Economy

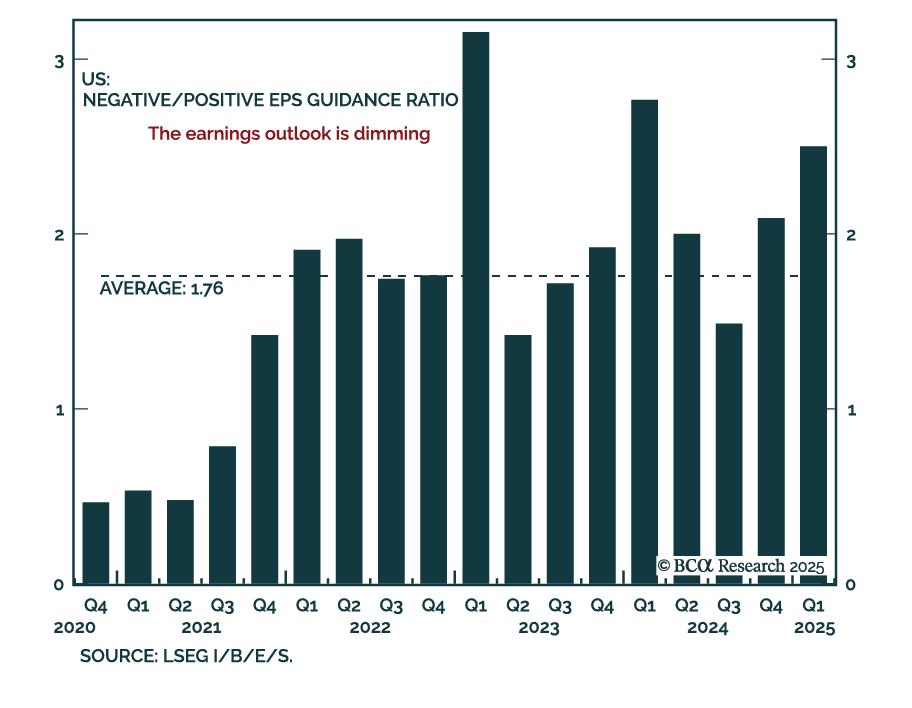

Our US Equity strategists assessed what companies are saying about tariffs, the US dollar, and the US consumer during their latest earnings calls. Q4 earnings were strong, with earnings and sales growth exceeding expectations. However, 2025 earnings…

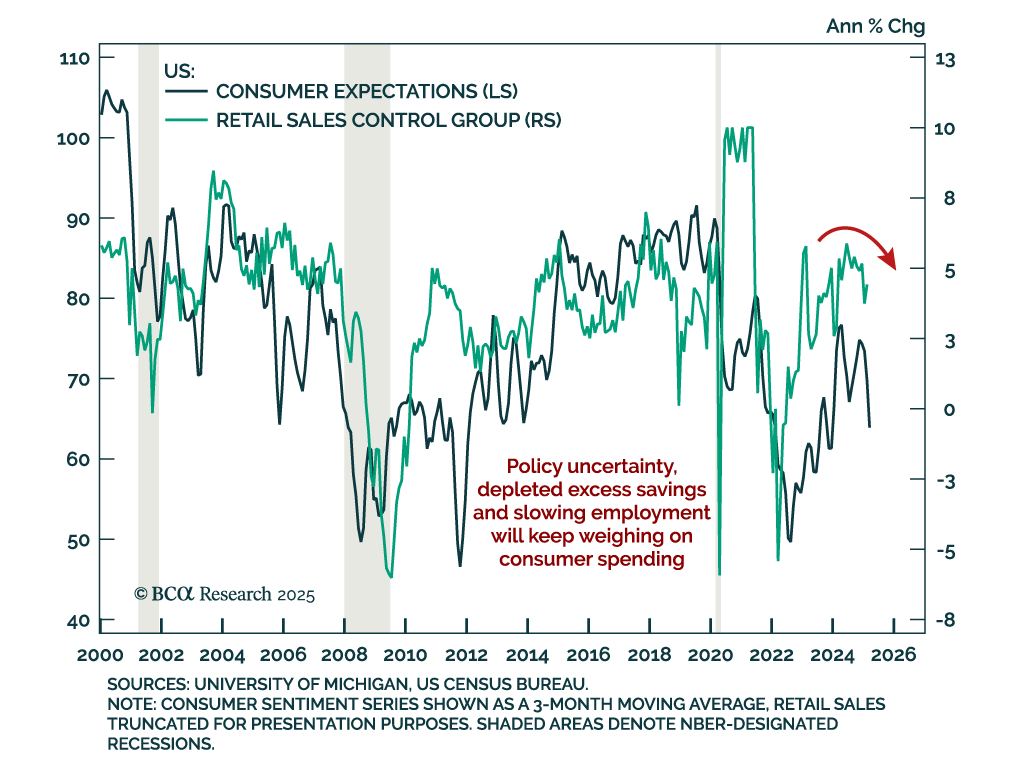

February US retail sales were mixed, with the headline number missing expectations at only 0.2% m/m. January’s reading was revised down to -1.2%. Core measures (excluding gas & autos) were roughly in line with estimates, but the control group saw a 1.0%…

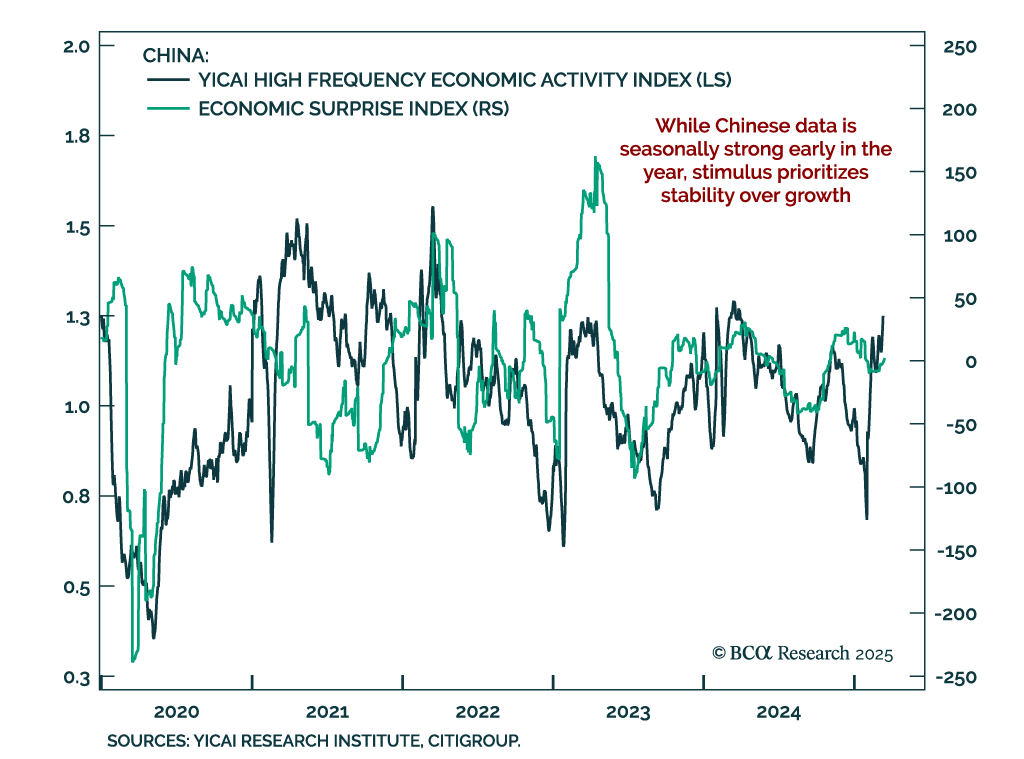

Outside of the real estate sector, Chinese activity was decent in January and February. Both industrial production and retail sales were slightly stronger than expected. The jobless rate ticked up to 5.4% while property investment was down -9.8%…

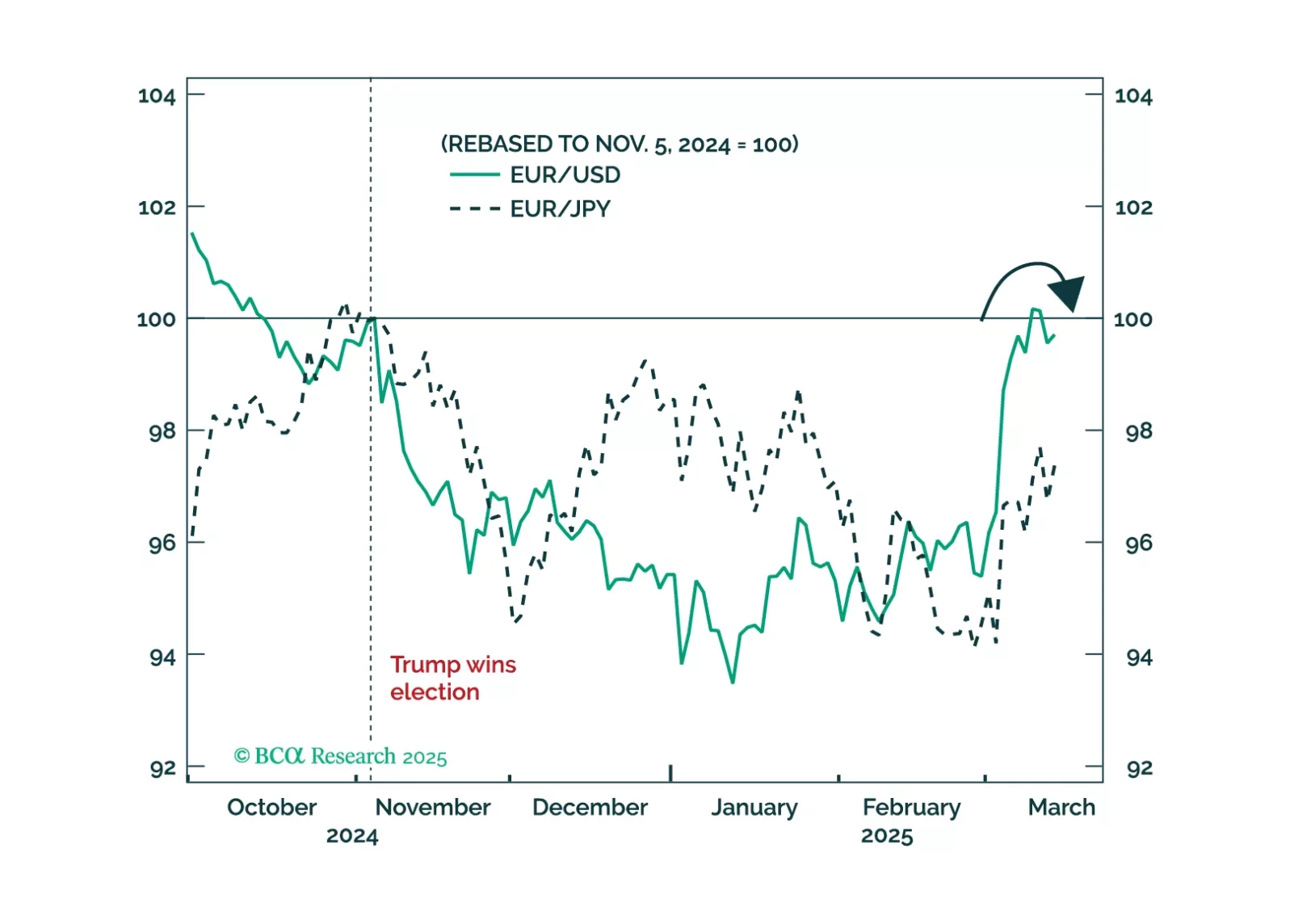

Trump’s foreign policy can be explained by rational US interests, but it requires settling the trade war with allies sooner rather than later. Book gains on EUR-USD for now.

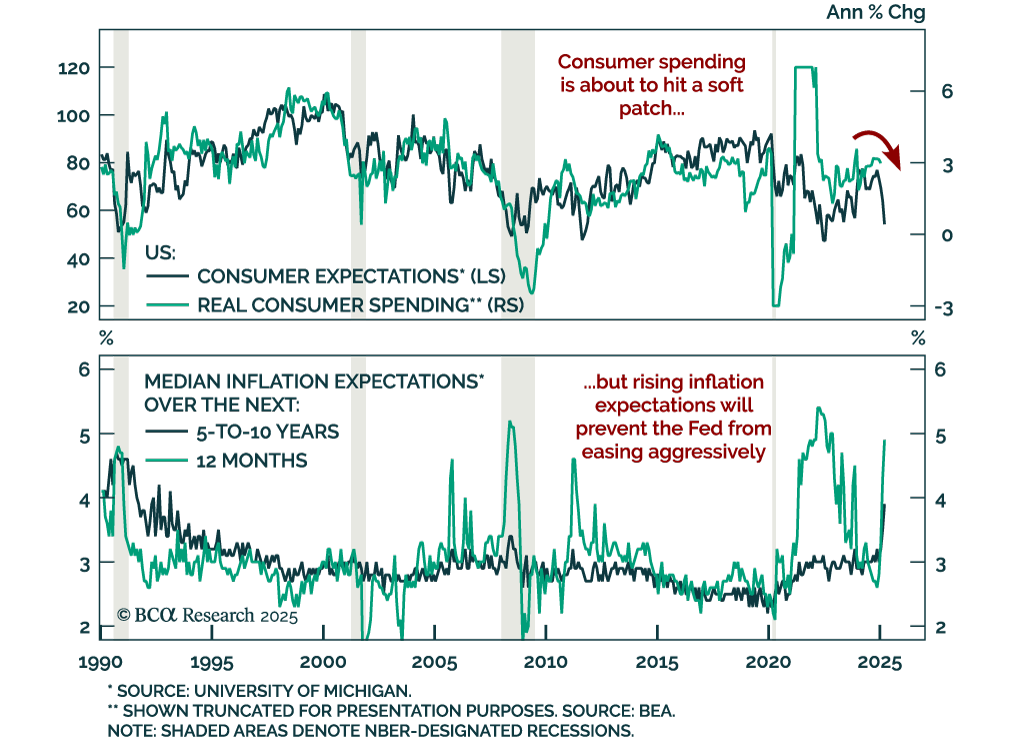

The preliminary March University of Michigan Consumer Sentiment Index missed estimates, falling to 57.9 from 64.7. The decrease came from both the assessment of current conditions and expectations, with the latter falling almost 10 points. Measures of 1-year…

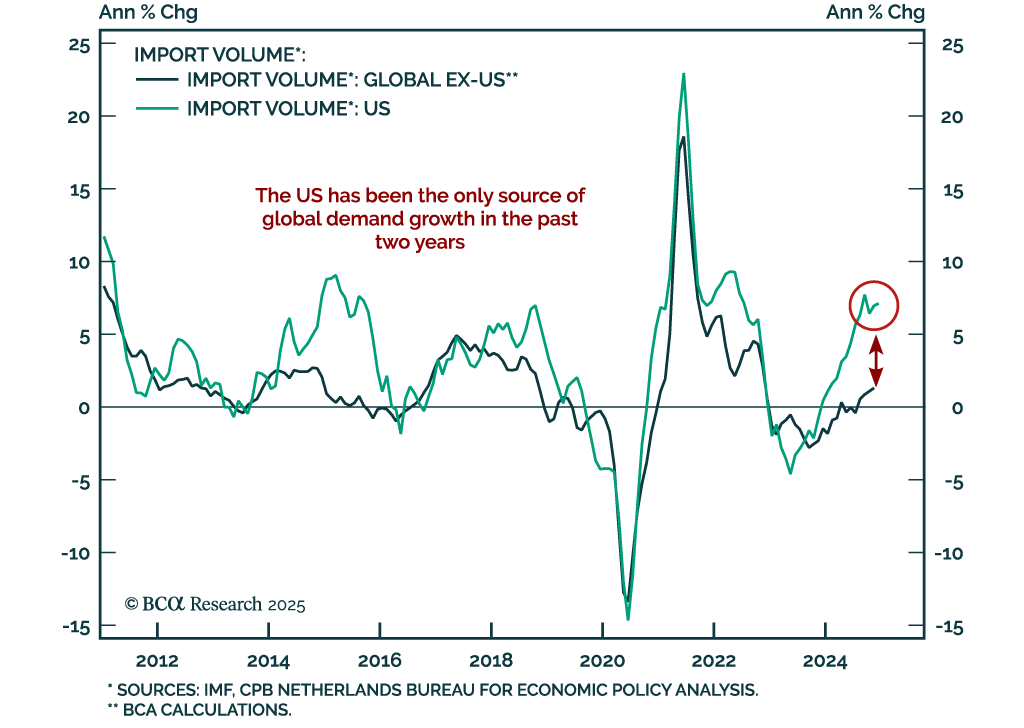

Our Chart Of The Week comes from Arthur Budaghyan, Chief Emerging Markets/China strategist. Arthur highlights a key risk for the global economy, and its implication for the US dollar. By and large, the US economy has been the only source of global…

Despite our Global Investment strategists’ bearish stance, their latest report reviews scenarios that could be bullish for equities. Our colleagues remain bearish on equities, expecting a US recession this year. However, several upside scenarios could…

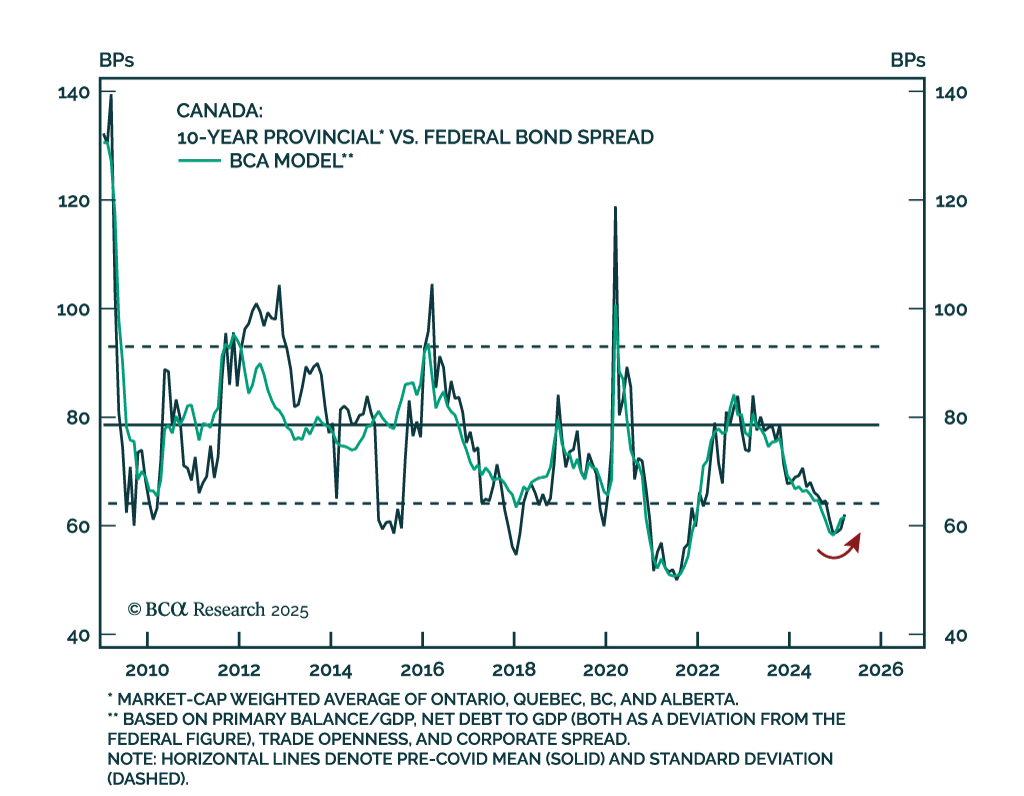

Our Global Fixed Income team wrote a primer on the Canadian provincial bond market, an overlooked yet substantial market. Canadian provincial bonds are a major segment of the country's fixed income market, with spreads primarily driven by fiscal…

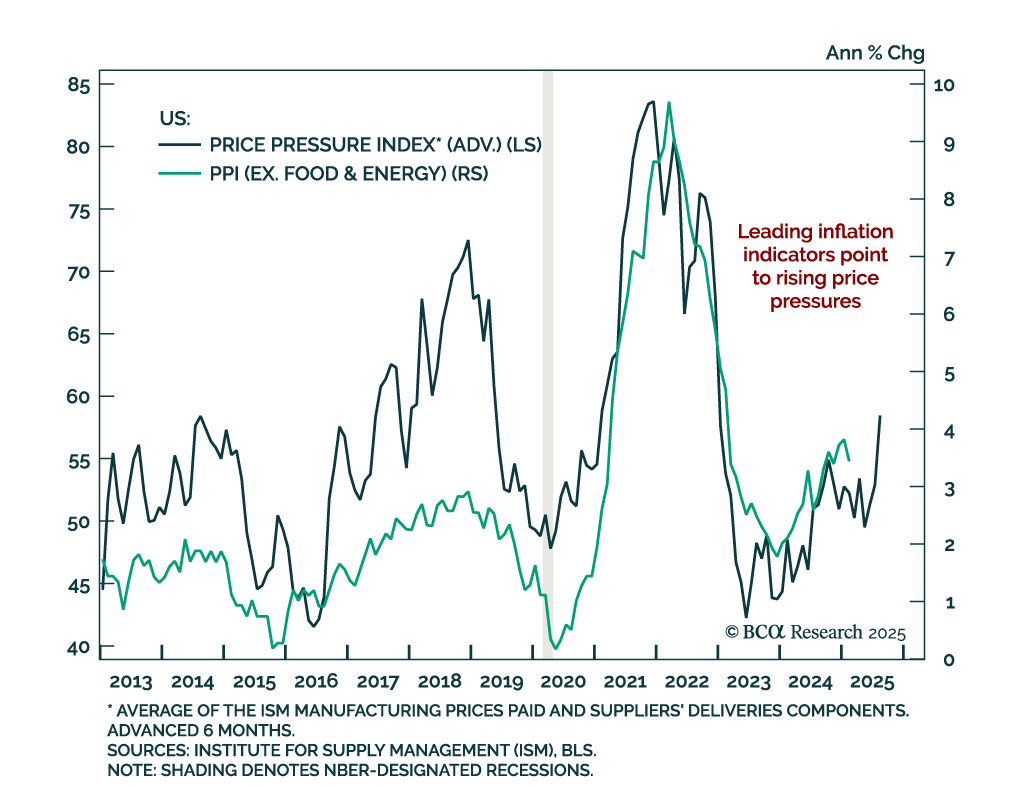

The February US Producer Price Index came in below estimates, with the headline measure showing no monthly change and standing at 3.2% y/y. Core PPI (excluding food, energy, and trade services) was also cooler than expected, coming in at 0.2% m/m (3.3%…

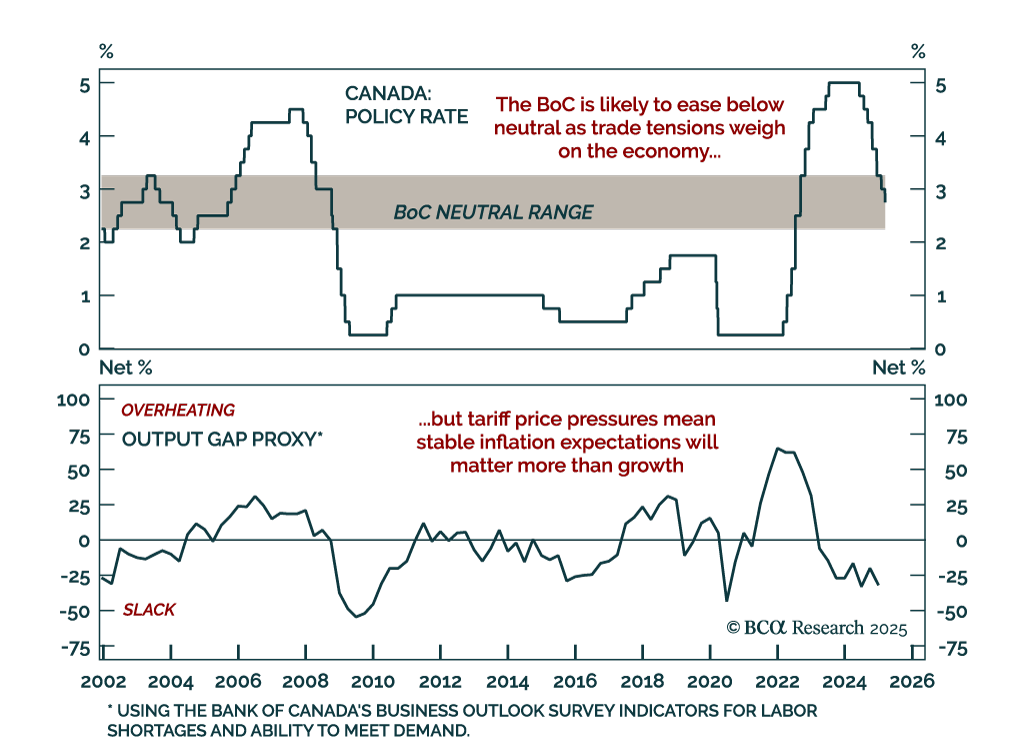

The Bank of Canada cut by 25 bps to 2.75% as expected. This seventh consecutive cut brings the policy rate further into neutral territory, estimated to be in the 2.25%-to-3.25% range. The BoC is in a tough place. The trade war will ultimately be…