Economy

US Treasuries typically outperform both equities and global government bonds during downturns. Recent political shifts could lessen that outperformance this cycle, but we doubt it will disappear completely.

Do not play the bounce in US and global cyclical assets as Trump backpedals from the trade war. China will talk, but the pace will be slow and the outcome disappointing. Fiscal stimulus will surprise marginally in the EU, China, and even the US, but still may not rescue the business cycle.

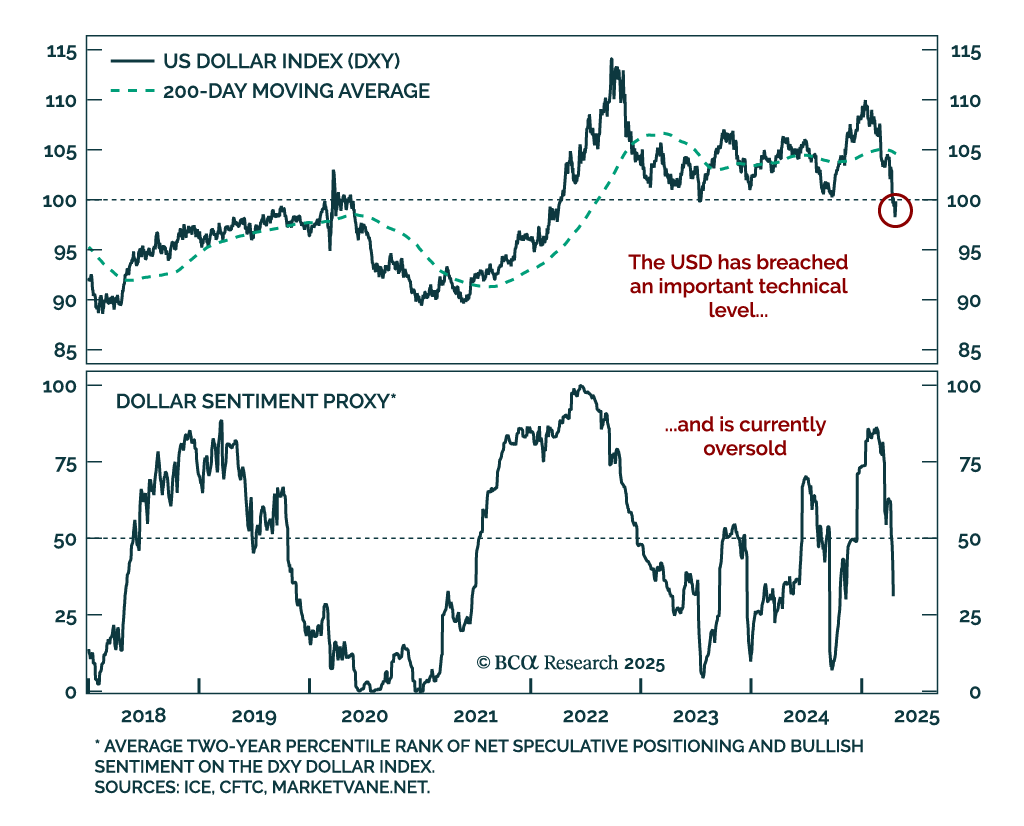

Although the sell-off in the US dollar and relative outperformance of non-US stocks will pause over the coming months as a global recession begins, the fading of US exceptionalism will still cause the dollar to weaken and US stocks to underperform over a multi-year horizon.

This report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who visited our office to discuss the rapidly evolving economic outlook. The US and global economies are likely to enter a recession this year barring a decisive tariff reversal or the passage of significant fiscal stimulus. Even the latter is not clearly bullish for stocks, as it risks a stagflationary outcome. Investors should be underweight stocks versus bonds and should respond to clear signs of stagflation by lowering fixed-income portfolio duration. We continue to recommend defensive equity sector positioning, an overweight stance toward value stocks, an underweight stance toward small caps, and gold over cyclically sensitive commodities.