Economy

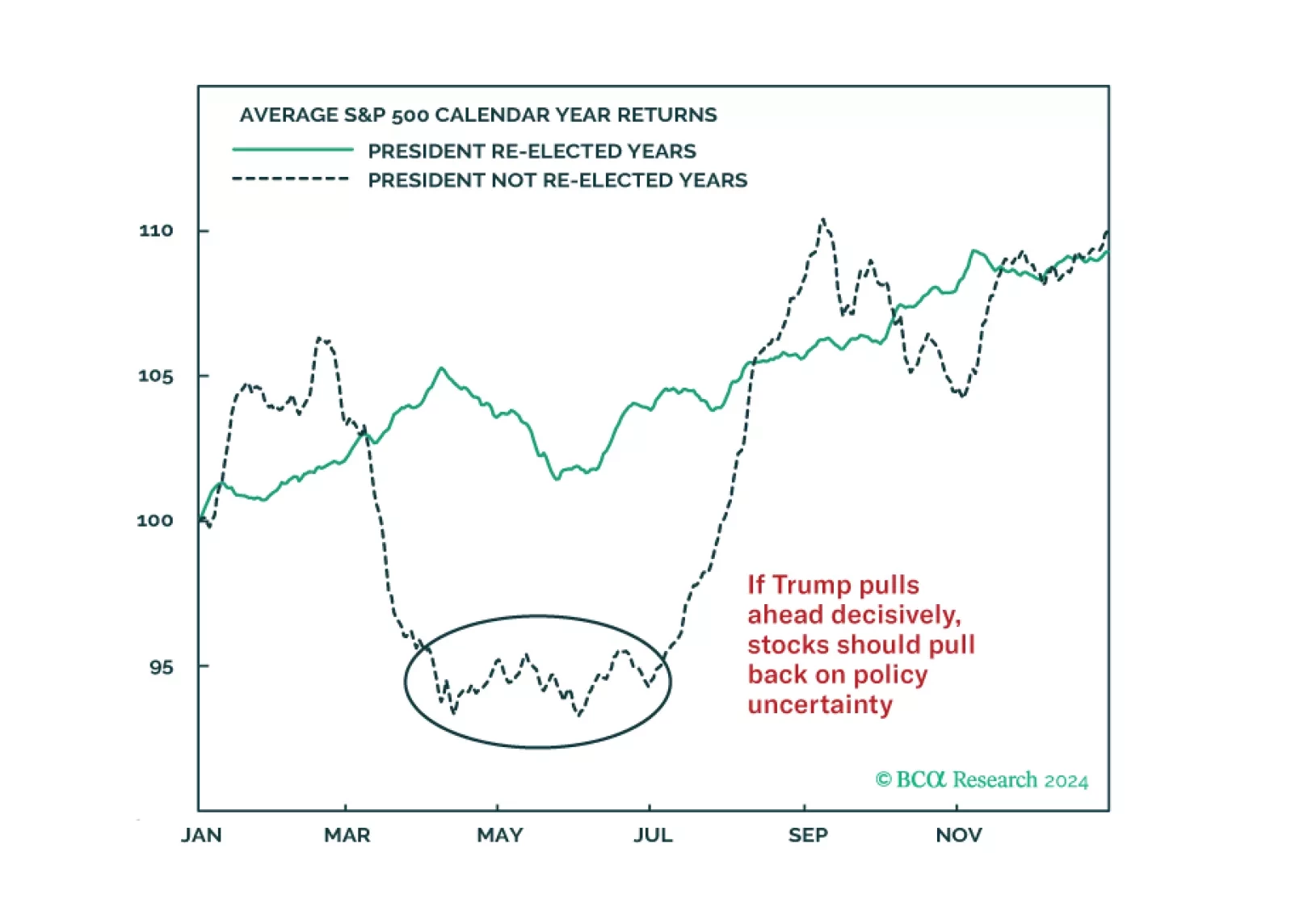

Investors around Europe and North America are concerned that the stock market is increasingly overbought and vulnerable to exogenous risks. We agree and have good reasons to fear that festering geopolitical risks and the US election season will deal negative surprises.

We expand our risk/reward analysis of US investment grade corporate bonds to focus on the 44 industry groups included in the Bloomberg index.

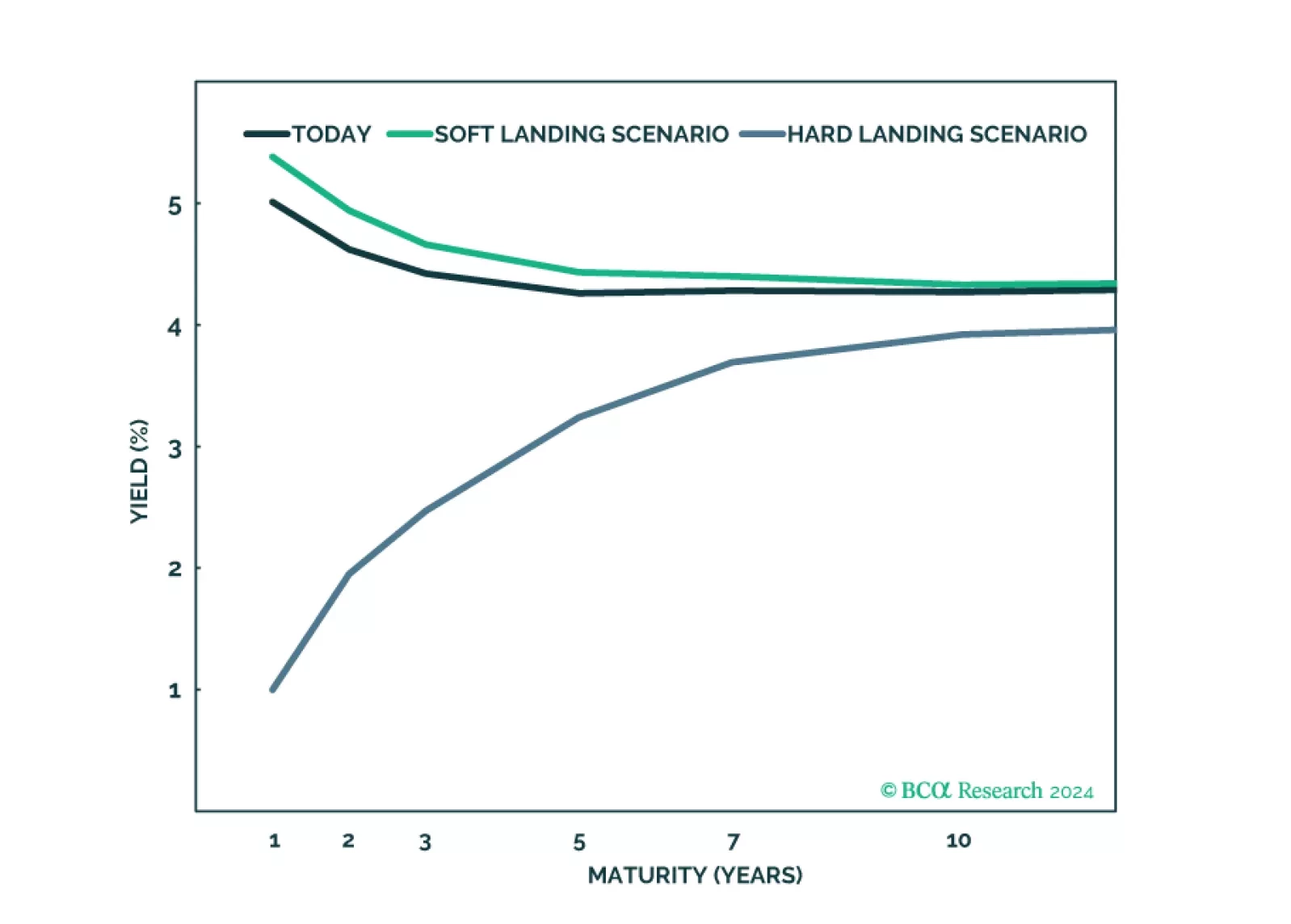

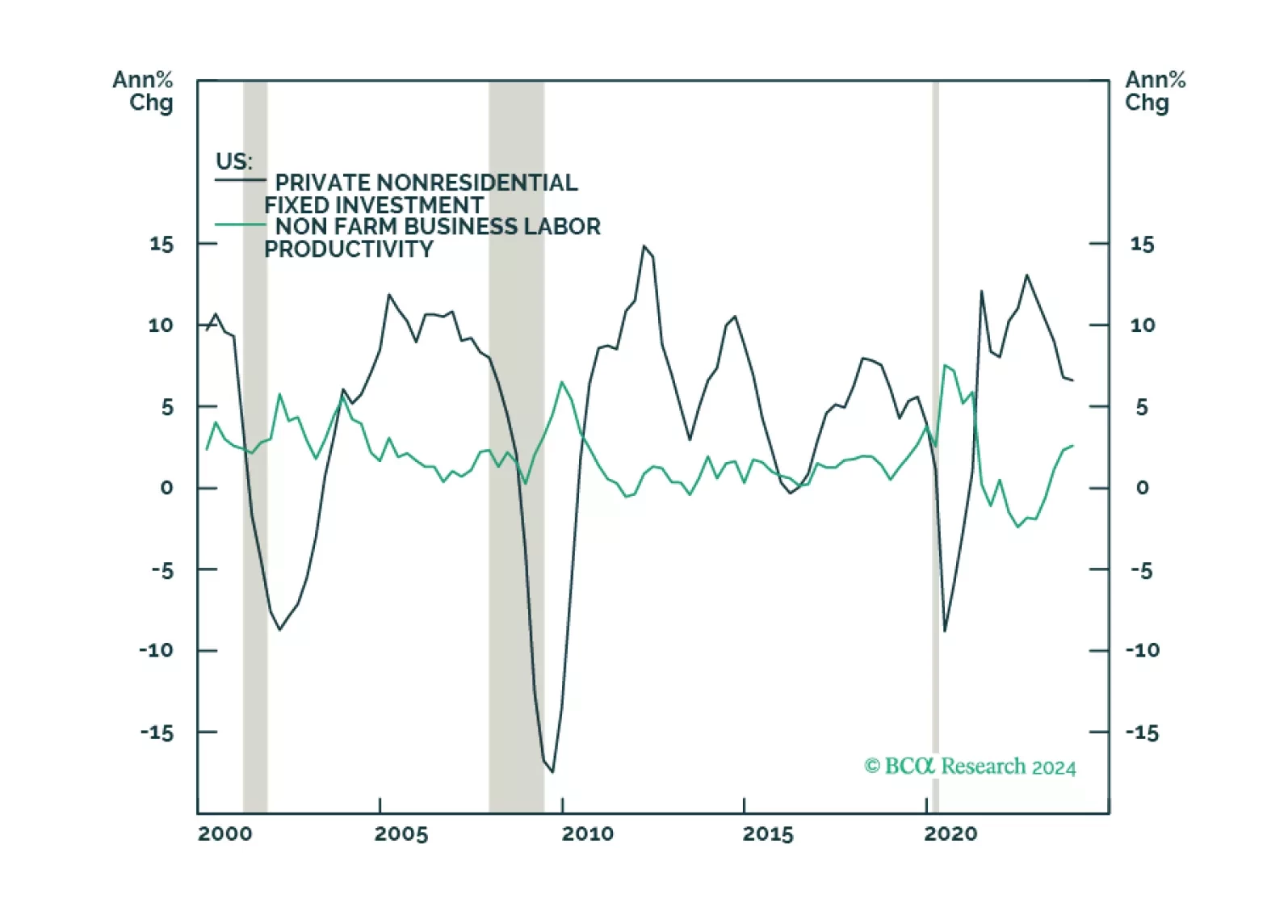

Inflationary pressures this year will remain subdued as labor-productivity growth – driven by strong capex and R+D spending – continues. This will make the Fed more confident in beginning its policy-rate-cutting cycle in June, and will keep gold well bid. We are raising our gold target to $2,300/oz. We continue to expect no recession this year.

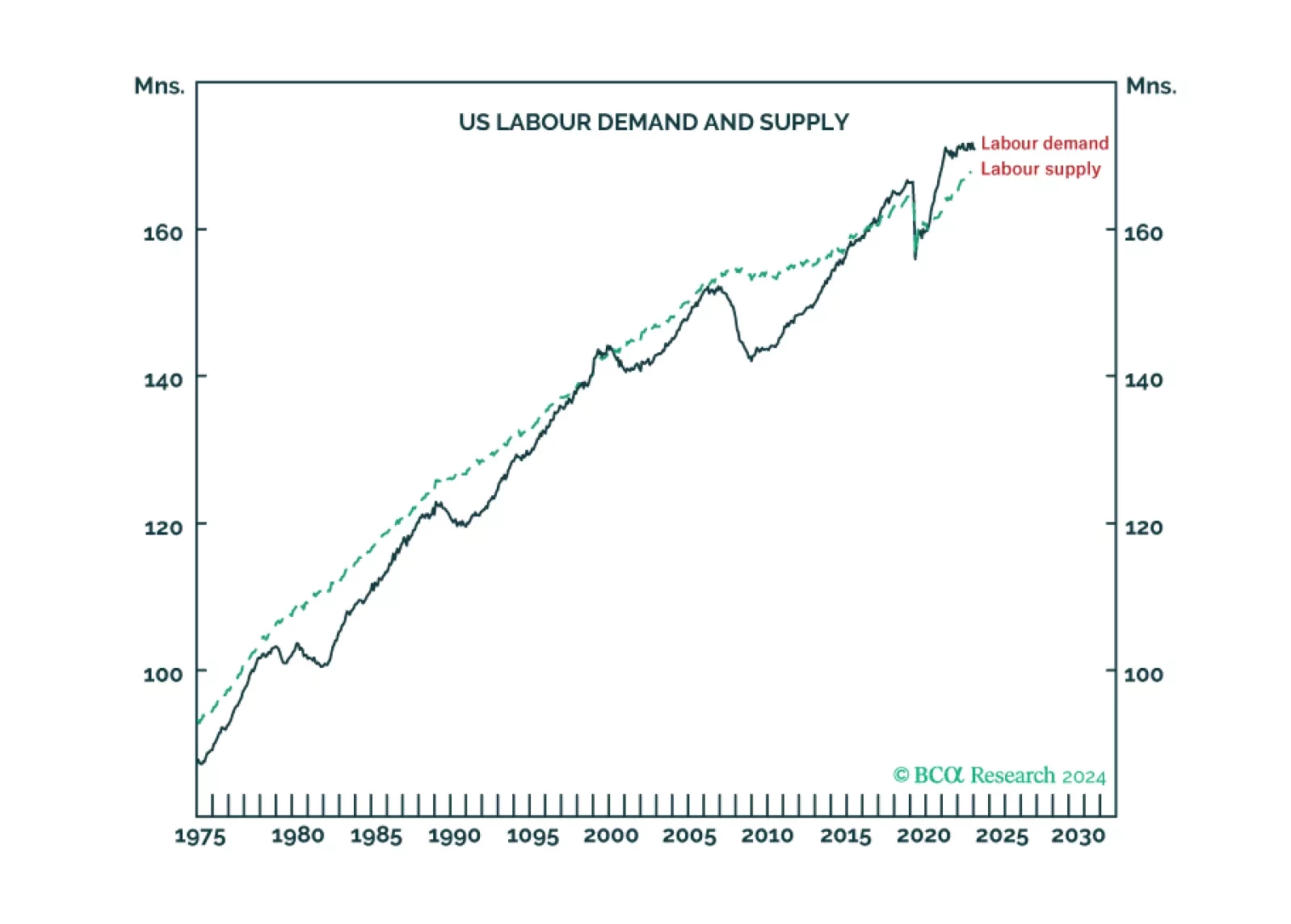

For the first time in at least fifty years, US labour supply is running well below labour demand, meaning the US economy is ‘inverted’. We discuss how and why the economy inverted, and what it means for recession, inflation, and asset allocation. Plus: NVDA is at a consolidation point.