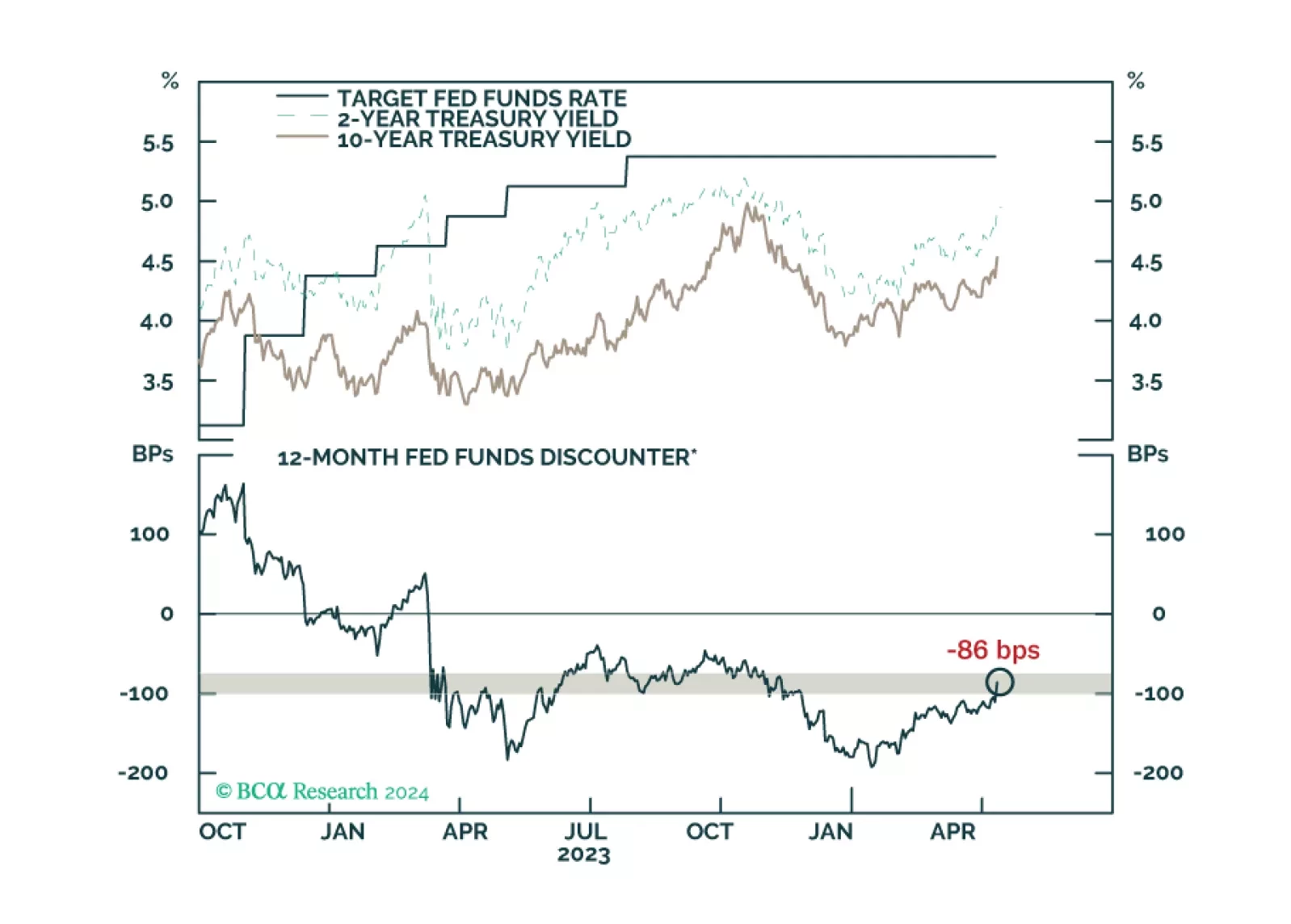

In terms of interest rate bets, markets are now roughly neutral on whether the Fed or Bank of Canada move the most in the next 12 months. BCA Research’s Foreign Exchange Strategy service’s bias is that it will be the BoC (with more cuts). Thus, a…

In this insight, we calibrate our investment views based on the latest Bank of Canada decision.

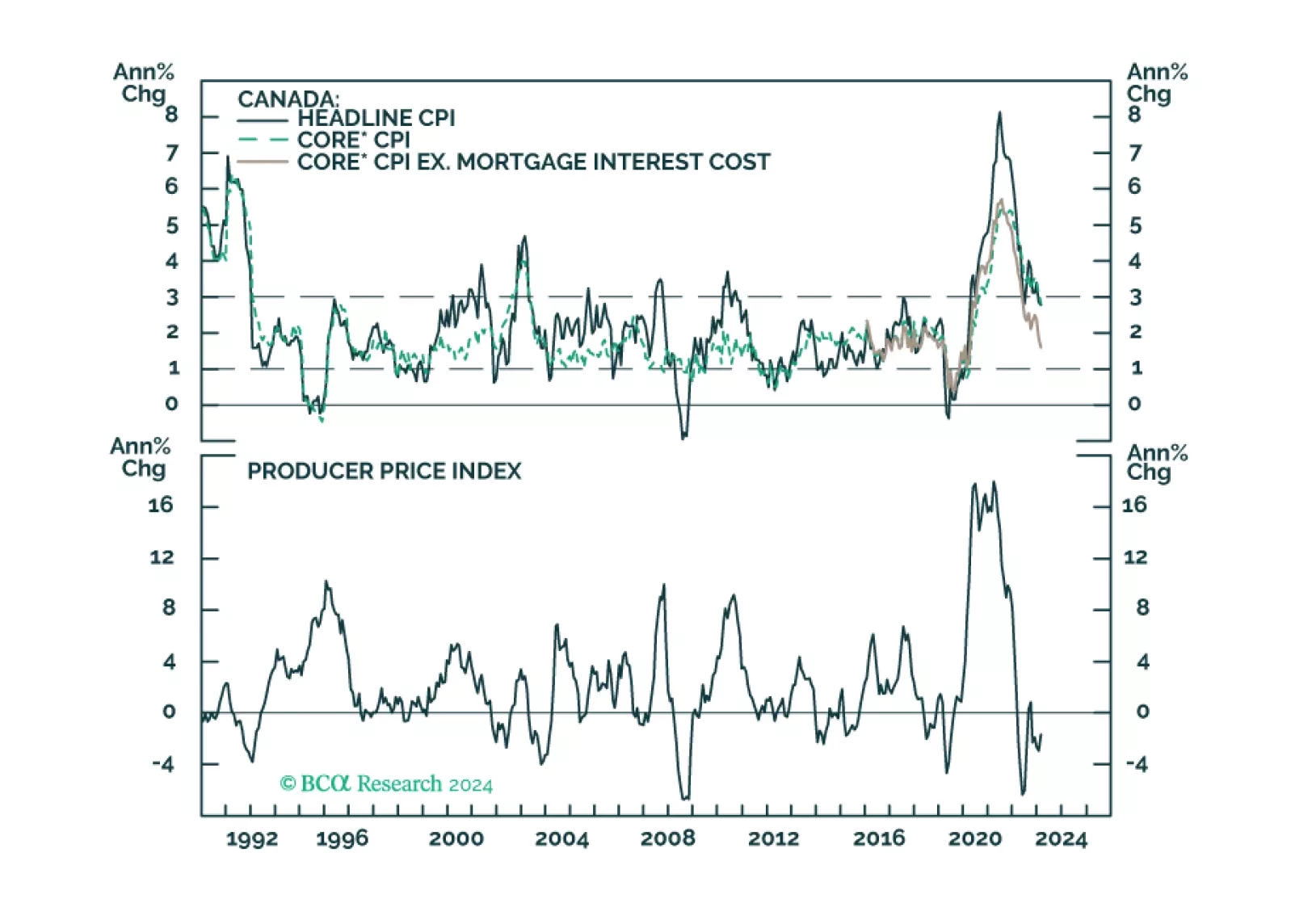

Headline inflation came in at 0.4% on a MoM basis and 3.5% on an annual basis, beating expectations of 0.3% and 3.4% respectively. Meanwhile core inflation came in at 0.4% on a MoM basis and 3.8% on an annual basis, beating expectations of 0.3% and 3.7%…

The Bank of Canada held its policy rate steady at 5% on Wednesday, in line with expectations. In his opening remarks following the announcement, Governor Tiff Macklem was cautiously dovish: “We don't want to leave monetary policy this restrictive longer…

Global material stocks have underperformed over the past 12 months, returning only 11.3% vs 21.4% for the overall market. But could they be a buy now? There are several arguments to argue that they will: The ISM has begun to stabilize and seems to be…

According to BCA Research’s US Equity Strategy service, rising inflation benefits Utilities, Energy, and Materials, and is a headwind for the Consumer Discretionary sector. After a protracted bout of underperformance, the Energy sector has rebounded …

Our reaction to this morning’s CPI report and bond market moves.

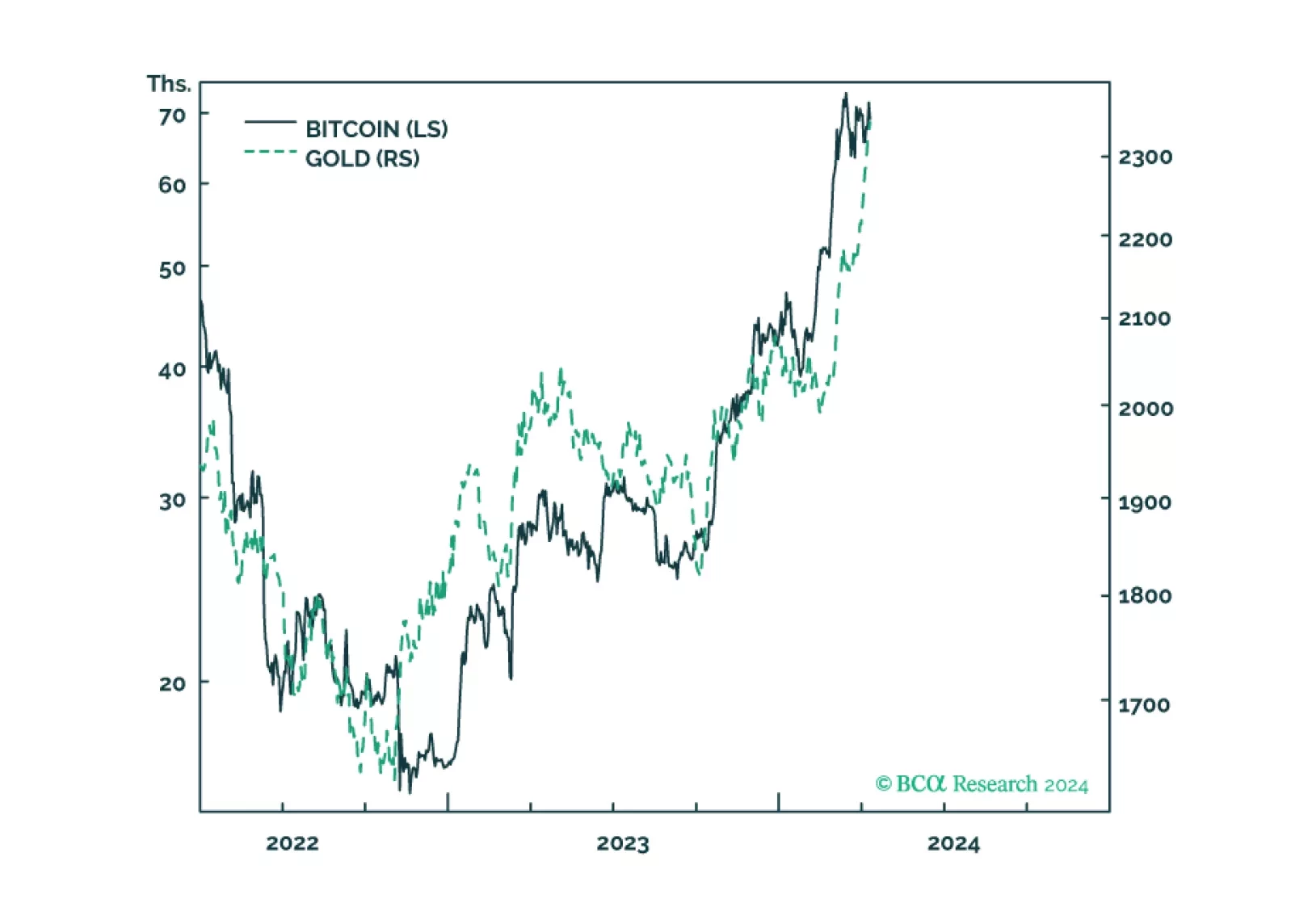

Gold and bitcoin are conceptually joined at the hip because the value of both comes from their ‘non-confiscatability’ by inflation, by bank failure, and in the case of bitcoin, by state expropriation. The sharp recent rallies in both gold and bitcoin reflect that the market has suddenly upped the value of non-confiscatability, and a plausible explanation is that recent US inflation data show that the journey to sustained 2 percent inflation has stalled, raising the risk that the Fed might balk at finishing the journey. Plus: JPM, CL, and USD/CHF are tactical reversal candidates.

The NFIB’s small business optimism index decreased by 0.9 points to 88.5 in March, missing expectations of 89.9, and reaching its lowest level since 2012. A few things stood out from the report: Labor market dynamics continue to slow. The net percent…