Economy

Gold has had a stunning rally over the past few weeks, gaining 9.2% since February 14 and reaching consecutive all-time highs last week before paring back some of its gains. Indeed, the drivers of gold have moved in a bullish direction for the yellow metal.…

BCA Research’s Bank Credit Analyst service ranks the major economies by their economic and financial performance under various categories. In the inflation category, the surprising top award goes to Italy, a country which historically has tended to have…

The latest MBA weekly survey shows mortgage applications rose 7.1% in the week ending March 8 on the back of a 4.7% increase in purchases and a 12.2% rise in refinancing, marking the second consecutive weekly increase. Higher mortgage activity comes amid…

There is a general consensus among BCA Research strategists that a US recession is highly likely over the next two years. While last month our Global Investment strategists reduced the probability that a recession will materialize in H1 2024 and raised the…

Despite the hotter-than-expected US CPI report for February, the S&P 500 rallied on Tuesday and closed at a fresh record high. Equity investors were unphased by the release and appear to have come to terms with projections that 2024 rate cuts will not be…

According to BCA Research’s Counterpoint service, ‘bad unemployment’ is on the rise in the US, despite resilient growth. There are two ways that you can become unemployed. Either by losing your job. Or by entering the labour force to look for a job. The…

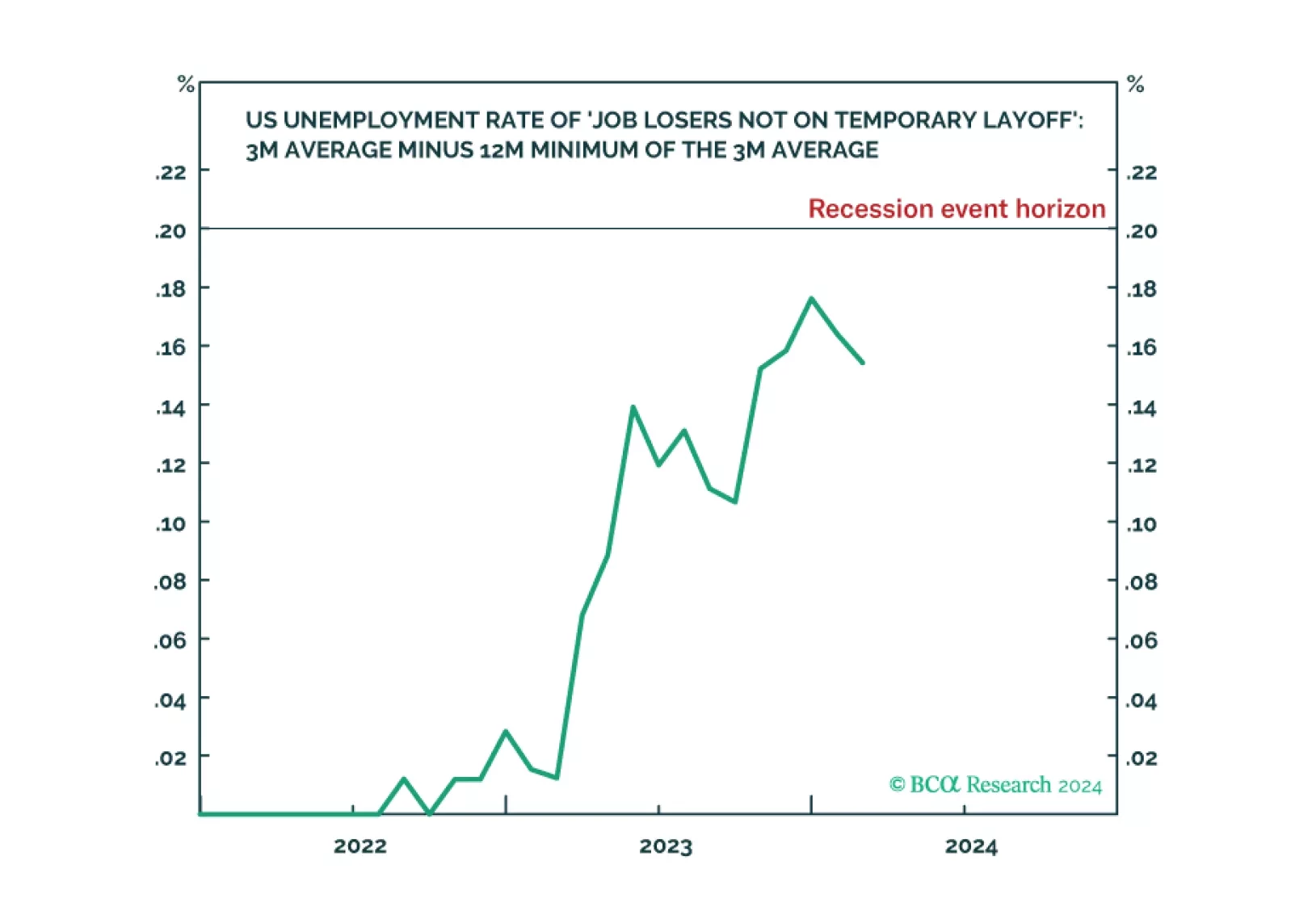

The Joshi rule real-time US recession indicator remains at an elevated 0.154 versus its recession event horizon of 0.200, indicating weakening US labour demand. With the last mile of US disinflation requiring labour demand to ‘catch down’ with labour supply, investors should watch the Joshi rule very closely to pre-empt a potential tipping-point. Plus: tactically long Portugal versus Europe, and wheat versus cotton; and tactically short USD/CLP, Qualcomm (QCOM), and Salesforce (CRM).

US headline CPI inflation accelerated from 0.3% m/m to 0.4% m/m in February, in line with expectations. A rise in gasoline prices and shelter inflation accounted for 60% of this increase. Meanwhile, the annual rate of change in the headline index unexpectedly…

Chinese stocks are experiencing their longest rally since the country’s exit from Covid restrictions over a year ago. The MSCI Onshore and Investable indices (in USD terms) have gained 15.8% and 9.1% respectively since February 5th, with the former…

Although the Atlanta Fed GDPNow estimates for Q1 have been trending lower, the latest 2.5% print (which is down from 3.4% a month ago) still suggests that economic conditions are resilient in the US. Yet small business owners are less optimistic. The results…