Economy

Regular readers are familiar with our expectations for a global recession over the cyclical investment timeframe. A global downturn is overwhelmingly bearish for oil demand. The supply side, on the other hand, is simultaneously facing the threat of supply…

In the fifth installment of a BCA Special Report series on nuclear energy, our colleagues argue that US nuclear energy dominance is decaying. Though still the world’s leader in generation and capacity, the US will not hold the mantle indefinitely given high…

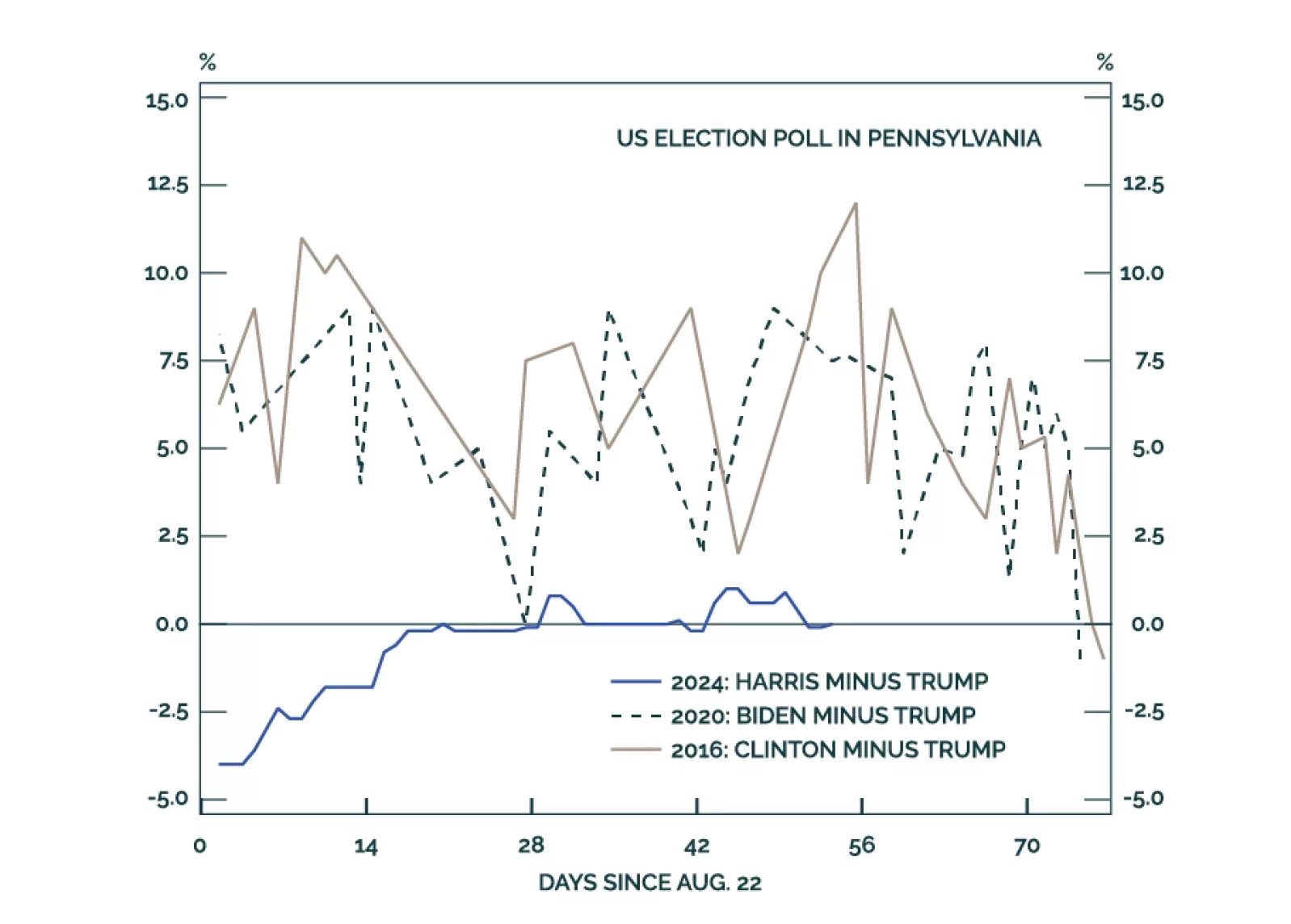

The month of October ahead of a US general election tends to be a volatile month with negative outcome for equities. As such, it is prudent to remain on the sidelines until after the election.

The US election underscores three long-term trends of Generational Change, Peak Polarization, and Limited Big Government. Investors should expect more volatility around the election and should assess the results before adding more risk. While we predicted the October surprise from the Middle East, more surprises are coming before the final vote is cast.

German factory orders contracted by a larger-than-anticipated 5.8% m/m (3.9% y/y) in August, from a 3.9% expansion (4.6% y/y). Domestically, Germany is constitutionally bound to maintain a balanced budget. The emergency pandemic funds disbursed in 2020 are…

Indian equities reached new highs in late September. Our Emerging Market strategists recommend dedicated EM investors use these gains as an opportunity to reduce Indian equity allocations from neutral to underweight. They expect both profits and multiples to…

The Swiss KOF Barometer is a composite leading indicator of the Swiss economy. It surprised to the upside in September coming in at 105.5 against expectations of 101.0. The August reading was also significantly revised higher, from 101.6 to 105.0. …

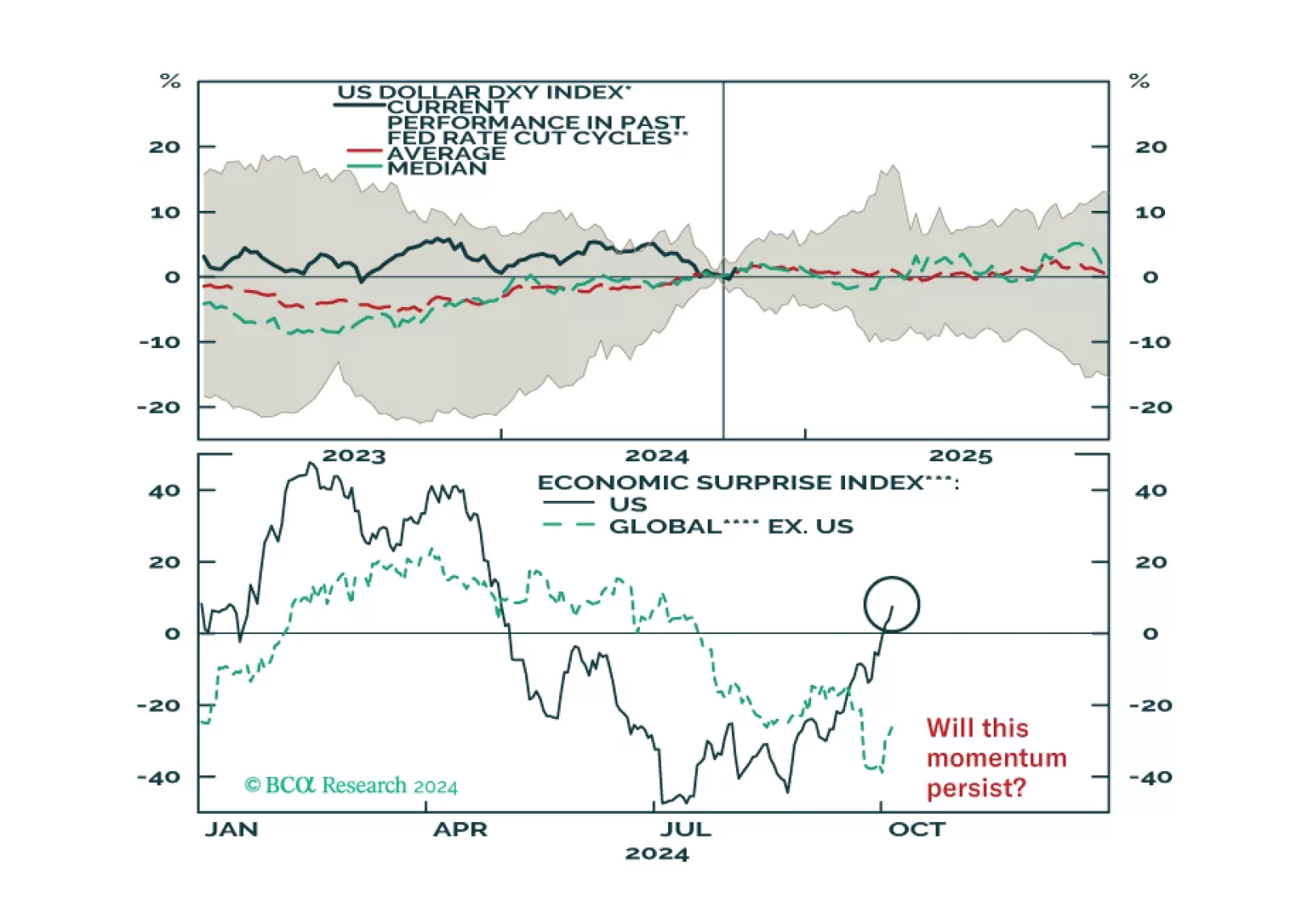

The dollar had erased all of its 2024 gains going into the fall, as markets prepared for Fed rate cuts. After a nearly 6% drawdown over the spring and summer, last week’s DXY rally brought the dollar back into the black YTD. Can these gains continue now…

According to BCA Research’s Private Markets & Alternatives service, intra-market repricing will offer investors a unique opportunity to enter the industrial real estate space in the next two years. In the short term, Mexico will be a big winner…

This report looks at the likely path for the dollar and bond yields over the next 6-to-12 months.