Economy

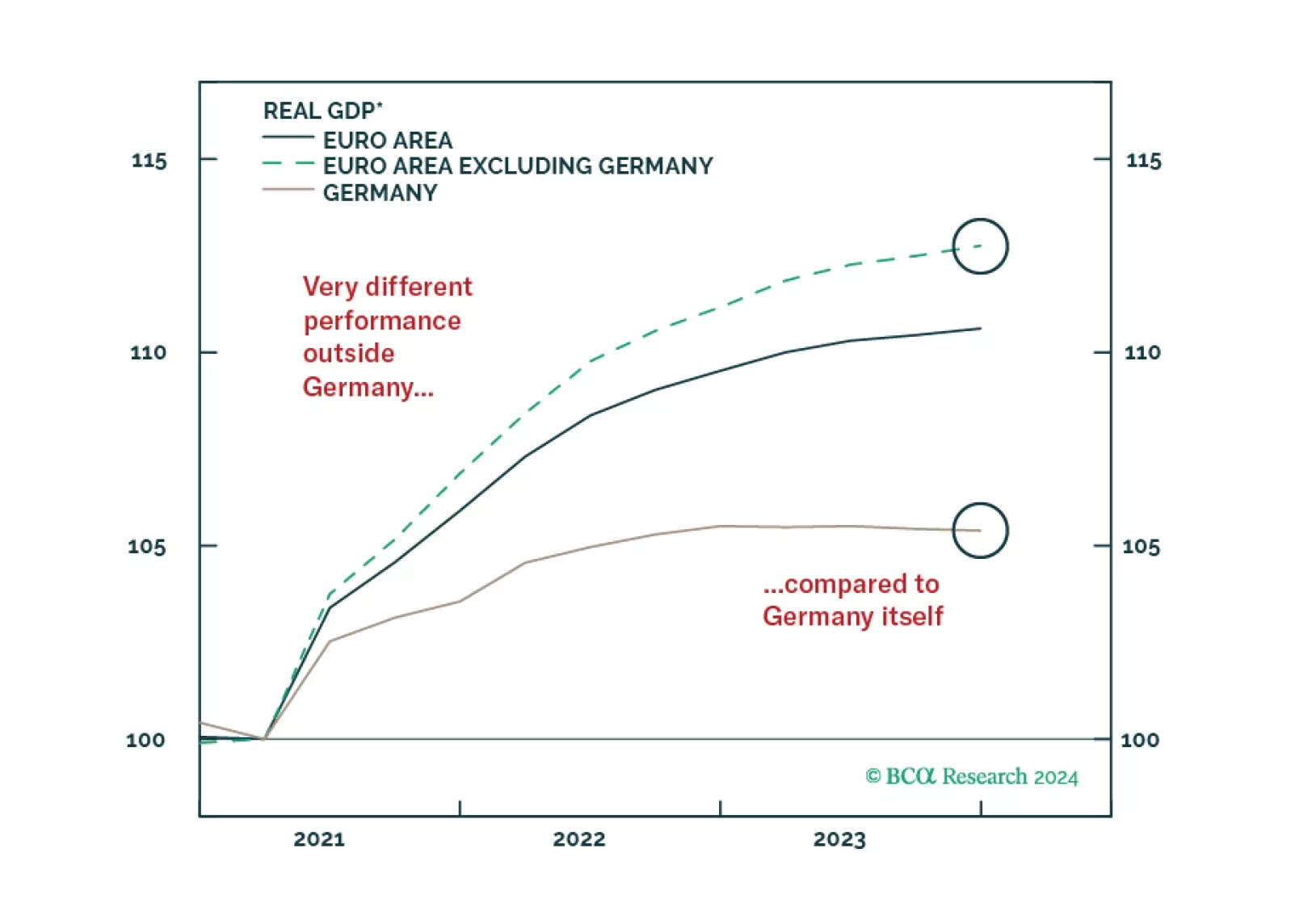

According to BCA Research’s European Investment Strategy service, Germany will likely drag the overall Euro Area into contraction, even if, individually, other countries manage to avoid a recession. This slightly better economic outcome will nonetheless…

The first in a series of Strategy Insights where we present a checklist for extending duration in each major government bond market. This first entry focuses on the US.

Outside of Germany, European growth fares better than many believe. Will this hidden resilience help the euro and push German yields higher?

Germany’s IFO Business Climate index ticked up 0.3 points to 85.5 in February, in line with consensus estimates. Expectations for the next 6 months explain the improvement in sentiment among German companies (up 0.6 points to 84.1), while their assessment of…

The messaging from the minutes of the ECB’s January meeting was similar to the Fed. Although Governing Council members noted that “for the first time in many meetings, the risks to reaching the inflation target were seen as broadly balanced or at least…

While efforts by policymakers to stabilize the stock market are buoying Chinese equities, domestic economic data remains soggy. Home prices declined further on both a monthly and annual basis in January, reinforcing the deflationary headwinds facing the…

In a recent Special Report, BCA’s Foreign Exchange Strategists update their long-term fair-value models for the real effective exchange rate. The model aims to capture deviations from the long-term drivers of a currency, such as relative productivity trends…

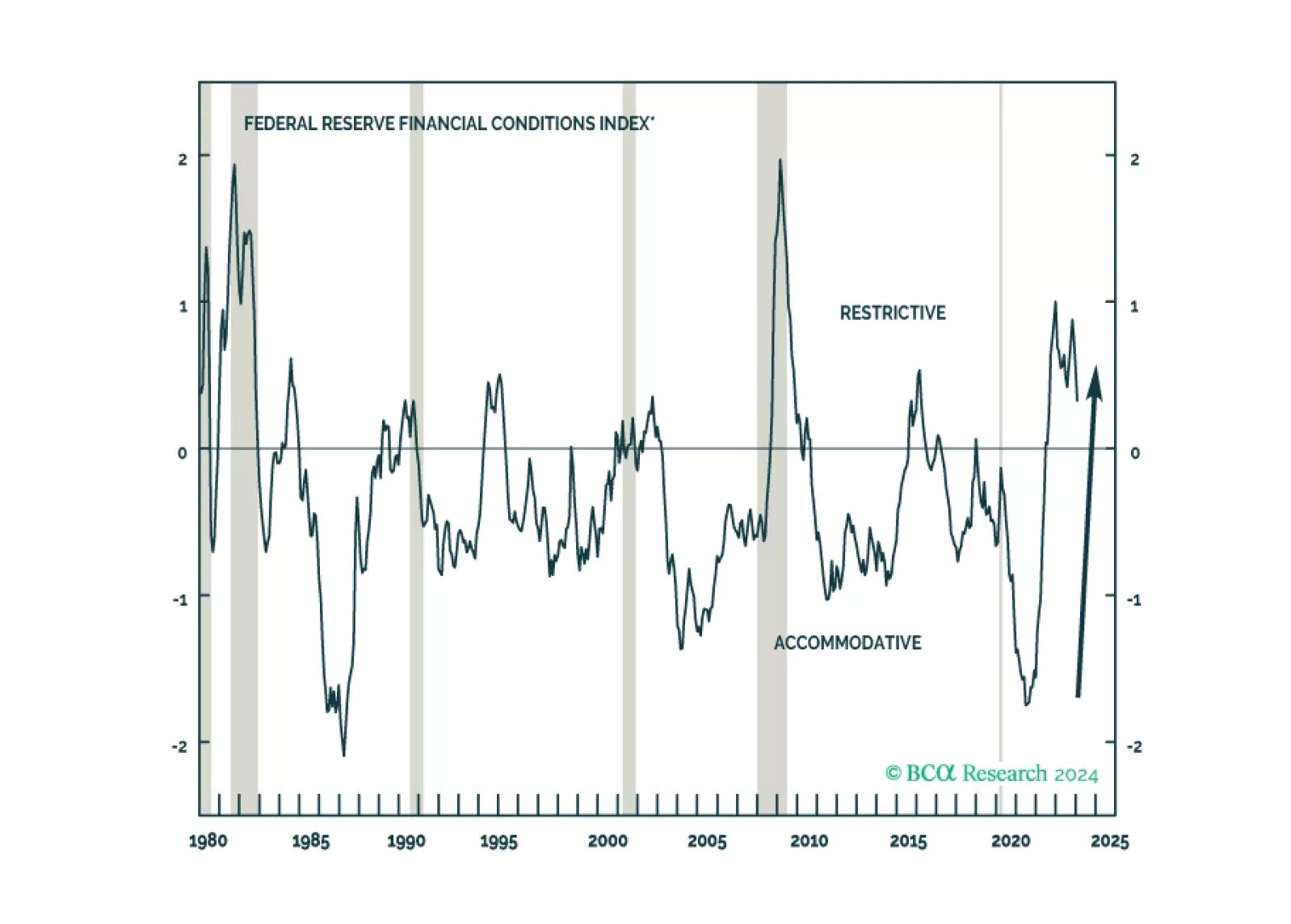

According to BCA Research’s US Investment Strategy service, investors should take care not to read too much into the recent easing in financial conditions. According to Goldman Sachs’ Financial Conditions Index (FCI) financial conditions have become…

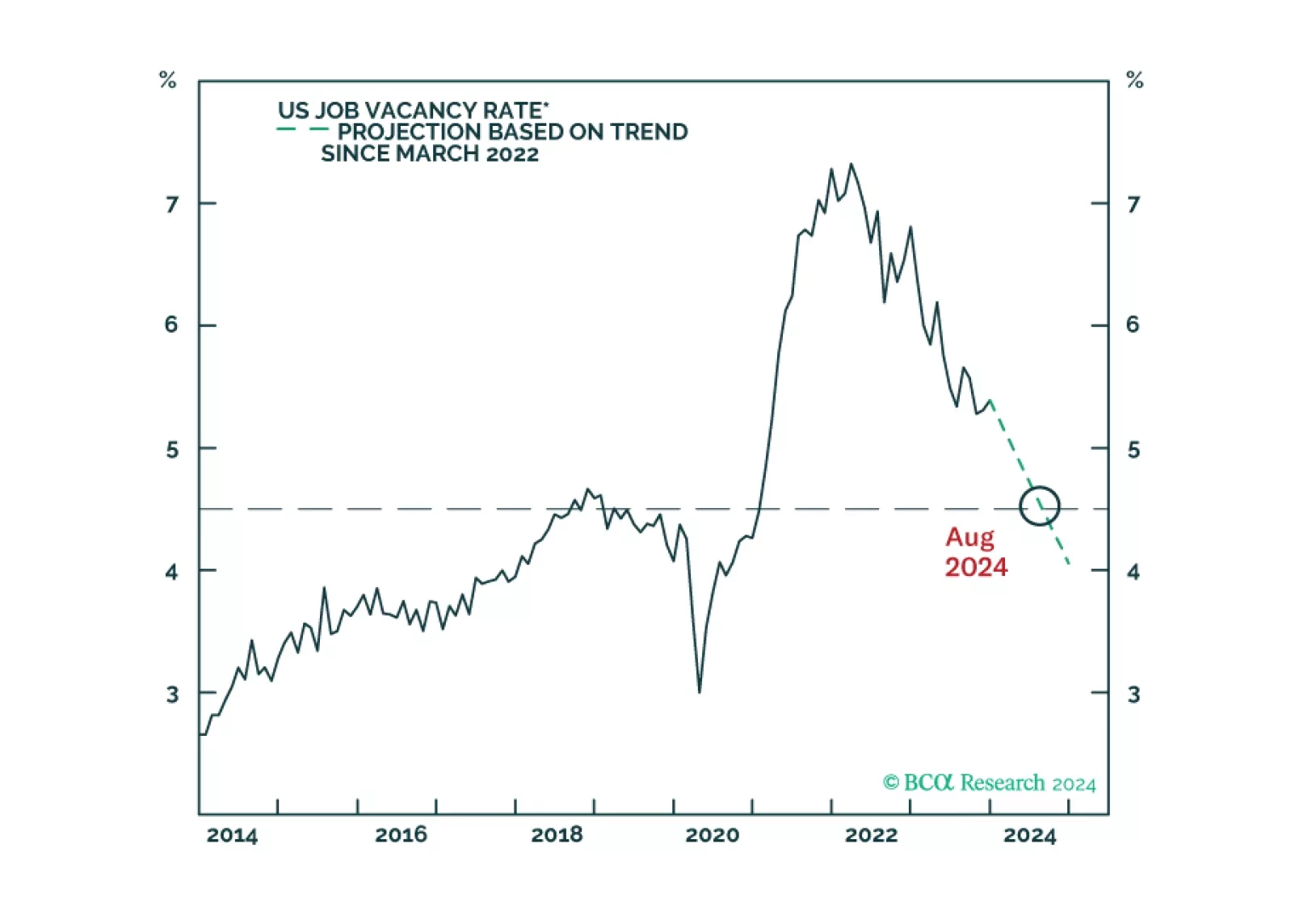

Clients have been pushing back on our recession call on the grounds that it is incompatible with the economy’s second-half acceleration and the more recent easing in financial conditions. We examine both of those points in the course of doing some pushing back of our own.

Preliminary PMI estimates suggest that service sector activity is expanding across DM economies in February. Most notably, services PMIs are back at or above 50 in Australia and the Eurozone from previously contracting levels. Meanwhile, the services sectors…