Economy

The conventional 30-year mortgage rate eased further to 6.2% from above 7% back in the spring, spurring a 20.3% surge in refinancing activity last week. Mortgage applications rose 11.0%, marking a fifth consecutive week of increase and the Conference Board…

In a widely expected move, the Riksbank lowered its policy rate from 3.5% to 3.25% in September, marking its third cut this year. It embarked on its easing cycle in May, leading many other DM central banks, and has been sending increasingly dovish messages…

A US recession remains our base case over a cyclical investment horizon. We expect the ongoing labor market deterioration to eventually tip the economy into a recession. We therefore continue to expect the disinflationary forces to dominate the US economy…

US investment grade and high yield spreads have tightened 22 and 75 bps since their August highs. Risk assets have cheered the outsized Fed rate cut as the narrative in markets aligns with the Fed’s conviction it can deliver a soft landing. Our US Bond…

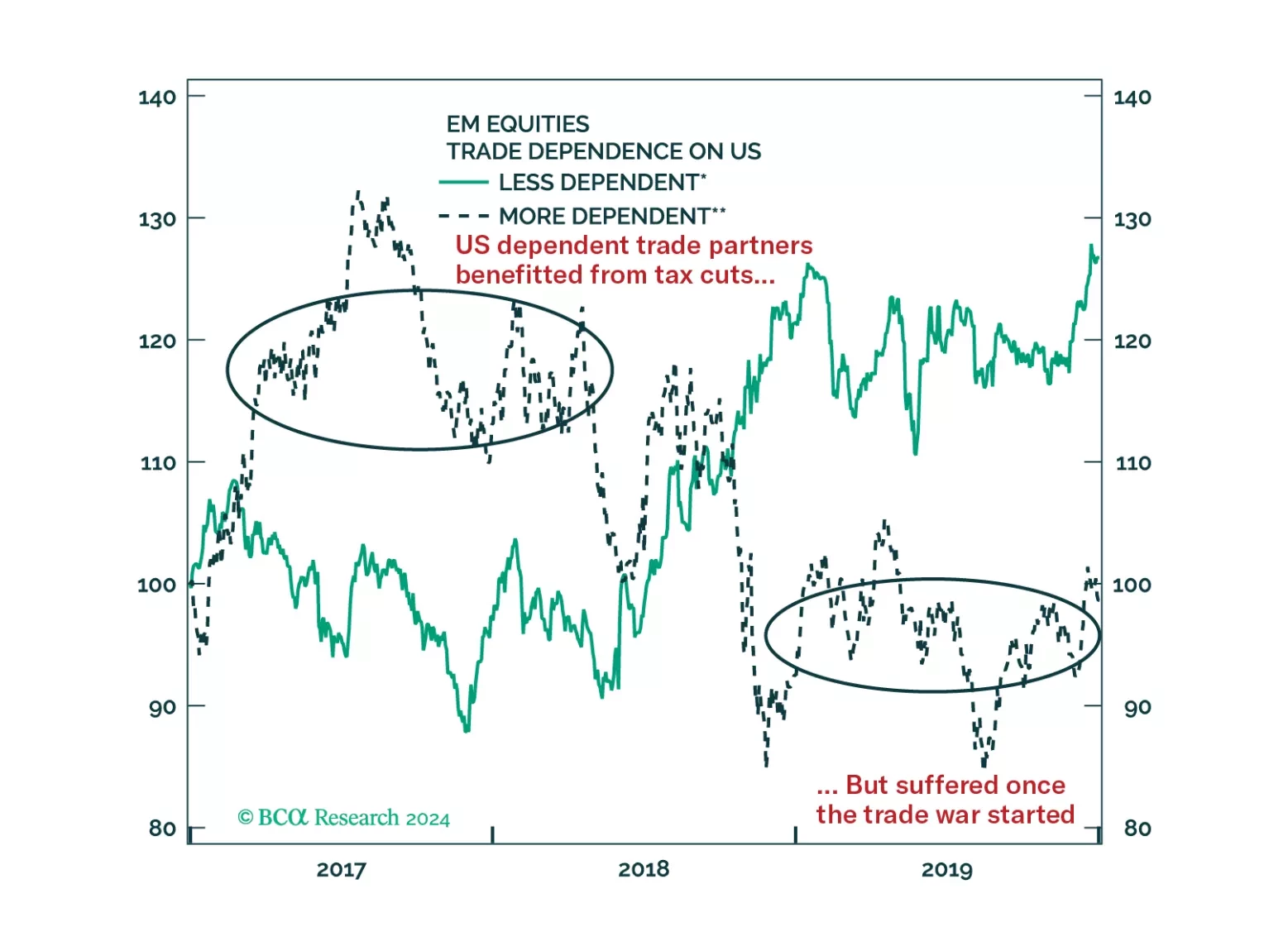

BCA Research’s Geopolitical Strategy service introduced a Global Political Capital Index. Investors should favor countries with newly elected government, small government size, and ample room to cut policy rate. Ideally, they should also be in a stable…

This insight parses through the RBA’s latest policy decision, and makes recommendations on whether to expect any rate cuts in 2024, and beyond.

As we head into a more turbulent macroeconomic and geopolitical period, investors should favor countries with newly elected government, small government size, and ample room to cut policy rate. Ideally, they should also be in a stable region, and not so dependent on the US or China. Hence, we are introducing the Global Political Capital Index as a way to integrate these factors into a score that can help narrow down the countries with the best and worst abilities to deal with the incoming challenges.

The Conference Board Consumer Confidence index unexpectedly shed 6.9 points to 98.7 in September. Both the Present Situation and Expectations components declined, by 10.3 and 4.6 points respectively. The decline in morale in September was broad-based across…

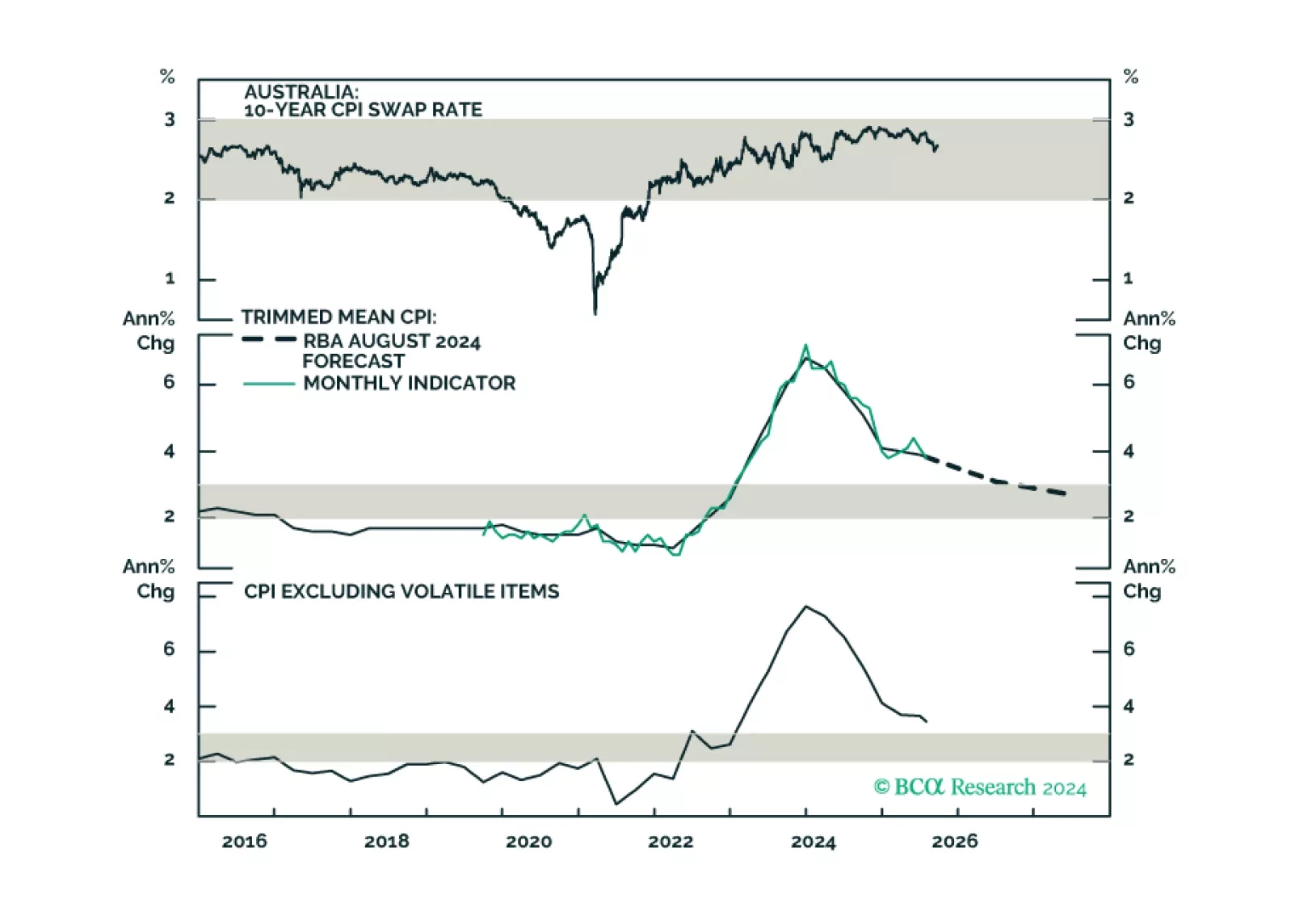

In a widely expected move, the Reserve Bank of Australia kept the cash rate unchanged at 4.35% in September. All measures of Australian CPI inflation remain well above the RBA target range. The Commonwealth Energy Bill Relief Fund and other…

Export dynamics from small open economies are a good bellwether for global growth conditions. Taiwan export orders accelerated from 4.8% y/y to a faster-than-anticipated 9.1% in August. The faster pace of growth was also broad-based among the country’s…