Economy

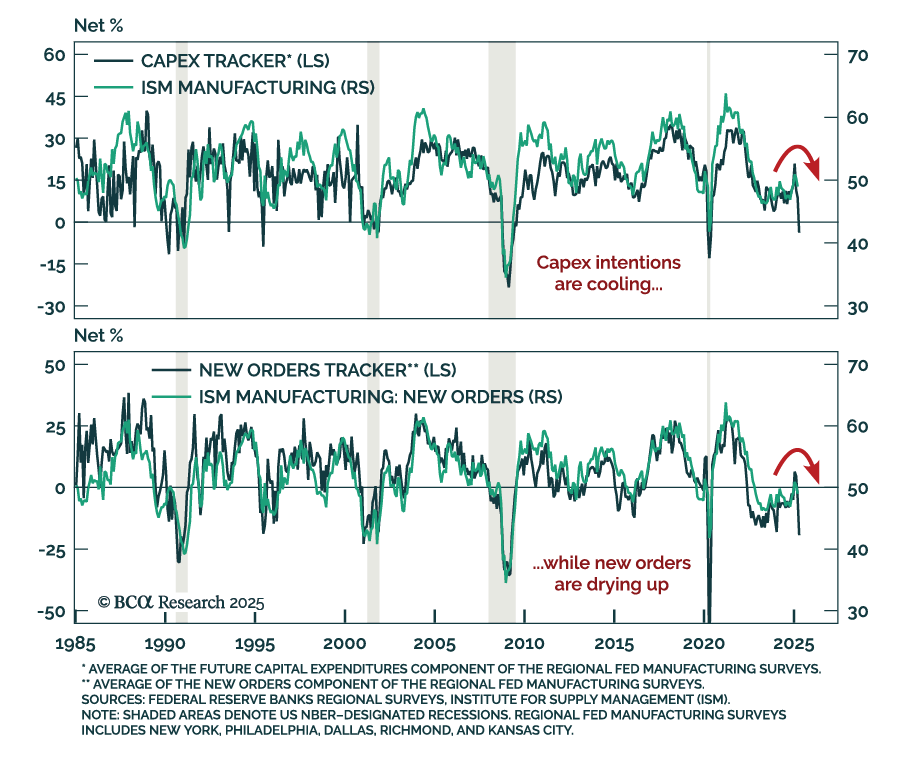

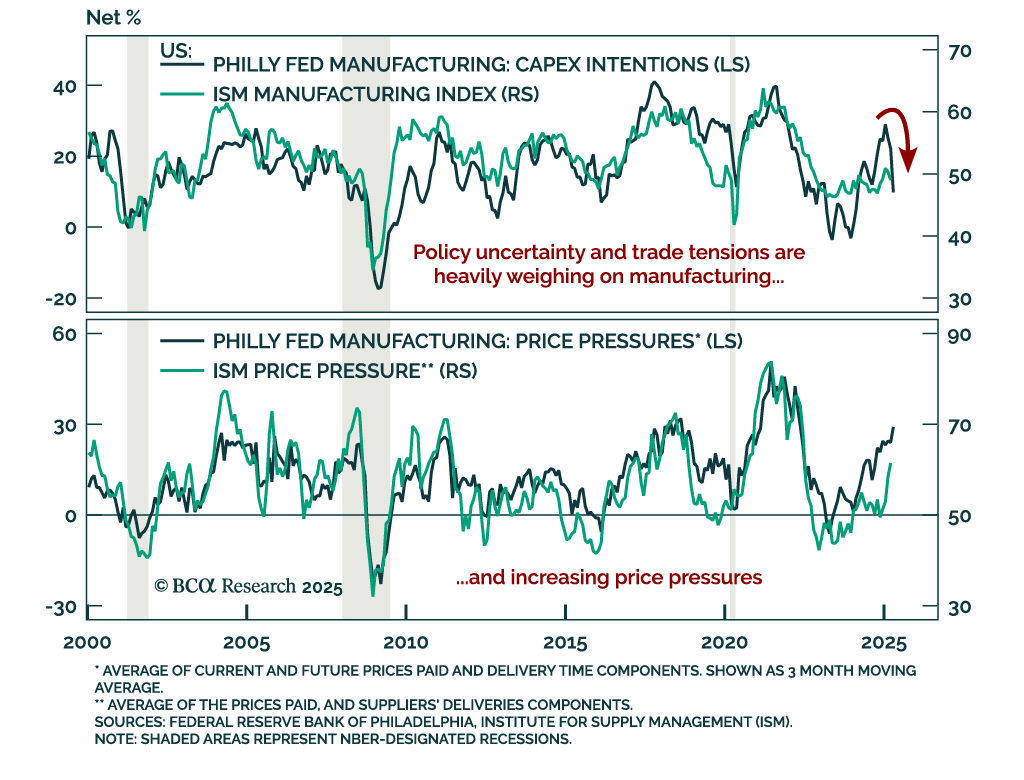

Advanced US indicators for April continue to deteriorate, reinforcing our defensive positioning as recession risks remain underpriced. After weak Empire and Philly Fed manufacturing prints, the Philly Fed services survey shows the slowdown is spreading beyond…

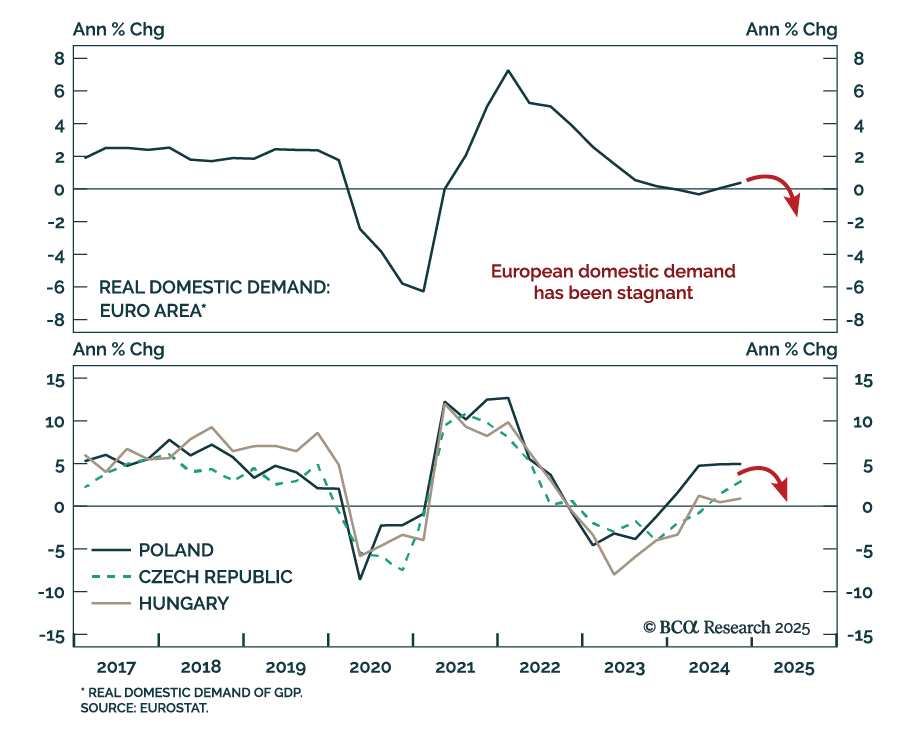

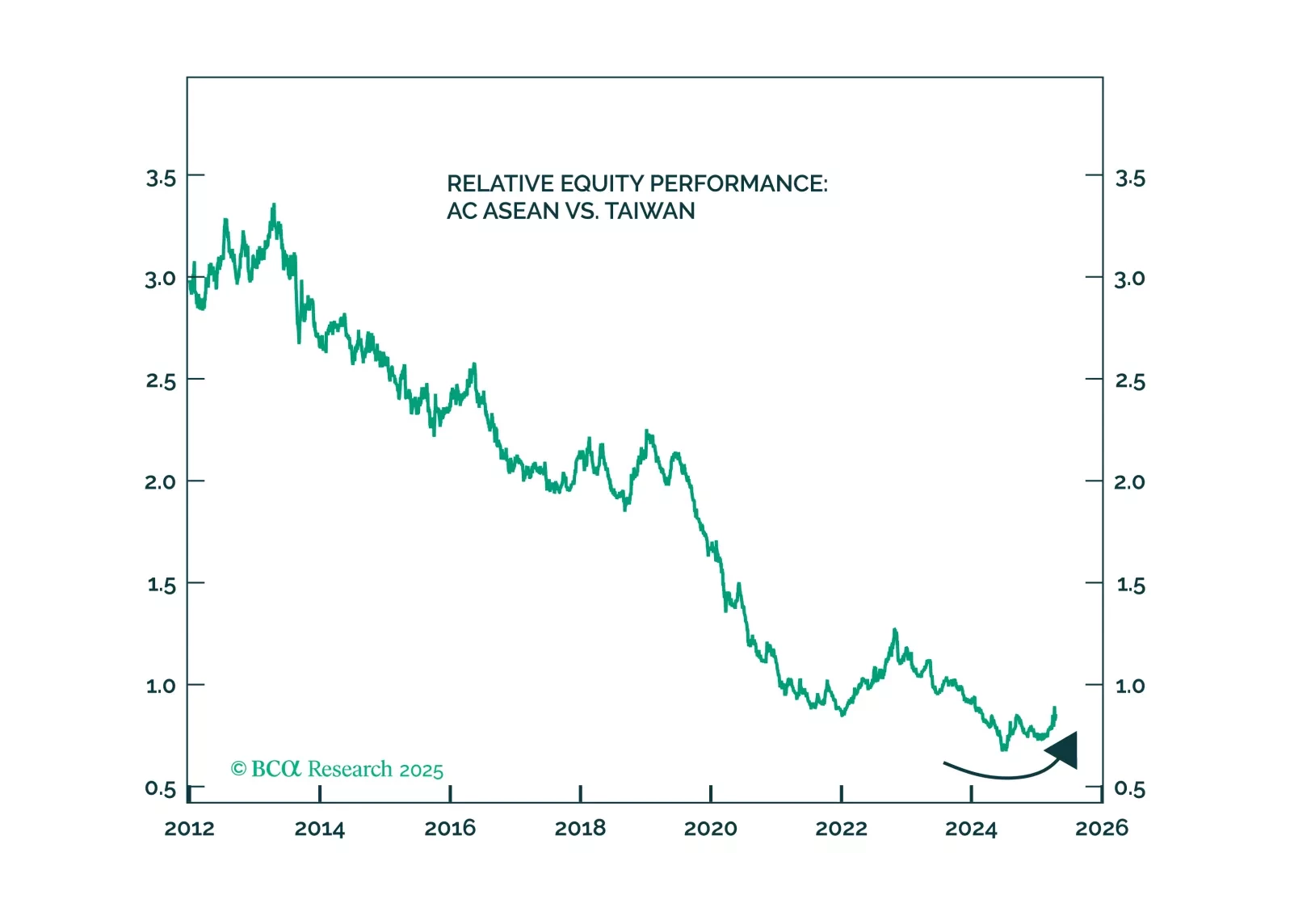

Our EM strategists recommend upgrading CE3 assets within EM portfolios, as a structural shift in the global currency regime is underway. They expect the greenback to depreciate against the euro amid a global downturn, supporting Central European currencies,…

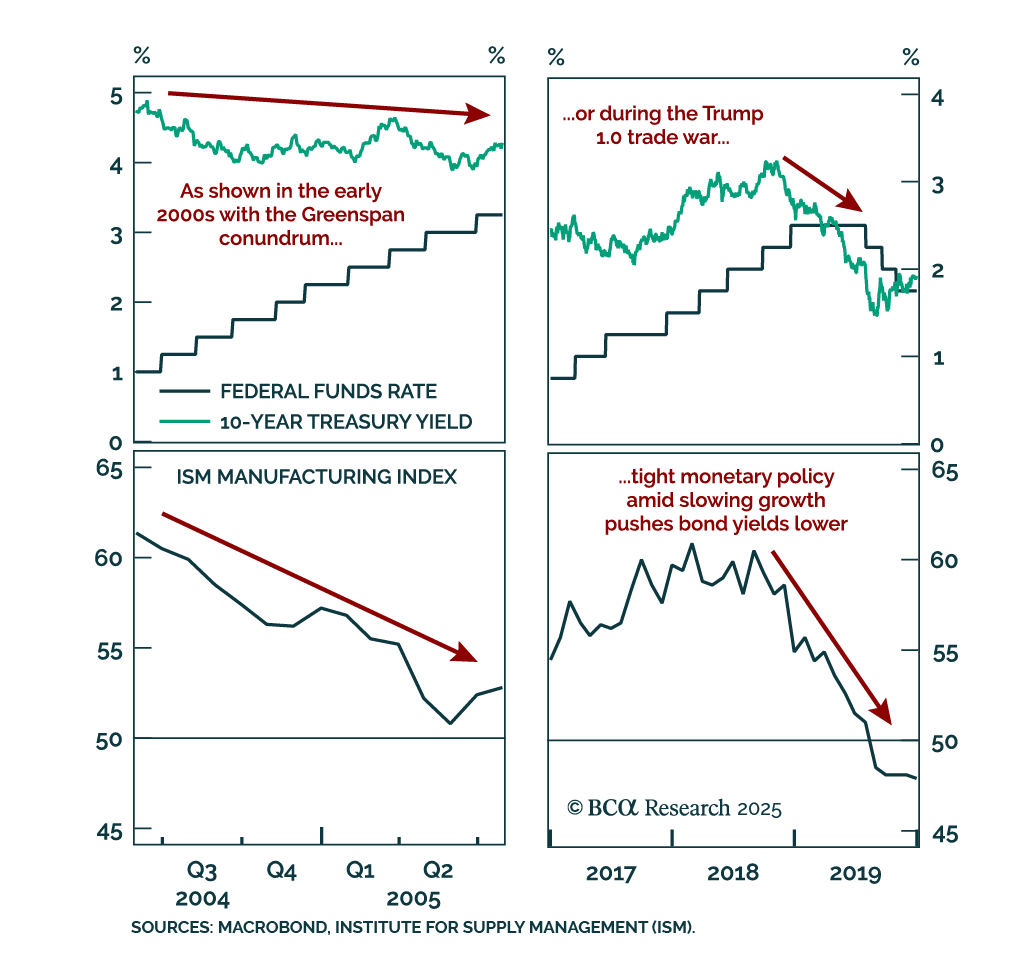

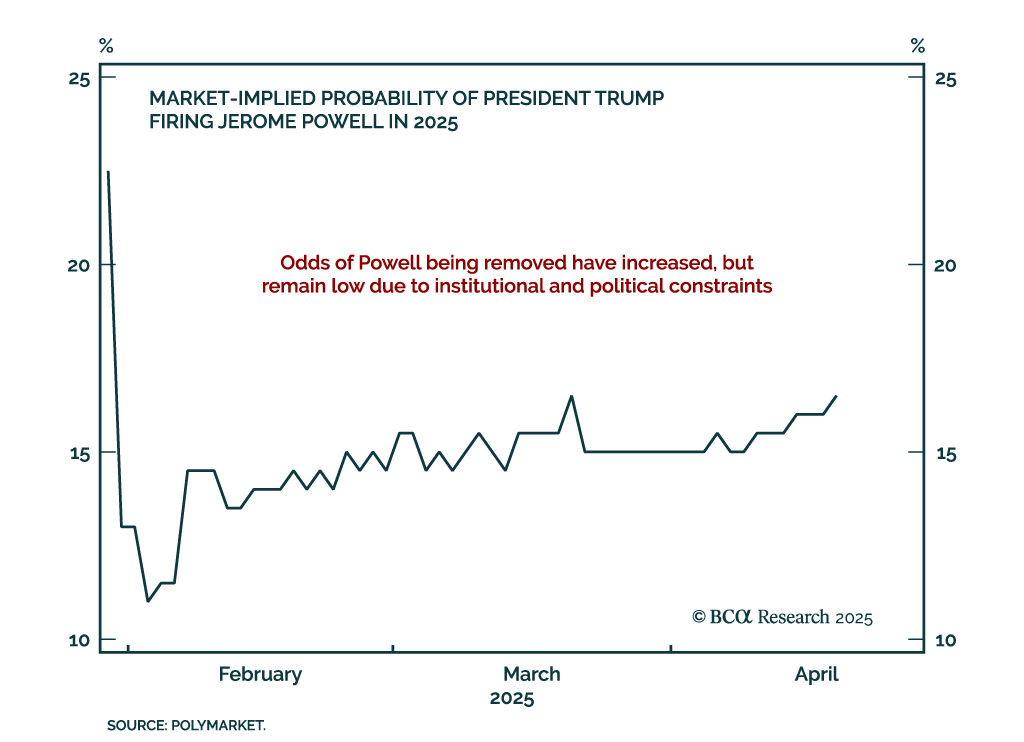

President Trump's pressure on Fed Chairman Powell is intensifying, but keeping Powell in place offers the administration political cover while keeping bond yields contained. Removing Powell would be legally difficult and risk unsettling markets, while his…

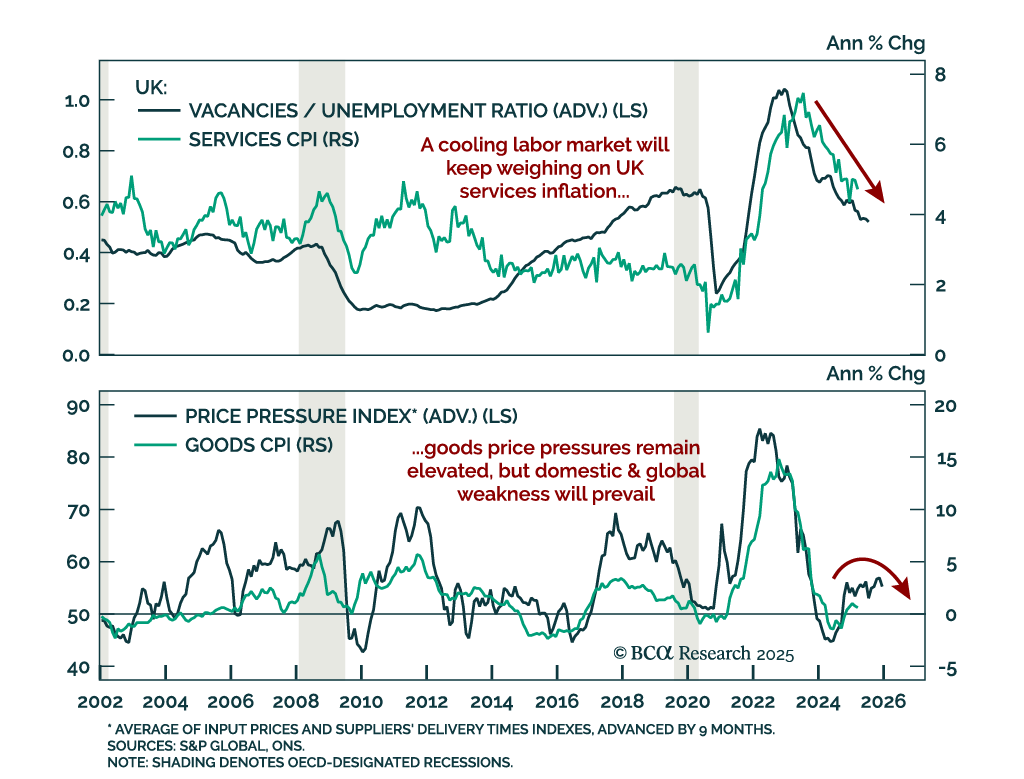

The latest UK data supports a May BoE cut, reinforcing our overweight in Gilts as growth headwinds build and inflation cools. Employment declined by 78k in March, accelerating from February’s downwardly revised 8k drop, while vacancies fell below pre-COVID…

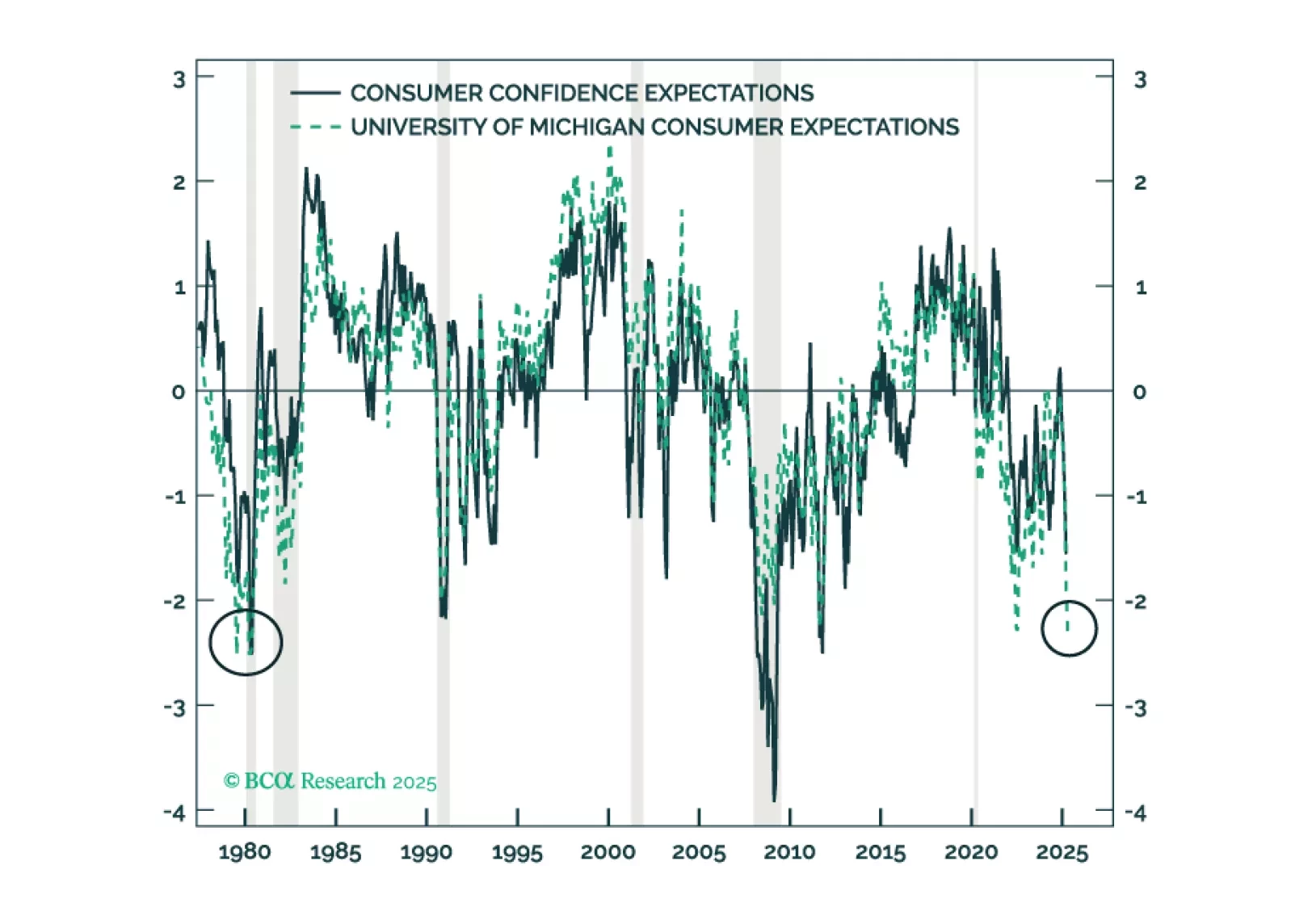

The policy-induced decline in consumer confidence has spread to businesses and investors, increasing the probability of a recession even if the administration reverses field on its aggressive tariff measures. We reiterate our defensive asset allocation recommendations.

Upgrade the odds of a full-scale war in the Taiwan Strait from 5% to 10%. Rapid escalation of US-China economic war raises the probability of tensions spilling into the military-strategic domain. Investors should buy insurance against this tail risk while it is cheap. Meanwhile, use this year’s trade shock and equity volatility to increase allocation to EM manufacturing states.

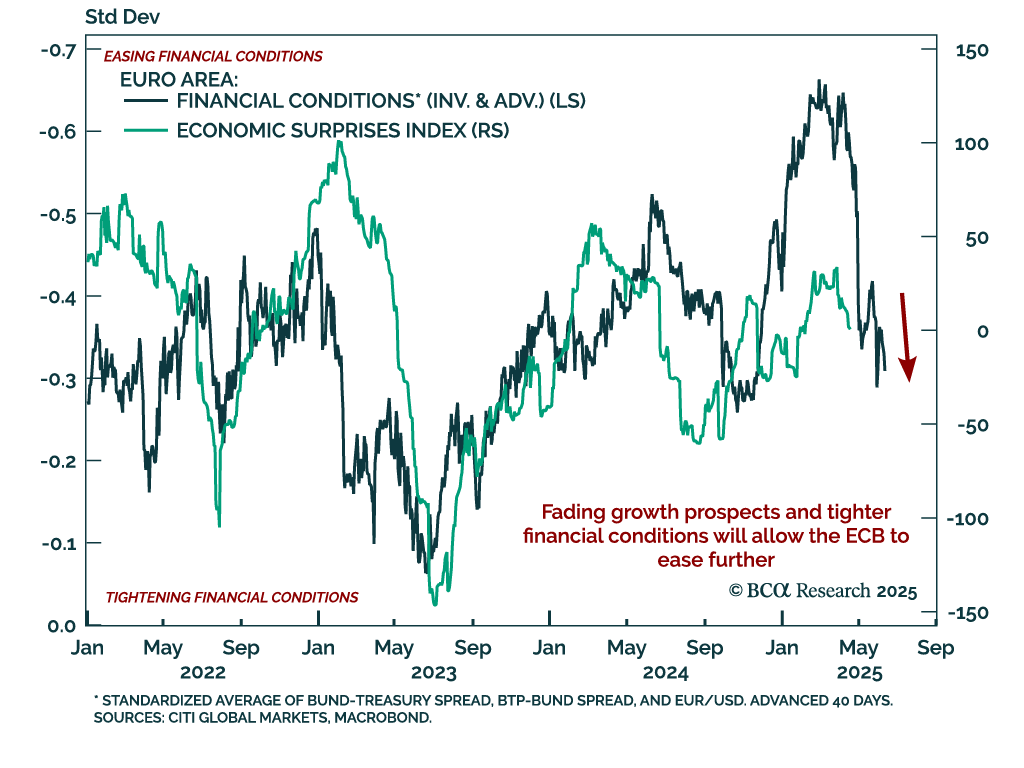

The ECB’s latest 25 bps cut and President Lagarde's notably dovish tone amid rising trade uncertainty reinforce our long December 2025 ESTR futures versus SOFR position. The deposit facility rate now stands at 2.25%, and Lagarde reiterated the disinflationary…

April’s Philadelphia Fed survey adds to recent stagflationary signals, reinforcing our defensive commodities positioning. The headline index collapsed to -26.4 from 12.5 in March, missing expectations and confirming the April deterioration seen in the Empire…

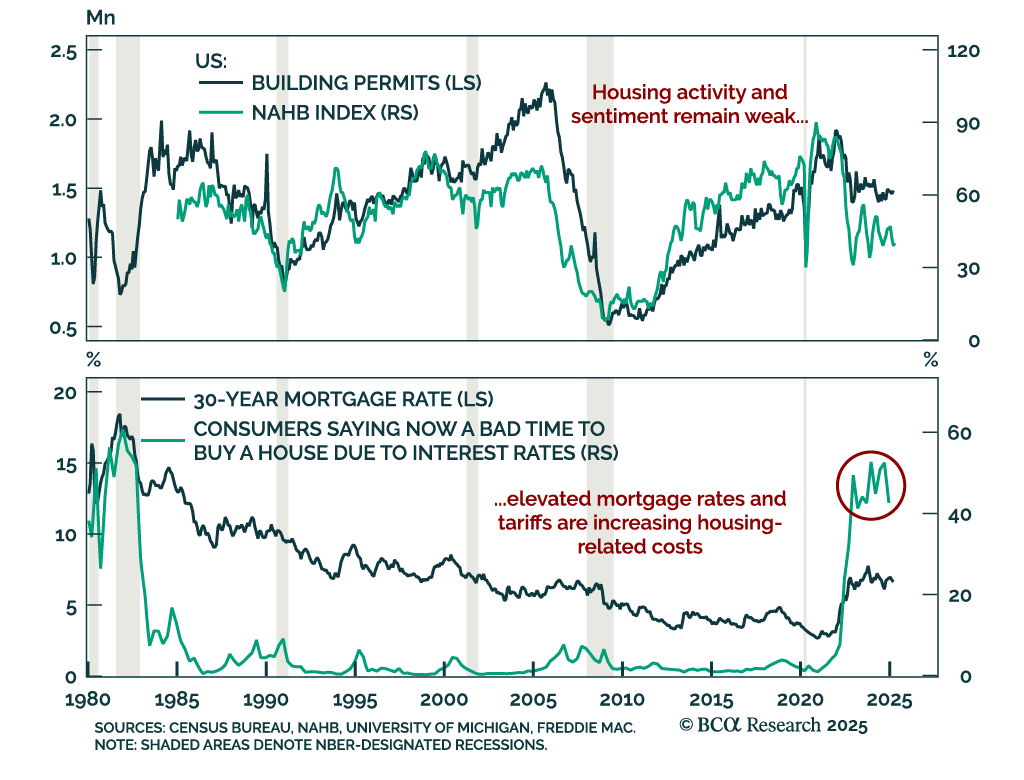

Weak housing data reinforces our defensive positioning, as recession odds remain underpriced in risk assets. US housing starts fell sharply, declining a larger-than-expected annualized rate of 11.4% in March after a 9.8% rebound in February, which was driven…

Trump’s renewed attacks on Fed Chairman Jerome Powell raise policy uncertainty but are unlikely to lead to Powell’s removal, reinforcing our expectation for continued restrictive policy and supporting our long duration stance. Trump's intensified criticism…