Economy

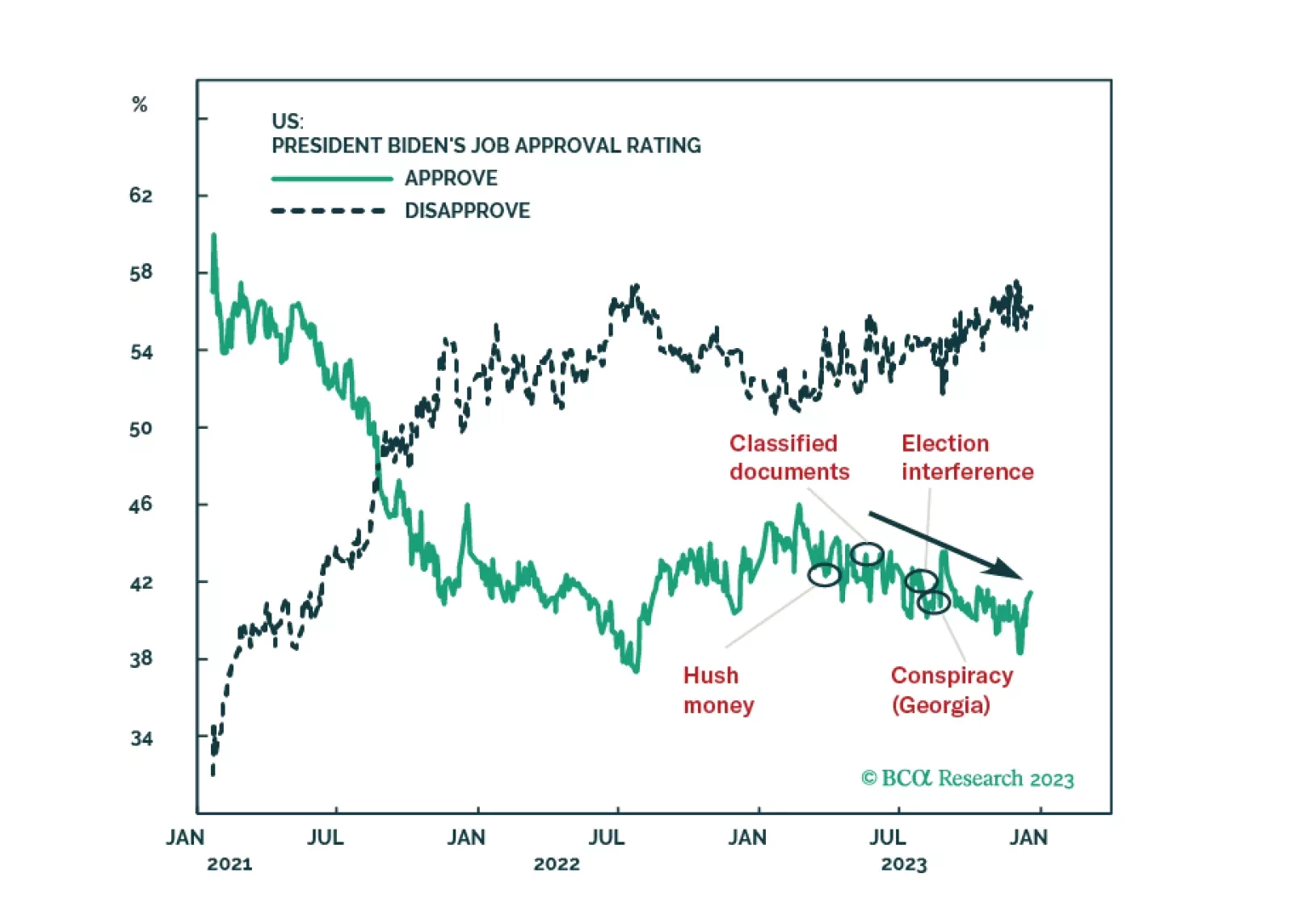

The Republican Party’s odds of winning the 2024 election will benefit, if anything, from state courts’ attempts to exclude President Trump from primary or general election ballots. Higher odds of a change of ruling party will increase stock and bond market volatility.

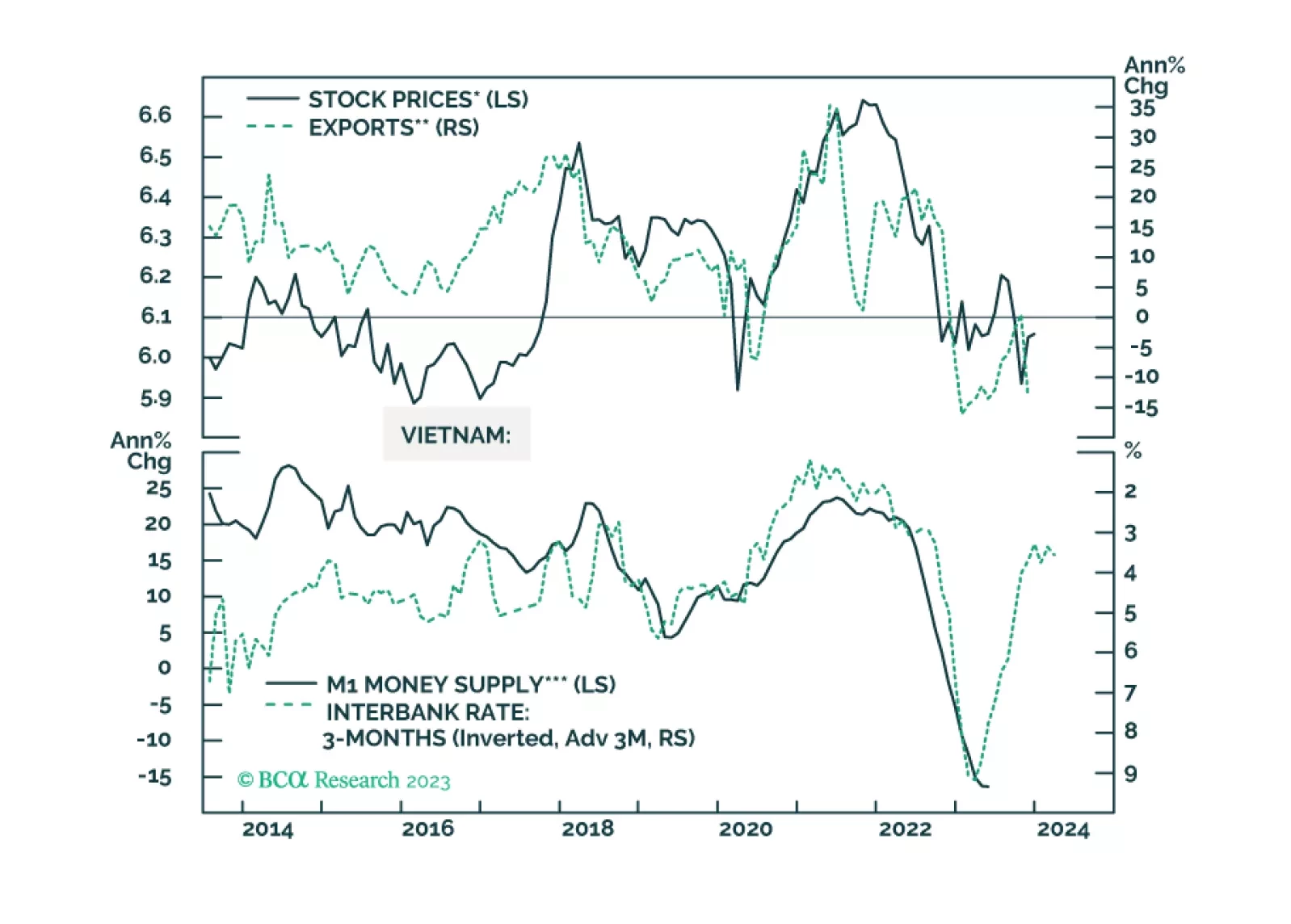

Vietnamese stocks may not see an immediate rally as global manufacturing and exports remain weak. But investors with longer-term horizons should stay overweight this market.

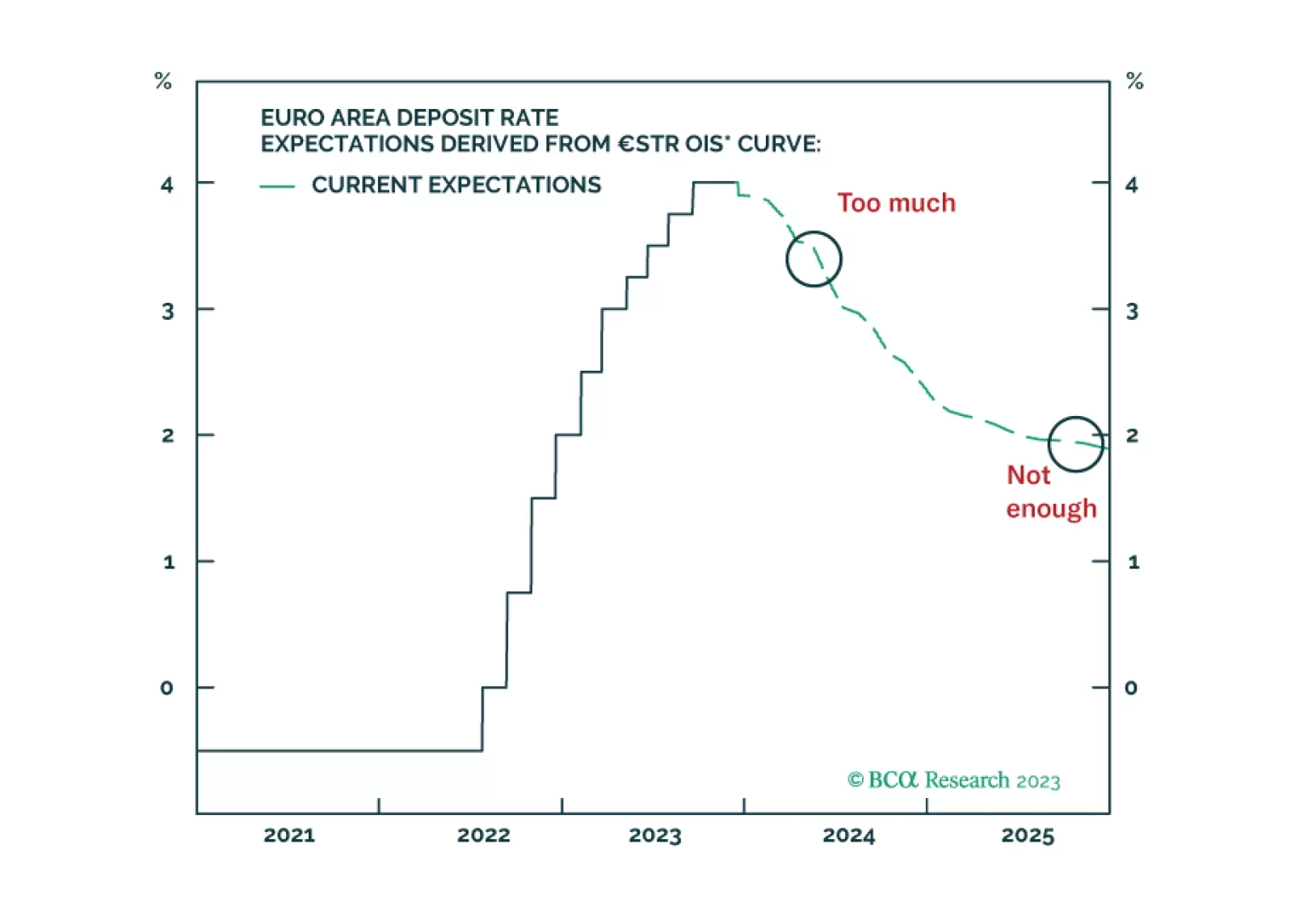

Explore the eight main themes that will drive the returns of European assets in 2024.

Our recommendations for blogs and X’s (on the economy, financial markets, asset allocation, bonds, quants, energy, real estate, geopolitics, and specific countries and regions) to try over the holidays.

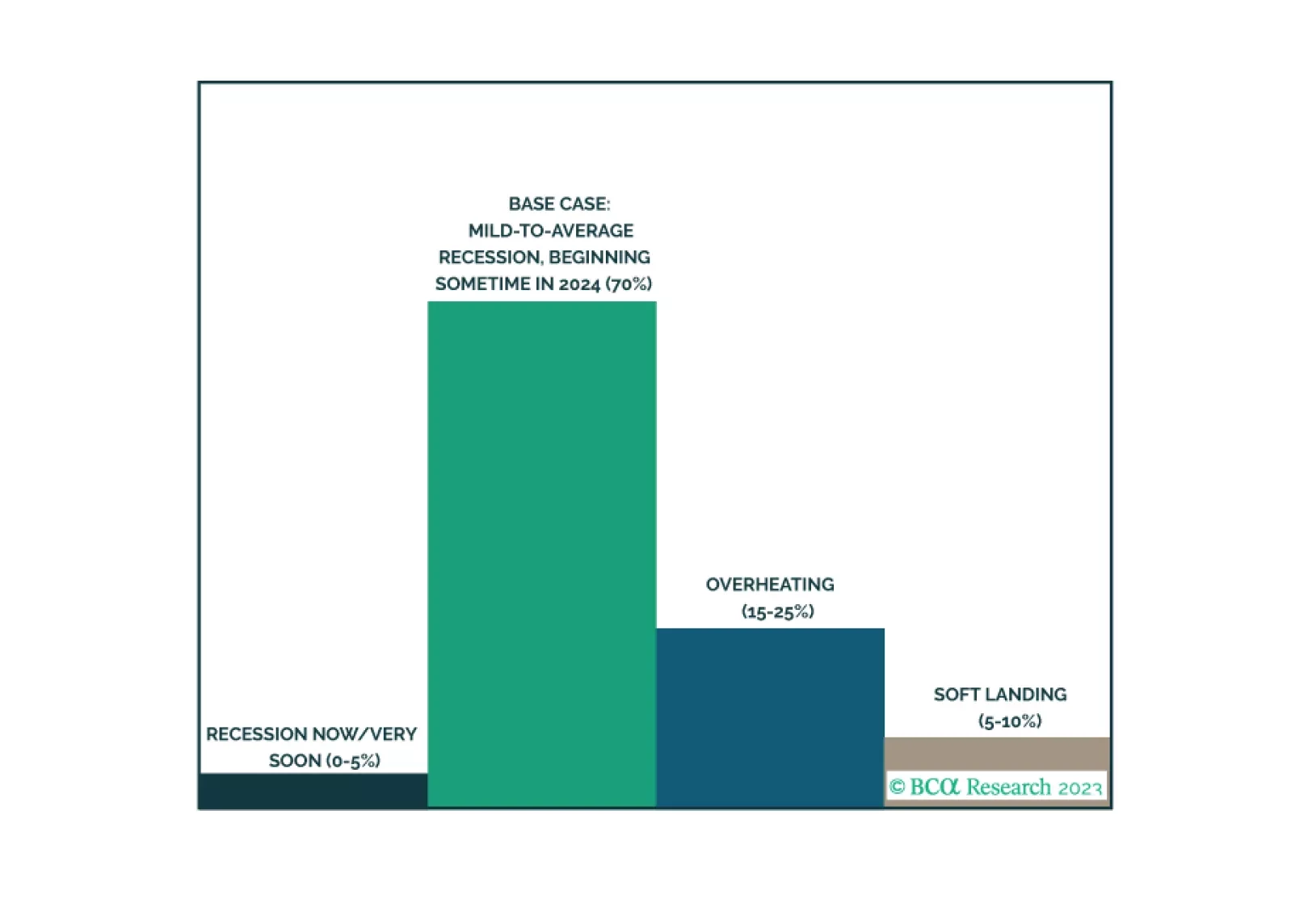

Our last publication of 2023 is an illustrated guide to our view that the economy will enter a recession around midyear. We expect equities will underperform Treasuries and cash over much of 2024, but we are waiting to turn tactically defensive until more investors are drawn into the soft-landing camp, capping the equity rally.

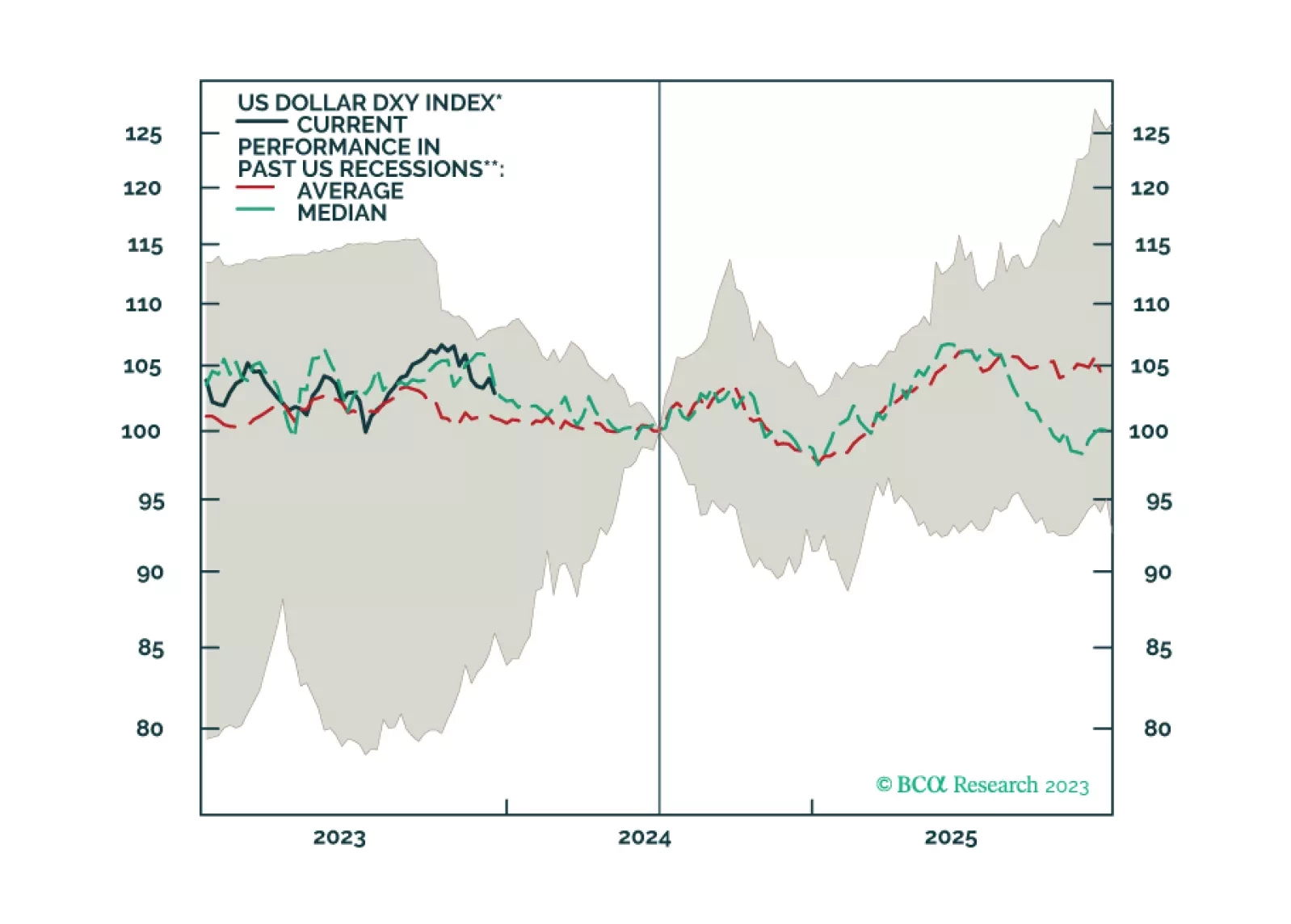

In this week’s report, we present our dollar view for 2024 and beyond, with a few trade ideas.