Economy

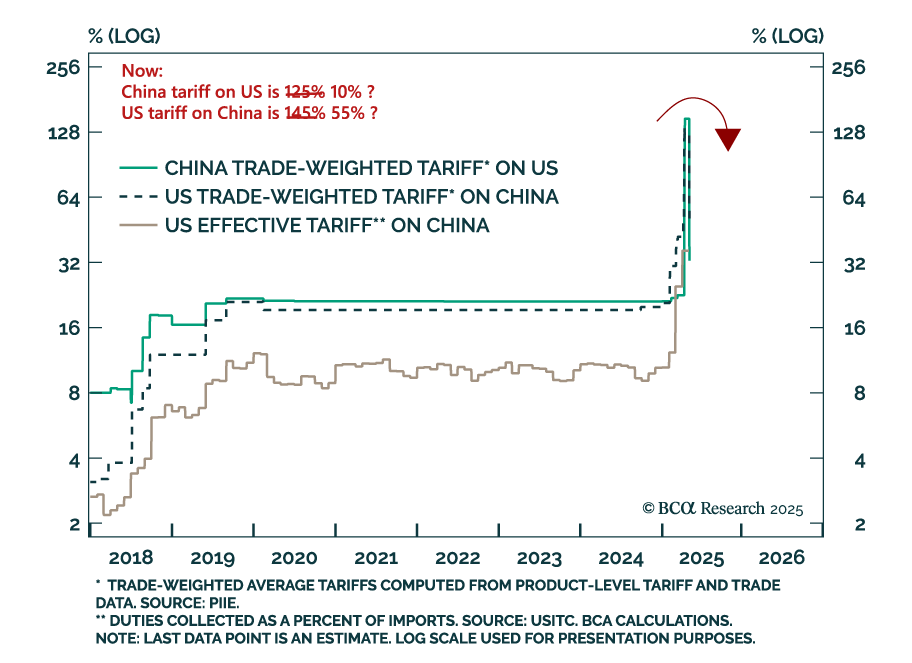

The US-China tariff deal confirms one thing: markets are still priced for perfection, with little upside even if a recession is dodged. The London negotiations yielded a partial agreement: The US will reduce tariffs, and China will remove export restrictions…

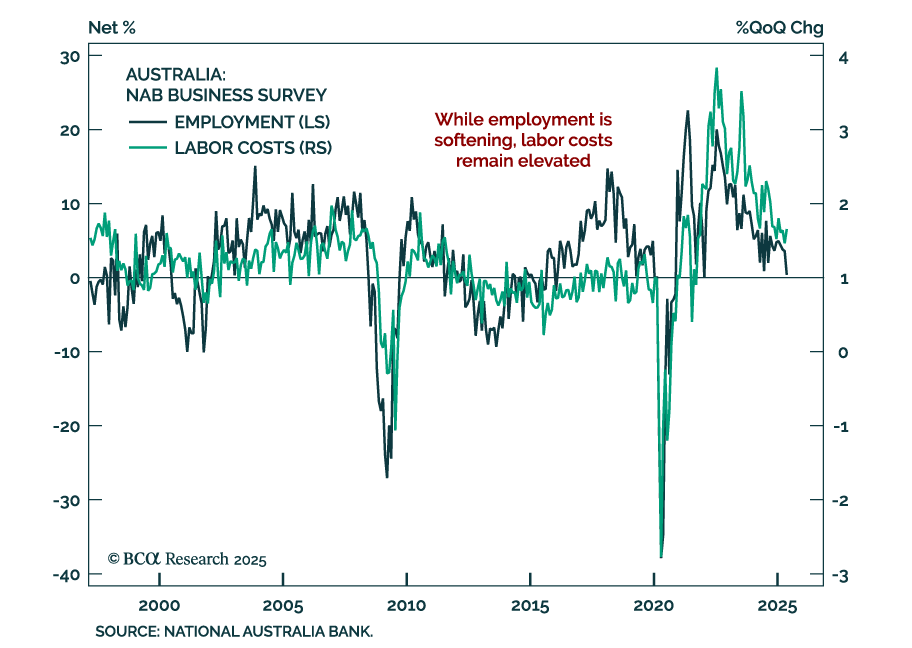

Mixed signals from the NAB Business Survey reinforce our underweight in Australian government bonds and long AUD exposure. In May, business confidence rebounded slightly, rising to 2 from -1, but current conditions dipped to 0 from 2. Profitability continued…

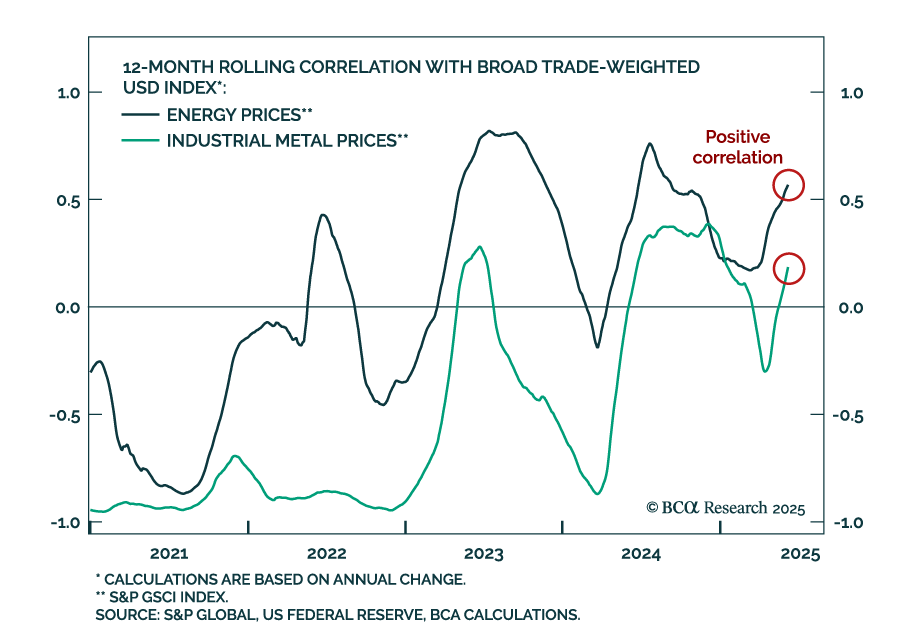

Our Commodity strategists see a breakdown of historical commodity correlations. The US dollar now shows a positive correlation with commodities, particularly energy, and a weaker dollar will no longer guarantee upside for commodity prices. Softening global…

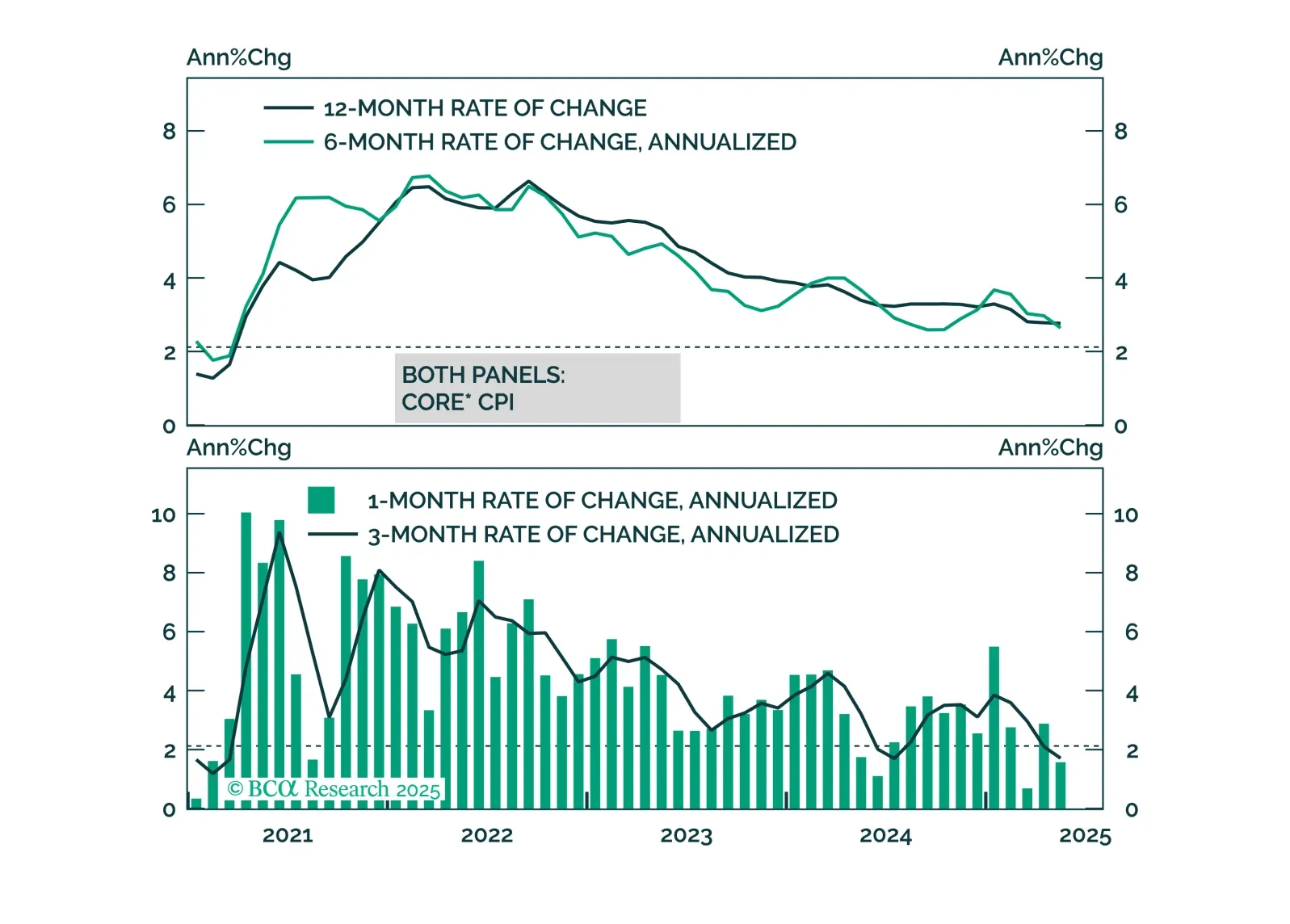

Colder May CPI reinforces our overweight in government bonds and tactical steepener trades as growth slows and the Fed stays cautious. Headline inflation rose 0.1% (2.4% y/y), below expectations, as did core CPI (2.8% y/y). Goods inflation was flat, and…

While we anticipate higher inflation in June, it looks increasingly likely that the price impact from tariffs will be less aggressive and long-lasting than many feared.

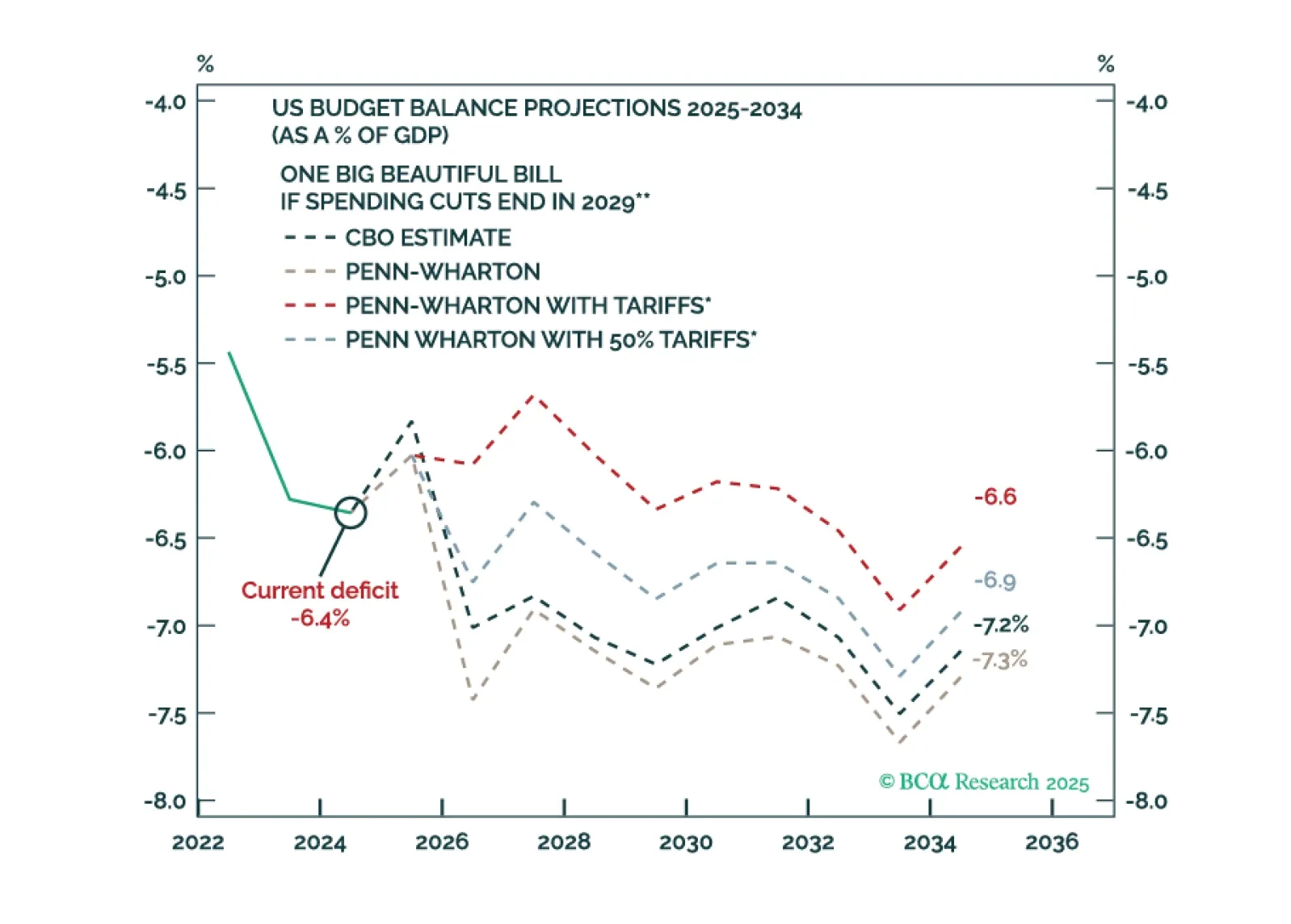

Bond market volatility will spike again in the near term. The Fed is committed to an easing cycle yet the Trump administration’s signature fiscal policy action will stimulate the economy. Tariffs are supposed to keep the budget deficit contained but they are inflationary.

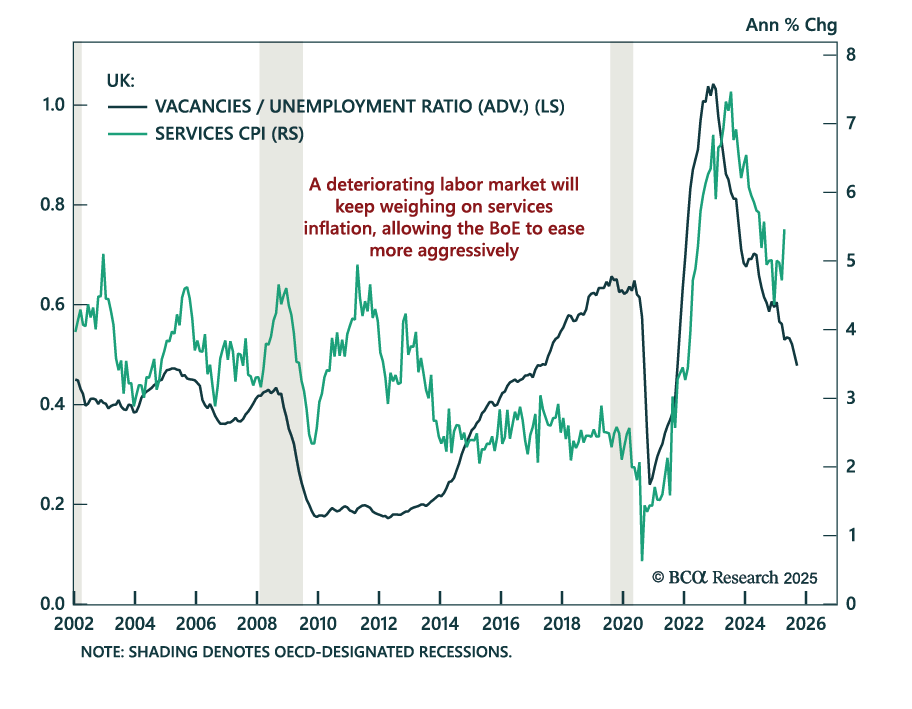

UK labor market deterioration reinforces our overweight on Gilts and dovish BoE policy trades. Payrolls fell by 109k in May, an acceleration from the 55k revised decline for April (originally reported as -33k), and job vacancies continued to slide. Slower…

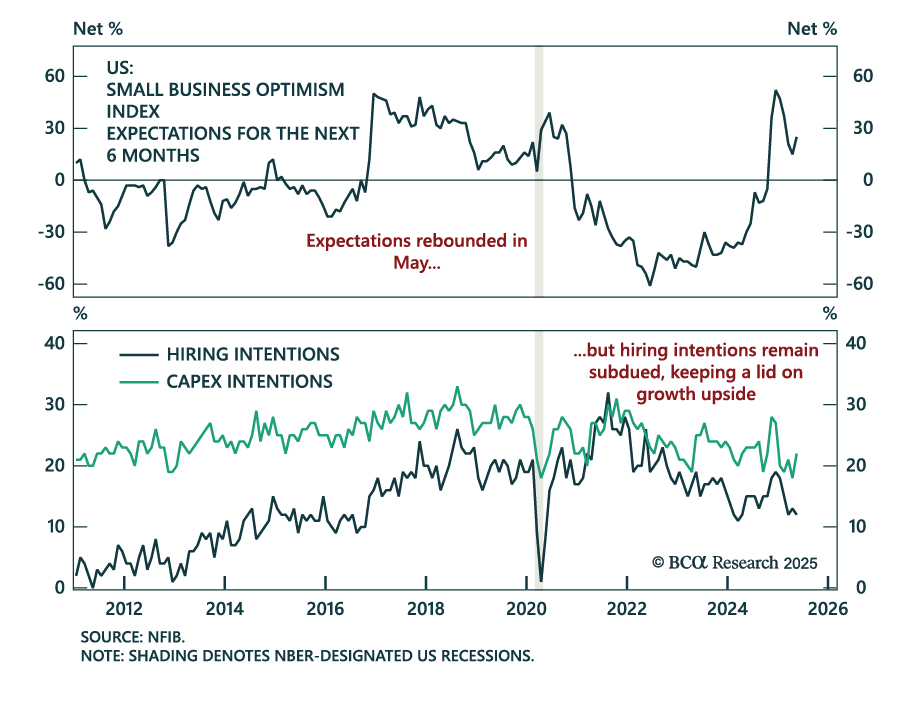

Small business confidence improved in May, but hiring intentions fell and activity remains sluggish, reinforcing our cautious equity stance. The NFIB Small Business Optimism Index rose to 98.8, beating expectations. However, most of the improvement came from…

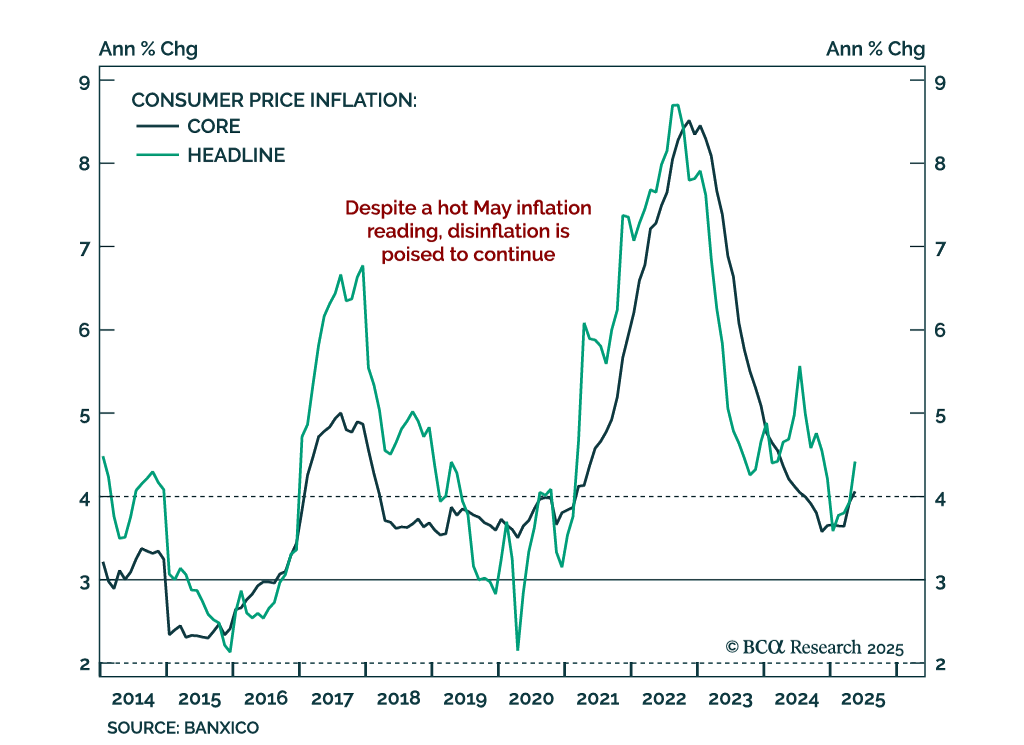

Hot May inflation should not derail Banxico’s easing cycle; we remain long Mexican local bonds. Headline inflation accelerated to 4.4% y/y from 3.9%, above expectations, while core inflation was roughly flat at 4.1% from 3.9%. The upside surprise was driven…

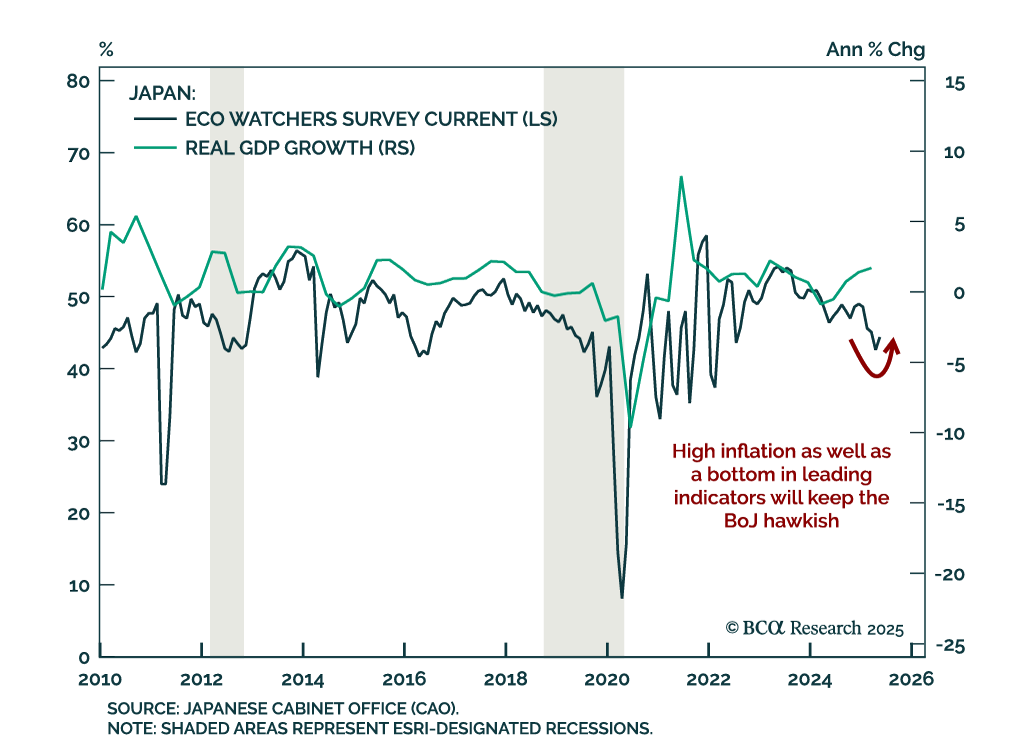

The BoJ will stay hawkish because of sticky inflation and better economic momentum. The May Eco Watchers Survey beat expectations, with current conditions rising to 44.4 and the outlook to 44.8. These levels still signal contraction, but the uptick,…