Economy

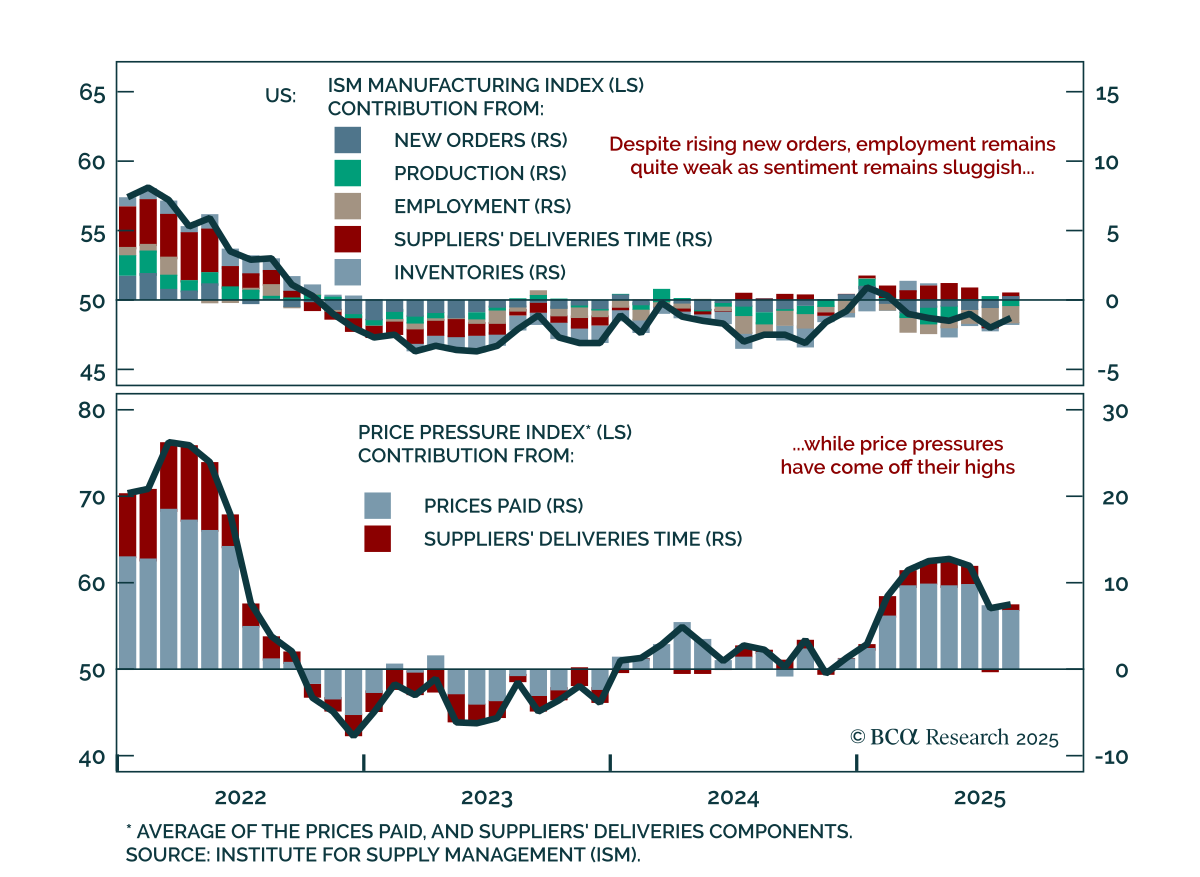

August ISM Manufacturing was mixed, with stronger orders offset by weak production and employment. The headline rose to 48.7 from 48.0, missing expectations. New orders beat estimates, rising into expansion at 51.4 and lifting the New…

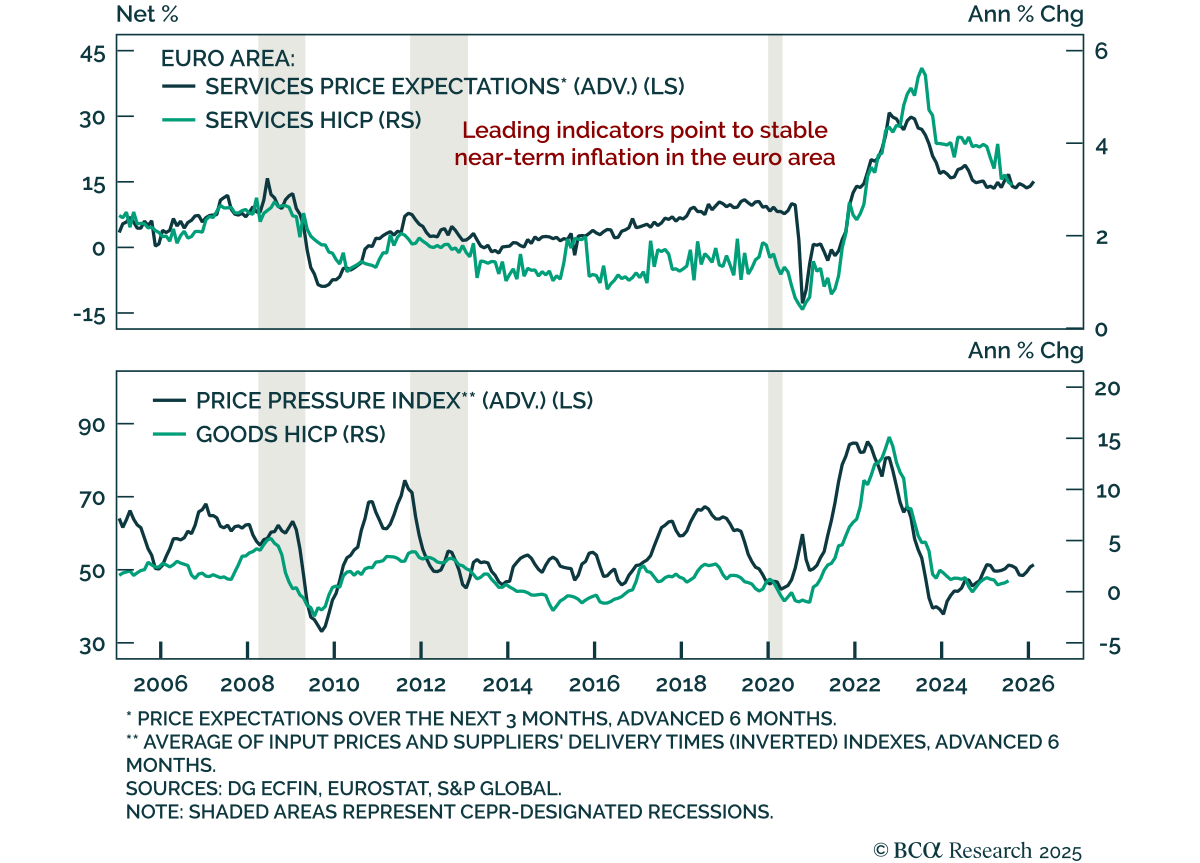

Euro area August flash HICP was slightly hotter than expected, reinforcing the case for the ECB to stay put in September. Headline inflation rose to 2.1% y/y from 2.0%, with the monthly print surprising at 0.2% m/m. Core inflation held at 2.3% y/y despite…

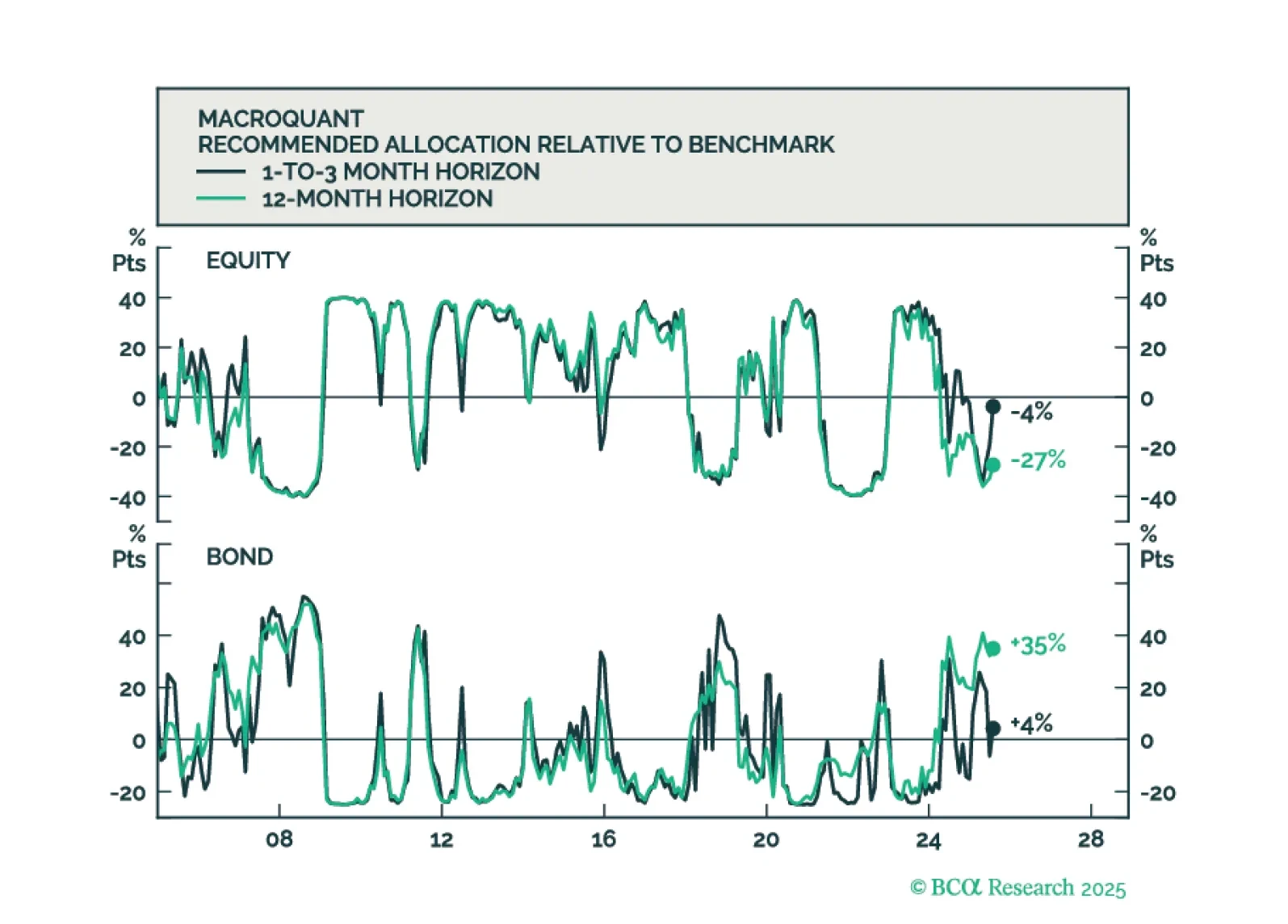

MacroQuant sees downside risks to stocks over a long-term horizon but is not yet saying that we are at imminent risk of an equity bear market.

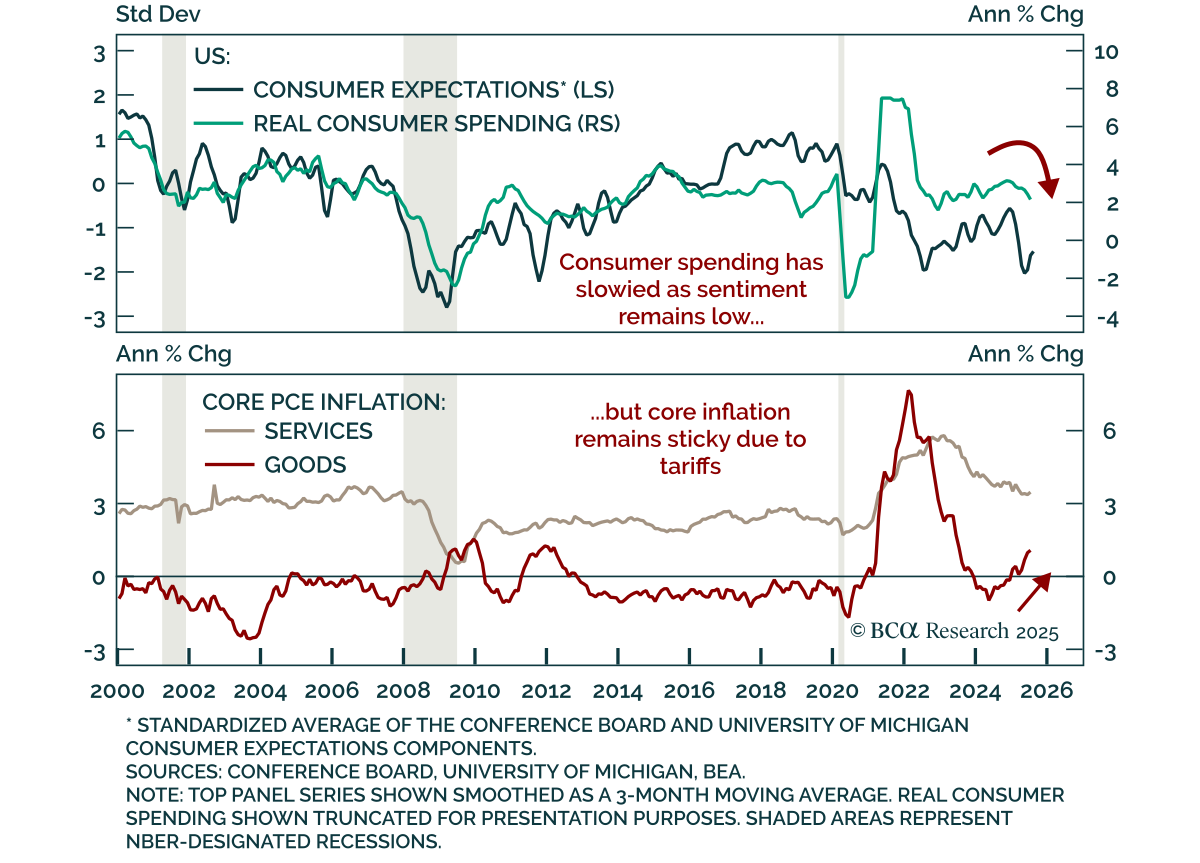

July income and spending data confirmed resilient consumption and sticky inflation, however, slowing labor momentum keeps us defensive. Real personal spending increased 0.3% m/m. Personal income rose 0.4% m/m, with real income ex-transfer payments…

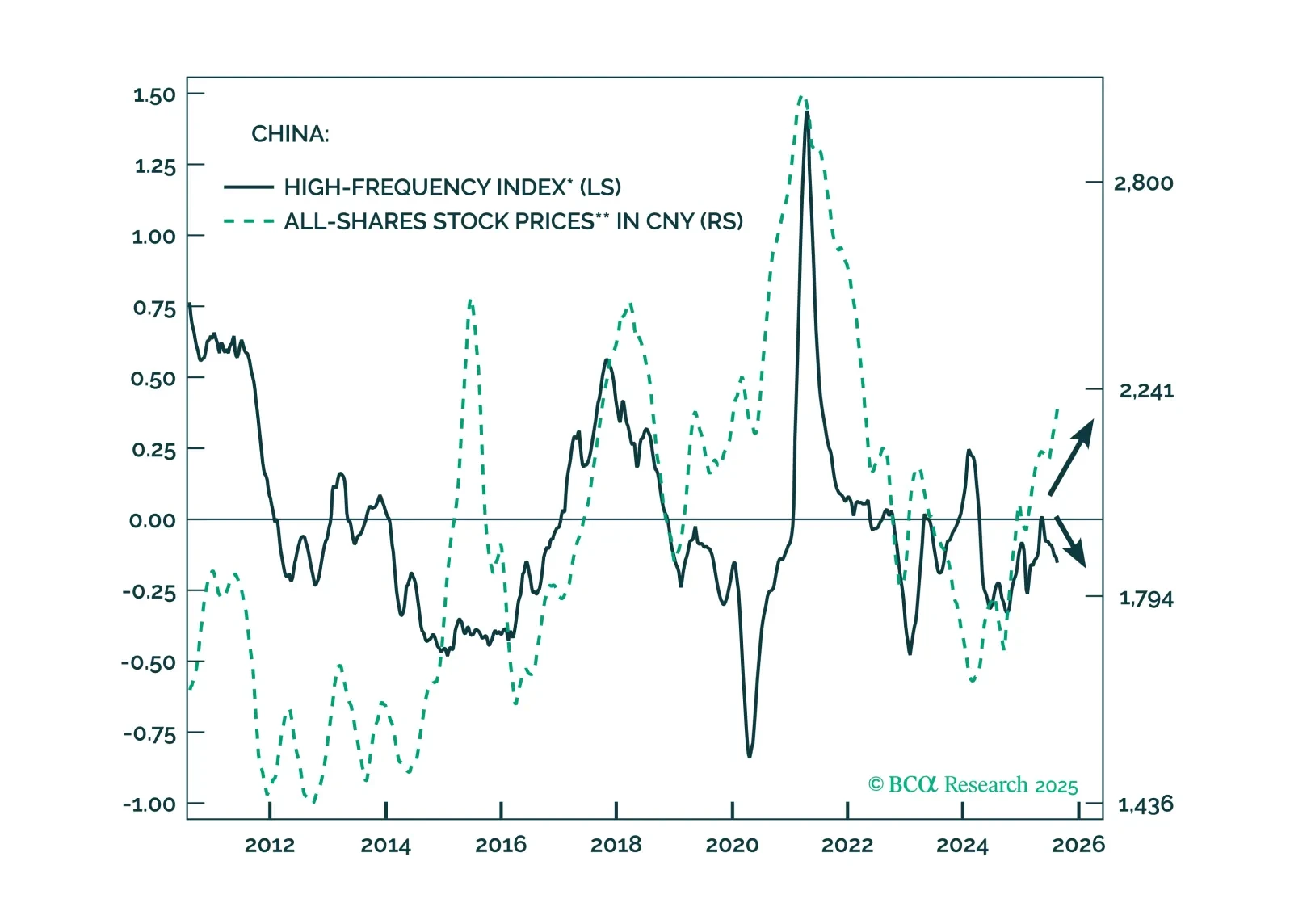

In this week’s Special Report, we introduce our newly constructed China High-Frequency Index (HFI). The HFI provides a timely measurement of China’s current economic conditions, helping investors to gauge cyclical turning points in the economy earlier and identify mini swings within a business cycle.

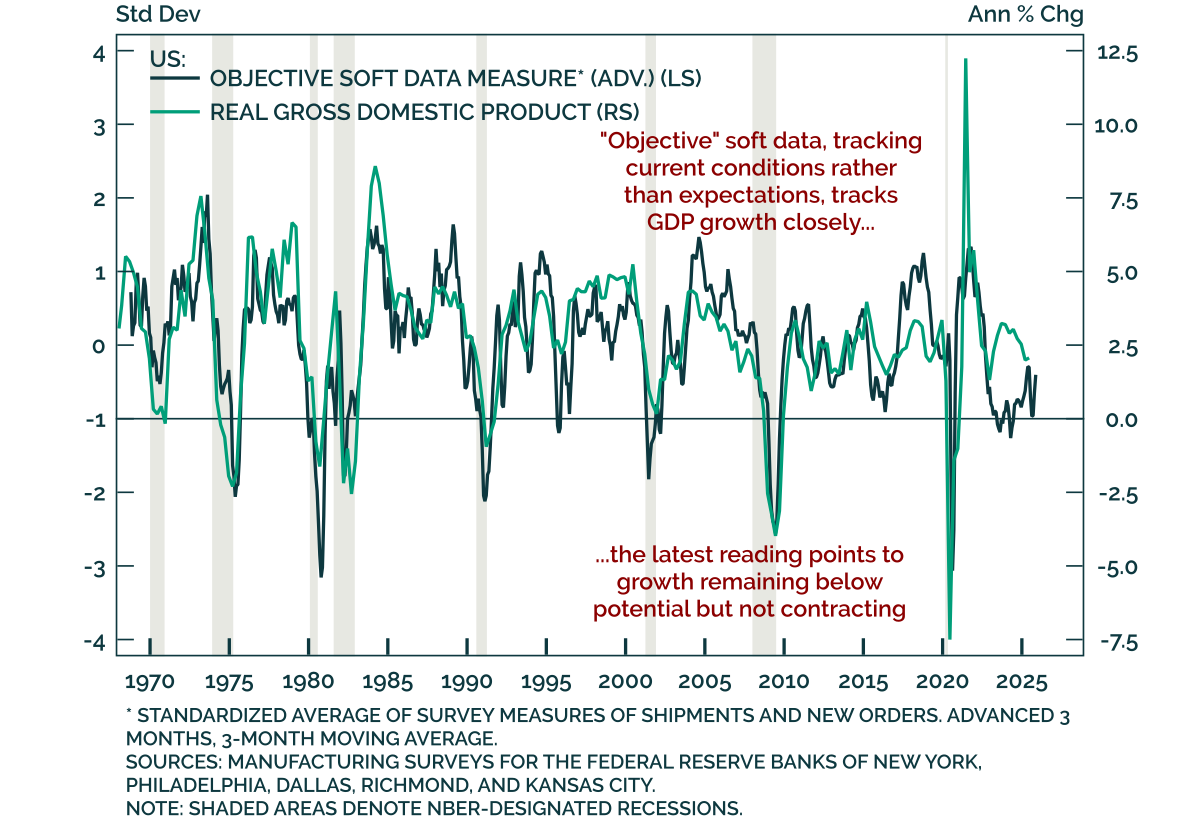

Regional Fed surveys point to low GDP growth, not an outright recession, which tactically supports low growth plays such as duration and tech. These timely surveys provide a snapshot of current month activity, combining “objective” indicators such as…

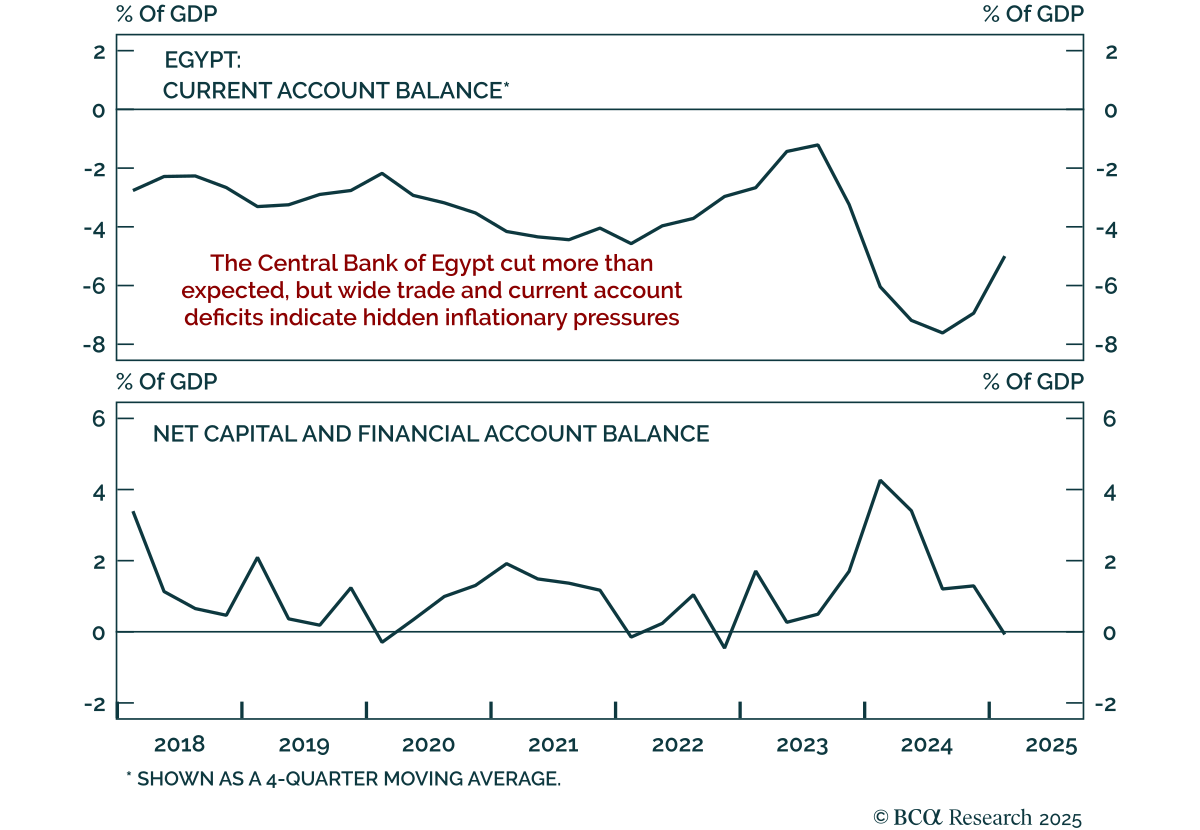

Egypt’s surprise 200 bps rate cut raises risks of re-accelerating inflation and currency pressure. The Central Bank of Egypt lowered the overnight lending rate to 23%, a larger-than-expected move. Our Emerging Markets strategists however expect inflation to…

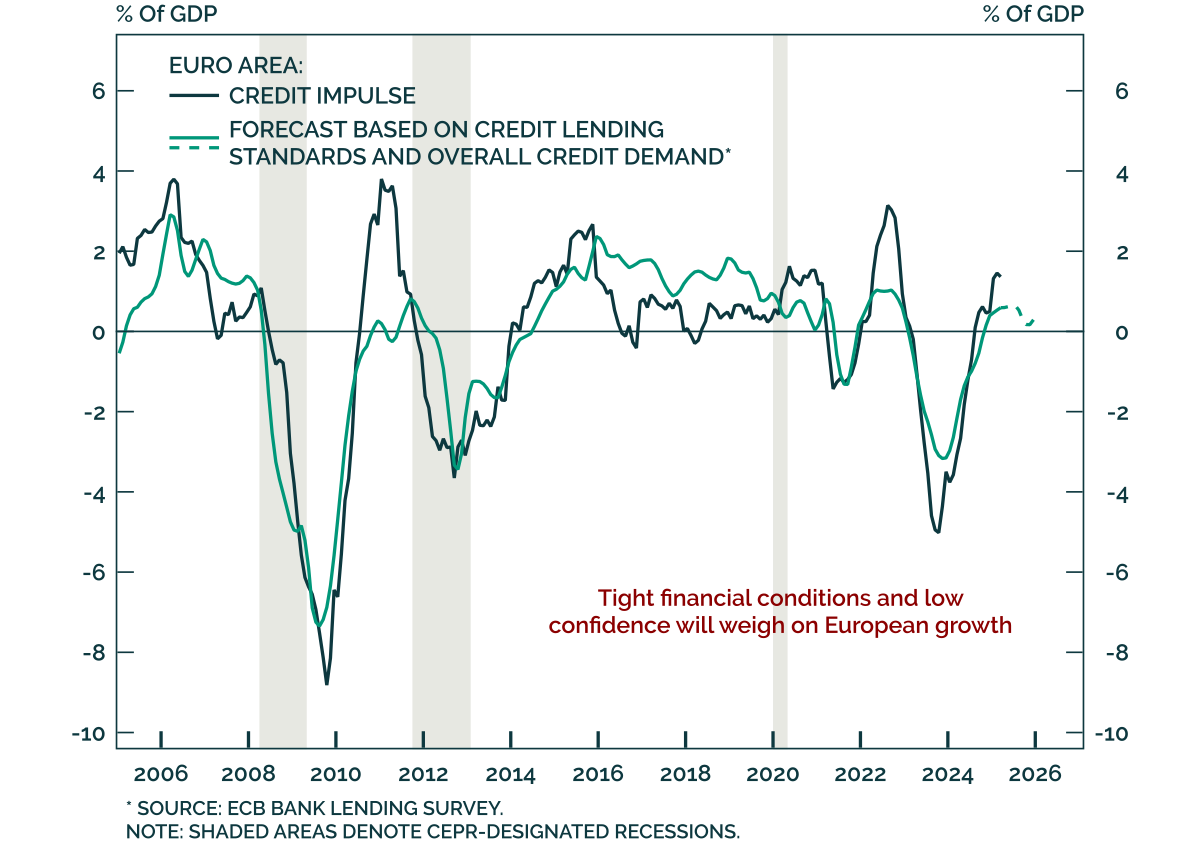

Weak Euro Area sentiment data and tight financial conditions support the case for a tactical US outperformance over Europe. July monetary data came in slightly below expectations, with M3 growth only edging up to 3.4% y/y from 3.3%. Household loan growth…

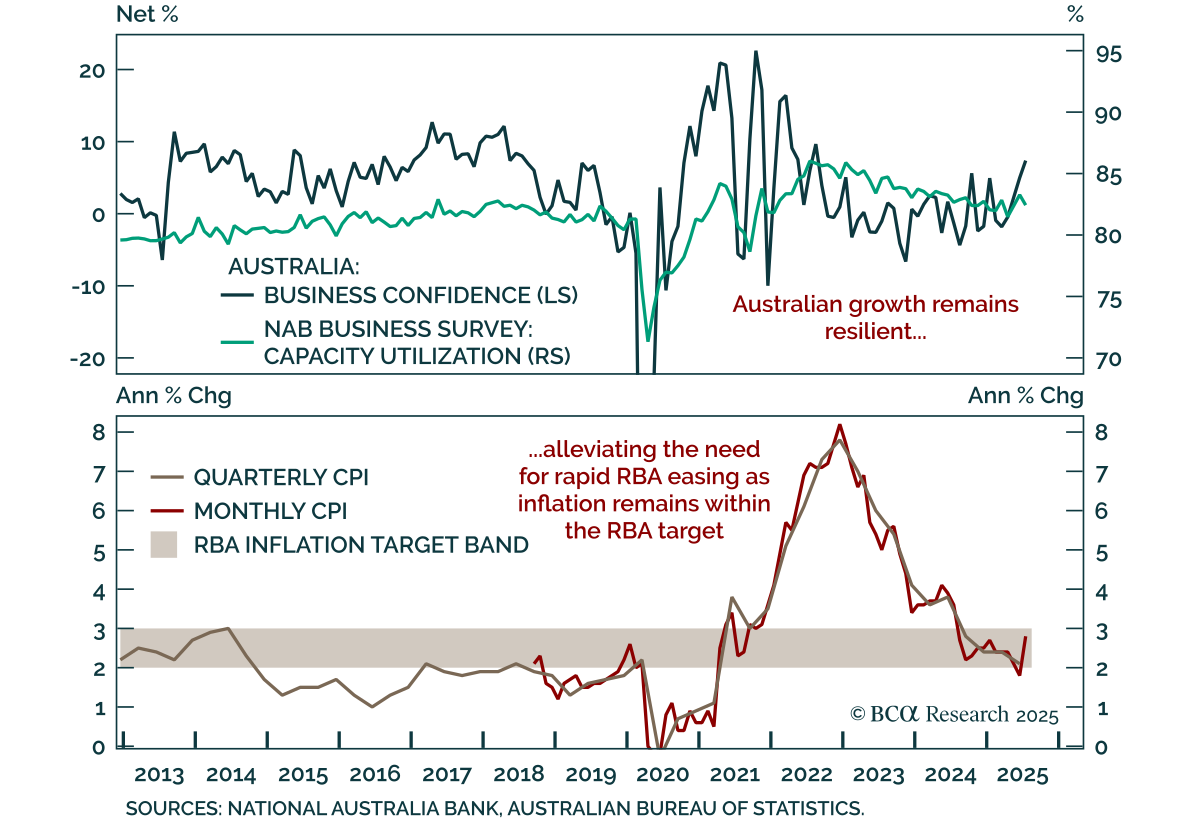

Australia’s July CPI surprise does not justify the aggressive easing priced, keeping us underweight ACGBs. Headline inflation accelerated to 2.8% y/y from 1.9% in June, with trimmed mean rising to 2.7% from 2.1%. Despite the rebound, inflation remains…

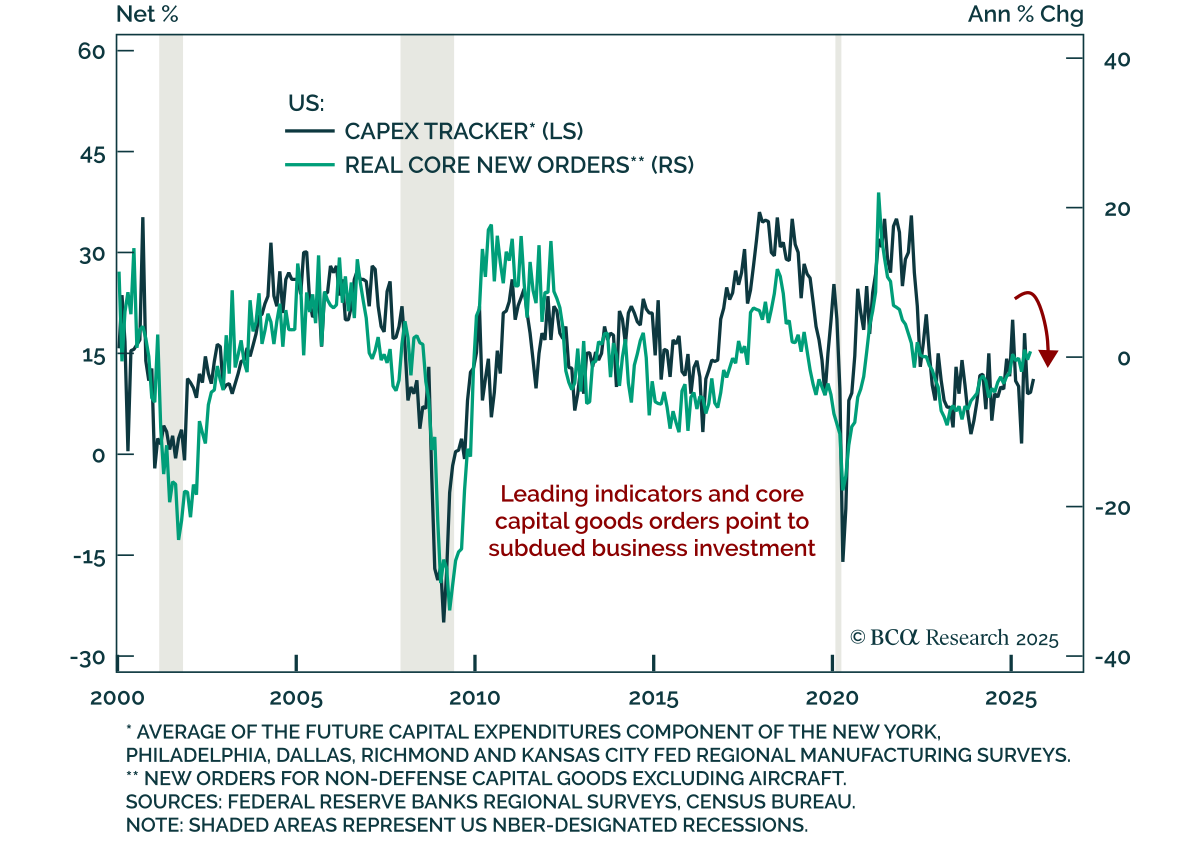

July US durable goods orders rebounded, but investment signals remain subdued and favor duration and tech. Orders fell 2.8% m/m after a 9.4% June drop, better than expected. Core measures excluding volatile components were stronger, with nondefense…