Economy

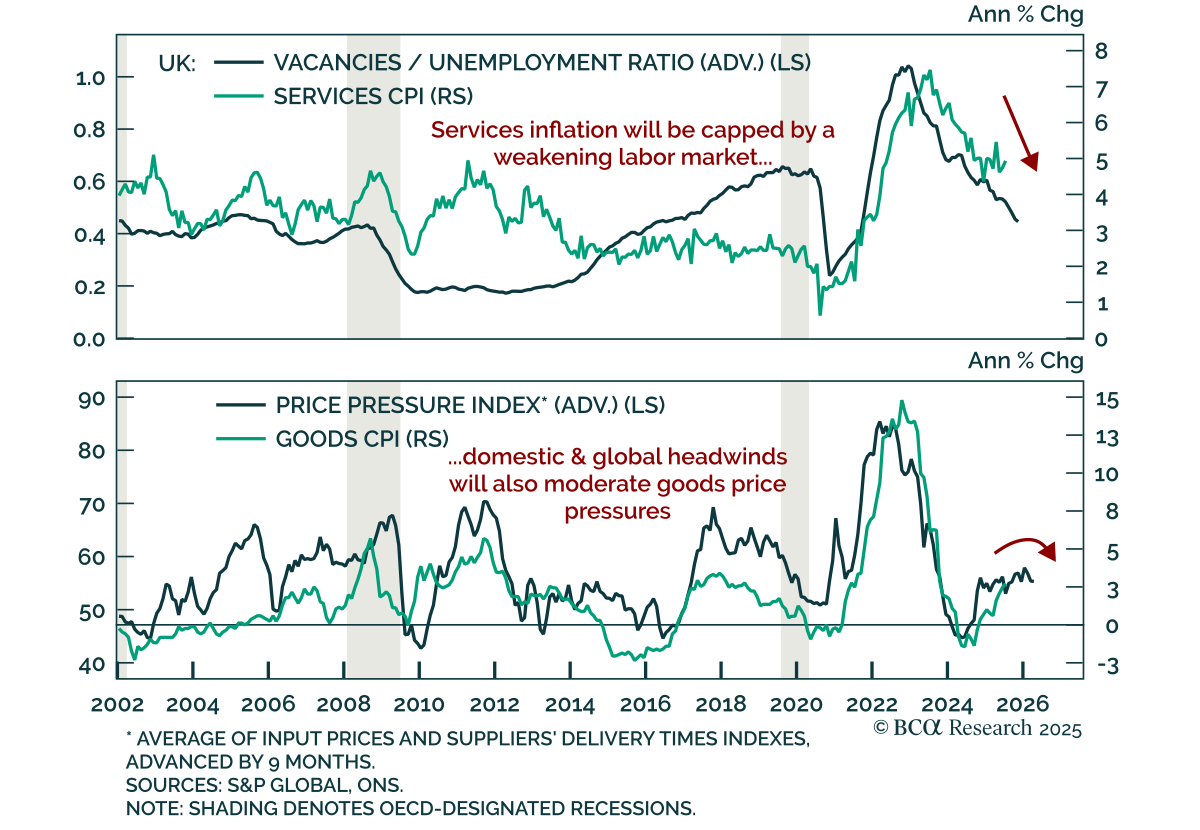

Hot July inflation does not alter the weakening UK backdrop, keeping Gilts attractive and GBP vulnerable. Headline CPI rose 0.1% m/m, lifting y/y inflation to 3.8% from 3.6%, while core ticked up to 3.8% from 3.7%. Services inflation remained sticky,…

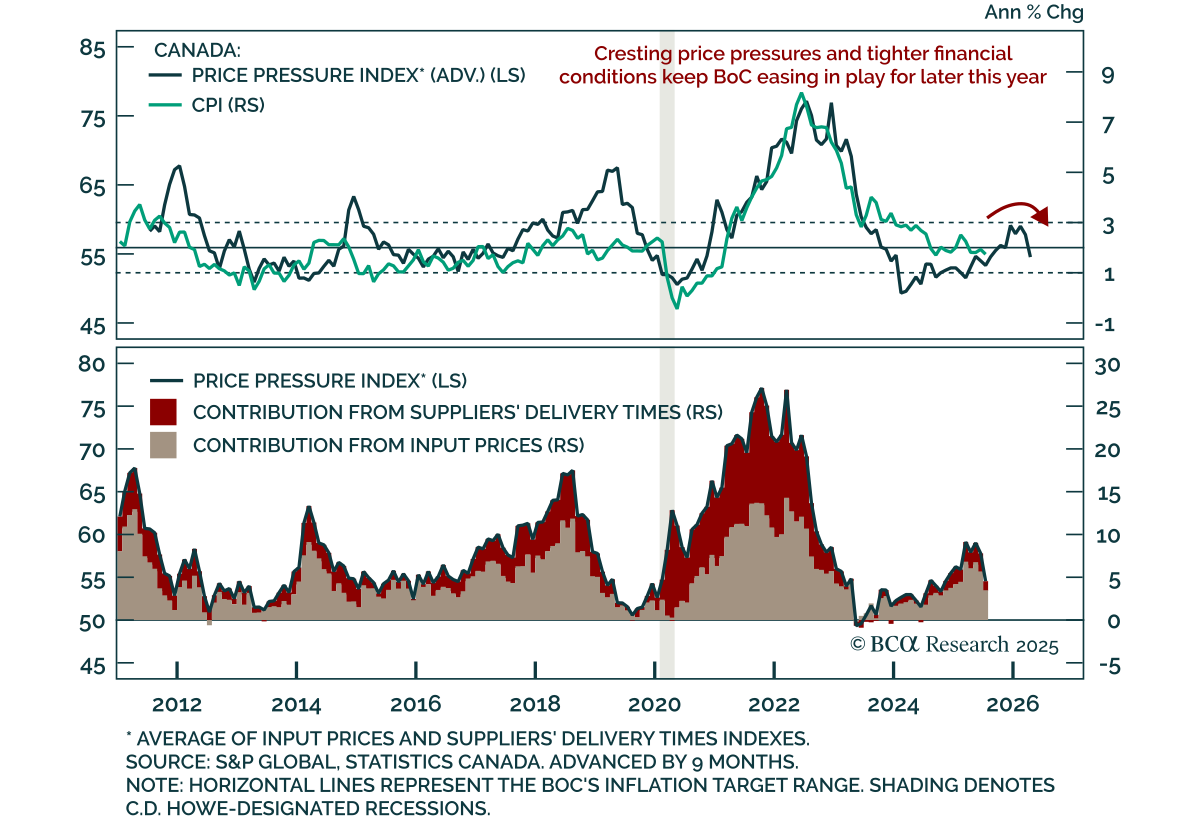

July’s softer Canadian inflation, set against lingering macro weakness, reinforces the case for more BoC easing than markets are currently pricing. Headline CPI slowed to 1.7% y/y from 1.9%, below expectations, driven by lower gasoline prices. The BoC’s…

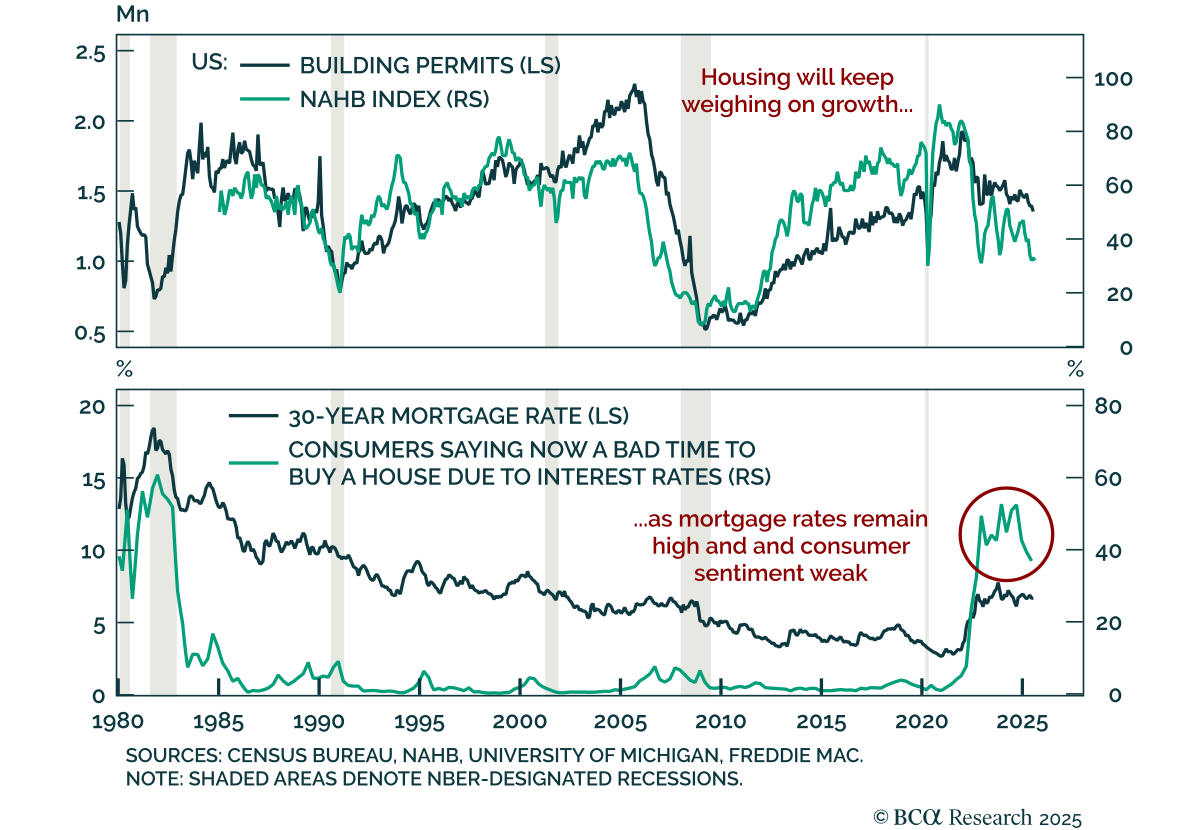

US housing data remain weak, reinforcing a fragile growth backdrop and the need for equity downside protection. July housing starts rose 5.2% m/m (annualized), but building permits fell 2.8% following a small June decline. The August NAHB Housing Market…

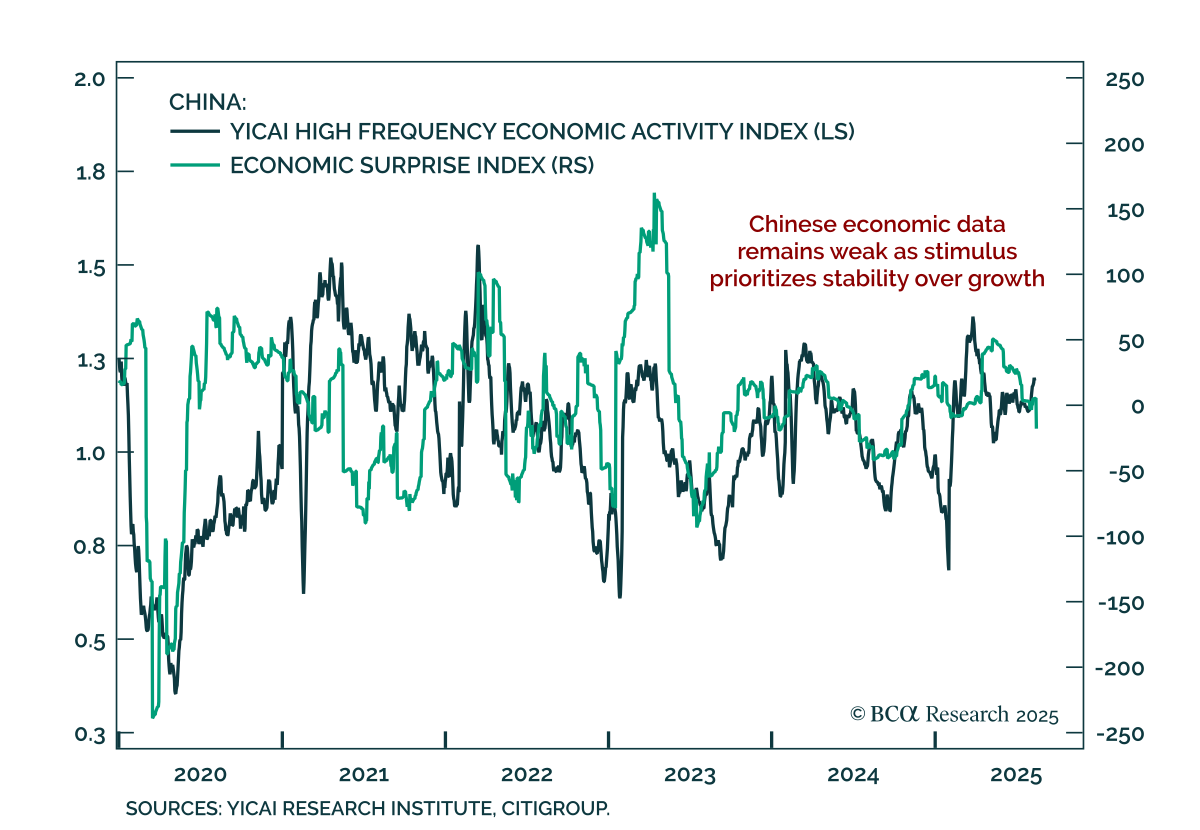

July data confirm China’s weak growth, with no near-term shift toward meaningful stimulus. New home prices fell 0.31% m/m, retail sales slowed to 3.7% y/y from 4.8%, and industrial production eased. Flooding in July disrupted infrastructure spending…

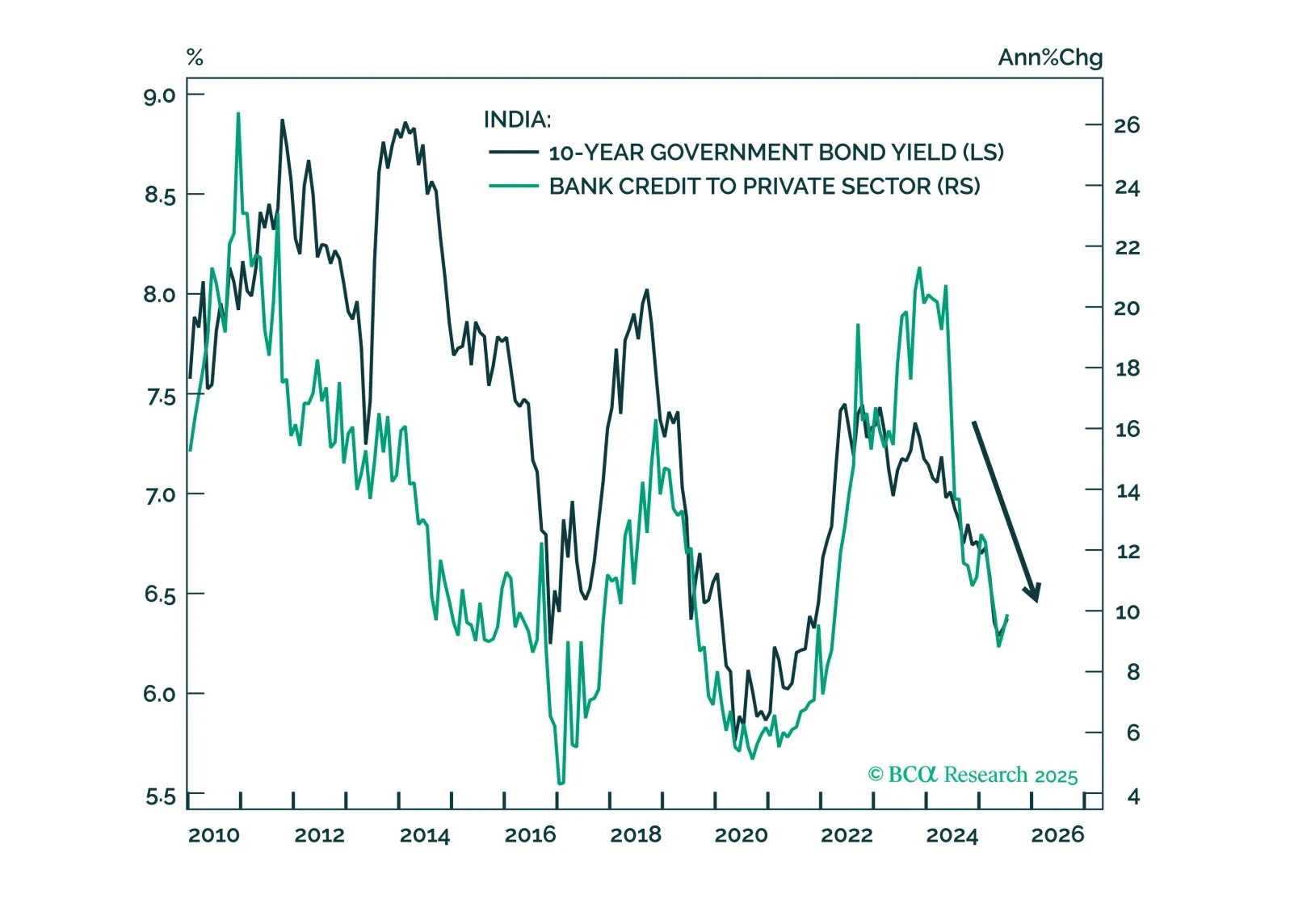

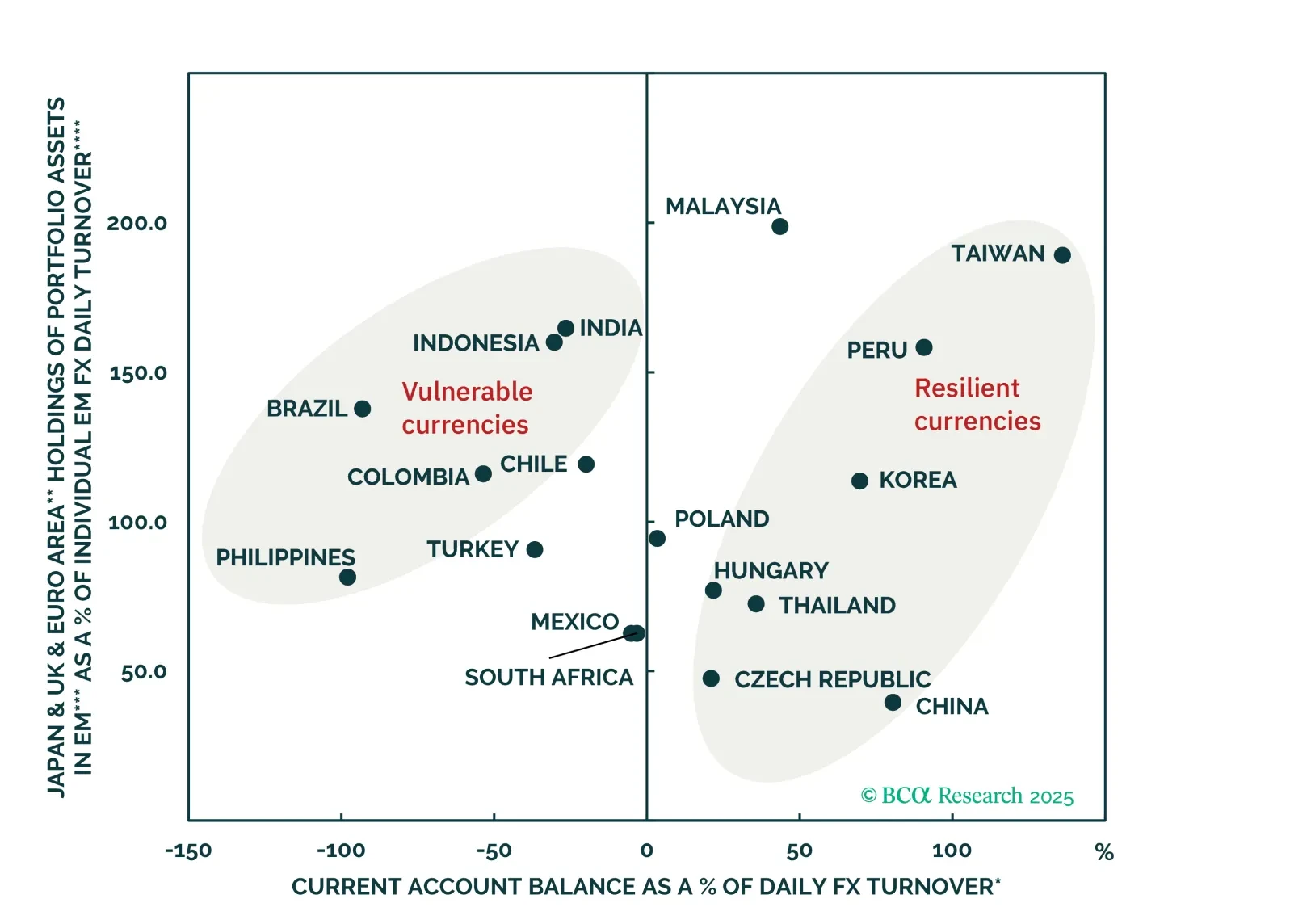

The Indian rupee remains vulnerable to further depreciation amid slowing growth, tight domestic policy, and fragile capital flows. Trade risks and a weakening external balance will likely keep INR underperforming EM Asia peers.

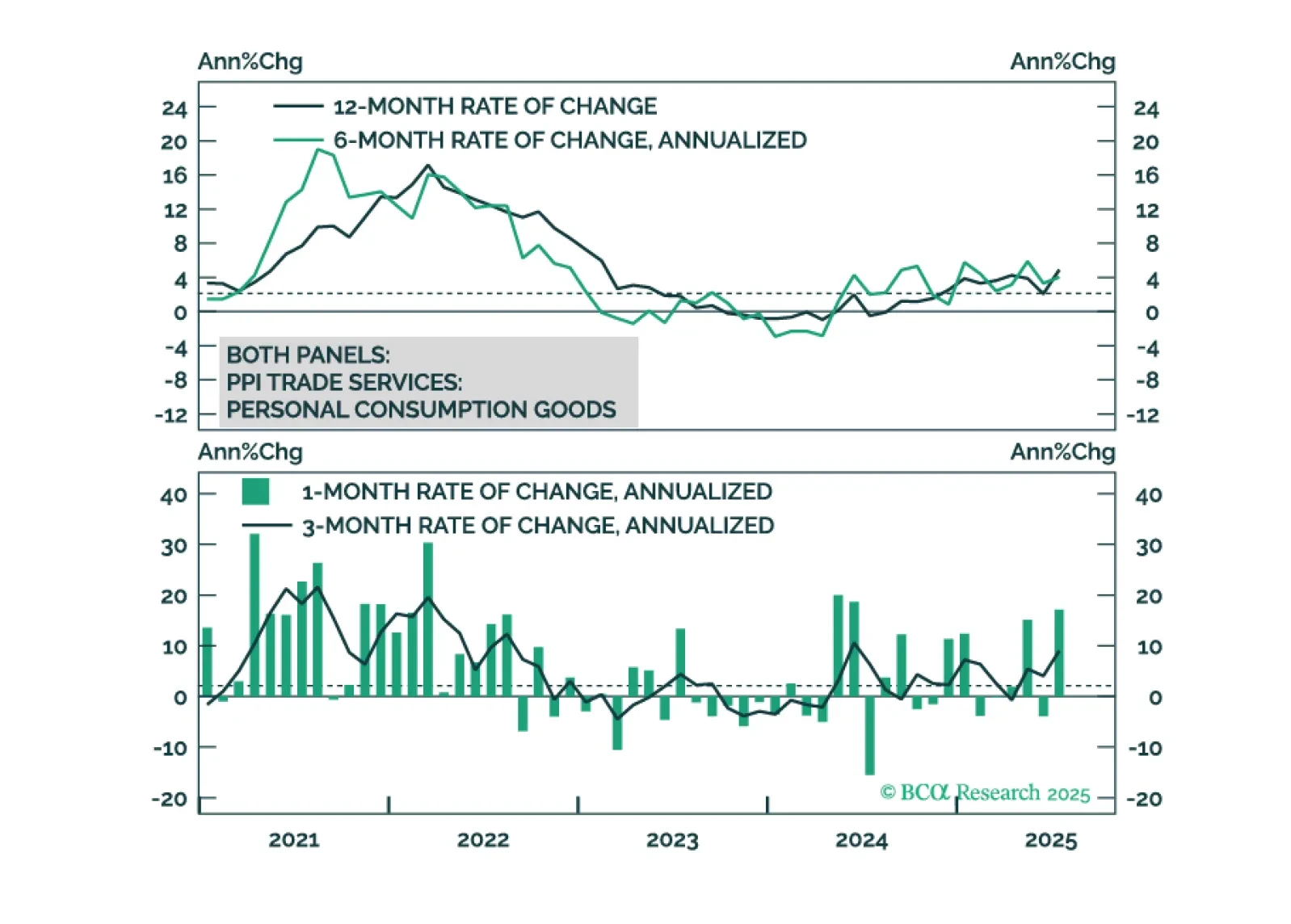

The cost of tariffs is falling on the US consumer, not foreign exporters or US firms.

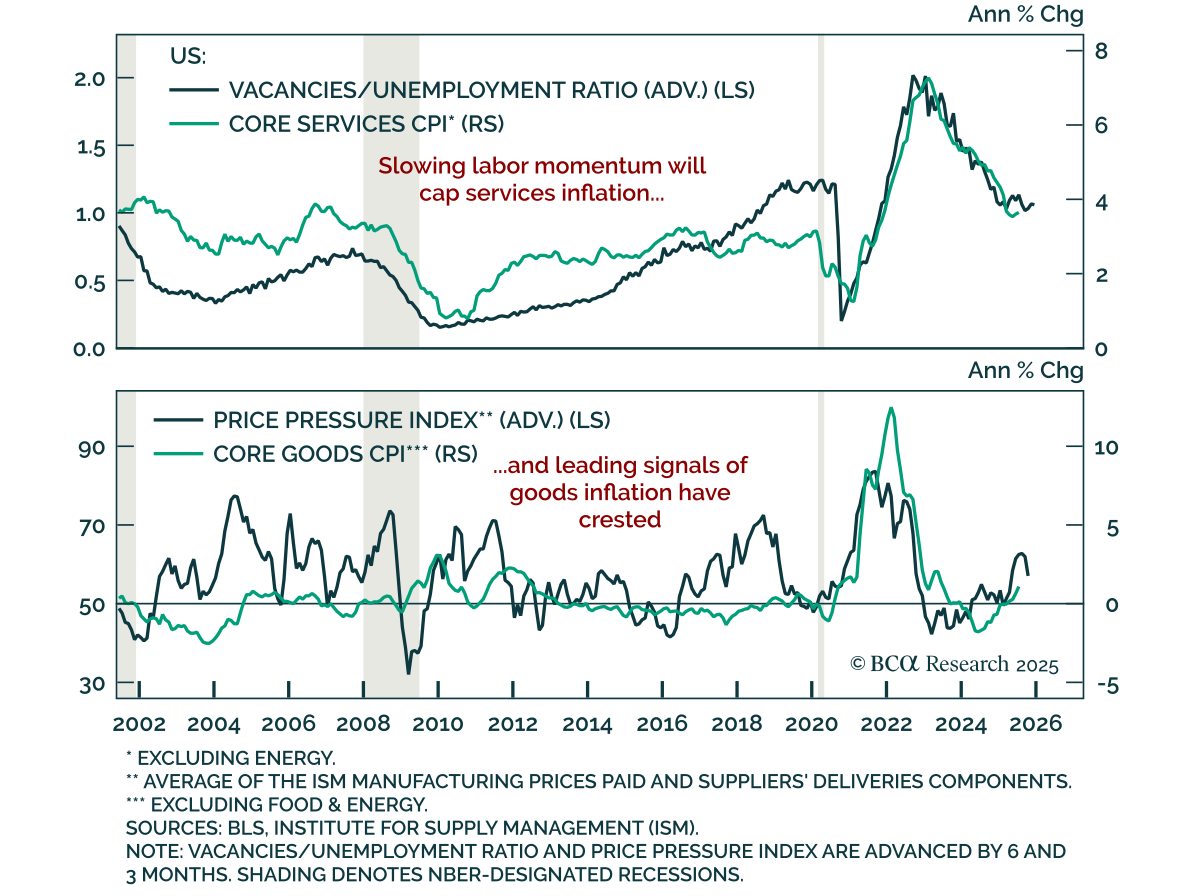

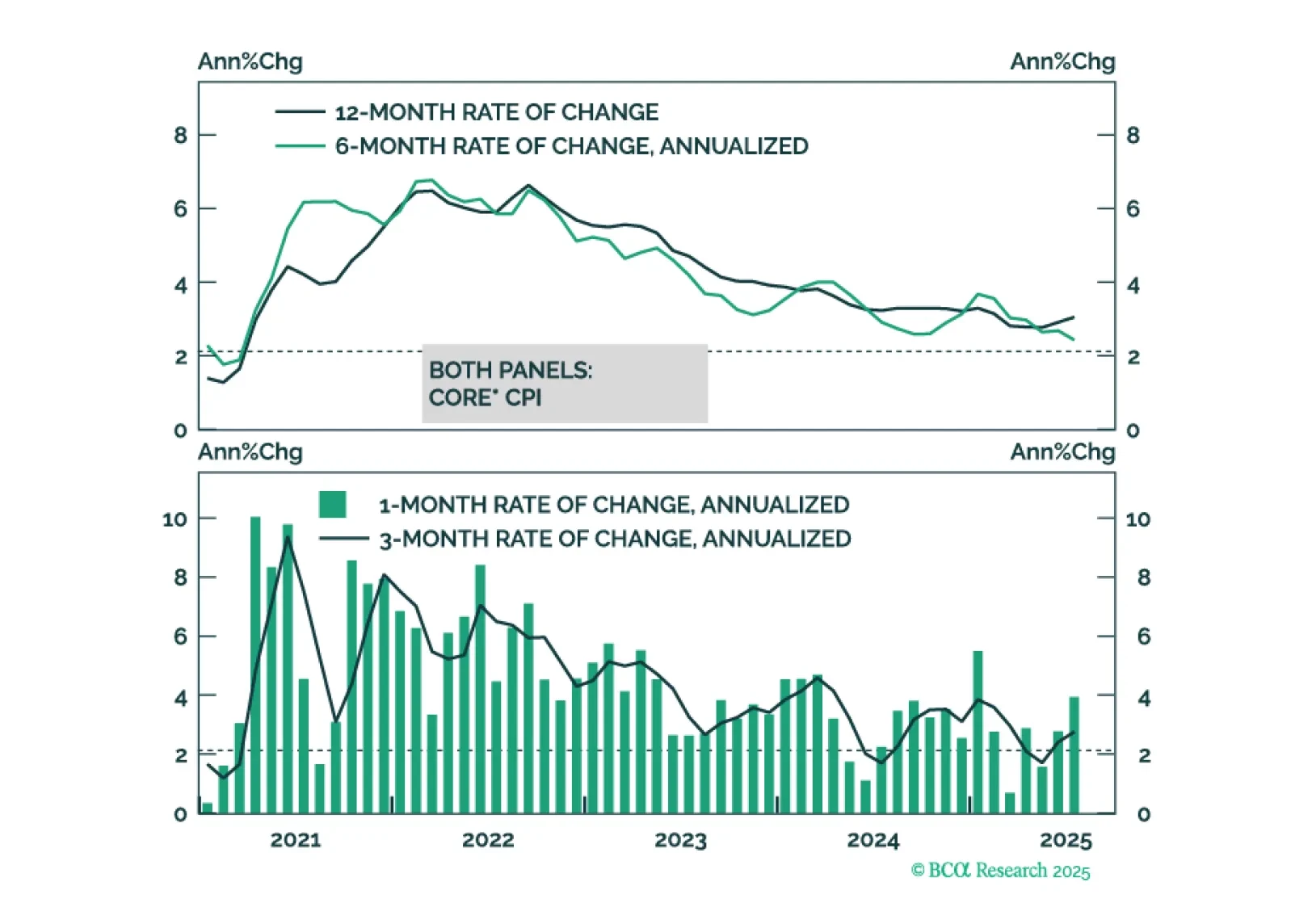

July US CPI met expectations as leading indicators point to disinflation, supporting our long duration stance and preference for 2s5s steepeners. Headline CPI rose 0.2% m/m (2.7% y/y), while core increased 0.3% m/m and accelerated to 3.1% y/y. Both goods…

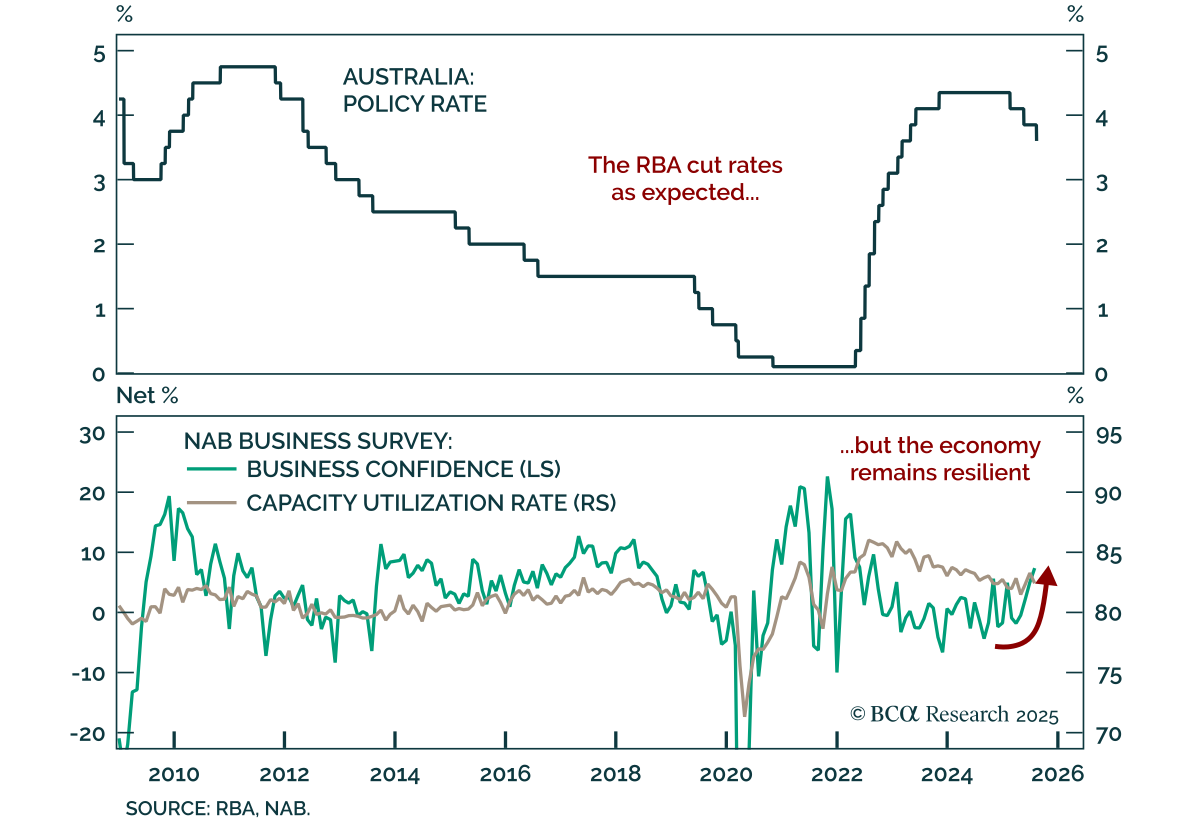

The RBA delivered a widely expected cut to 3.6%, but resilient data warrant an ACGBs underweight. The 25 bps cut was the third this year and Governor Bullock’s guidance was consistent with a cut every other meeting, keeping ACGB yields roughly…

This morning’s CPI report marginally tips the scales in favor of a September rate cut.

Despite widespread investor optimism Brazil’s currency outlook is challenged by a toxic mix of poor external, fiscal, and macro fundamentals. Expect BRL to underperform most EM peers.