Economy

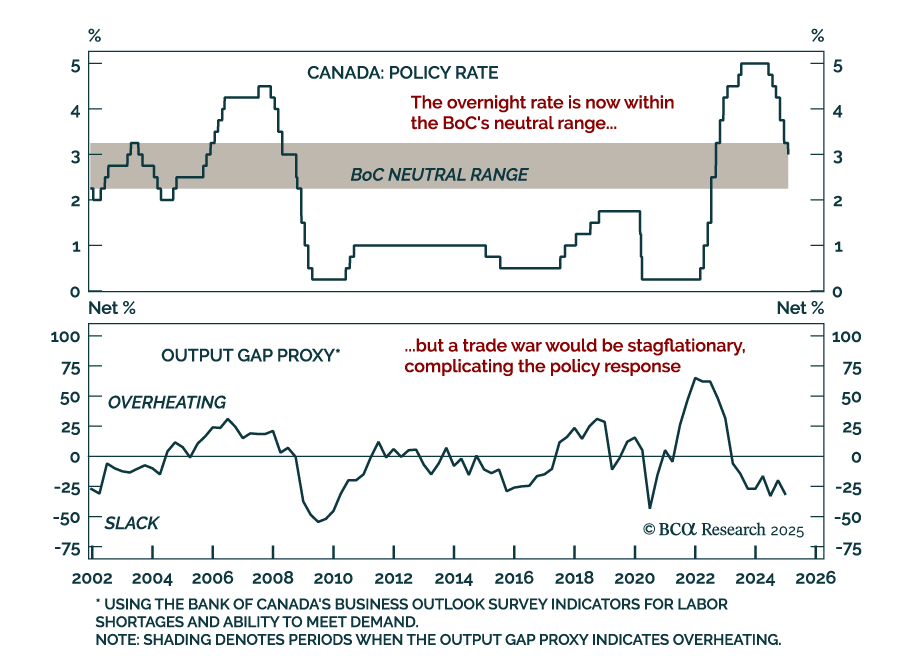

The Bank of Canada cut by 25 bps to 3% as expected, and announced the end of quantitative tightening. This sixth consecutive cut brings the policy rate further into neutral territory, estimated to be in the 2.25%-to-3.25% range. The BoC assessed…

The Federal Reserve kept rates on hold in its 4.25%-to-4.5% range, as expected. The main change in the statement was the removal of the reference to progress towards the Fed’s 2% target, leaving instead a simple mention that inflation “remains somewhat…

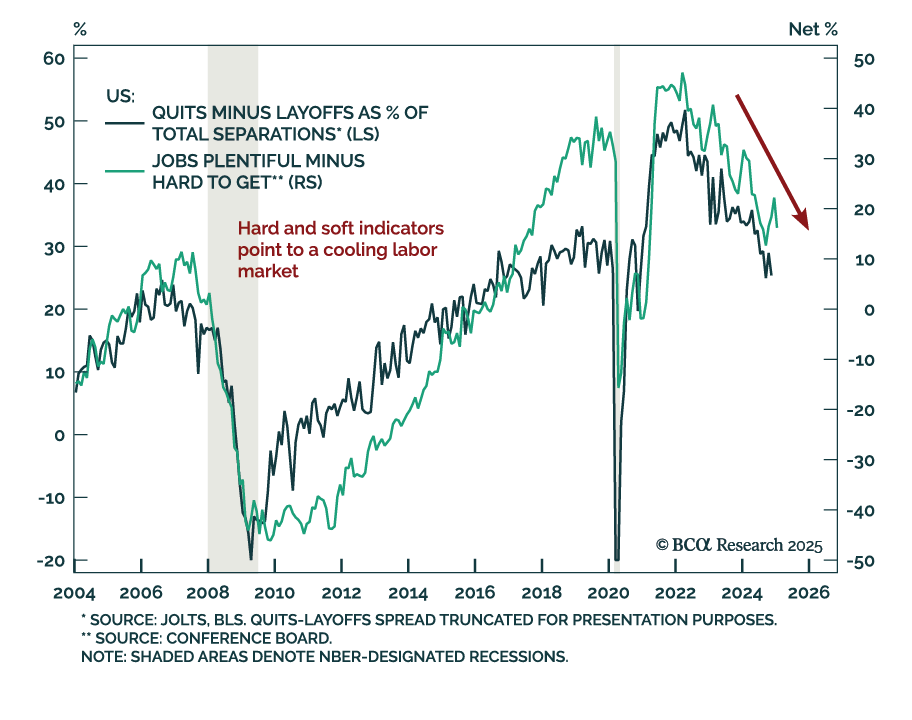

The January Conference Board Consumer Confidence index missed estimates, decreasing to 104.1 from an upwardly-revised 109.5 in December. The decrease was driven by both the present situation and expectations subcomponents. The labor differential, the…

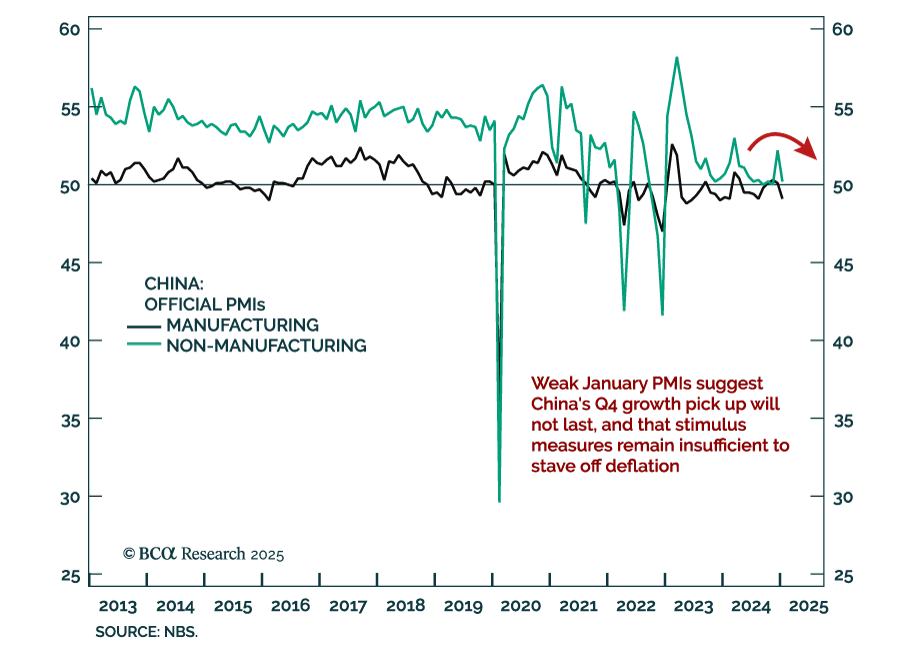

China’s official January PMIs disappointed, with the composite ticking down to 50.1 from 52.2. The decrease was driven by both the manufacturing and non-manufacturing components, with the former indicating contraction, and the latter showing very low…

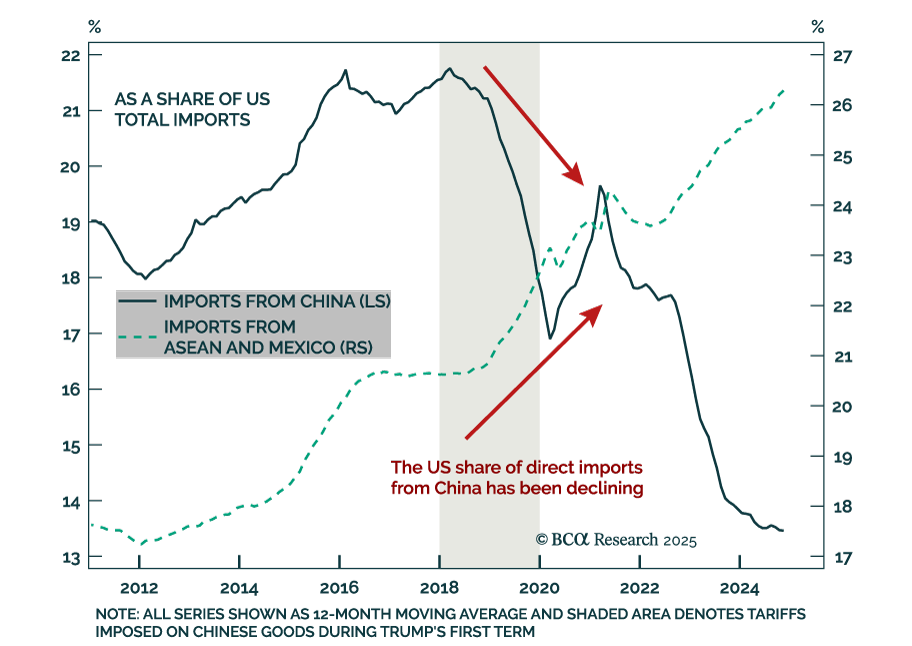

Our China Investment Strategy team explored how the costs of higher tariffs might be distributed among foreign suppliers, US importers, and consumers. The inflationary impact of new US tariffs is likely to remain modest unless President Trump imposes…

The January Ifo Business Climate index for Germany beat estimates, increasing to 85.1 vs. 84.7 in December. The increase came from the survey’s current assessment component, which increased a full point, as the expectations component missed estimates and…

News of a cheaper Chinese-developed AI model sent a tremor through markets, with a selloff in the S&P 500, NASDAQ, and leading tech names associated with AI. The narrative on Monday was that the eye-watering sums spent on AI capex by mega-cap tech…

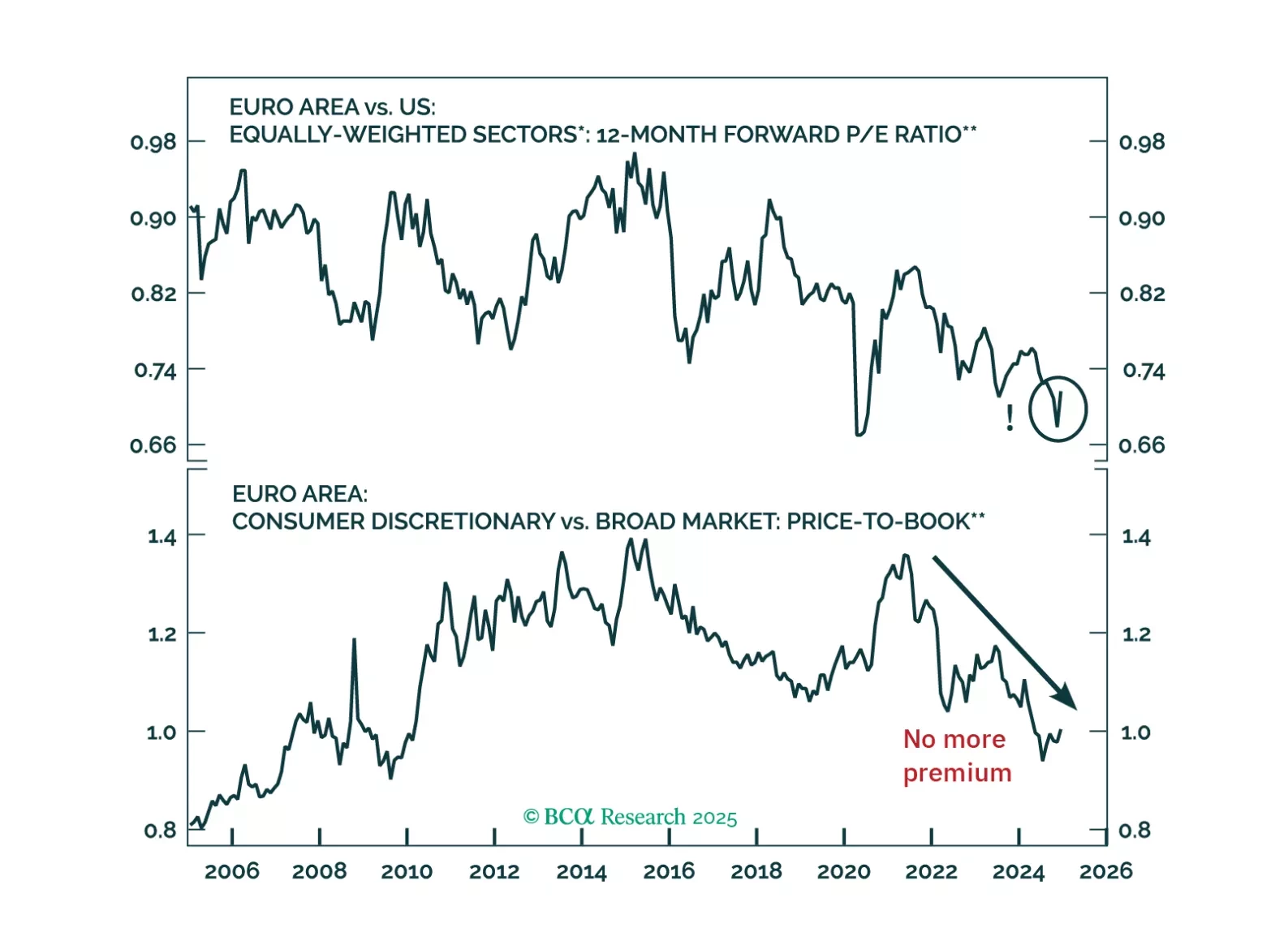

Global risk assets are engulfed in a wave of euphoria, which is pulling Europe higher along the way. However, risks still abound. How should investors adjust their allocation to Europe under these highly uncertain conditions?

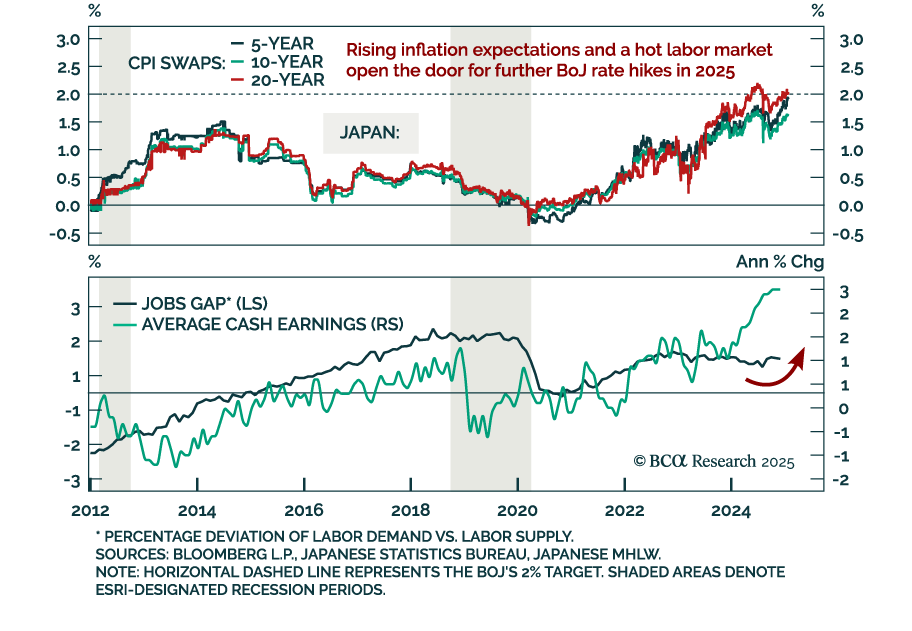

The Bank of Japan hiked rates by 25 bps as expected to 0.50%, or a 17-year high. The BoJ is currently the only G10 central bank in a hiking cycle, as the hot labor market creates sustained domestic price pressures. Additionally, the BoJ signaled a…

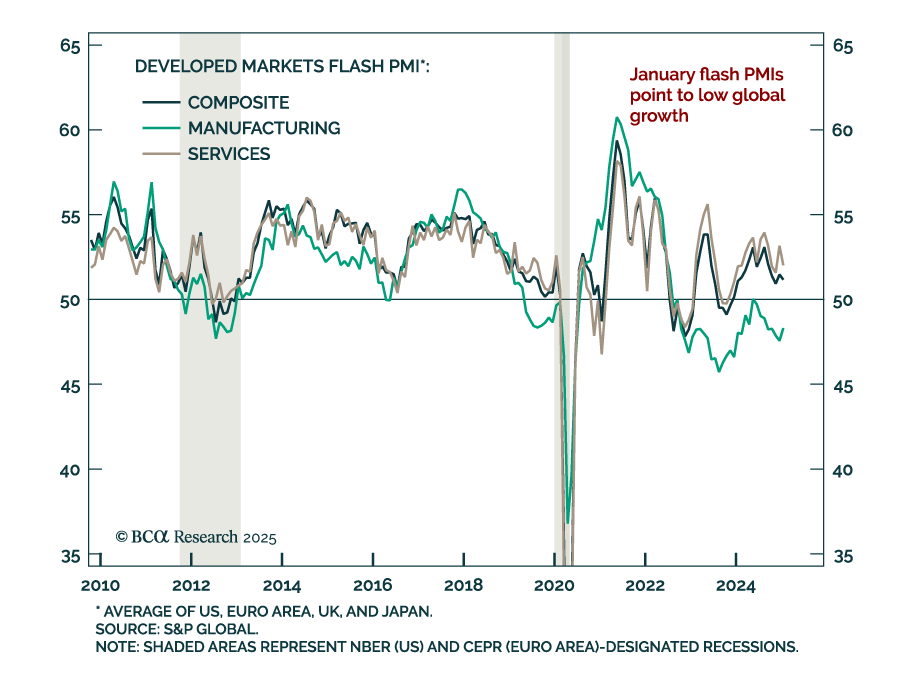

January’s flash PMIs for the major developed markets showed that manufacturing contracted at a slower pace and service activity continues to display significant regional differences. Moreover, the performance gap between the US and its DM peers…