Economy

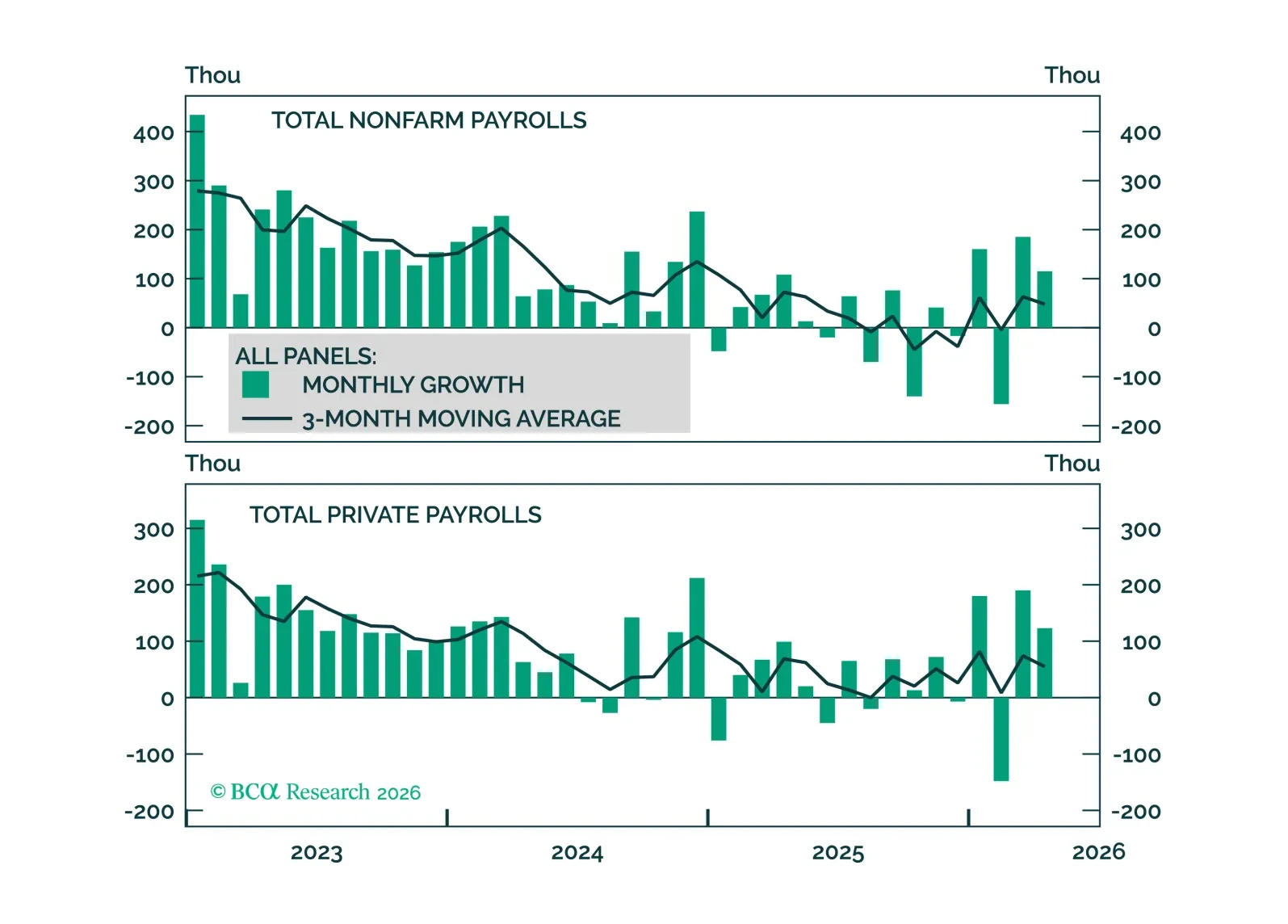

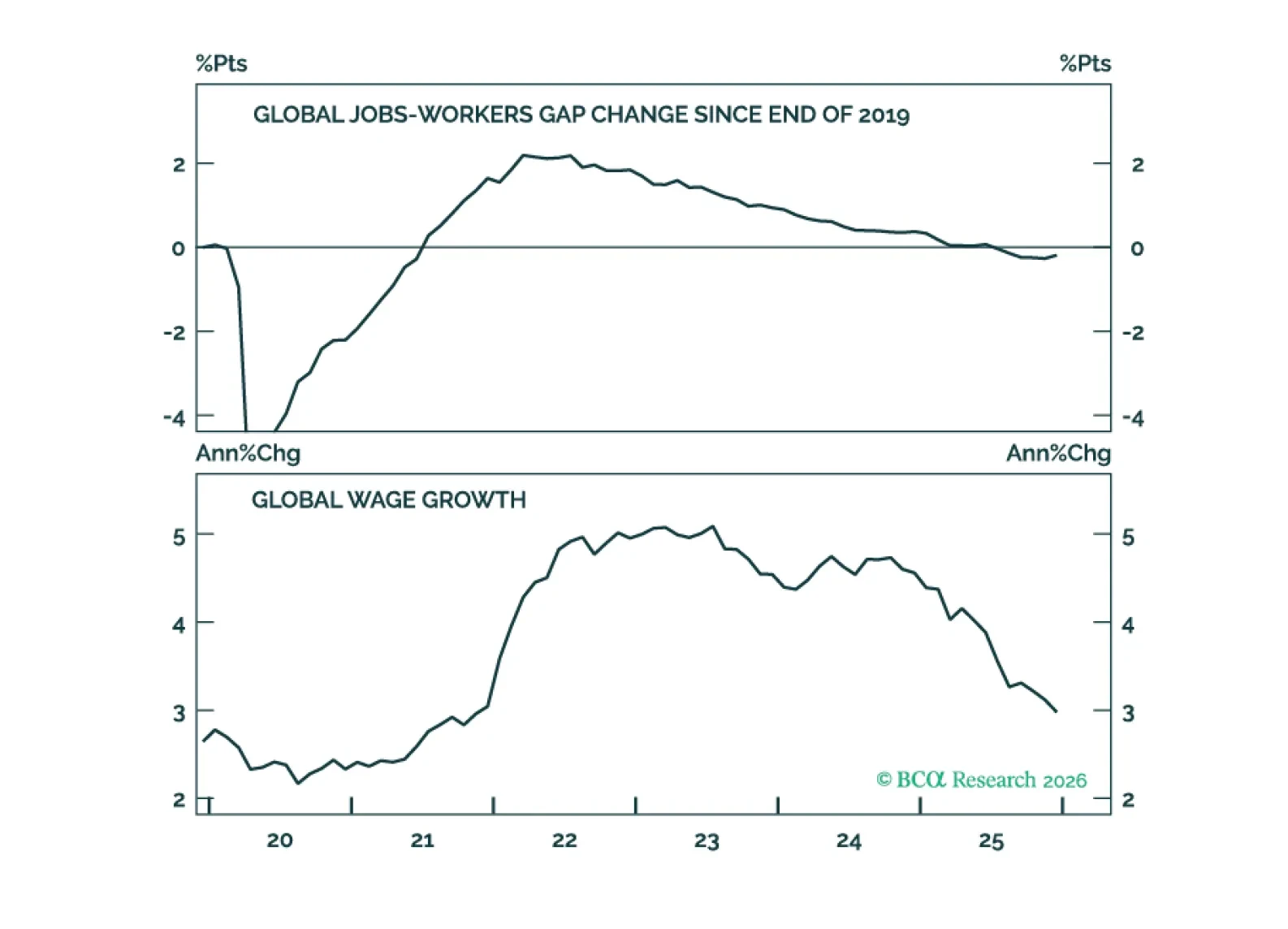

Improving job growth keeps Fed rate cuts off the table, but evidence of labor market tightening will be required before rate hikes become part of the discussion.

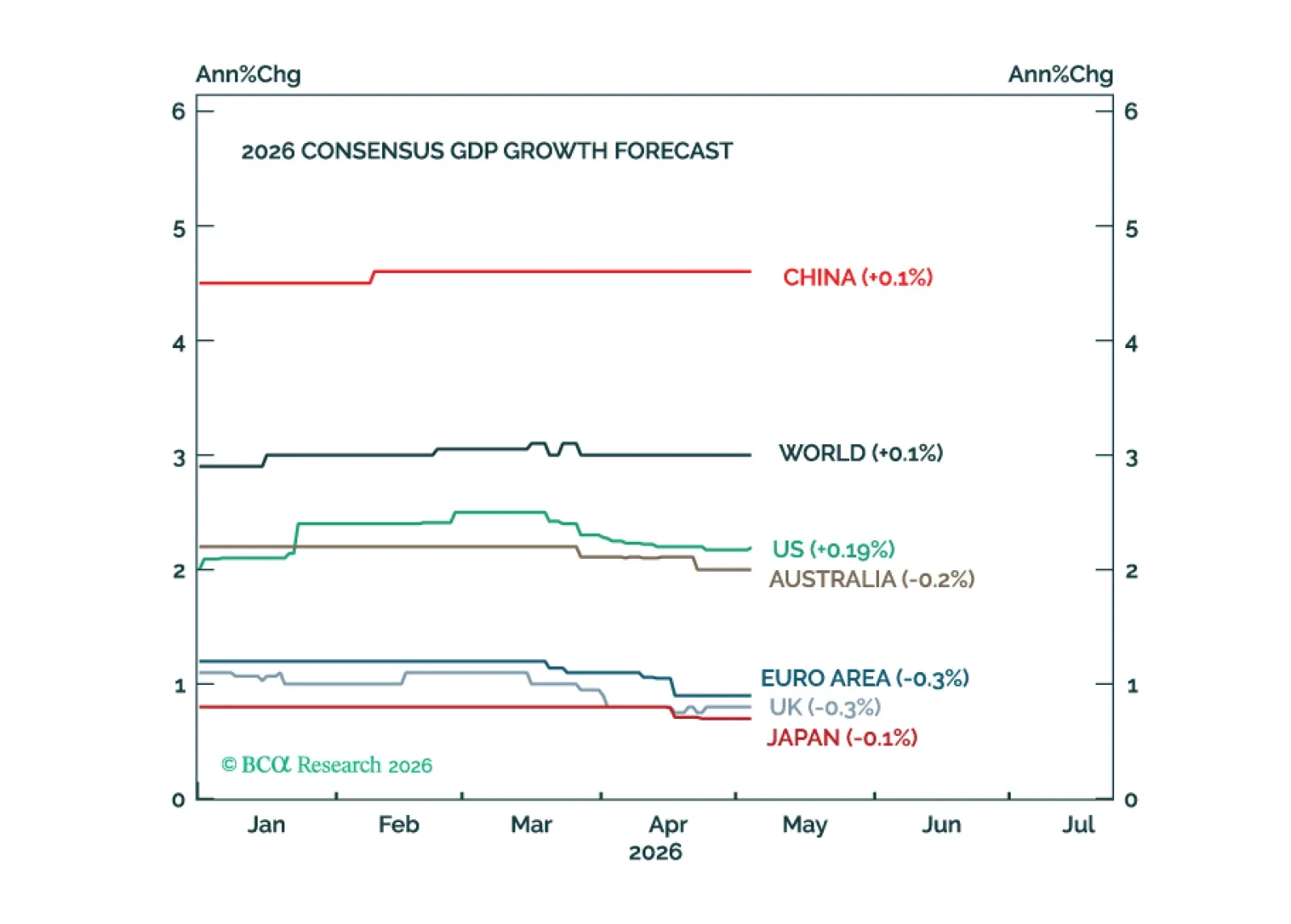

Our Portfolio Allocation Summary for May 2026.

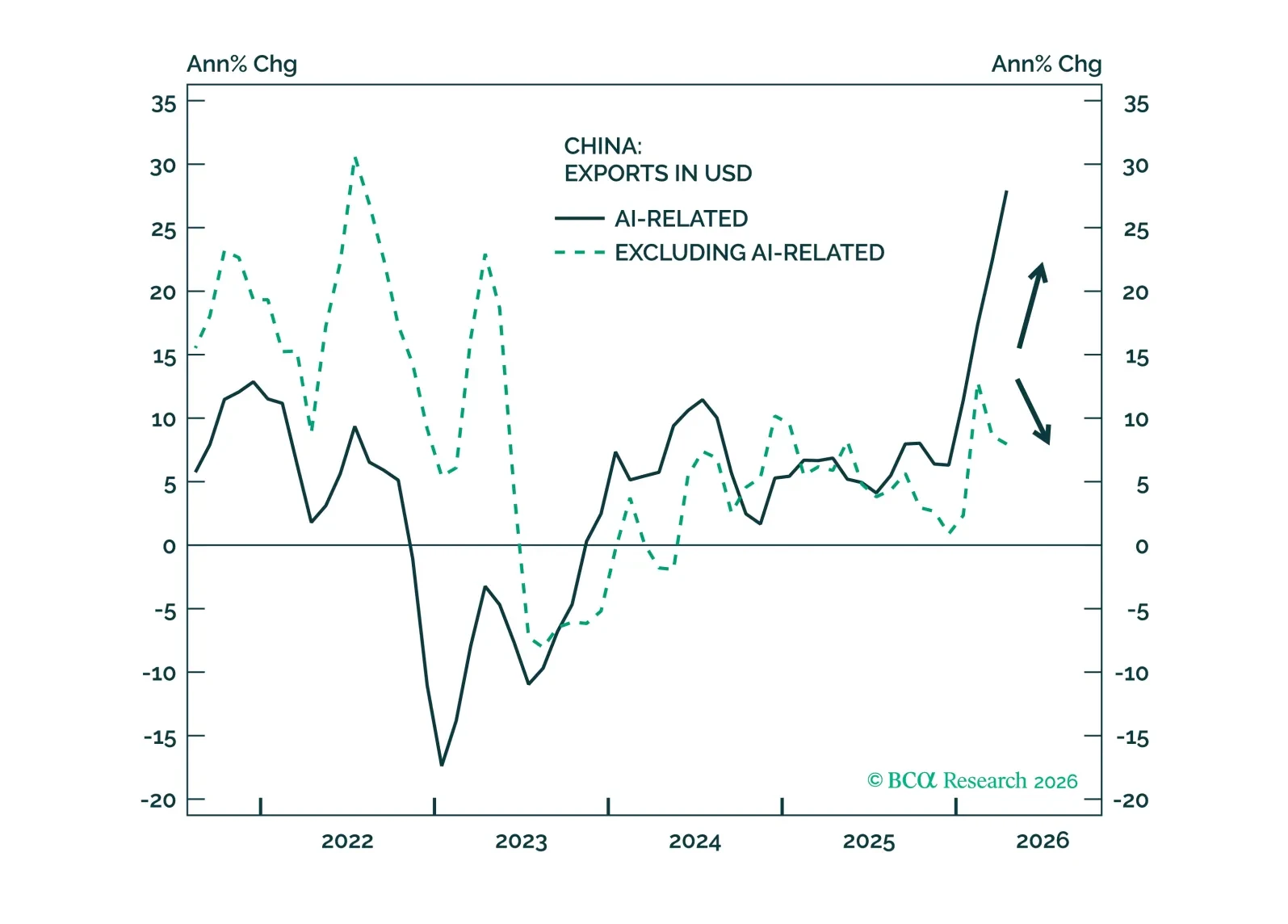

China’s K-shaped economy is widening, with resilient exports and subdued domestic consumption. Over the next 6–12 months, we see a higher probability that global capex momentum persists than China delivers meaningful consumer-focused stimulus.

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

So far, there is no evidence of second-round effects from the oil price shock showing up in the US economy. Fed rate hikes are off the table unless those effects emerge.

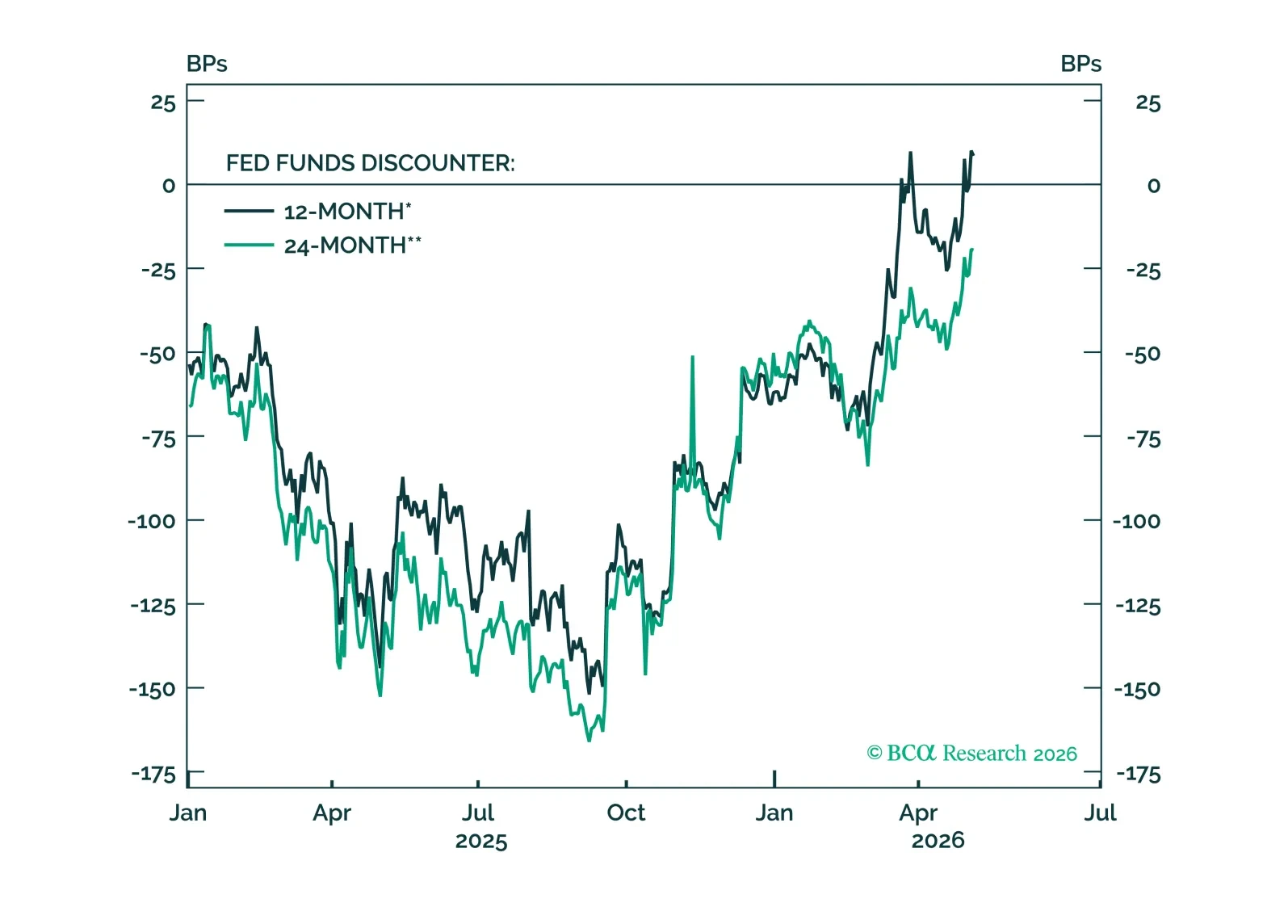

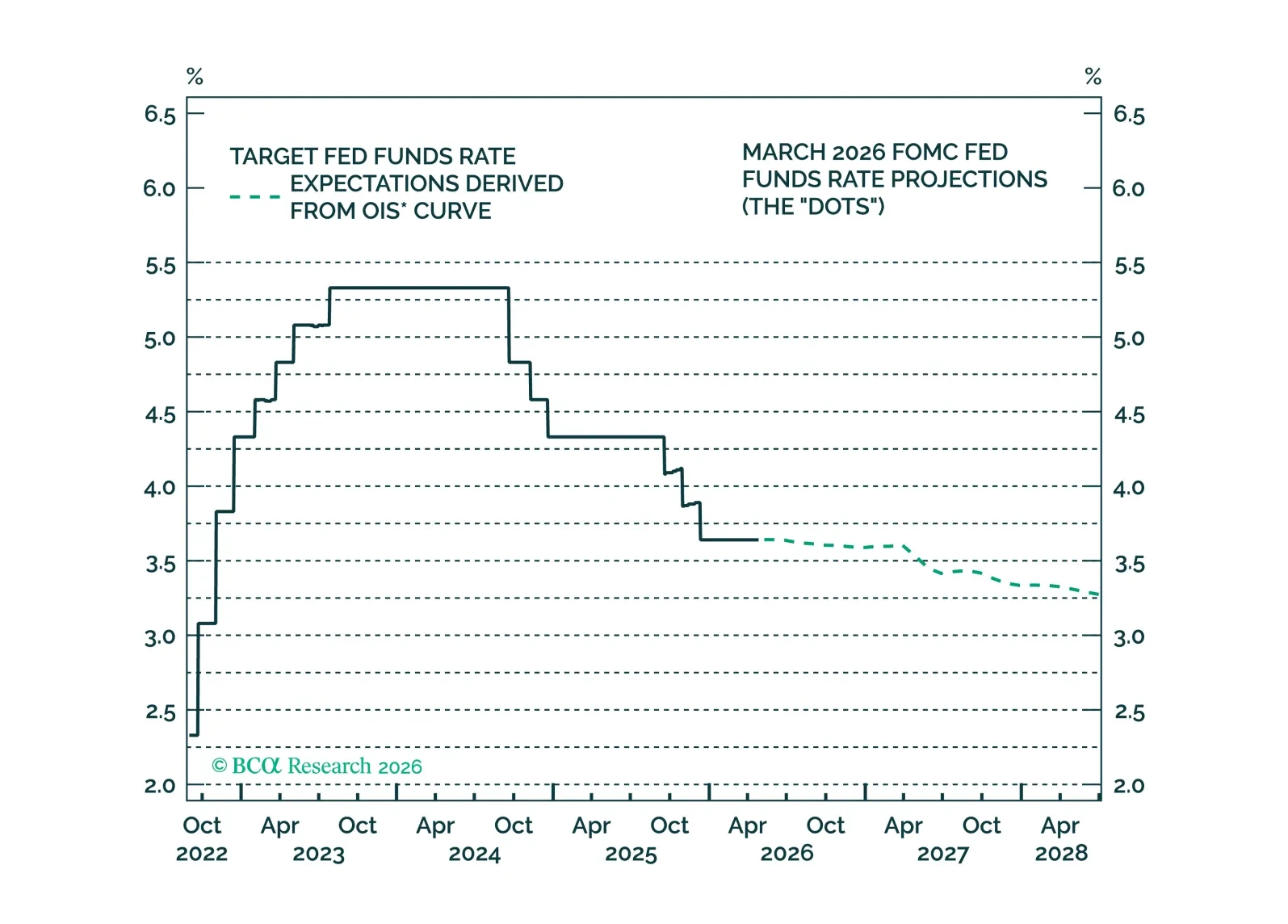

FOMC participants are coalescing around the idea that the funds rate will stay on hold for some time, an outcome that is now well priced in the bond market and that will not materially change under a new Fed Chair.

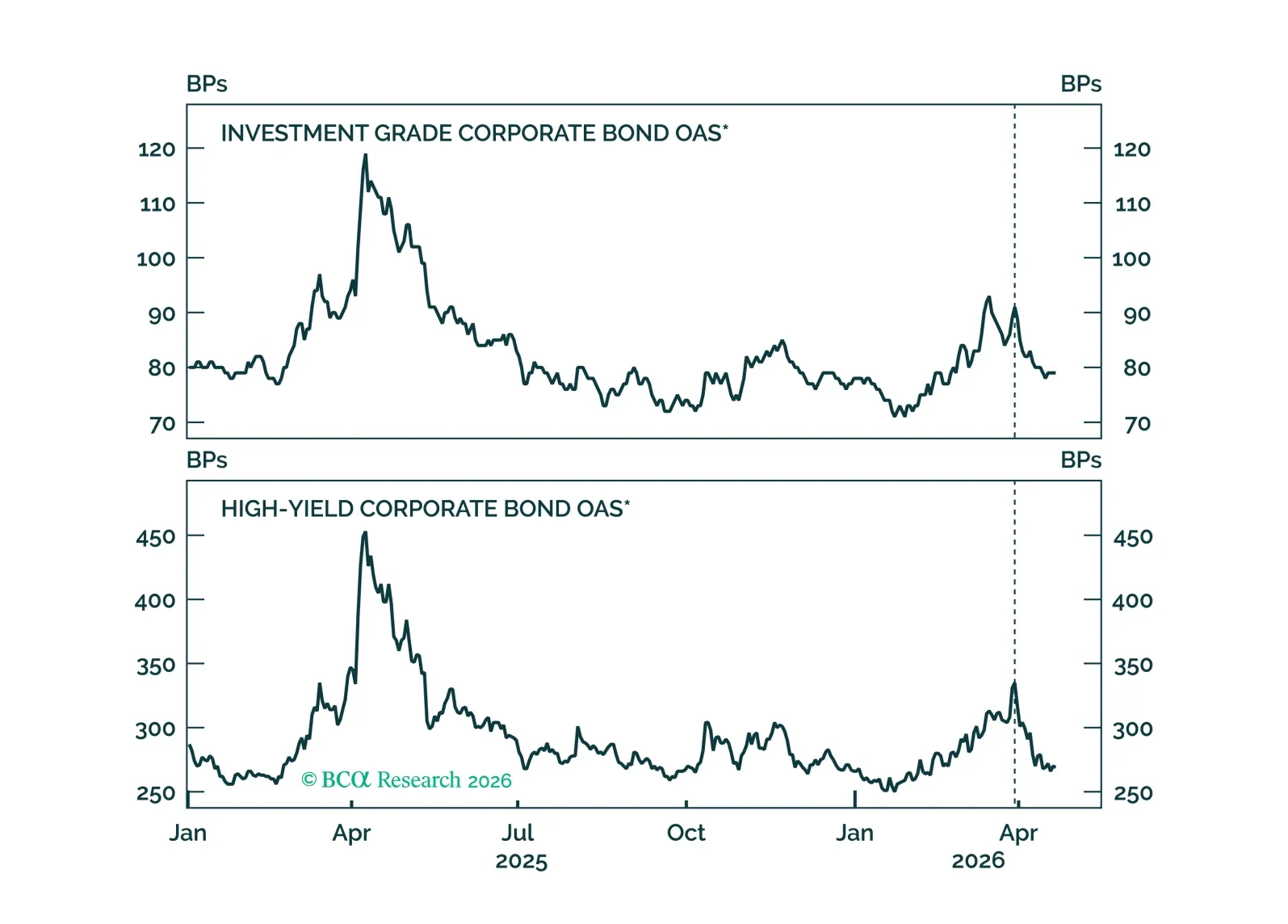

We recommend increasing exposure to spread product as the US economy transitions back into a low rate vol regime.

We do not expect the oil shock to have a lasting effect on inflation. Looking further out, a variety of structural forces will influence inflation, including fiscal policy, globalization, demographics, and AI.

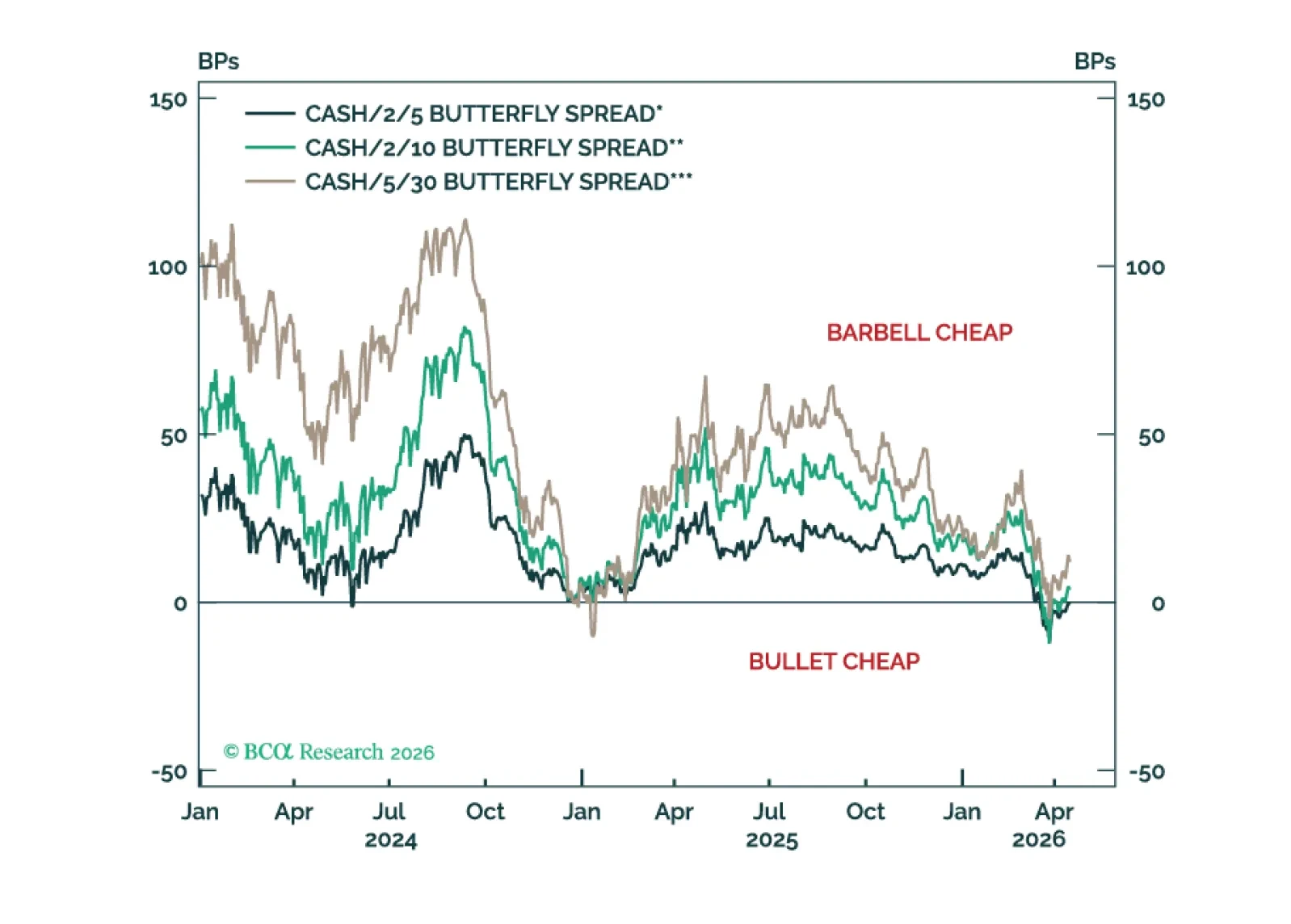

The rates market is moving back into a low vol regime, but with yields at a higher level. This argues for maximizing carry across the Treasury curve.

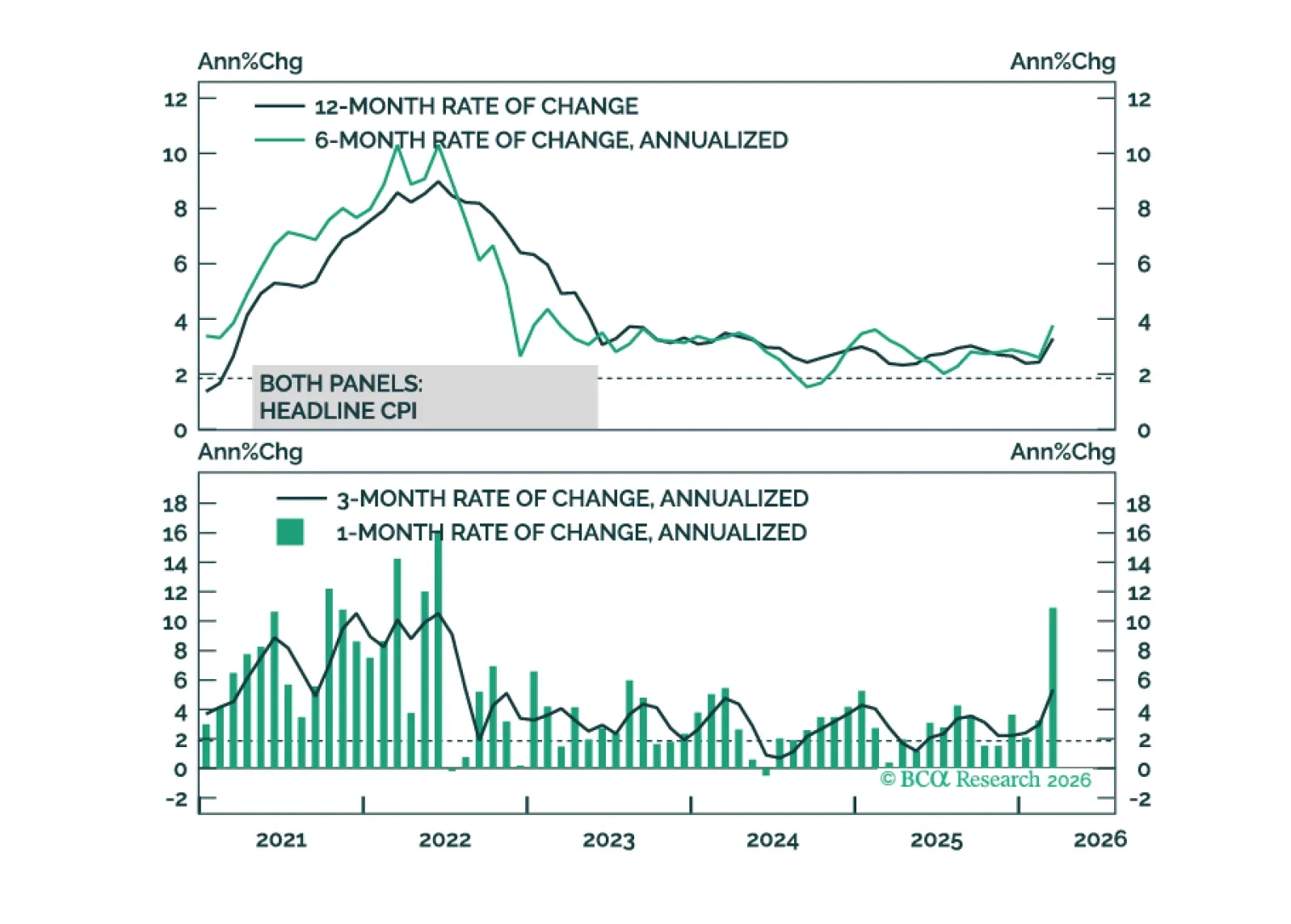

Inflation’s underlying trend was headed lower prior to the Iran war. This makes the recent back-up in bond yields look like an attractive buying opportunity.