Economy

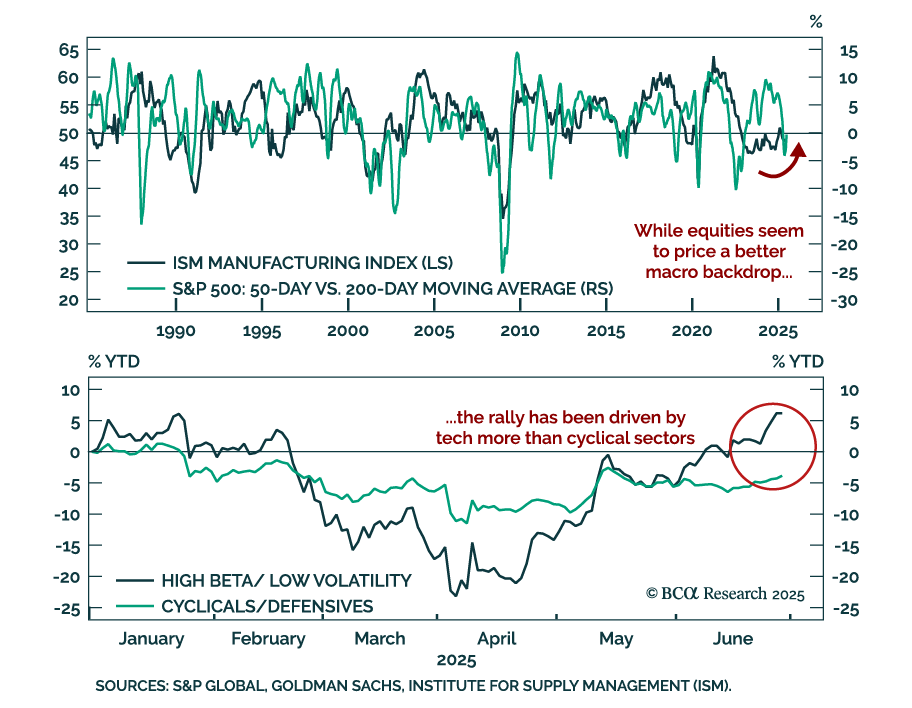

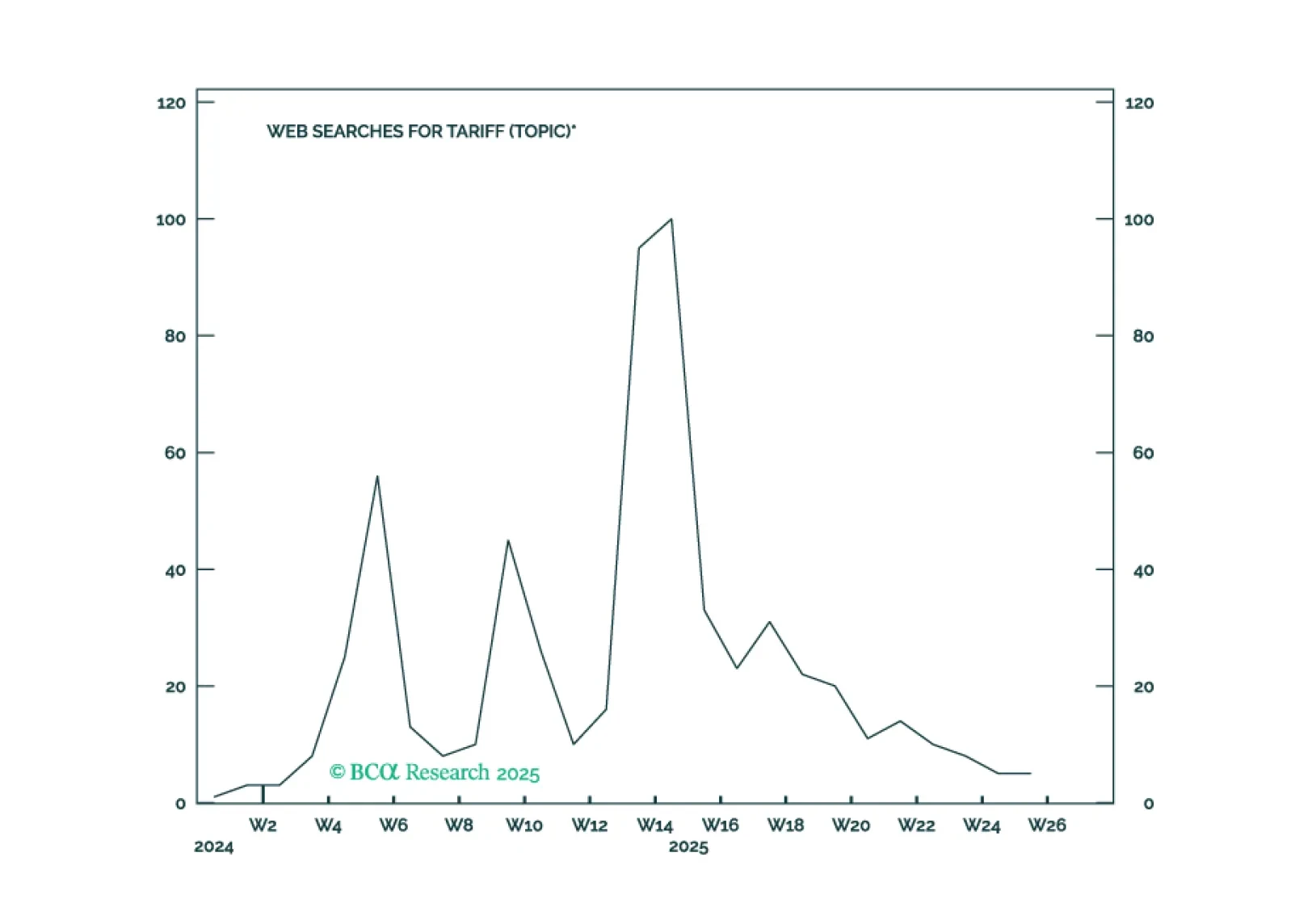

Tech-led momentum is driving the S&P 500 to new highs despite weak growth and rising cyclical risks. The rally has accelerated following a de-escalation in geopolitical tensions and ongoing hopes for positive trade developments. Momentum signals confirm…

Weak consumption data and deteriorating labor market signals reinforce our defensive stance. The May US Personal Income & Outlays report showed real personal spending declining 0.3% m/m, missing expectations, while core PCE inflation came in slightly…

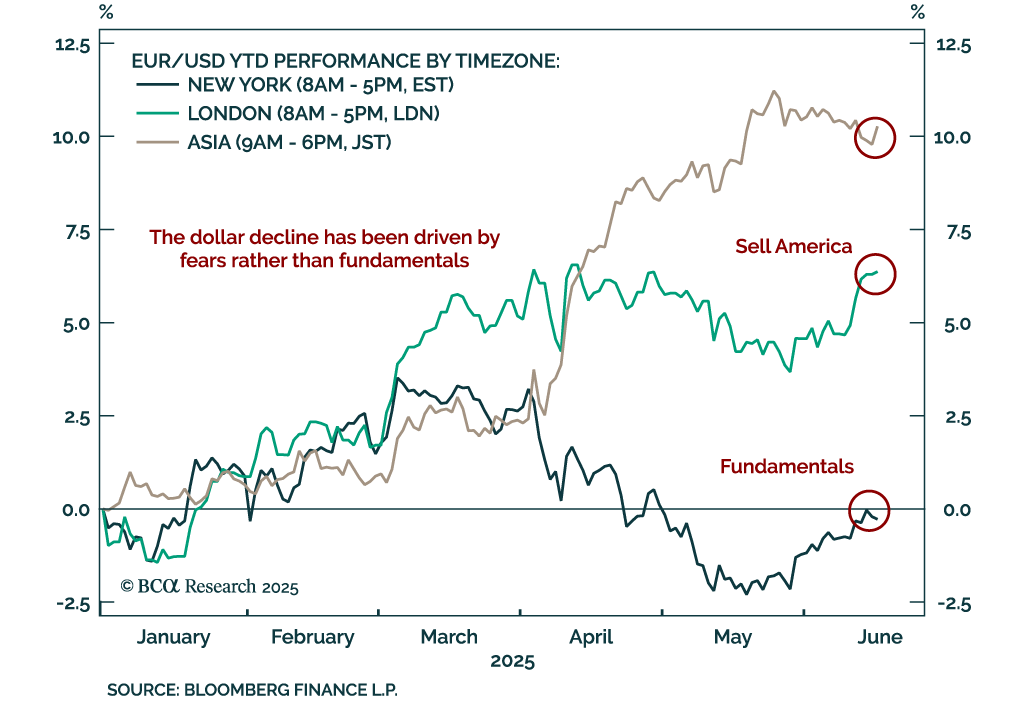

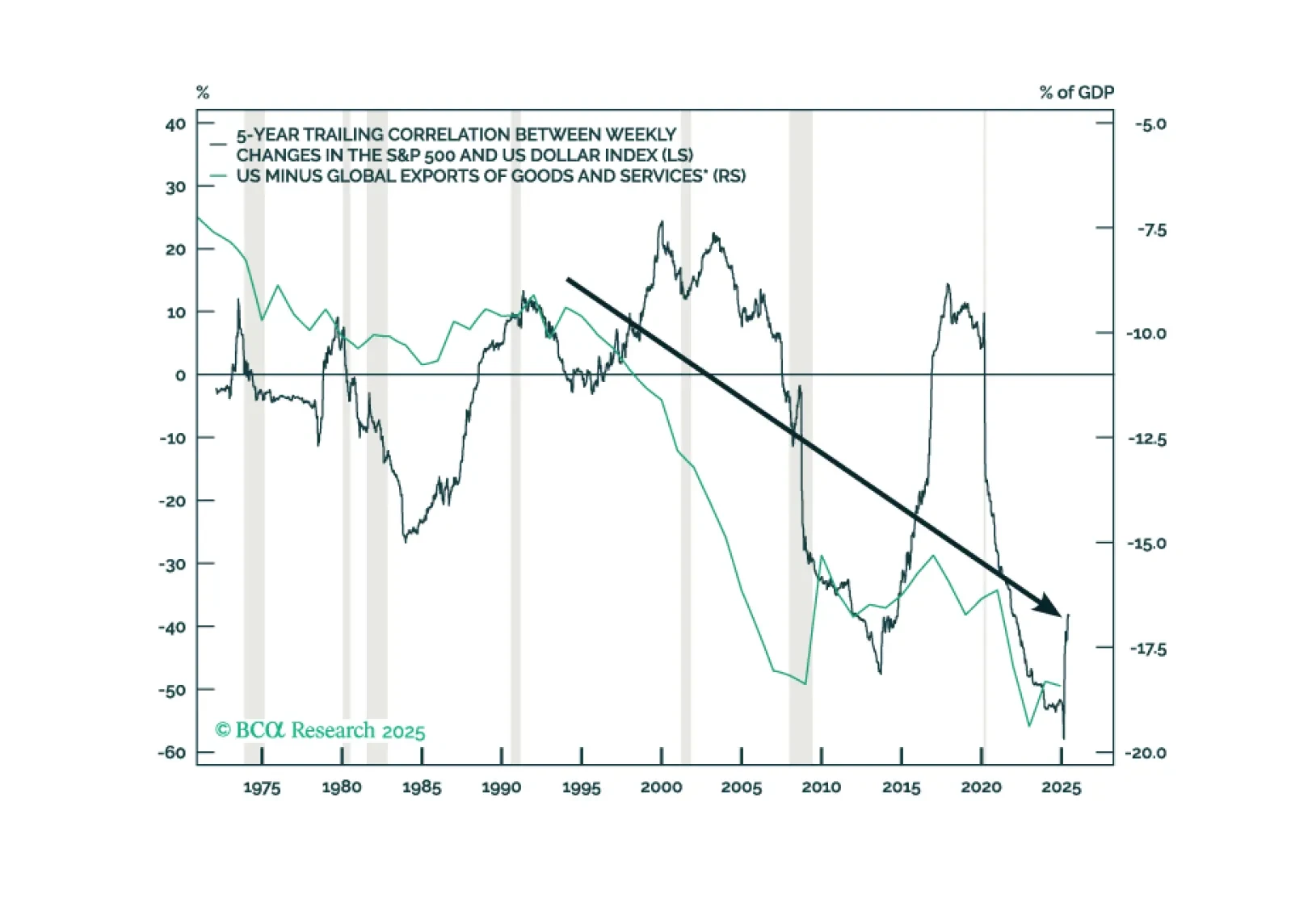

Foreign investors are selling US assets. Our Chart Of The Week comes from Juan Correa, Chief Global Asset Allocation Strategist. Splitting cumulative year-to-date EUR/USD returns by trading session reveals a clear pattern: The dollar weakens during…

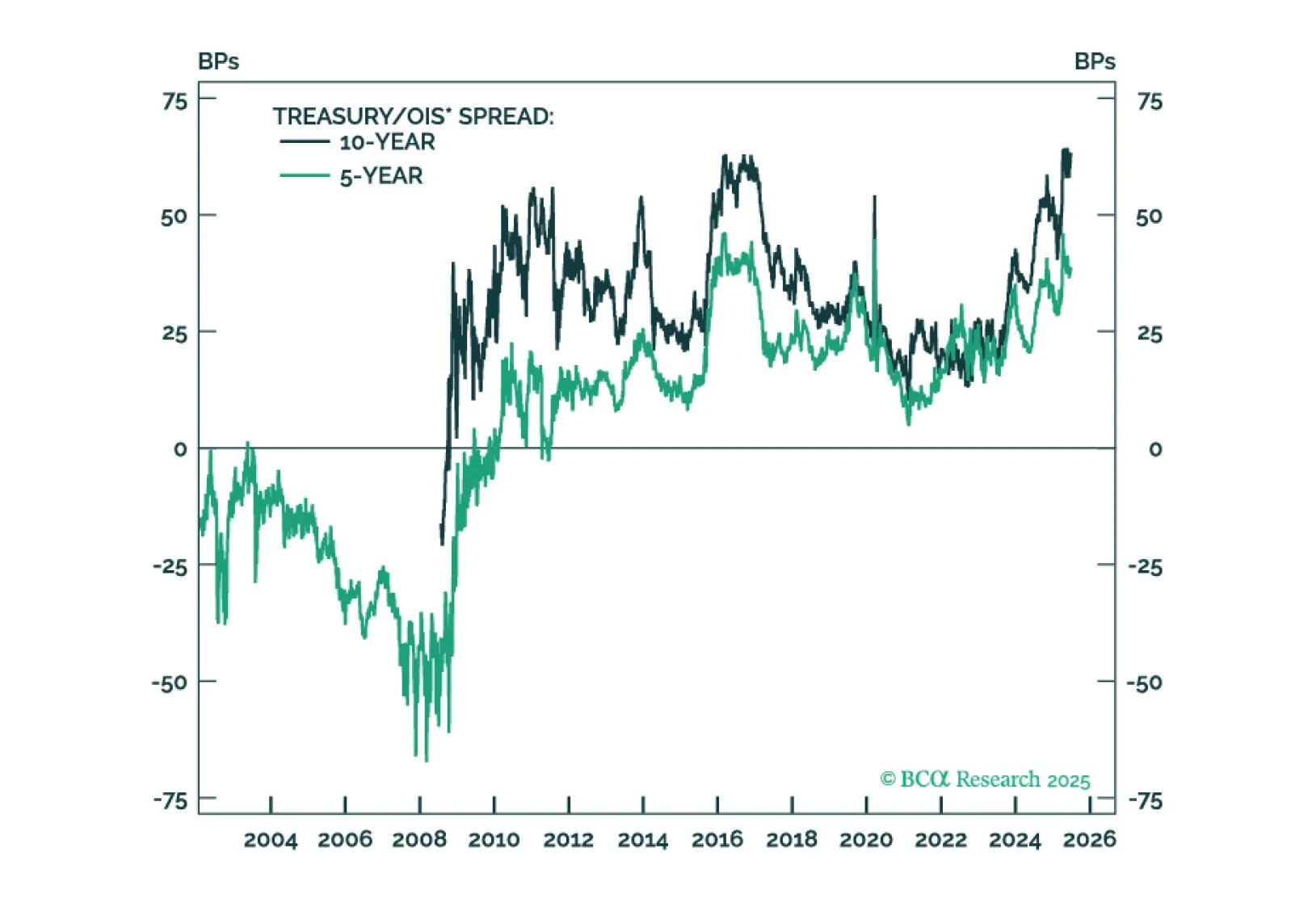

The Treasury/OIS spread has exerted notable upward pressure on Treasury yields during the past year, but the factors driving the spread are now turning more favorable.

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.

In Section I, Doug underscores that the full weight of tariffs has yet to be felt on the US and global economies, against the dangerous backdrop of a softening labor market. In Section II, Jonathan presents the bullish case for the US dollar over the coming year.

In Section II, Jonathan presents the bullish case for the US dollar over the coming year.

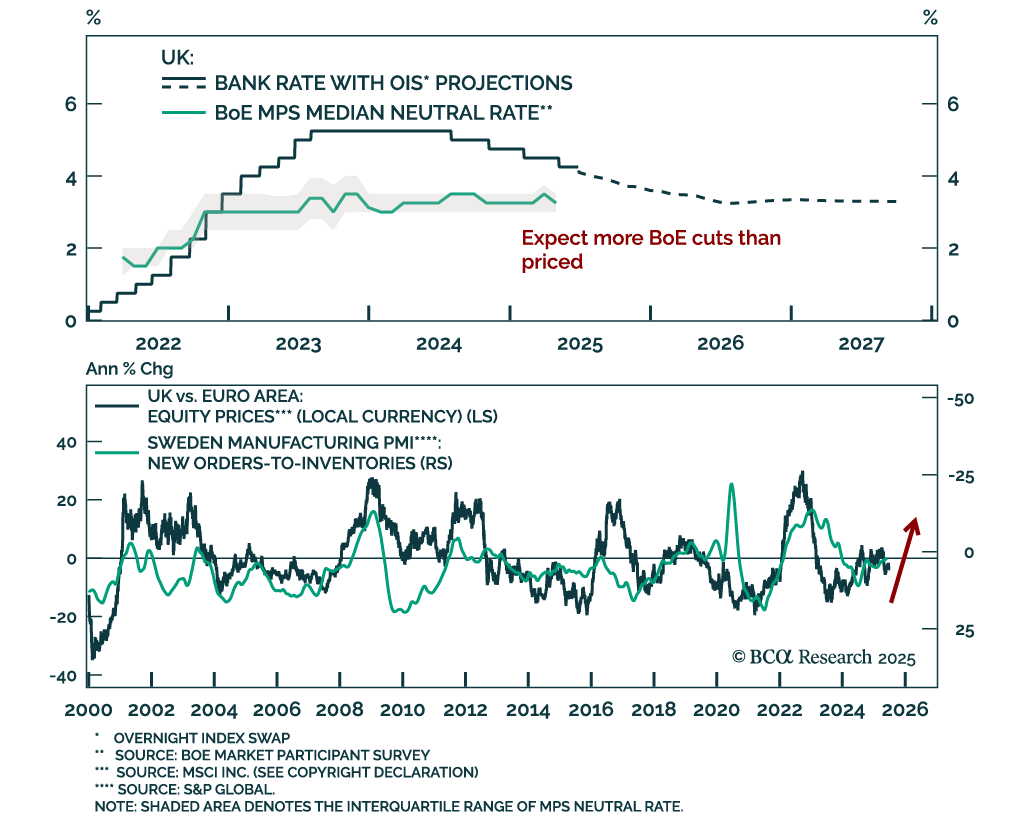

Our Global Fixed Income, FX, and European strategists expect aggressive BoE easing amid disinflation and labor market weakness, supporting an overweight in Gilts and UK equities versus the euro area. While UK productivity remains sluggish, a recovery in labor…

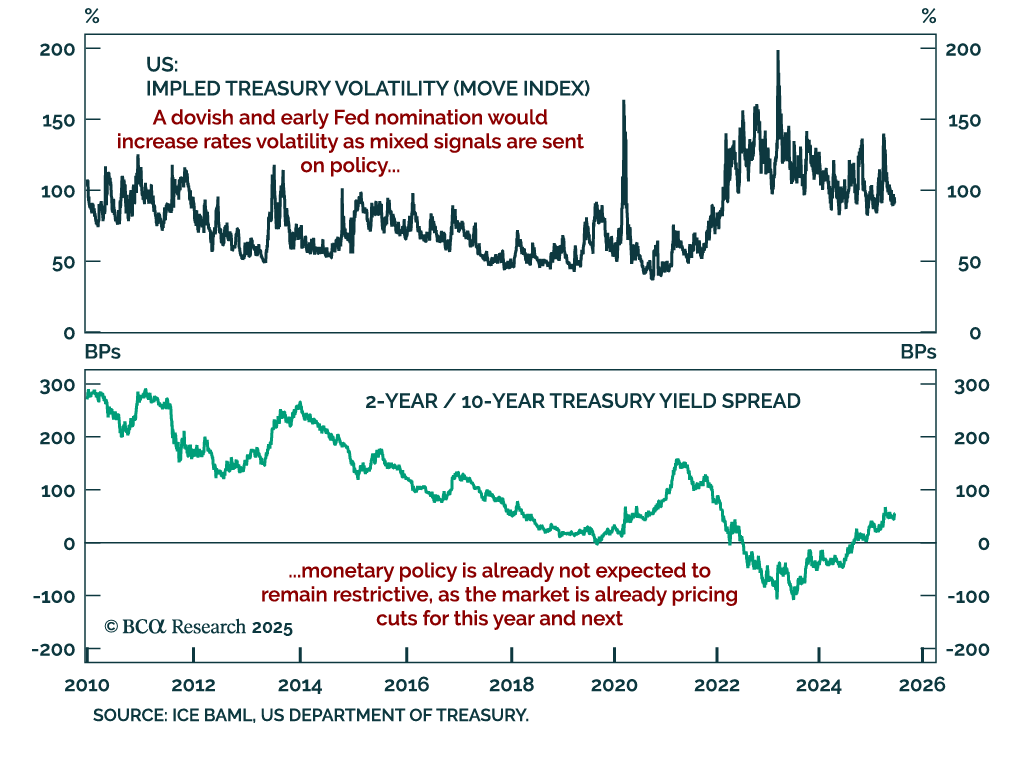

A dovish early Fed nominee would increase volatility in rates and FX as markets reassess the credibility of US monetary policy. News reports indicate the Trump administration is considering nominating a Fed successor ahead of the end of Chairman Powell’s…

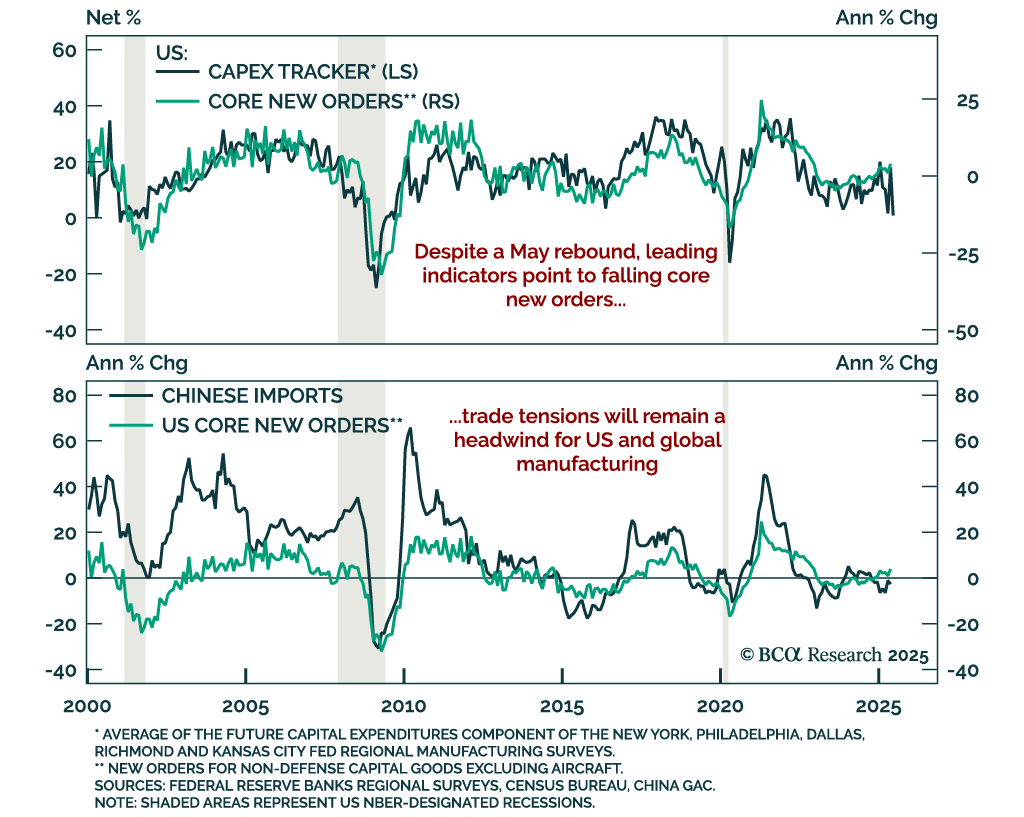

Headline strength in US capital goods orders is unlikely to last, reinforcing our defensive stance and preference for steepeners. New orders for core capital goods (nondefense ex-aircraft) rose 1.7% m/m in May, beating expectations after a 1.5% drop in April.…