Economy

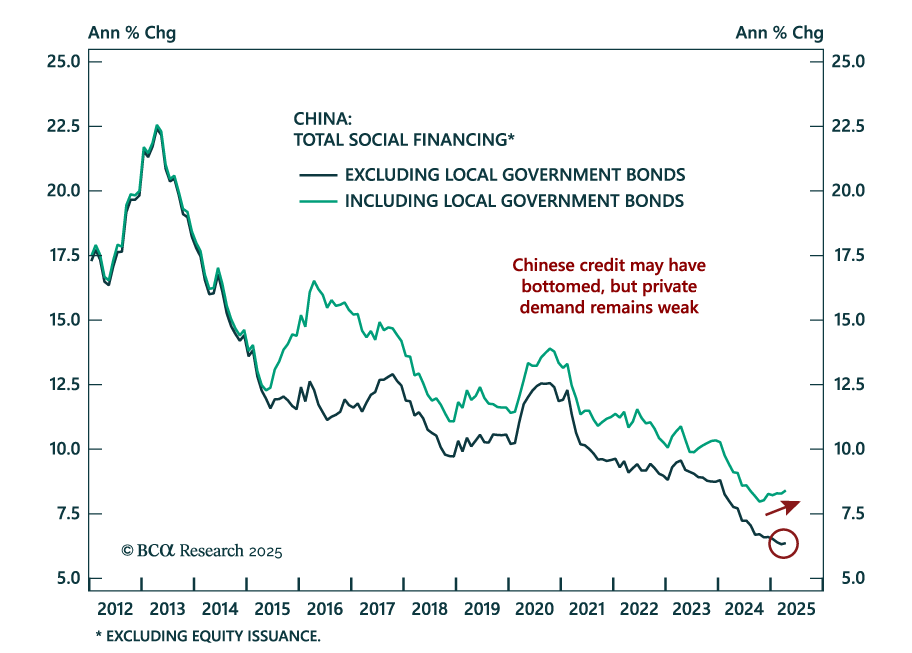

China’s weak April credit data reinforces the case for defensive positioning, with policy aimed at stability, not recovery. New yuan loans and aggregate financing both rose less than expected. While credit growth may have bottomed, it remains public-sector…

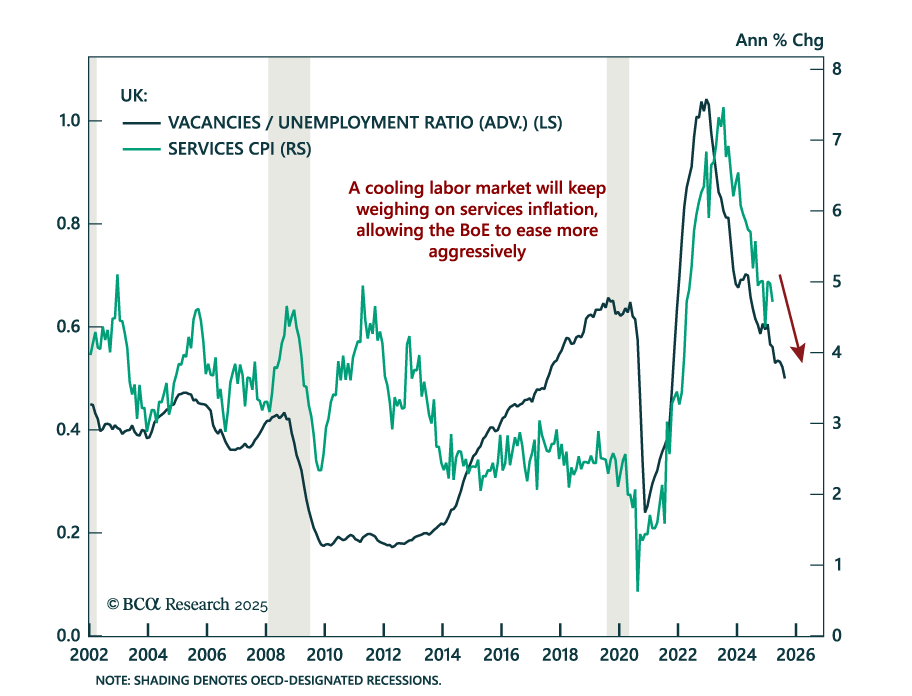

UK labor market weakness is reinforcing the case for BoE cuts and supporting our overweight in UK Gilts. April payrolls fell by 33k, marking a third consecutive monthly decline, while job vacancies remain below pre-COVID levels for the first time in nearly…

April’s CPI came in cooler than expected, but tariff-driven supply shocks will keep the Fed tight, supporting long-duration exposure. Headline CPI rose 0.2% m/m (2.3% y/y) while core inflation held steady at 2.8%. Services inflation remained firm at 3.7%, and…

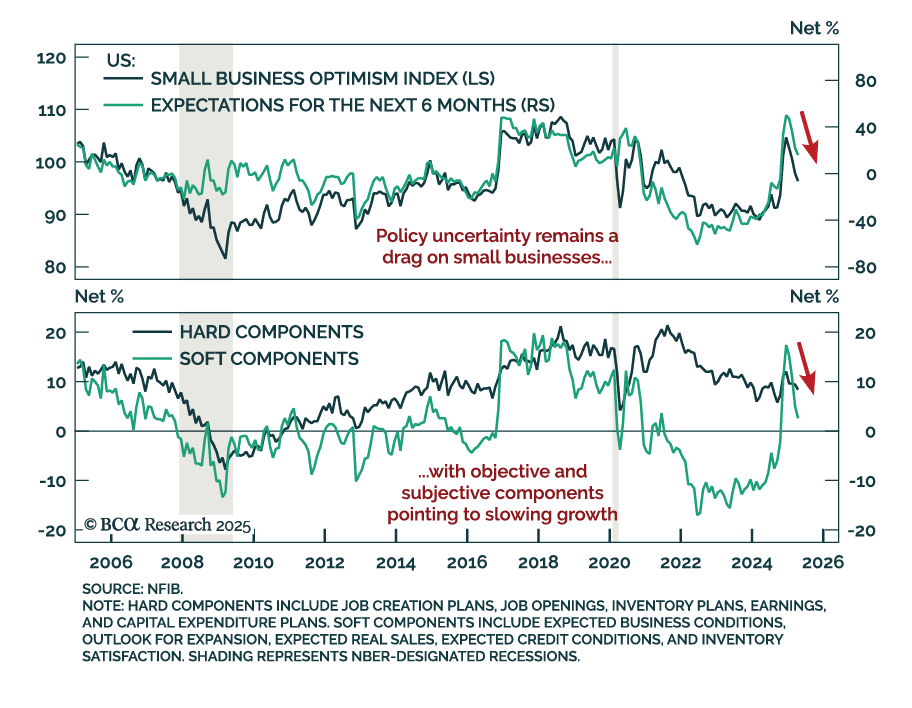

Small business sentiment remains recessionary, supporting our defensive asset allocation stance. The NFIB Small Business Optimism Index fell less than expected to 95.8, reinforcing the cratering in soft data witnessed since the election with policy…

A weakening economy will apply downward pressure to Treasury yields, but the Trump term premium will keep long-dated yields higher than they would otherwise be. This makes Treasury curve steepeners the most attractive trade in US fixed income.

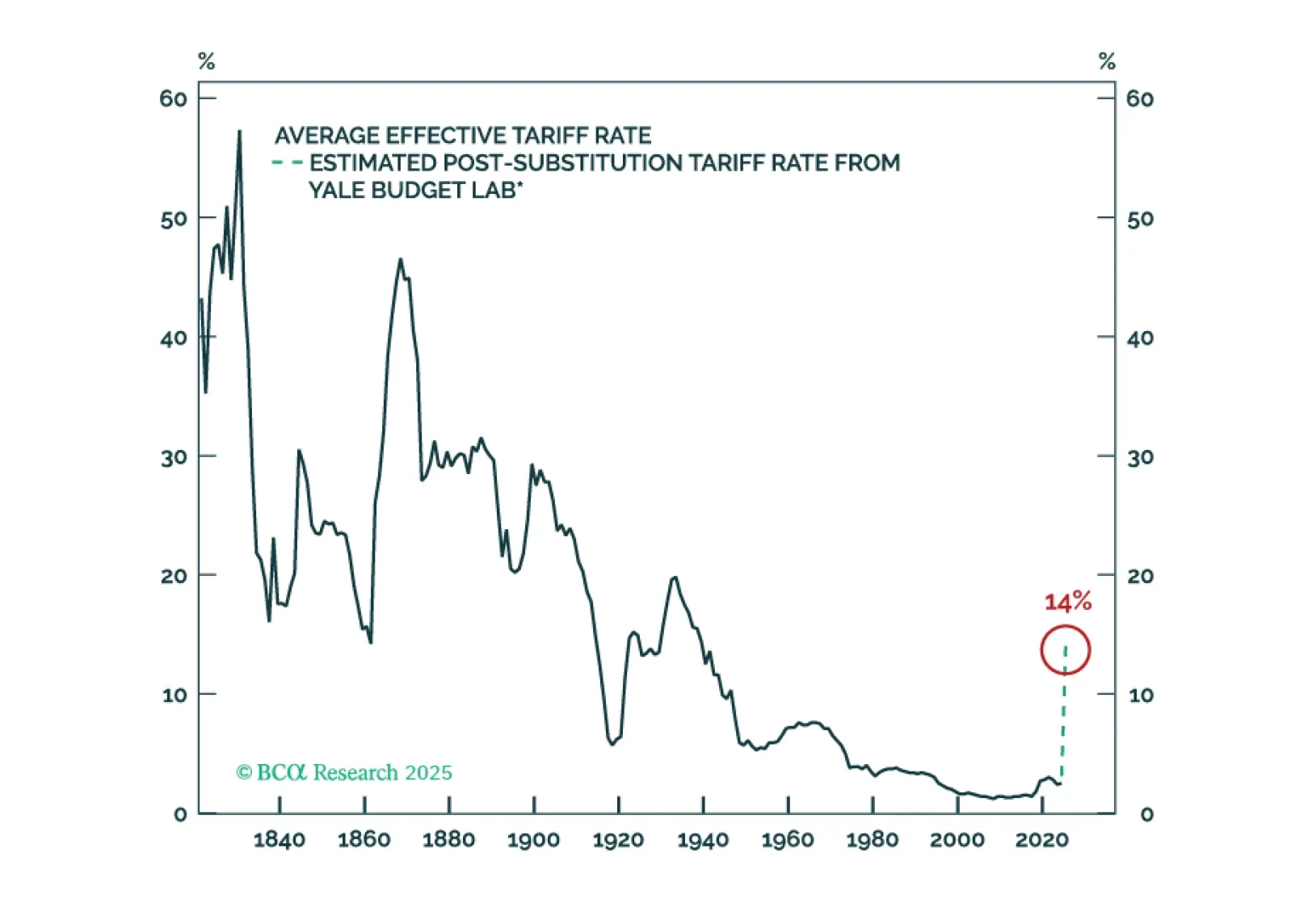

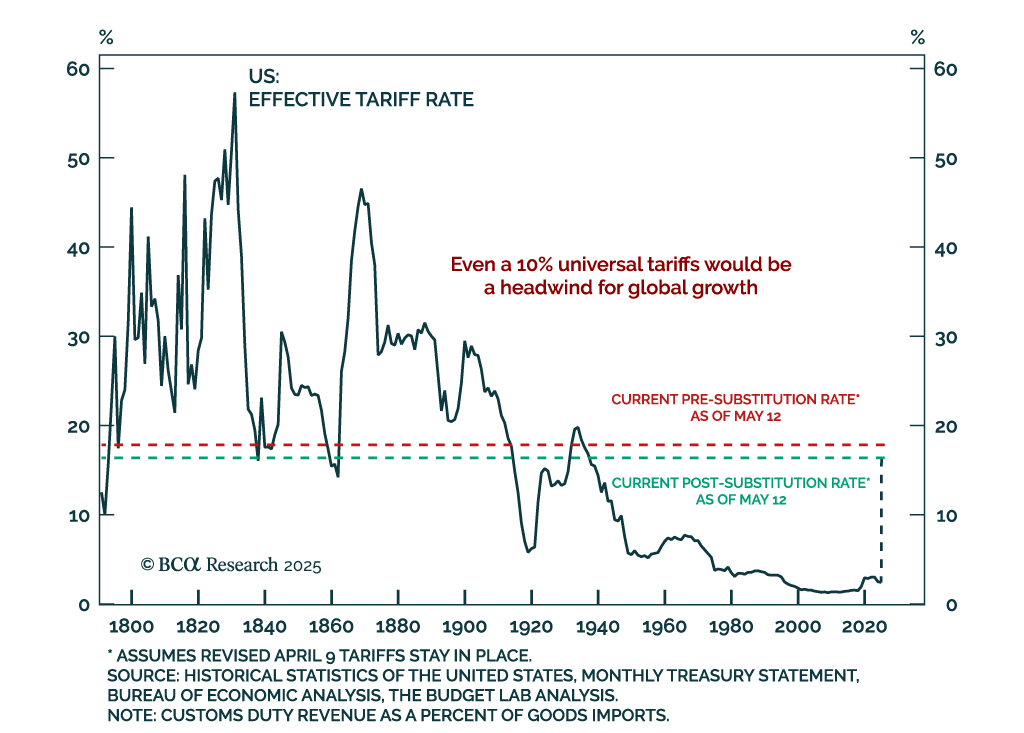

The US-China trade truce triggered a market rally, but tight policy, lingering inflation risks, and tariff-related drag still support a defensive stance. Risk assets and the USD surged on Monday following the de-escalation announcement, while safe havens…

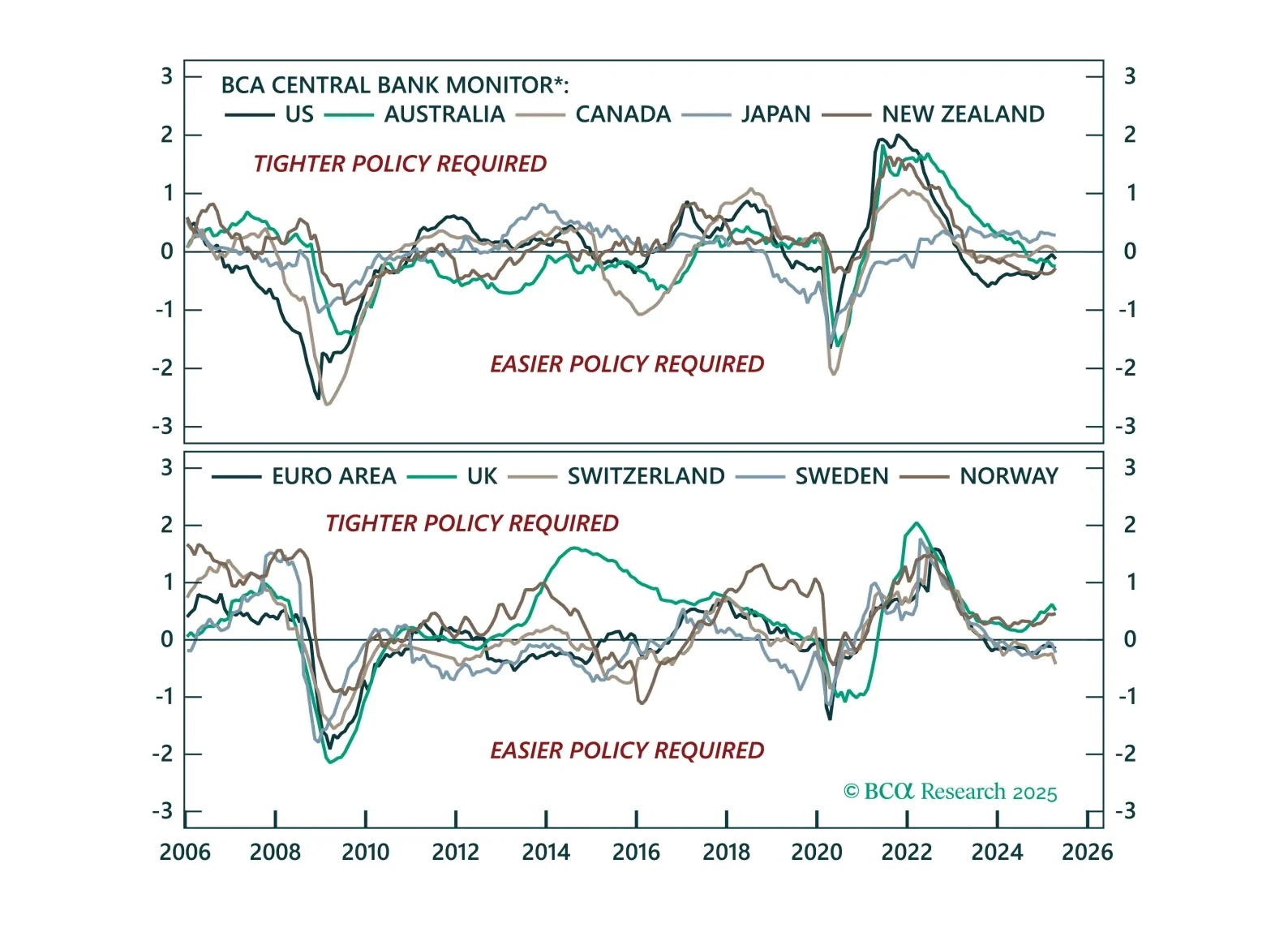

The easing bias remains, but not all central banks are equal. This Central Bank Monitor update reveals who is ready to cut more and who is still pretending not to.

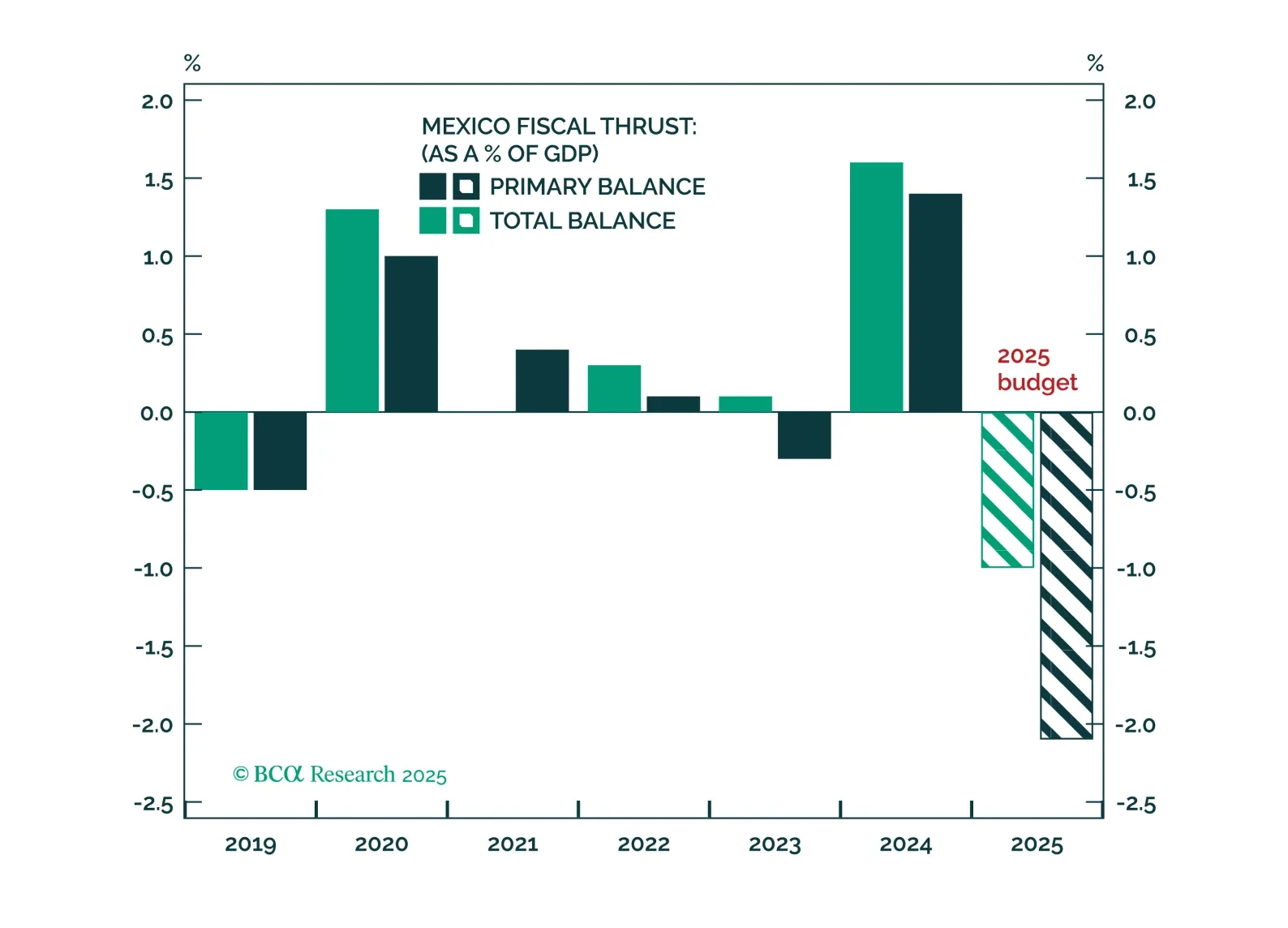

Short-term pain from Trump-related concessions, fiscal tightening amid a US and Mexican slowdown, and rising labor slack will weigh further on Mexican assets. But long-run, policy direction will capitalize on the nearshoring trend and resume the trend of Mexican asset outperformance relative to other emerging markets.

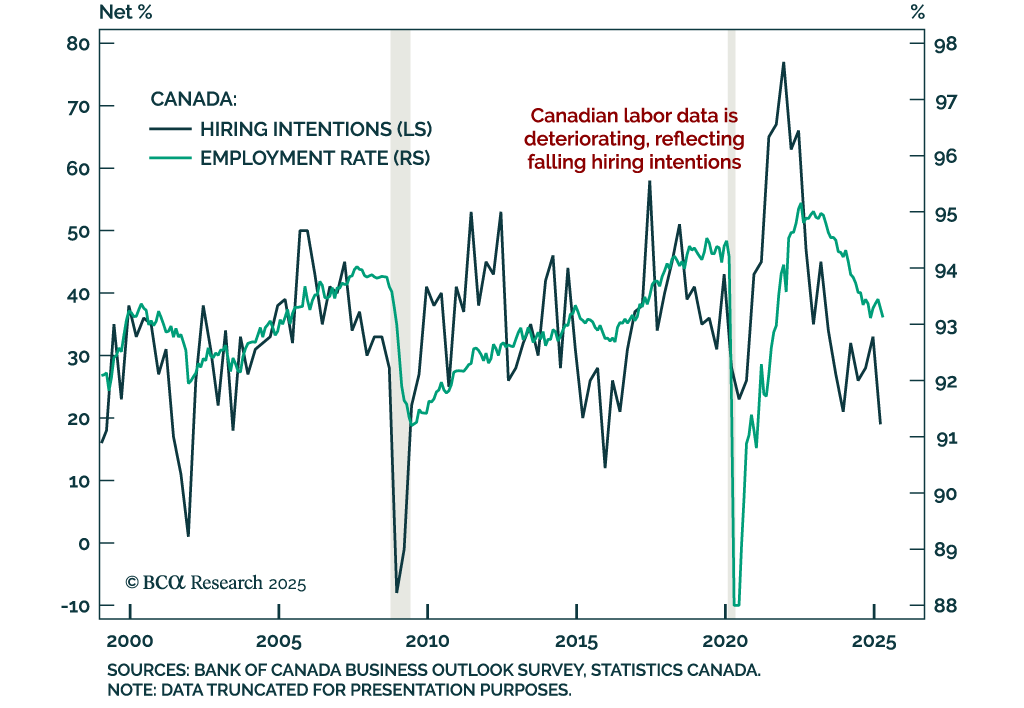

Soft April jobs confirm the Canadian labor market stall, yet we remain neutral on CGBs and structurally bullish on the CAD. The unemployment rate rose more than expected to 6.9% from 6.7%. Employment growth exceeded expectations but remains soft at 7.4k after…

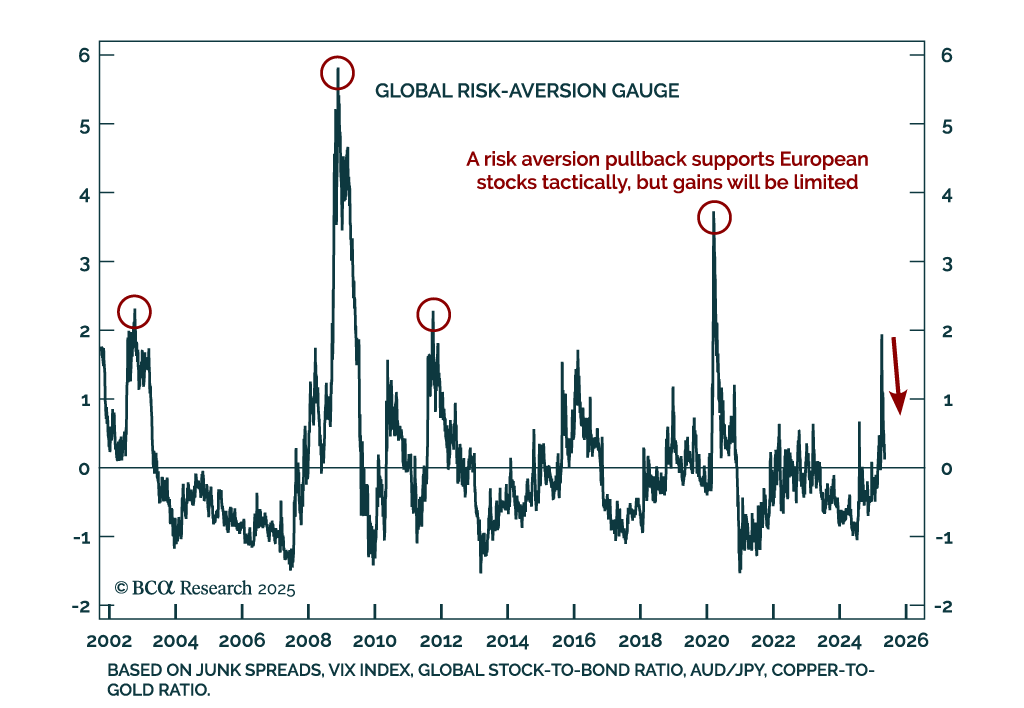

European equities have some short-term support, but global growth risks will cap gains. Our Chart Of The Week comes from Mathieu Savary, Chief European Investment Strategist. Mathieu sees probable but limited upside for European equities in the near term. His…