Economy

Our Portfolio Allocation Summary for March 2024.

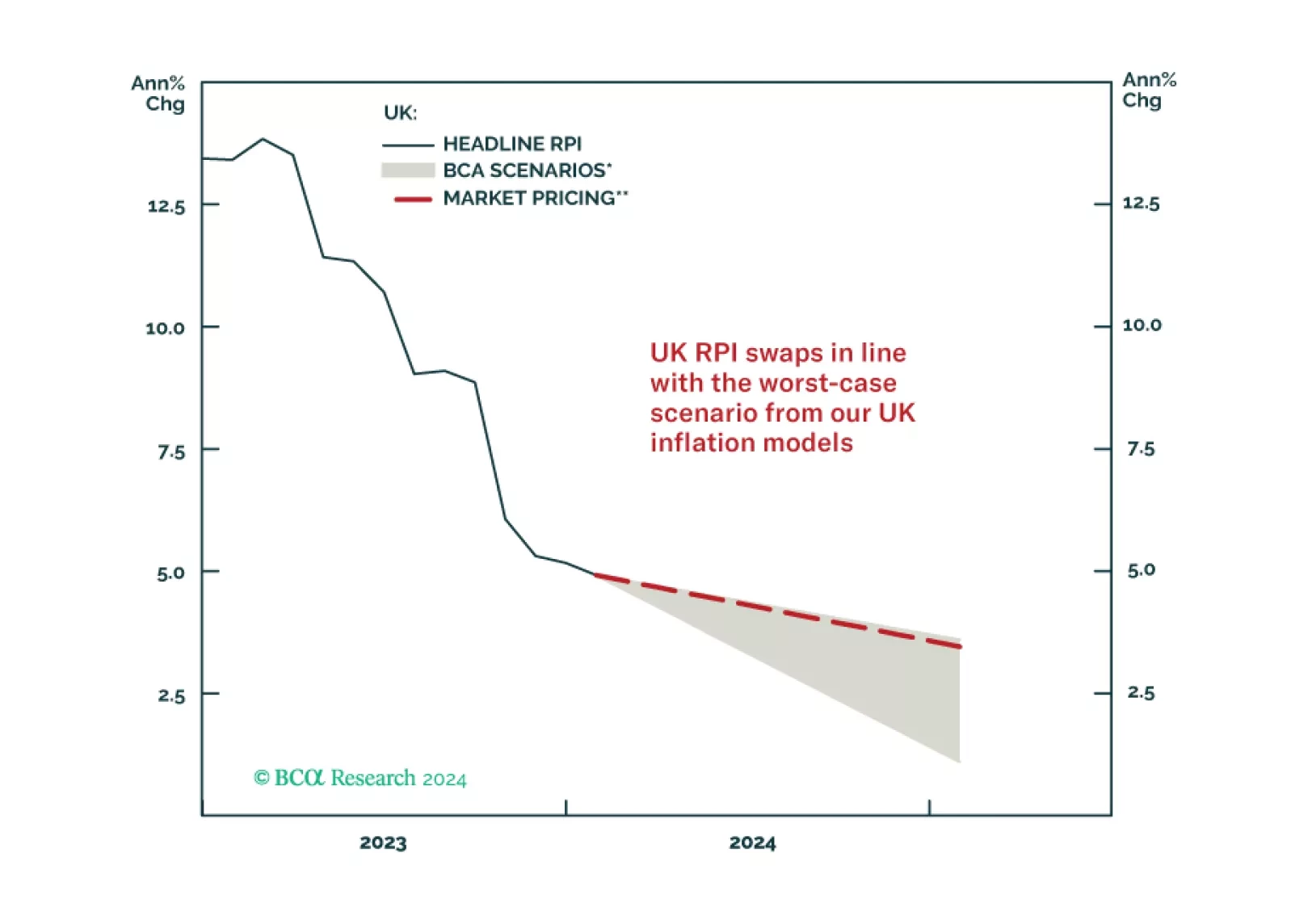

In this Special Report, we introduce our UK Linkers Golden Rule – a framework to profitably trade and invest in UK inflation-linked bonds versus nominal UK gilts. The Rule is currently signaling that nominal Gilts should outperform UK linkers over the next year as UK inflation slows.

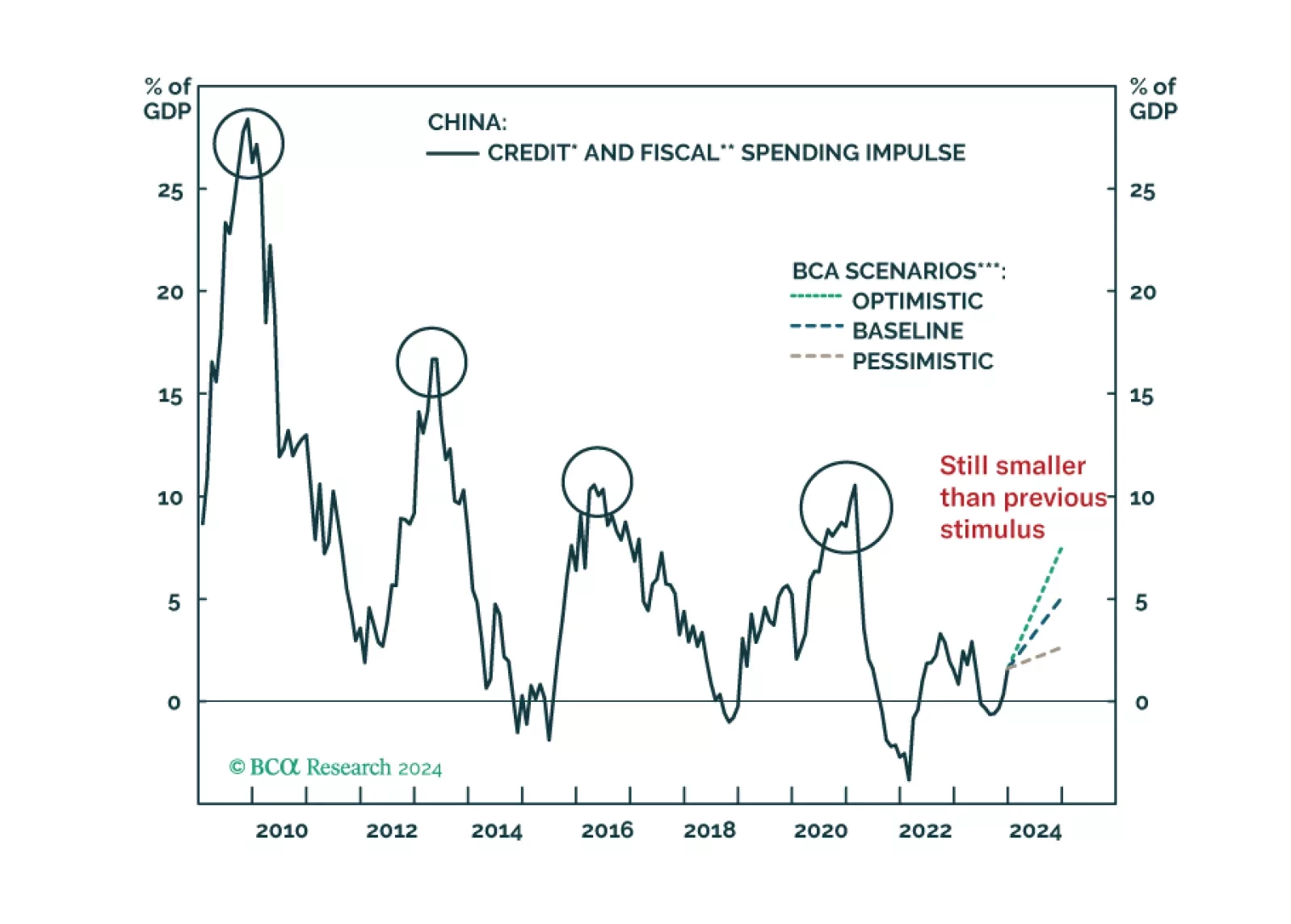

The stimulus measures announced at last week's NPC were not a game changer. As in 2023, we expect aggregate government spending will fall short of the budgeted amount again this year.

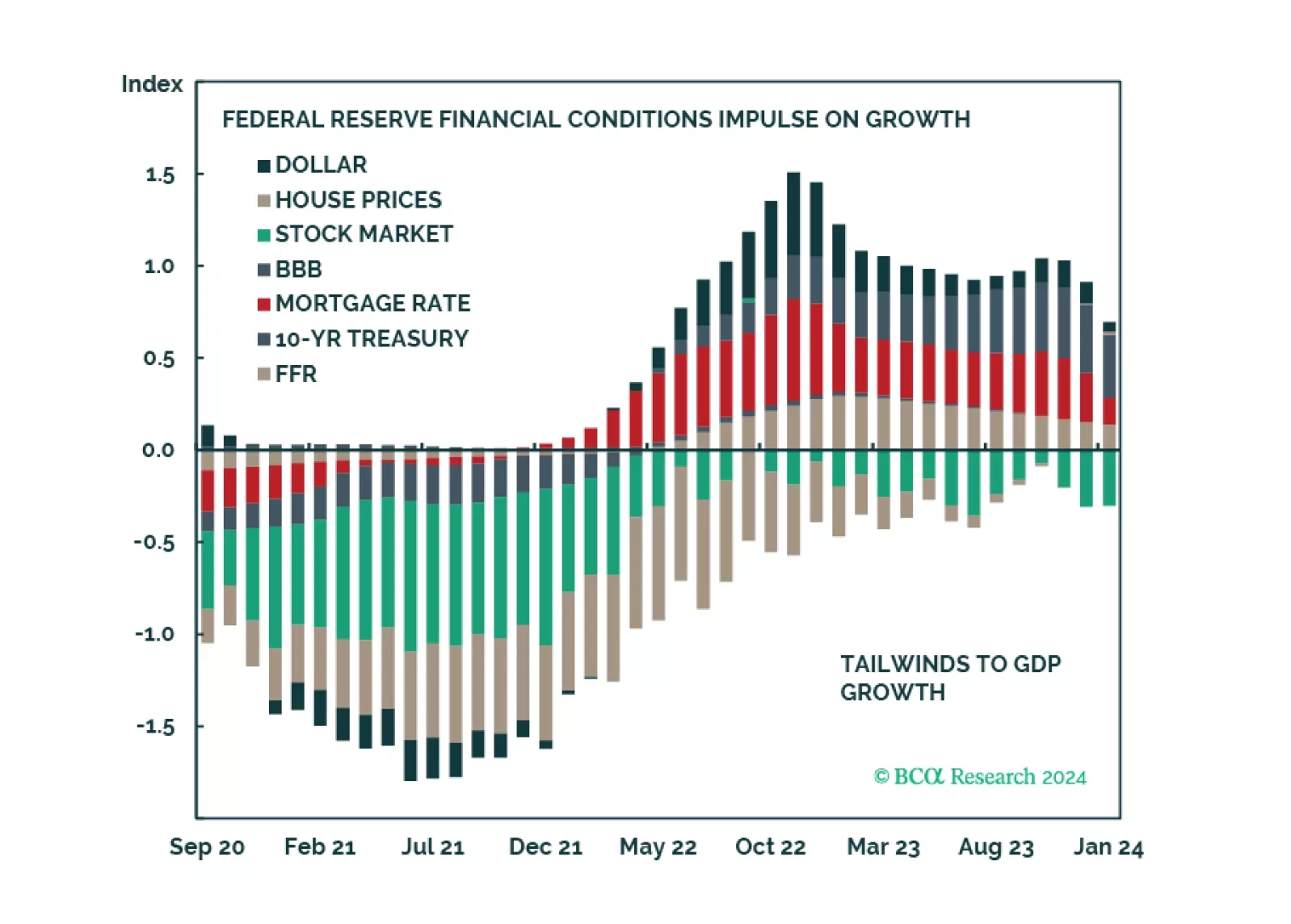

Clients are increasingly more positive about the US economy, but there are no signs of exuberance. The rally could continue as the majority is not fully invested. Financial conditions have already eased, and the Fed is unlikely to surprise on the upside but will deliver a promised cut this summer. CRE is a still pain point of the US economy. We are not bearish, but after a fast and furious rally, markets are fragile.