Economy

The Global Manufacturing PMI clocked in at 50 in January – exactly on the boom-bust line. The index has been on a general uptrend since mid-2023 with the January figure marking the first non-contractionary reading since August 2022. The headline index…

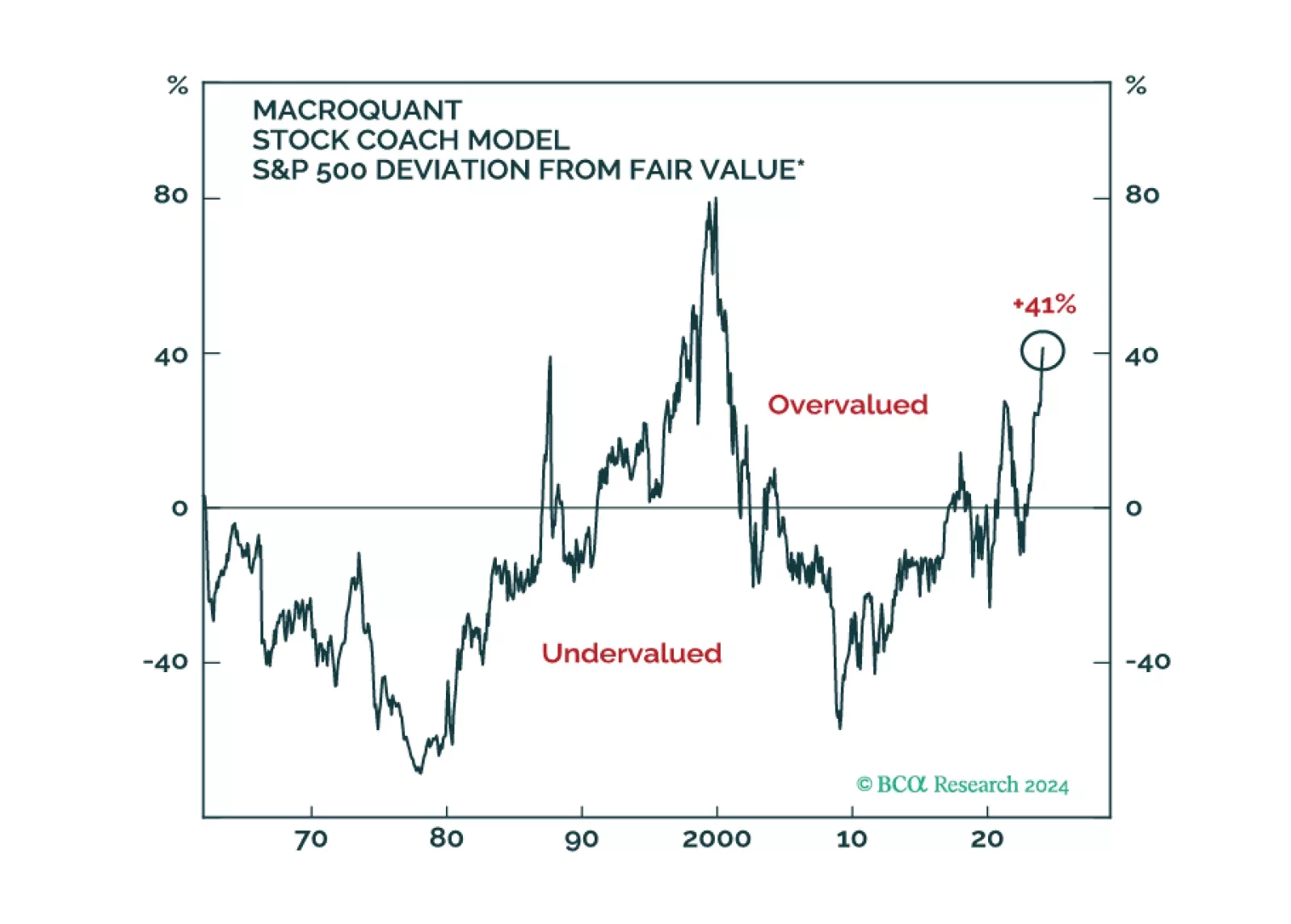

According to BCA Research’s Global Investment Strategy service, although the next recession is likely to be mild-to-moderate, the ensuing financial avalanche will be more severe. Valuations are highly stretched and hopes that today’s tech leaders will…

Recessions often begin seemingly out of the blue when the economy’s temperature falls enough to set in motion adverse feedback loops that cause unemployment to rise. We expect the US economy to suddenly freeze over towards the end of this year or in early 2025. For now, a benchmark allocation to equities is appropriate, but a more defensive stance will be necessary later this year.

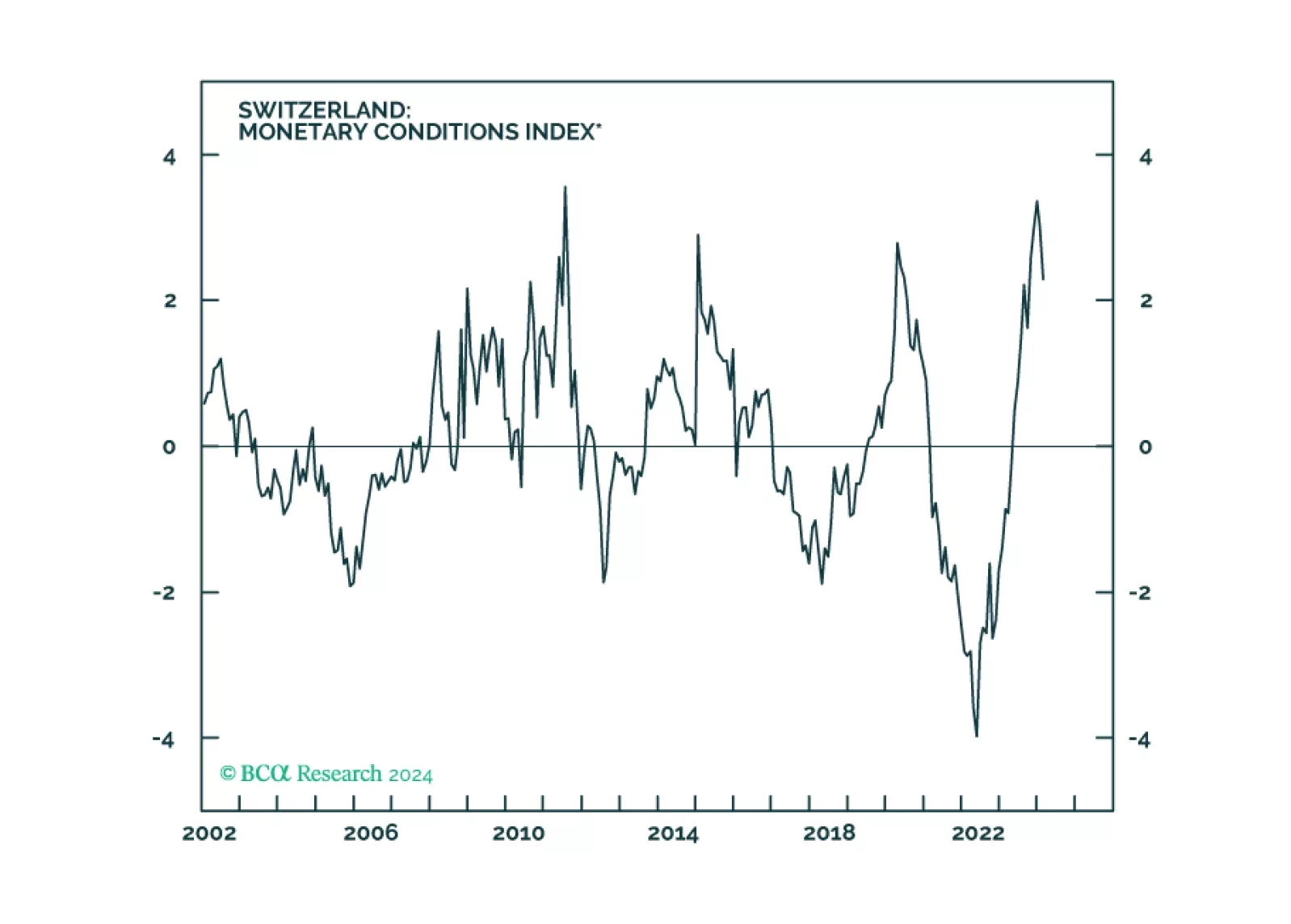

In this Insight, we speculate on the outlook for the CHF.

The US retail sales report for January delivered a disappointing message about consumer spending. The 0.8% m/m drop in overall retail sales was worse than expectations of a 0.2% m/m decline and marked the most severe monthly contraction since last March. The…

The first two regional fed manufacturing surveys for February delivered strong upside surprises. The New York Fed’s Empire Index surged from -43.7 to -2.4, unwinding its January slump. Similarly, the Philly Fed current activity index jumped by 15.8 points to…

Our Commodity & Energy colleagues see oil markets balanced in the short run, which keeps their Brent price forecasts at $95/bbl and $105/bbl for 2024 and 2025. That said, they note the odds are increasing demand growth could surprise to the…

According to BCA Research’s Emerging Markets Strategy service, the diminishing pace of disinflation in the US could pose a threat to US share prices in the near term. In the medium term, the key risk to US share prices is shrinking corporate profits. …

Over the next six months, the deterioration in non-US growth will occur earlier and be more pronounced than in the US. This expectation reinforces our confidence to bet on the strength of the US dollar. As usual, the flip side of the US dollar strength will be weakness in EM risk assets.

We are now more than midway through the Q4 2023 earnings season. Roughly two-thirds of the companies in the S&P 500 have released their earnings reports. It’s therefore worthwhile to stand back and observe some of the trends. According to FactSet, 75%…