Economy

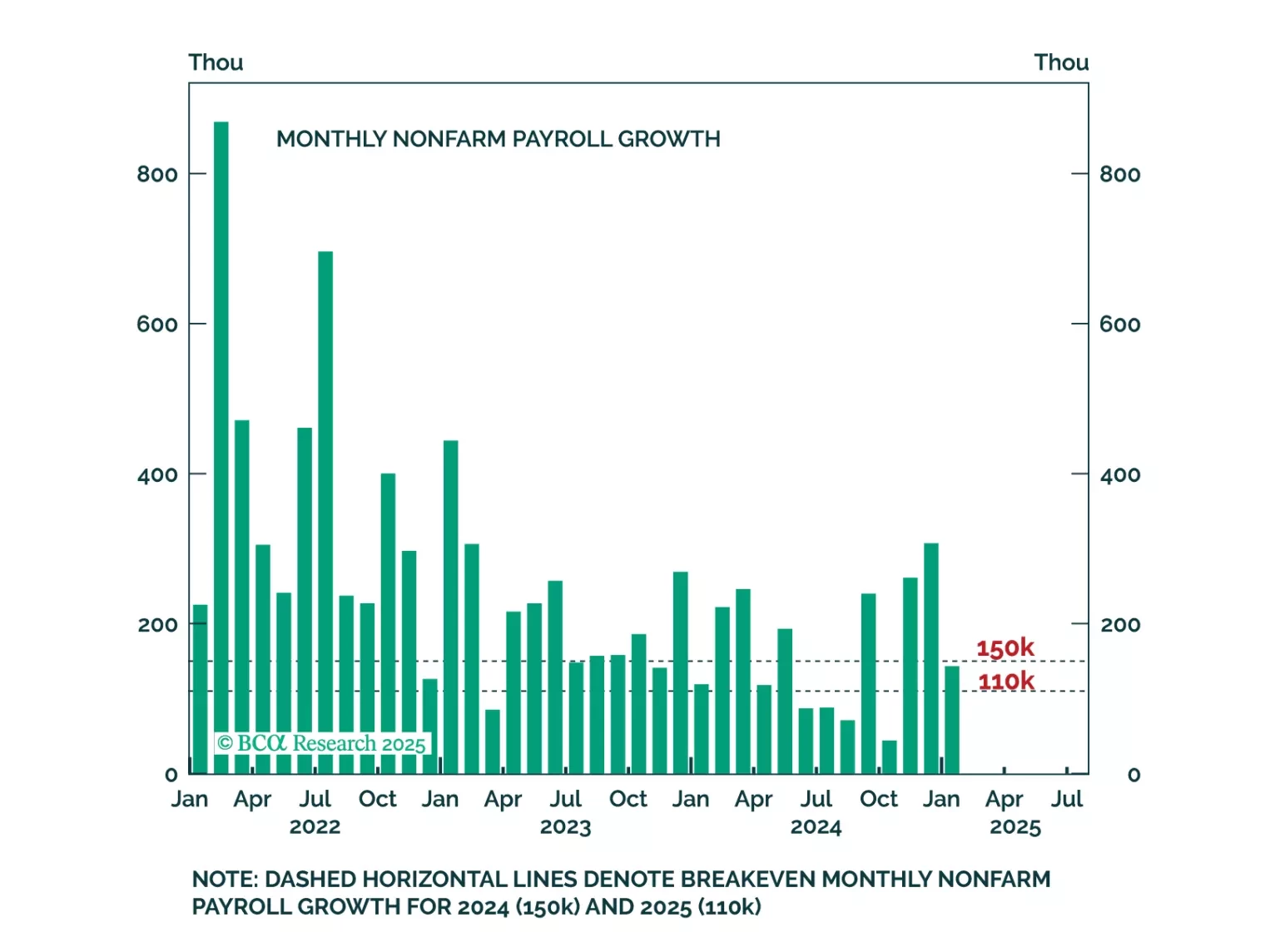

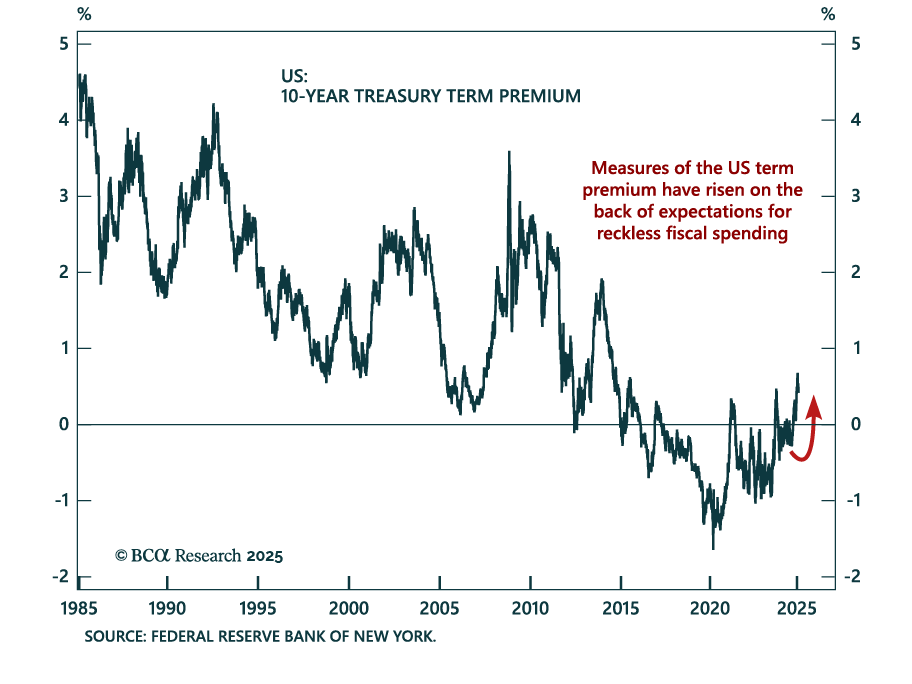

Some thoughts on this morning's employment data and Treasury Secretary Bessent's recent attempts to talk down the 10-year Treasury yield.

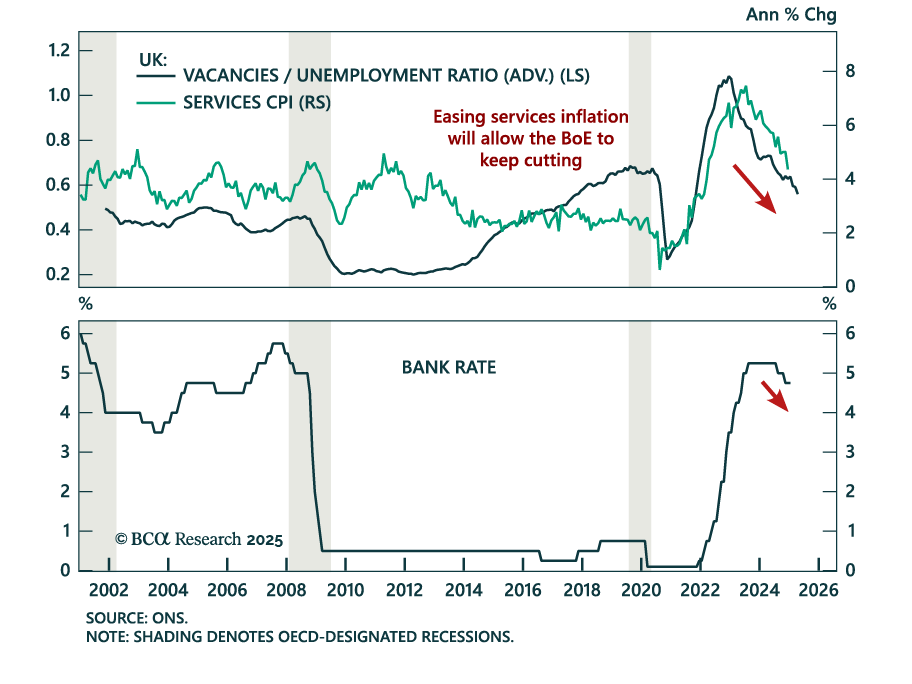

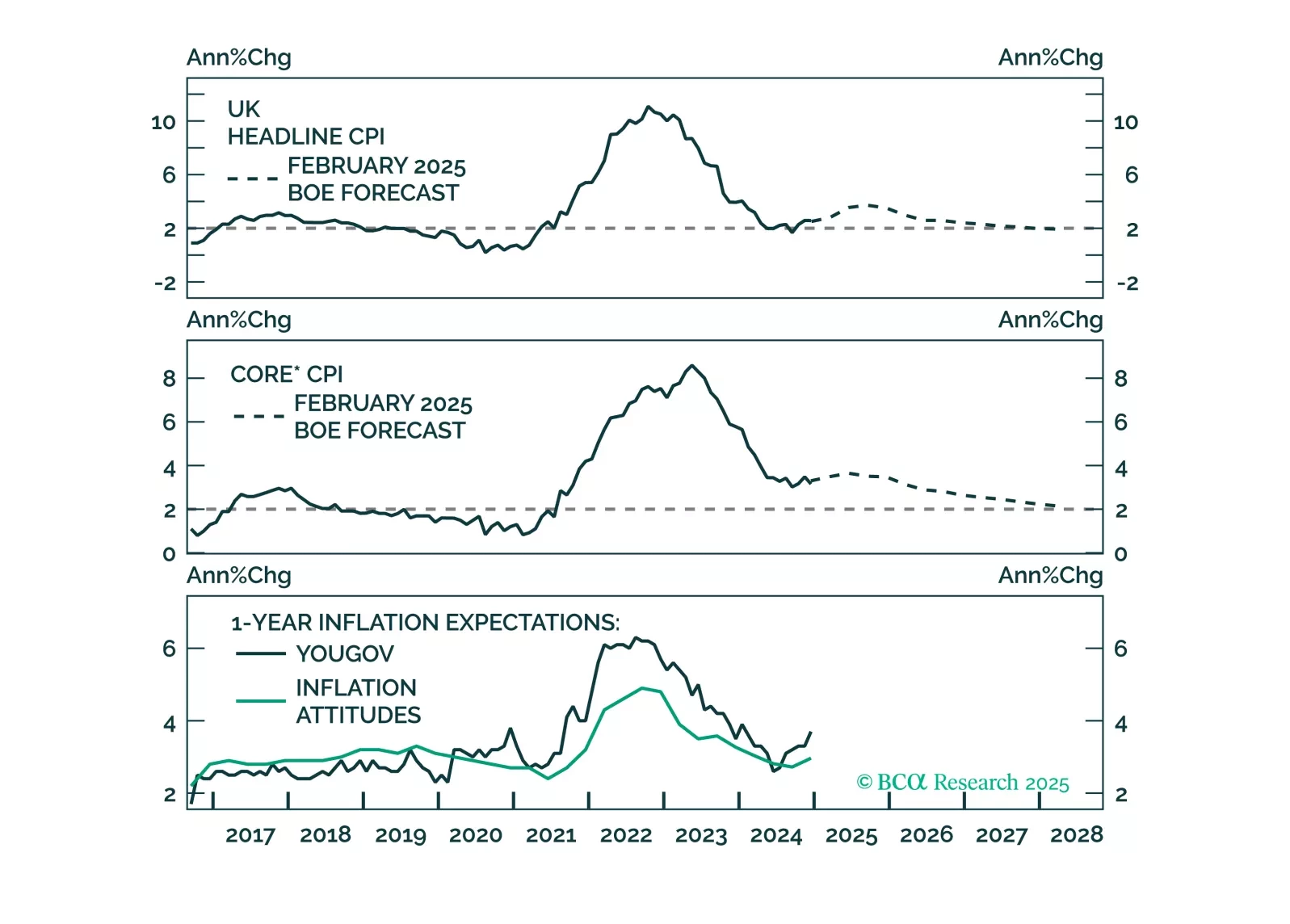

Following today’s Bank of England’s policy meeting, at which the policy rate was cut by 25 bps, we discuss our outlook for monetary policy in the UK. We expect the gradual easing to continue and discuss the investment implications for UK gilts and sterling.

Our Portfolio Allocation Summary for January 2025.

This is a follow-up report on Bessenomics – the policy mix that US Treasury Secretary Scott Bessent plans to pursue. The direction of US and global financial markets depends on the amount of fiscal tightening required to bring down US interest rates. Can the Trump administration cut fiscal spending just enough to bring down US bond yields but not cause a recession?