Elections

Highlights Our three strategic themes over the long run: (1) great power rivalry (2) hypo-globalization (3) populism and nationalism. The implications are inflationary over the long run. Nations that gear up for potential conflict and expand the social safety net to appease popular discontent will consume a lot of resources. Our three key views for 2022: (1) China’s reversion to autocracy (2) America’s policy insularity (3) petro-state leverage. The implications are mostly but not entirely inflationary: China will ease policy, the US will pass more stimulus, and energy supply may suffer major disruptions. Stay long gold, neutral US dollar, short renminbi, and short Taiwanese dollar. Stay tactically long global large caps and defensives. Buy aerospace/defense and cyber-security stocks. Go long Japanese and Mexican equities – both are tied to the US in an era of great power rivalry. Feature Chart 1US Resilience

US Resilience

US Resilience

Global investors have not yet found a substitute for the United States. Despite a bout of exuberance around cyclical non-US assets at the beginning of 2021, the year draws to a close with King Dollar rallying, US equities rising to 61% of global equity capitalization, and the US 30-year Treasury yield unfazed by inflation fears (Chart 1). American outperformance is only partly explained by its handling of the lingering Covid-19 pandemic. The US population was clearly less restricted by the virus (Chart 2). But more to the point, the US stimulated its economy by 25% of GDP over the course of the crisis, while the average across major countries was 13% of GDP. Americans are still more eager to go outdoors and the government has been less stringent in preventing them (Chart 3).

Chart 2

Chart 3Social Restrictions Short Of Lockdown

Social Restrictions Short Of Lockdown

Social Restrictions Short Of Lockdown

Going forward, the pandemic should decline in relevance, though it is still possible that a vaccine-resistant mutation will arise that is deadlier for younger people, causing a new round of the crisis. The rotation into assets outside the US will be cautious. Across the world, monetary and credit growth peaked and rolled over this year, after the extraordinary effusion of stimulus to offset the social lockdowns of 2020 (Chart 4). Government budget deficits started to normalize while central banks began winding down emergency lending and bond-buying. More widespread and significant policy normalization will get under way in 2022 in the face of high core inflation. Tightening will favor the US dollar, especially if global growth disappoints expectations. Chart 4Waning Monetary And Credit Stimulus

Waning Monetary And Credit Stimulus

Waning Monetary And Credit Stimulus

Chart 5Global Growth Stabilization

Global Growth Stabilization

Global Growth Stabilization

Global manufacturing activity fell off its peak, especially in China, where authorities tightened monetary, fiscal, and regulatory policy aggressively to prevent asset bubbles from blowing up (Chart 5). Now China is easing policy on the margin, which should shore up activity ahead of an important Communist Party reshuffle in fall 2022. The rest of the world’s manufacturing activity is expected to continue expanding in 2022, albeit less rapidly. This trend cuts against US outperformance but still faces a range of hurdles, beginning with China. In this context, we outline three geopolitical themes for the long run as well as three key views for the coming 12 months. Our title, “The Gathering Storm,” refers to the strategic challenge that China and Russia pose to the United States, which is attempting to form a balance-of-power coalition to contain these autocratic rivals. This is the central global geopolitical dynamic in 2022 and it is ultimately inflationary. Three Strategic Themes For The Long Run The international system will remain unstable in the coming years. Global multipolarity – or the existence of multiple, competing poles of political power – is the chief destabilizing factor. This is the first of our three strategic themes that will persist next year and beyond (Table 1). Our key views for 2022, discussed below, flow from these three strategic themes. Table 1Strategic Themes For 2022 And Beyond

2022 Key Views: The Gathering Storm

2022 Key Views: The Gathering Storm

1. Great Power Rivalry Multipolarity – or great power rivalry – can be illustrated by the falling share of US economic clout relative to the rest of the world, including but not limited to strategic rivals like China. The US’s decline is often exaggerated but the picture is clear if one looks at the combined geopolitical influence of the US and its closest allies to that of the EU, China, and Russia (Chart 6).

Chart 6

China’s rise is the most destabilizing factor because it comes with economic, military, and technological prowess that could someday rival the US for global supremacy. China’s GDP has surpassed that of the US in purchasing power terms and will do so in nominal terms in around five years (Chart 7).

Chart 7

True, China’s potential growth is slowing and Chinese financial instability will be a recurring theme. But that very fact is driving Beijing to try to convert the past 40 years of economic success into broader strategic security. Chart 8America's Global Role Persists (If Lessened)

America's Global Role Persists (If Lessened)

America's Global Role Persists (If Lessened)

Since China is capable of creating an alternative political order in Asia Pacific, and ultimately globally, the United States is reacting. It is penalizing China’s economy and seeking to refurbish alliances in pursuit of a containment policy. The American reaction to the loss of influence has been unpredictable, contradictory, and occasionally belligerent. New isolationist impulses have emerged among an angry populace in reaction to gratuitous wars abroad and de-industrialization. These impulses appeared in both the Obama and Trump administrations. The Biden administration is attempting to manage these impulses while also reinforcing America’s global role. The pandemic-era stimulus has enabled the US to maintain its massive trade deficit and aggressive defense spending. But US defense spending is declining relative to the US and global economy over time, encouraging rival nations to carve out spheres of influence in their own neighborhoods (Chart 8). Russia’s overall geopolitical power has declined but it punches above its weight in military affairs and energy markets, a fact which is vividly on display in Ukraine as we go to press. The result is to exacerbate differences in the trans-Atlantic alliance between the US and the European Union, particularly Germany. The EU’s attempt to act as an independent great power is another sign of multipolarity, as well as the UK’s decision to distance itself from the continent and strengthen the Anglo-American alliance. If the US and EU do not manage their differences over how to handle Russia, China, and Iran then the trans-Atlantic relationship will weaken and great power rivalry will become even more dangerous. 2. Hypo-Globalization The second strategic theme is hypo-globalization, in which the ancient process of globalization continues but falls short of its twenty-first century potential, given advances in technology and governance that should erode geographic and national boundaries. Hypo-globalization is the opposite of the “hyper-globalization” of the 1990s-2000s, when historic barriers to the free movement of people, goods, and capital seemed to collapse overnight. Chart 9From 'Hyper-Globalization' To Hypo-Globalization

From 'Hyper-Globalization' To Hypo-Globalization

From 'Hyper-Globalization' To Hypo-Globalization

The volume of global trade relative to industrial production peaked with the Great Recession in 2008-10 and has declined slowly but surely ever since (Chart 9). Many developed markets suffered the unwinding of private debt bubbles, while emerging economies suffered the unwinding of trade manufacturing. Periods of declining trade intensity – trade relative to global growth – suggest that nations are turning inward, distrustful of interdependency, and that the frictions and costs of trade are rising due to protectionism and mercantilism. Over the past two hundred years globalization intensified when a broad international peace was agreed (such as in 1815) and a leading imperial nation was capable of enforcing law and order on the seas (such as the British empire). Globalization fell back during times of “hegemonic instability,” when the peace settlement decayed while strategic and naval competition eroded the global trading system. Today a similar process is unfolding, with the 1945 peace decaying and the US facing the revival of Russia and China as regional empires capable of denying others access to their coastlines and strategic approaches (Chart 10).1 Chart 10Hypo-Globalization And Hegemonic Instability

Hypo-Globalization And Hegemonic Instability

Hypo-Globalization And Hegemonic Instability

Chart 11Hypo-Globalization: Temporary Trade Rebound

Hypo-Globalization: Temporary Trade Rebound

Hypo-Globalization: Temporary Trade Rebound

No doubt global trade is rebounding amid the stimulus-fueled recovery from Covid-19. But the upside for globalization will be limited by the negative geopolitical environment (Chart 11). Today governments are not behaving as if they will embark on a new era of ever-freer movement and ever-deepening international linkages. They are increasingly fearful of each other’s strategic intentions and using fiscal resources to increase economic self-sufficiency. The result is regionalization rather than globalization. Chinese and Russian attempts to revise the world order, and the US’s attempt to contain them, encourages regionalization. For example, the trade war between the US and China is morphing into a broader competition that limits cooperation to a few select areas, despite a change of administration in the United States. The further consolidation of President Xi Jinping’s strongman rule will exacerbate this dynamic of distrust and economic divorce. Emerging Asia and emerging Europe live on the fault lines of this shift from globalization to regionalism, with various risks and opportunities. Generally we are bullish EM Asia and bearish EM Europe. 3. Populism And Nationalism A third strategic theme consists of populism and nationalism, or anti-establishment political sentiment in general. These forces will flare up in various forms across the world in 2022 and beyond. Even as unemployment declines, the rise in food and fuel inflation will make it difficult for low wage earners to make ends meet. The “misery index,” which combines unemployment and inflation, spiked during the pandemic and today stands at 10.8% in the US and 11.4% in the EMU, up from 5.2% and 8.1% before the pandemic, respectively (Chart 12). Large budget deficits and trade deficits, especially in the US and UK, feed into this inflationary environment. Most of the major developed markets have elected new governments since the pandemic, with the notable exception of France and Spain. Thus they have recapitalized their political systems and allowed voters to vent some frustration. These governments now have some time to try to mitigate inflation before the next election. Hence policy continuity is not immediately in jeopardy, which reduces uncertainty for investors. By contrast, many of the emerging economies face higher inflation, weak growth, and are either coming upon elections or have undemocratic political systems. Either way the result will be a failure to address household grievances promptly. The misery index is trending upward and governments are continually forced to provide larger budget deficits to shore up growth, fanning inflation (Chart 13). Chart 12DM: Political Risk High But New Governments In Place

DM: Political Risk High But New Governments In Place

DM: Political Risk High But New Governments In Place

Chart 13EM: Political Risk High But Governments Not Recapitalized

EM: Political Risk High But Governments Not Recapitalized

EM: Political Risk High But Governments Not Recapitalized

Chart 14EM Populism/Nationalism Threatens Negative Surprises In 2022

EM Populism/Nationalism Threatens Negative Surprises In 2022

EM Populism/Nationalism Threatens Negative Surprises In 2022

Just as social and political unrest erupted after the Great Recession, notably in the so-called “Arab Spring,” so will new movements destabilize various emerging markets in the wake of Covid-19. Regime instability and failure can lead to big changes in policies, large waves of emigration, wars, and other risks that impact markets. The risks are especially high unless and until Chinese imports revive. Investors should be on the lookout for buying opportunities in emerging markets once the bad news is fully priced. National and local elections in Brazil, India, South Korea, the Philippines, and Turkey will serve as market catalysts, with bad news likely to precede good news (Chart 14). Bottom Line: These three themes – great power rivalry, hypo-globalization, and populism/nationalism – are inflationary in theory, though their impact will vary based on specific events. Multipolarity means that governments will boost industrial and defense spending to gear up for international competition. Hypo-globalization means countries will attempt to put growth on a more reliable domestic foundation rather than accept dependency on an unreliable international scene, thus constraining supplies from abroad. Populism and nationalism will lead to a range of unorthodox policies, such as belligerence abroad or extravagant social spending at home. Of course, the inflationary bias of these themes can be upset if they manifest in ways that harm growth and/or inflation expectations, which is possible. But the general drift will be an inflationary policy setting. Inflation may subside in 2022 only to reemerge as a risk later. Three Key Views For 2022 Within this broader context, our three key views for 2022 are as follows: 1. China’s Reversion To Autocracy As President Xi Jinping leads China further down the road of strongman rule and centralization, the country faces a historic confluence of internal and external risks. This was our top view in 2021 and the same dynamic continues in 2022. The difference is that in 2021 the risk was excessive policy tightening whereas this coming year the risk is insufficient policy easing. Chart 15China Eases Fiscal Policy To Secure Recovery In 2022

China Eases Fiscal Policy To Secure Recovery In 2022

China Eases Fiscal Policy To Secure Recovery In 2022

China’s economy is witnessing a secular slowdown, a deterioration in governance, property market turmoil, and a rise in protectionism abroad. The long decline in corporate debt growth points to the structural slowdown. Animal spirits will not improve in 2022 so government spending will be necessary to try to shore up overall growth. The Politburo signaled that it will ease fiscal policy at the Central Economic Work Conference in early December, a vindication of our 2021 view. Neither the combined fiscal-and-credit impulse nor overall activity, indicated by the Li Keqiang Index, have shown the slightest uptick yet (Chart 15). Typically it takes six-to-nine months for policy easing to translate to an improvement in real economic activity. The first half of the year may still bring economic disappointments. But policymakers are adjusting to avoid a crash. Policy will grow increasingly accommodative as necessary in the first half of 2022. The key political constraint is the Communist Party’s all-important political reshuffle, the twentieth national party congress, to be held in fall 2022 (usually October). While Xi may not want the economy to surge in 2022, he cannot afford to let it go bust. The experience of previous party congresses shows that there is often a policy-driven increase in bank loans and fixed investment. Current conditions are so negative as to ensure that the government will provide at least some support, for instance by taking a “moderately proactive approach” to infrastructure investment (Chart 16). Otherwise a collapse of confidence would weaken Xi’s faction and give the opposition faction a chance to shore up its position within the Communist Party. Chart 16China Aims For Stability, Not Rapid Growth, Ahead Of 20th National Party Congress

China Aims For Stability, Not Rapid Growth, Ahead Of 20th National Party Congress

China Aims For Stability, Not Rapid Growth, Ahead Of 20th National Party Congress

Party congresses happen every five years but the ten-year congresses, such as in 2022, are the most important for the country’s overall political leadership. The party congresses in 1992, 2002, and 2012 were instrumental in transferring power from one leader to the next, even though the transfer of power was never formalized. Back in 2017 Xi arranged to stay in power indefinitely but now he needs to clinch the deal, lest any unforeseen threat emerge from at home or abroad. Xi’s success in converting the Communist Party from “consensus rule” to his own “personal rule” will be measurable by his success in stacking the Politburo and Politburo Standing Committee with factional allies. He will also promote his faction across the Central Committee so as to shape the next generations of party leaders and leave his imprint on policy long after his departure. The government will be extremely sensitive to any hint of dissent or resistance and will move aggressively to quash it. Investors should not be surprised to see high-level sackings of public officials or private magnates and a steady stream of scandals and revelations that gain prominence in western media. The environment is also ripe for strange and unexpected incidents that reveal political differences beneath the veneer of unity in China: defections, protests, riots, terrorist acts, or foreign interference. Most incidents will be snuffed out quickly but investors should be wary of “black swans” from China in 2022. Chinese government policies will not be business friendly in 2022 aside from piecemeal fiscal easing. Everything Beijing does will be bent around securing Xi’s supremacy at all levels. Domestic politics will take precedence over economic concerns, especially over the interests of private businesses and foreign investors, as is clear when it comes to managing financial distress in the property sector. Negative regulatory surprises and arbitrary crackdowns on various industrial sectors will continue, though Beijing will do everything in its power to prevent the property bust from triggering contagion across the economic system. This will probably work, though the dam may burst after the party congress. Relations with the US and the West will remain poor, as the democracies cannot afford to endorse what they see as Xi’s power grab, the resurrection of a Maoist cult of personality, and the betrayal of past promises of cooperation and engagement. America’s midterm election politics will not be conducive to any broad thaw in US-China relations. While China will focus on domestic politics, its foreign policy actions will still prove relatively hawkish. Clashes with neighbors may be instigated by China to warn away any interference or by neighbors to try to embarrass Xi Jinping. The South and East China Seas are still ripe for territorial disputes to flare. Border conflicts with India are also possible. Taiwan remains the epicenter of global geopolitical risk. A fourth Taiwan Strait Crisis looms as China increases its military warnings to Taiwan not to attempt anything resembling independence (Chart 17A). China may use saber-rattling, economic sanctions, cyber war, disinformation, and other “gray zone” tactics to undermine the ruling party ahead of Taiwan’s midterm elections in November 2022 and presidential elections in January 2024. A full-scale invasion cannot be ruled out but is unlikely in the short run, as China still has non-military options to try to arrange a change of policy in Taiwan.

Chart 17

Chart 17BMarket-Based Risk Indicators Say China/Taiwan Risk Has Not Peaked

Market-Based Risk Indicators Say China/Taiwan Risk Has Not Peaked

Market-Based Risk Indicators Say China/Taiwan Risk Has Not Peaked

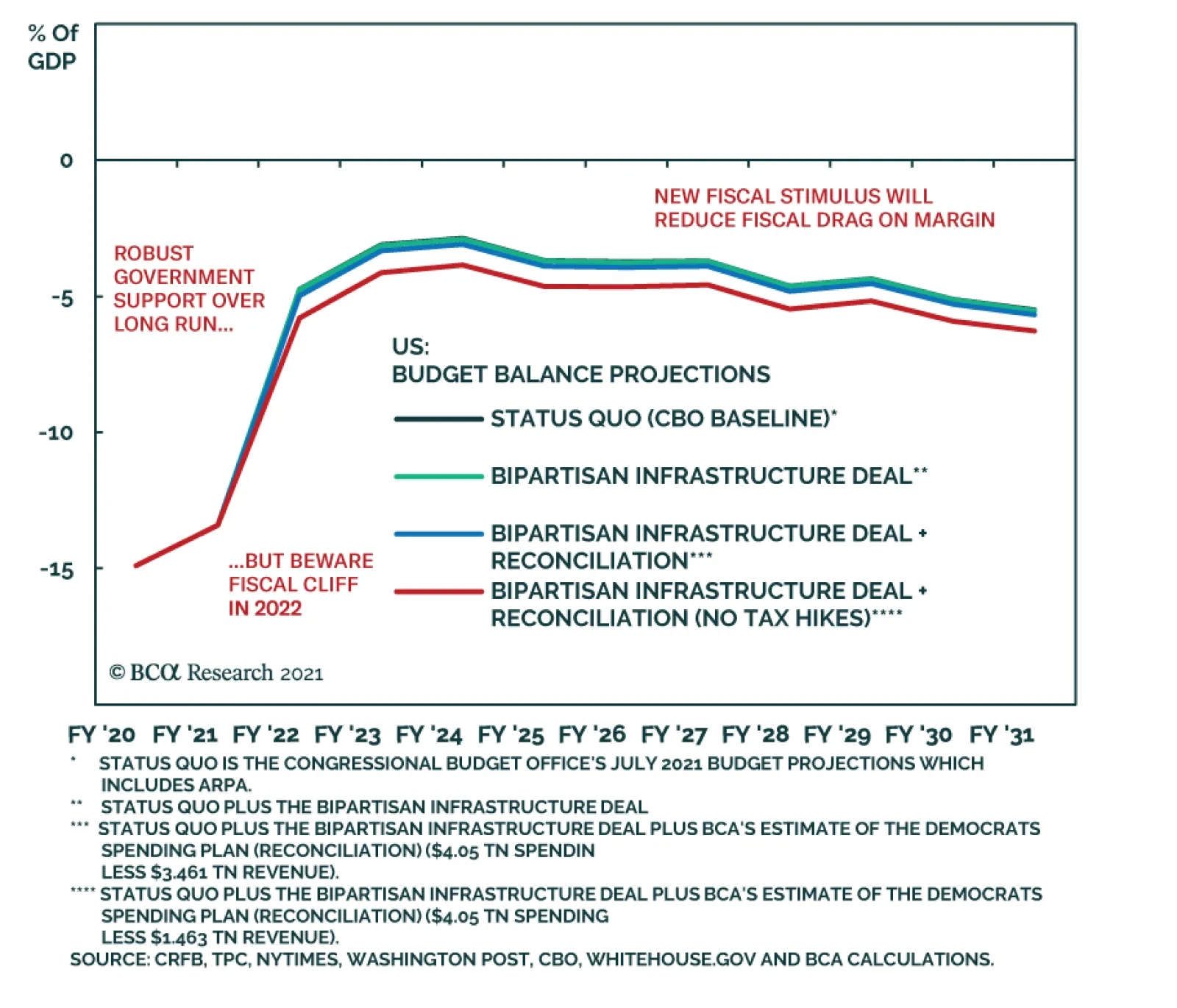

China has not yet responded to the US’s deployment of a small number of troops in Taiwan or to recent diplomatic overtures or arms sales. It could stage a major show of force against Taiwan to help consolidate power at home. China also has an interest in demonstrating to US allies and partners that their populations and economies will suffer if they side with Washington in any contingency. Given China’s historic confluence of risks, it is too soon for global investors to load up on cheap Chinese equities. Volatility will remain high. Weak animal spirits, limited policy easing, high levels of policy uncertainty, regulatory risk, ongoing trade tensions, and geopolitical risks suggest that investors should remain on the sidelines, and that a large risk premium can persist throughout 2022. Our market-based geopolitical risk indicators for both China and Taiwan are still trending upwards (Chart 17B). Global investors should capitalize on China’s policy easing indirectly by investing in commodities, cyclical equity sectors, and select emerging markets. 2. America’s Policy Insularity Our second view for 2022 centers on the United States, which will focus on domestic politics and will thus react or overreact to the many global challenges it faces. The US faces the first midterm election after the chaotic and contested 2020 presidential election. Political polarization remains at historically high levels, meaning that social unrest could flare up again and major domestic terrorist incidents cannot be ruled out. So far the Biden administration has focused on the domestic scene: mitigating the pandemic and rebooting the economy. Biden’s signature “Build Back Better” bill, $1.75 trillion investment in social programs, has passed the House of Representatives but not the Senate. The spike in inflation has shaken moderate Democratic senators who are now delaying the bill. We expect it to pass, since tax hikes were dropped, but our conviction is low (65% subjective odds), as a single defection would derail the bill. The implication would be inflationary since it would mark a sizable increase in government spending at a time when the output gap is already virtually closed. Spending would likely be much larger than the Congressional Budget Office estimate, shown in Chart 18, because the bill contains various gimmicks and hard-to-implement expiration clauses. Equity markets may not sell if the bill fails, since more fiscal stimulus would put pressure on the Federal Reserve to hike rates faster.

Chart 18

Chart 19

Whether the bill passes or fails, Biden’s legislative agenda will be frozen thereafter. He will have to resort to executive powers and foreign policy to lift his approval rating and court the median voter ahead of the midterm elections. Currently Democrats are lined up to lose the House and probably also the Senate, where a single seat would cost them their majority (Chart 19). The Senate is still in play so Biden will be averse to taking big risks. For the same reason, Biden’s foreign policy goal will be to stave off various bubbling crises. Restoring the Iranian nuclear deal was his priority but Russia has now forced its way to the top of the agenda by threatening a partial reinvasion of Ukraine. In this context Biden will not have room for maneuver with China. Congress will be hawkish on China ahead of the midterms, and Xi Jinping will be reviving autocracy, so Biden will not be able to improve relations much. Biden’s domestic policy could fuel inflation, while his domestic-focused foreign policy will embolden strategic rivals, which increases geopolitical risks. 3. Petro-State Leverage A surge in gasoline prices at the pump ahead of the election would be disastrous for a Democratic Party that is already in disarray over inflation (Chart 20). Biden has already demonstrated that he can coordinate an international release of strategic oil reserves this year. Oil and natural gas producers gain leverage when the global economy rebounds, commodity prices rise, and supply/demand balances tighten. The frequency of global conflicts, especially those involving petro-states, tend to rise and fall in line with oil prices (Chart 21). Chart 20Inflation Constrains Biden Ahead Of Midterms

Inflation Constrains Biden Ahead Of Midterms

Inflation Constrains Biden Ahead Of Midterms

Chart 21

Both Russia and Iran are vulnerable to social unrest at home and foreign strategic pressure abroad. Both have long-running conflicts with the US and West that are heating up for fundamental reasons, such as Russia’s fear of western influence in the former Soviet Union and Iran’s nuclear program. Both countries are demanding that the US make strategic concessions to atone for the Trump administration’s aggressive policies: selling lethal weapons to Ukraine and imposing “maximum pressure” sanctions on Iran. Biden is not capable of making credible long-term agreements since he could lose office as soon as 2025 and the next president could reverse whatever he agrees. But he must try to de-escalate these conflicts or else he faces energy shortages or price shocks, which would raise the odds of stagflation ahead of the election. The path of least resistance for Biden is to lift the sanctions on Iran to prevent an escalation of the secret war in the Middle East. If this unilateral concession should convince Iran to pause its nuclear activities before achieving breakout uranium enrichment capability, then Biden would reduce the odds of a military showdown erupting across the region. Opposition Republicans would accuse him of weakness but public opinion polls show that few Americans consider Iran a major threat. The problem is that this logic held throughout 2021 and yet Biden did not ease the sanctions. Given Iran’s nuclear progress and the US’s reliance on sanctions, we see a 40% chance of a military confrontation with Iran over the coming years. With regard to Ukraine, an American failure to give concessions to Russia will probably result in a partial reinvasion of Ukraine (50% subjective odds). This in turn will force the US and EU to impose sanctions on Russia, leading to a squeeze of natural gas prices in Europe and eventually price pressures in global energy markets. If Biden grants Russia’s main demands, he will avoid a larger war or energy shock but will make the US vulnerable to future blackmail. He will also demoralize Taiwan and other US partners who lack mutual defense treaties. But he may gain Russian cooperation on Iran. If Biden gives concessions to both Russia and Iran, his party will face criticism in the midterms but it will be far less vulnerable than if an energy shock occurs. This is the path of least resistance for Biden in 2022. It means that the petro-states may lose their leverage after using it, given that risk premiums would fall on Biden’s concessions. Of course, if energy shocks happen, Europe and China will suffer more than the US, which is relatively energy independent. For this reason Brussels and Beijing will try to keep diplomacy alive as long as possible. Enforcement of US sanctions on Iran may weaken, reducing Iran’s urgency to come into compliance. Germany may prevent a hardline threat of sanctions against Russia, reducing Russia’s fear of consequences. Again, petro-states have the leverage. Therefore investors should guard against geopolitically induced energy price spikes or shocks in 2022. What if other commodity producers, such as Saudi Arabia, crank up production and sink oil prices? This could happen. Yet the Saudis prefer elevated oil prices due to the host of national challenges they face in reforming their economy. If the US eases sanctions on Iran then the Saudis may make this decision. Thus downside energy price shocks are possible too. The takeaway is energy price volatility but for the most part we see the risk as lying to the upside. Investment Takeaways Traditional geopolitical risk, which focuses on war and conflict, is measurable and has slipped since 2015, although it has not broken down from the general uptrend since 2000. We expect the secular trend to be reaffirmed and for geopolitical risk to resume its rise due to the strategic themes and key views outlined above. The correlation of geopolitical risk with financial assets is debatable – namely because some geopolitical risks push up oil and commodity prices at the expense of the dollar, while others cause a safe-haven rally into the dollar (Chart 22). Global economic policy uncertainty is also measurable. It is in a secular uptrend since the 2008 financial crisis. Here the correlation with the US dollar and relative equity performance is stronger, which makes sense. This trend should also pick up going forward, which is at least not negative for the dollar and relative US equity performance (Chart 23). Chart 22Geopolitical Risk Will Rise, Market Impacts Variable

Geopolitical Risk Will Rise, Market Impacts Variable

Geopolitical Risk Will Rise, Market Impacts Variable

Chart 23Economic Policy Uncertainty Will Rise, Not Bad For US Assets

Economic Policy Uncertainty Will Rise, Not Bad For US Assets

Economic Policy Uncertainty Will Rise, Not Bad For US Assets

We are neutral on the US dollar versus the euro and recommend holding either versus the Chinese renminbi. We are short the currencies of emerging markets that suffer from great power rivalry, namely the Taiwanese dollar versus the US dollar, the Korean won versus the Japanese yen, the Russian ruble versus the Canadian dollar, and the Czech koruna versus the British pound. We remain long gold as a hedge against both geopolitical risk and inflation. We recommend staying long global equities. Tactically we prefer large caps and defensives. Within developed markets, we favor the UK and Japan. Japan in particular will benefit from Chinese policy easing yet remains more secure from China-centered geopolitical risks than emerging Asian economies. Within emerging markets, Mexico stands to benefit from US economic strength and divorce from China. We would buy Indian equities on weakness and sell Chinese and Russian equities on strength. We remain long aerospace and defense stocks and cyber-security stocks. -The GPS Team We Read (And Liked) … Conspiracy U: A Case Study “Crazy, worthless, stupid, made-up tales bring out the demons in susceptible, unthinking people.” Thus the author’s father, a Holocaust survivor translated from Yiddish, on conspiracy theories and the real danger they present in the world. Scott A. Shay, author and chairman of Signature Bank, whose first book was a finalist for the National Jewish Book Award, has written an intriguing new book on the topic and graciously sent it our way.2 Shay is a regular reader of BCA Research’s Geopolitical Strategy and an astute observer of international affairs. He is also a controversialist who has written essays for several of America’s most prominent newspapers. Shay’s latest, Conspiracy U, is a bracing read that we think investors will benefit from. We say this not because of its topical focus, which is too confined, but because of its broader commentary on history, epistemology, the US higher education system – and the very timely and relevant problem of conspiracy theories, which have become a prevalent concern in twenty-first century politics and society. The author and the particular angle of the book will be controversial to some readers but this very quality makes the book well-suited to the problem of the conspiracy theory, since it is not the controversial nature of conspiracy theories but their non-falsifiability that makes them specious. As the title suggests, the book is a polemical broadside. The polemic arises from Shay’s unique set of moral, intellectual, and sociopolitical commitments. This is true of all political books but this one wears its topicality on its sleeve. The term “conspiracy” in the title refers to antisemitic, anti-Israel, and anti-Zionist conspiracy theories, particularly the denial of the Holocaust, coming from tenured academics on both the right and the left wings of American politics. The “U” in the title refers to universities, namely American universities, with a particular focus on the author’s beloved alma mater, Northwestern University in Chicago, Illinois. Clearly the book is a “case study” – one could even say the prosecution of a direct and extended public criticism of Northwestern University – and the polemical perspective is grounded in Shay’s Jewish identity and personal beliefs. Equally clearly Shay makes a series of verifiable observations and arguments about conspiracy theories as a contemporary phenomenon and their presence, as well as the presence of other weak and lazy modes of thought, in “academia writ large.” This generalization of the problem is where most readers will find the value of the book. The book does not expect one to share Shay’s identity, to be a Zionist or support Zionism, or to agree with Israel’s national policies on any issue, least of all Israeli relations with Arabs and Palestinians. Shay’s approach is rigorous and clinical. He is a genuine intellectual in that he considers the gravest matters of concern from various viewpoints, including viewpoints radically different from his own, and relies on close readings of the evidence. In other words, Shay did not write the book merely to convince people that two tenured professors at Northwestern are promoting conspiracy theories. That kind of aberration is sadly to be expected and at least partially the result of the tenure system, which has advantages as well, not within the scope of the book. Rather Shay wrote it to provide a case study for how it is that conspiracy theories can manage to be adopted by those who do not realize what they are and to proliferate even in areas that should be the least hospitable – namely, public universities, which are supposed to be beacons of knowledge, science, openness, and critical thinking, but also other public institutions, including the fourth estate. Shay is meticulous with his sources and terminology. He draws on existing academic literature to set the parameters of his subject, defining conspiracy theories as “improbable hypotheses [or] intentional lies … about powerful and sinister groups conspiring to harm good people, often via a secret cabal.” The definition excludes “unwarranted criticism” and “unfair/prejudiced perspectives,” which are harmful but unavoidable. Many prejudices and false beliefs are “still falsifiable in the minds of their adherents,” which is not the case with conspiracy theories, although deep prejudices can obviously be helpful in spreading such theories. Conspiracy theories often depend on “a stunning amount of uniformity of belief and coordination of action without contingencies.” They also rely excessively on pathos, or emotion, in making their arguments, as opposed to logos (reason) and ethos (credibility, authority). Unfortunately there is no absolute, infallible distinction between conspiracy theories and other improbable theories – say, yet-to-be-confirmed theories about conspiracies that actually occurred. Conspiracy theories differ from other theories “in their relationship to facts, evidence, and logic,” which may sound obvious but is very much to the point. Again, “the key difference is the evidence and how it is evaluated.” There is no ready way to refute the fabrications, myths, and political propaganda that people believe without taking the time to assess the claims and their foundations. This requires an open mind and a grim determination to get to the bottom of rival claims about events even when they are extremely morally or politically sensitive, as is often the case with wars, political conflicts, atrocities, and genocides: Reliable historians, journalists, lawyers, and citizens must first approach the question of the cause or the identity of perpetrators and victims of an event or process with an open mind, not prejudiced to either party, and then evaluate the evidence. The diagnosis may be easy but the treatment is not – it takes time, study, and debate, and one’s interlocutors must be willing to be convinced. This problem of convincing others is critical because it is the part that is so often left out of modern political discourse. Conspiracy theories are often hateful and militant, so there is a powerful urge to censor or repress them. Openly debating with conspiracy theorists runs the risk of legitimizing or appearing to legitimize their views, providing them with a public forum, which seems to grant ethos or authority to arguments that are otherwise conspicuously lacking in it. In some countries censorship is legal, almost everywhere when violence is incited. The problem is that the act of suppression can feed the same conspiracy theories, so there is a need, in the appropriate context, to engage with and refute lies and specious arguments. Clients frequently email us to ask our view of the rise of conspiracy theories and what they entail for the global policy backdrop. We associate them with the broader breakdown in authority and decline of public trust in institutions. Shay’s book is an intervention into this topic that clients will find informative and thought-provoking, even if they disagree with the author’s staunchly pro-Israel viewpoint. It is precisely Shay’s ability to discuss and debate extremely contentious matters in a lucid and empirical manner – antisemitism, the history of Zionism, Holocaust denialism, Arab-Israeli relations, the Rwandan genocide, QAnon, the George Floyd protests, various other controversies – that enables him to defend a controversial position he holds passionately, while also demonstrating that passion alone can produce the most false and malicious arguments. As is often the case, the best parts of the book are the most personal – when Shay tells about his father’s sufferings during the Holocaust, and journey from the German concentration camps to New York City, and about Shay’s own experiences scraping enough money together to go to college at Northwestern. These sequences explain why the author felt moved to stage a public intervention against fringe ideological currents, which he shows to have gained more prominence in the university system than one might think. The book is timely, as American voters are increasingly concerned about the handling of identity, inter-group relations, history, education, and ideology in the classroom, resulting in what looks likely to become a new and ugly episode of the culture and education wars. Let us hope that Shay’s standards of intellectual freedom and moral decency prevail. Matt Gertken, PhD Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 The downshift in globalization today is even worse than it appears in Chart 10 because several countries have not yet produced the necessary post-pandemic data, artificially reducing the denominator and making the post-pandemic trade rebound appear more prominent than it is in reality. 2 Scott A. Shay, Conspiracy U: A Case Study (New York: Post Hill Press, 2021), 279 pages. Strategic Themes Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Appendix: GeoRisk Indicator China

China: GeoRisk Indicator

China: GeoRisk Indicator

Russia

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

United Kingdom

UK: GeoRisk Indicator

UK: GeoRisk Indicator

Germany

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

France

France: GeoRisk Indicator

France: GeoRisk Indicator

Italy

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Canada

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Spain

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Taiwan

Taiwan Territory: GeoRisk Indicator

Taiwan Territory: GeoRisk Indicator

Korea

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Turkey

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Brazil

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Australia

Australia: GeoRisk Indicator

Australia: GeoRisk Indicator

South Africa

South Africa: GeoRisk Indicator

South Africa: GeoRisk Indicator

Section III: Geopolitical Calendar

Highlights Few emerging market peers have a track record of democracy like India does. Russia and others have long histories of political instability and one-man rule. Several large EMs have experienced stints of military rule in the post-WWII era. While India’s democratic credentials are real, these should not be exaggerated. India’s political system suffers from some structural and cyclical vulnerabilities. These imperfections deserve attention today, more than ever, given that India trades at a record premium to peers. From a strategic perspective, we remain Buyers of India. India’s democratic traditions will lend political stability as the country’s economic heft grows. However, on a time horizon, we recommend paring exposure to Indian assets. A loaded state election calendar awaits in 2022, which will be followed by crucial state elections in 2023 and general elections in 2024. While we expect the incumbent political party to retain power in 2024, history suggests that the road to general elections is paved with policy risks. Policymakers tend to shift attention from market friendly-reform to voter-friendly policies as these key state elections approach. Additionally, geopolitical risks for India are ascendant as dangerous transitions are underway to India’s west and east too. Feature

Chart 1

Investors regard India as being exceptionally well-off on political parameters. It is viewed by many as the blue-eyed boy of emerging market democracies. And for good reason. Despite its massive population and very low per capita incomes, India has remained a functional democracy for over seventy years. Democratic political regimes are a relatively new trend. The number of democracies began exceeding the number autocracies in the world only very recently in 2002 (Chart 1). India was one of the earliest adopters of this trend compared to emerging market peers. Its democratic traditions are so well-entrenched now that they are comparable to those of some of the most developed economies of the world (Chart 2). To add to these democratic credentials, every government at the national level in India has completed its full five-year term since 1999, thereby offering stability. Investors greatly value the political stability that India offers. While political stability is only one factor that investors consider, India has traded at a 28% premium relative to democracies and a 67% premium to non-democracies like Russia and China over the last decade (Chart 3).

Chart 2

Chart 3

In this report we highlight that while India’s democratic credentials are real, these should not be exaggerated. The political system in India is solid but far from perfect. It suffers from both structural and cyclical vulnerabilities. These imperfections deserve attention today more than ever, given that India trades at a record premium to peers (Chart 3). Also, a closer look at India’s political system is warranted given that both geopolitical and macroeconomic risks for India are ascendant. With India, the devil always lies in the details. India is the largest democracy of the world but is also one of the few large democracies that follows a first-past-the-post (FPTP) method of determining election winners and has no effective limit on the number of political parties that can contest elections. Most democracies, either combine an FPTP system with natural or legislative limit on the number of competing political parties (such as in the case of UK and US) or rely on a non-FPTP system, with specific vote thresholds to enter Parliament. The combination of an FPTP system along with a system that allows multiple small political parties to exist entails challenges and makes the system vulnerable to some structural policy problems that are often overlooked. These include: A Tendency To Go All-In: An FPTP system means that at an election, the contestant with the highest number of votes is declared the winner even if the victory margin is very low. For instance, the narrowest victory margin recorded at an Indian constituency-level election is a mere 9 votes! Such a system where the winner takes all, irrespective of the victory margin, creates perverse incentives for contesting candidates to go all-in on populism ahead of elections. Indian elections have thus seen candidates offer everything from food and free laptops, to free alcohol and hard cash, in a bid to woo voters in the run up to elections. Too Many Players Can Spoil The Election: An FPTP system alongside a multi-party system can lead to very high degrees of political competition. While competition is usually a virtue, very high levels of political competition tend to fragment the electorate. Owing to these reasons, political competition in India tends to be very high in general. For instance, the last two general elections in India saw 15 candidates contest from each constituency on average. This compares to an average number of contestants from each constituency being 5 for UK or 6 for Canada. The problem with this fragmentation is that the victorious politician may lack a strong popular mandate. Smaller Indian states bear the brunt of this problem. The smaller the state, the cost of the pre-election campaign is lower, so the number of contestants shoots up in smaller regions (Chart 4).

Chart 4

Rent-Seeking Becomes A Necessity: Such a system which combines FPTP and no major entry barriers for contestants arguably encourages rent-seeking behavior, which election winners frequently display. Populist spending promised by candidates to lure voters ahead of elections can be very high, especially when political competition is stiff. Winners then are keen to recover this “sunk cost” and to create a war chest for the next election. This prompts the rent-seeking that often becomes a necessity for candidates who run expensive election campaigns. To conclude, few emerging market peers have a sustained track record of democracy like India does. Russia and others have long histories of both political instability and one-man rule. Brazil, Turkey, Thailand, South Korea, Taiwan, and Indonesia have all experienced stints of military rule and revolutions in the post-WWII era. Whilst India’s political stability credentials are solid, the existence of high degrees of political competition alongside high degrees of social complexity will spawn both structural and cyclical policy risks in India. Navigating India’s Political Peculiarities It is heuristically convenient to assume that policy risks in India are uniform across time. However, in this report, we highlight that policy risks for India hardly tend to be the same through the five-year term of a political party in charge at the national level. The five-year term of any central government in India is paved with cyclical policy risks. The good news is that there is a method to the madness. We present a simple method to identify a “pattern” to the cyclical policy risks: We break down India’s general election cycle into a five-year sequence. Year 1 is defined as the year after a general election takes place (such as 2020) and Year 5 is defined as the year in which a general election takes place (such as 2019 or 2024). (See the Appendix for a quick overview of India’s political system.) Given that India has 28 states and a state government’s term lasts five years, about six state elections are held each year. After identifying this five-year sequence, we then identify specific states that become due for state elections during this five-year period. Such a characterization of India’s election cycle shows how the five-year period from one election to the other is hardly the same. In fact, it becomes clear how policy risks tend to be definitively elevated in the years leading up to a general election. Year 3 in such a framework sees elections in some of India’s largest states (size), India’s politically most sensitive states (sensitivity), and India’s socially most complex states (complexity). 2022 will mark the beginning of Year 3 of the current five-year cycle and will see: Size: The most loaded state election schedule which will affect more than a quarter of India’s population (Chart 5). Sensitivity: Elections take place in most of India’s northern region (Chart 6), which is a key constituency for the ruling Bhartiya Janata Party (BJP).

Chart 5

Chart 6

Complexity: Elections take place in some of the most socially conflict-prone states such as say Manipur (Chart 7). Year 3 of India’s cycle is also worth bracing for as it typically sees the policy machinery’s attention shift away from big-ticket reform to populism. This is probably because Year 4 sees some of the poorest states in India undergo elections (Chart 8) and then Year 5 sees a general election.

Chart 7

Chart 8

What becomes clear now is that India is set to enter the business-end of its five-year election cycle in 2022. So, what specific policy changes should investors expect? The Road To Elections … Is Paved With Policy Risks Irrespective of the political party in power at the centre, populism as a theme tends to become more defined in the two years leading to a general election in India. For instance, history suggests that government spending in the two years leading up to a general election tends to be higher than in the previous three years (Chart 9). The last time this theme did not play out was in the run up to the elections of 2014 when in fact the incumbent i.e., the Indian National Congress (INC) lost elections to the Bhartiya Janata Party (BJP). Distinct from the fiscal support to the economy that tends to rise in the run up to elections, it is notable that even money supply growth, inflation to an extent and even the pace of Rupee depreciation tends to be faster in India in the years leading up to a general election (Chart 10).

Chart 9

Chart 10

The run up to Year 3 and Year 4 of India’s election cycle also tends to see the announcement of voter-friendly policies that may not necessarily be market-friendly. Examples of this phenomenon include: Record Increase In Revenue Spends Ahead Of 1999 General Elections: In 1998 the-then Finance Minister oversaw a whopping 20% year-on-year increase in revenue expenditure. This is almost double the average growth rate of 13% seen in this metric over the last 25 years. Farm-loan Waiver Ahead of 2009 General Elections: In 2008 i.e., the year before the general elections of 2009, the Indian National Congress (INC)-led central government announced its decision to write off farm loans of about $15 billion (in inflation-adjusted terms today). Demonetization Decision Ahead Of 2017 Uttar Pradesh State Elections: The BJP-led central government announced its decision to demonetize 86% of currency in circulation in November 2016 in a bid to prove the government’s commitment to crackdown on black money. GST Rate Cuts Ahead Of 2017 Gujarat State Elections: The Goods and Services Tax (GST) council announced a cut in the GST rate for over 150 items in November 2017. This was ahead of Gujarat state elections that were due in December 2017. Such decisions are known to work with voters. The incumbent political party that announced these policy decisions, in each of the three cases cited above, won the elections that they subsequently contested. Just last week, the Indian Government decided to repeal farm sector reform related laws which it had announced a year ago. It is not entirely coincidental that this pro-voter decision has been announced just a few months ahead of critical state elections due in 2022. Key State Elections To Watch In 2022

Chart 11

State elections are due in seven states in India in 2022. State elections due in 2022 will have an indelible impact on India’s policy outlook for 2022 because the BJP is the incumbent party in most of these states and BJP’s popularity has suffered because of the pandemic (Chart 11). The government’s decision last week to roll back farm sector reform is a great example of this phenomenon. Of all the state elections due in 2022, the two key elections that will have the biggest bearing on the 2024 general elections will be the elections in Uttar Pradesh in February 2022 and in Gujarat in December 2022. BJP’s popularity in these states should be closely watched to get a better sense of the 2024 general election outcome. The BJP won about 80% of the cumulative seats these two states offer at the 2019 general elections. At the last state elections held in Uttar Pradesh in 2017, the BJP stormed into power in the state, winning 77% of seats. BJP’s entry into power there was symbolic as the road to New Delhi is said to pass through this state (Chart 12). Gujarat on the other hand has been a BJP stronghold and PM Modi began his political innings as the chief minister of this state. Despite being in power in Gujarat for over two decades, the BJP managed to retain power in this state at the last elections held in 2017 (Chart 13).

Chart 12

Chart 13

Accurate pre-poll data for these states will be available only closer to election day. Our early on-ground checks suggest that the BJP is set to almost certainly retain power in Uttar Pradesh in 2022. However, the BJP runs the risk of losing some vote share in Gujarat owing to the anti-incumbency effect it faces and owing to the rise of parties like the Aam Aadmi Party (AAP) in the state of Gujarat. Another tool that can be used to estimate the likely result of these two key state elections is the economic growth momentum in these states. State election results from 2021 suggest that this macro variable matters a great deal. While it is not the only variable that matters, the incumbent lost elections in large states in 2021 when growth decelerated excessively (Chart 14). For instance, in 2021, Tamil Nadu saw its GDP growth decelerate significantly but West Bengal saw its GDP growth decelerate by a lesser extent. Notably, the incumbent was displaced out of power in Tamil Nadu but managed to retain power in West Bengal possibly because of several factors including a lesser slowdown in economic growth (Chart 14). If GDP growth were to affect election outcomes in 2022 as well then, the incumbent i.e., the BJP, will comfortably retain power in Uttar Pradesh but may have to deal with the risk of losing some vote share in Gujarat. This is because economic growth accelerated in Uttar Pradesh over the last five years before the pandemic. GDP growth rates remained high in Gujarat but the pace of acceleration was weaker (Chart 15).

Chart 14

Chart 15

However, from the perspective of the general elections of 2024, BJP’s position in these two states remains fairly strong, and this is true even if it experiences minor setbacks in the upcoming state elections. National parties like the BJP tend to enjoy greater fervor amongst voters in general elections as opposed to state elections. It hence would take an earthquake defeat in these state elections to alter this assumption – an outcome which appears unlikely at this stage. The takeaway from the above is that investors must brace for the BJP pursuing populist policies over the next two years. In fact, we are increasingly convinced that the BJP government’s budget for FY23 (due to be announced on 1 February 2022) will see a marked increase in transfer payments for farmers in specific or low-income groups in general. The announcement of a brand-new program aimed at lifting incomes of India’s lowest economic strata cannot be ruled out. But from the perspective of the 2024 elections, the BJP appears well-placed to retain power. Investors will face negative policy turbulence in the short run but should maintain a base case of policy continuity over the long run. Investment Conclusions If You Are Playing A Long Game, Then Hold: From a strategic perspective, we remain Buyers of India. India’s democratic traditions will lend political stability as the country’s economic heft grows. Its democratic credentials will also yield geopolitical advantages as America aims to create an axis of democracies to contain autocratic regimes. It is notable that the US’s most recent alliance-formation efforts - such as the Quadrilateral Security Dialogue or the AUKUS nuclear submarine deal - involve some of the oldest democracies of the world. As India sheds its historical stance of neutrality, in favor of closer alignment with the US against China, its democratic credentials will help India deepen its engagement with geopolitically powerful democracies. If You Are Playing A Short Game, Then Fold: The Indian market appears priced for perfection today. We recommend paring exposure to Indian assets on a tactical time horizon. Historically India’s premium relative to emerging markets has shown some correlation with the BJP’s popularity (Chart 16). However, India’s premium relative to EMs has shot through the roof over the last year and hence even if BJP wins the Uttar Pradesh elections (our base case), then it is unclear if that victory will drive another bout of price-to-earnings re-rating for India. Moreover, as outlined, the road to state elections in 2022 will be paved with policy risks as the government prioritizes populism ahead of pro-market reform.

Chart 16

The BJP has managed to expand its influence in India over the last decade (Chart 17). But a unique problem now confronts Indian policymakers: while stock markets in India have risen almost vertically, wage inflation has collapsed (Chart 18). Additionally, India has administered a weak post-pandemic fiscal stimulus (Chart 19). We reckon that this fiscal restraint will be tested in the run up to key elections in 2022-23.

Chart 17

Chart 18

Chart 19

Unlike in developed economies, where fiscal stimulus is seen as pro-market because it suggests policymaking is improving and deflationary risks will be dispelled, fiscal stimulus can be market-negative in the context of an EM like India. Increases in populist spending can end up adding to existent inflationary pressures and hence can drive bond yields higher. Stock market earnings too may not end up getting a major boost on the back of increase in transfer payments to low-income groups. This is because the share of market cap accounted for by sectors which directly benefit from pro-poor spending, like Consumer Staples, has been drifting lower on Indian bourses from 10.8% in 2013 to 8.9% today. As we have been highlighting, distinct from policy risks that confront India on a tactical horizon, geopolitical risks confronting India are elevated too. Dangerous transitions are underway to India’s west (involving Pakistan and Afghanistan) as well as east (involving China). While China’s woes drive EM investors to India, any clashes with neighbors will create much better entry points into Indian stocks. Ritika Mankar, CFA Editor/Strategist ritika.mankar@bcaresearch.com Appendix: An Overview Of India’s Political System India follows a parliamentary model of democracy with a federal structure where the government at the centre as well as state level is elected for a period of five years. The central government of India is formed through general elections that are held every five years. Power is held by a political party (or a coalition of parties) that can secure and maintain a simple majority in the Lower House (or Lok Sabha) through this five-year term. India also constitutes 28 states, each with its own legislative assembly. Each state government is formed through a state election held every five years. Much like at the centre, power is held by a political party that can maintain a simple majority at the legislative assembly for this five-year term.

Highlights Japan’s long-term weaknesses – a shrinking population, low productivity growth, excess indebtedness – are very well known. However, it still punches above its weight in the realm of geopolitics. Abenomics – sorry, Kishidanomics – can still deliver some positive surprises every now and then. As the global pandemic wanes, and China faces a historic confluence of internal and external risks, investors should begin buying the yen on weakness. Japanese industrials also are an attractive play in a global portfolio. While the yen will likely fare better than the dollar over the next 6-9 months, it will lag other procyclical currencies. Feature Japan has always been an “earthquake society,” in which things seem never to change until suddenly everything changes at once. The good news for investors is that that change occurred in 2011 and the latest political events reinforce policy continuity. Why “Abenomics” Remains The Playbook Over ten years have passed since Japan suffered a triple crisis of earthquake, tsunami, and nuclear meltdown. In fact, the Fukushima nuclear crisis merely punctuated a long accumulation of national malaise: the country had suffered two “Lost Decades” and was in the thrall of the Great Recession, a rare period of domestic political change, and a rise in national security fears over a newly assertive China. The nuclear meltdown marked the nadir. The result of all these crises was a miniature policy revolution in 2012 – Prime Minister Shinzo Abe and the Liberal Democratic Party (LDP) returned to power and initiated a range of bolder policies to whip the country’s deflationary mindset and reboot its foreign and trade relations. The new economic program, “Abenomics,” consisted of easy money, soft budgets, and pro-growth reforms. It succeeded in changing Japan. Both private debt and inflation, which had fallen during the lost decades, bottomed after the 2011 crisis and began to rise under Abe (Chart 1). By the 2019 House of Councillors election, however, Abe was running out of steam. Consumption tax hikes, the US-China trade war, and COVID-19 thwarted his plans of national revival. In particular, Abe hoped to capitalize on excitement over the 2020 Tokyo Olympics to hold a popular referendum on revising the constitution. Constitutional revision is necessary to legitimize the Self-Defense Forces and thus make Japan a “normal” nation again, i.e. one that can maintain armed forces. But the global pandemic interrupted. Until the next heavyweight prime minister comes along, Japan will relapse into its old pattern of a “revolving door” of prime ministers who come and go quickly. For example, the only purpose of Abe’s immediate successor, Yoshihide Suga, was to tie off loose ends and oversee the Olympics before passing the baton (Chart 2). Chart 1Abenomics Was Making Progress

Abenomics Was Making Progress

Abenomics Was Making Progress

Chart 2

The next few Japanese prime ministers will almost inevitably lack Abe’s twin supermajority in parliament, which was exceptional in modern history (Chart 3). It will be hard for the LDP to expand its regional grip given that it holds a majority in all 11 of the regional blocks in which the political parties contend for seats based on their proportion of the popular vote (Table 1).

Chart 3

Table 1LDP+ Komeito Regional Performance

Japan: Foreign Threats, Domestic Reflation

Japan: Foreign Threats, Domestic Reflation

Short-lived, traditional prime ministers will not be able to create a superior vision for Japan and will largely follow in Abe’s footsteps. In September Prime Minister Fumio Kishida replaced Suga – a badly needed facelift for the ruling Liberal Democrats ahead of the October 31 election. The LDP retained its single-party majority in the Diet, so Kishida is off to a tolerable start (Chart 4). But he is far from charismatic and will not last long if he fumbles in the upper house elections in July 2022. This gives him a little more than half a year to make a mark.

Chart 4

Kishida will oversee a roughly 30-40 trillion yen stimulus package, or supplemental budget, by the end of this year. Japanese stimulus packages are almost always over-promised and under-delivered. However, given the electoral calendar, he will put together a large package that will not disappoint financial markets. His other goal will be to build on recent American efforts to cobble together a coalition of democracies to counter China and Russia. Japan’s Grand Strategy In Brief Chart 5Japan Exposed To China Trade

Japan Exposed To China Trade

Japan Exposed To China Trade

Japan’s grand strategy over centuries consists of maintaining its independence from foreign powers, controlling its strategic geographic approaches to prevent invasion, and stopping any single power from dominating the eastern side of the Eurasian landmass. Originally the hardest part of this grand strategy was that it required establishing unitary political control over the far-flung Japanese archipelago. However, since the Meiji Restoration, Tokyo has maintained centralized government. Since then Japan has focused on controlling its strategic approaches and maintaining a balance among the Asian powers. During the imperialist period it tried to achieve these objectives on its own. After World War II, the United States became critical to Japan’s grand strategy. Through its broad alliance with Washington, Tokyo can maintain independence, make sure critical territories are not hostile (e.g. Taiwan and South Korea), and deter neighboring threats (North Korea, China, Russia). It can at least try to maintain a balance of power in Eurasia. Yet these constant national interests underscore Japan’s growing vulnerabilities today: China’s economy is now two-times larger than Japan’s and Japan is more dependent on China’s trade than vice versa (Chart 5). Under Xi Jinping, Beijing is actively converting its wealth into military and strategic capabilities that threaten Japan’s security. Rising tensions across the Taiwan Strait are fueling nationalism and re-armament in Japan. Russia’s post-Soviet resurgence entails an ever-closer Russo-Chinese partnership. It also entails Russian conflicts with the US that periodically upset any attempts at Russo-Japanese détente. North Korea’s asymmetric war capabilities and nuclearization pose another security threat. South Korea’s attempts to engage with the North and China, and compete with Japan, are unhelpful. All of these realities drive Japan closer to the United States. Even the US is increasingly unpredictable, though not yet to the point of causing serious doubts about the alliance. If the US were fundamentally weakened, or abandoned the alliance, Japan would either have to adopt nuclear weapons or accommodate itself to Chinese hegemony to meet its grand strategy. Nuclearization would be the more likely avenue. The stability of Asia depends greatly on American arbitration. Japan’s Strategy Since 1990 Beneath this grand strategy Japan’s ruling elites must pursue a more particular strategy suited to its immediate time and place. Ever since Japan’s working population and property bubble peaked in the early 1990s, the country’s relative economic heft has declined. To maintain stability and security, the central government in Tokyo has had to take on a very active role in the economy and society. The first step was to stabilize the domestic economy despite collapsing potential growth. This has been achieved through a public debt supercycle (Chart 6). Unorthodox monetary and fiscal policy largely stabilized demand, at the cost of the world’s highest net debt-to-GDP ratio. The economic adjustment was spread out over a long period of time so as to prevent a massive social and political backlash. Unemployment peaked in 2009 at 5.5% and never rose above this level. The ruling elite and the Liberal Democrats maintained control of institutions and government. The second step was to ensure continued alliance with the United States. Japan could deal with its economic problems – and the rise of China – if it maintained access to US consumers and protection from the US military. To maintain the alliance required making investments in the American economy, in US-led global institutions, and cooperating with the US on various initiatives, including controversial foreign policies. As in the 1950s-60s, Japan would bulk up its Self-Defense Forces to share the burden of global security with the United States, despite the US-written constitution’s prohibition on keeping armed forces. The third step was to invest abroad and put Japan’s excess savings to work, developing materials and export markets abroad while employing foreign workers and factories to become Japan’s new industrial base in lieu of the shrinking Japanese workforce (Chart 7). Chart 6Japan's Public Debt Supercycle

Japan's Public Debt Supercycle

Japan's Public Debt Supercycle

Chart 7

Japan’s post-1990 strategy has staying power because of the massive pressures on Japan listed above: China’s rise, Russo-Chinese partnership, North Korean threats, and American distractions. Investors tend to underrate the impact of these trends on Japan. Unless they fundamentally change, Japan’s strategy will remain intact regardless of prime minister or even ruling party. Russia’s role is less clear and could serve as a harbinger of any future change. President Vladimir Putin and Abe had the best chance in modern memory to resolve the two countries’ territorial disputes, build on mutual interests, and maybe even sign a peace treaty. But Russia’s clash with the West proved an insurmountable obstacle. New opportunities could emerge at some later juncture, as Japan’s interest in preventing China from dominating Eurasia gives it a strong reason to normalize ties with Russia. Russia will at some point worry about overdependency on China. But this change is not on the immediate horizon. Japan’s Tactics Since 2011

Chart 8

Japan is nearly a one-party state. Brief spells of opposition rule, in 1993 and 2009-11, are exceptions that prove the rule. The Liberal Democrats did not fall from power so much as suffer a short “time out” to reflect on their mistakes before voters put them right back into power. However, these timeouts have been important in forcing the ruling party to adjust its tactics for changing times, as with Abenomics. Kishida will not have enough political capital to change direction. The emphasis will still be on defeating deflation and rekindling animal spirits and corporate borrowing (as opposed to relying exclusively on public debt). Kishida has talked about a new type of capitalism and a more active redistribution of wealth, in keeping with the current zeitgeist among the global elite. However, Japan lacks the impetus for dramatic change. Wealth inequality is not extreme and political polarization is non-existent (Chart 8). The LDP is wary of losing votes to the populist Japan Innovation Party, or other regional movements, but populism does not have as fertile ground in countries with low inequality. The desire to boost wages was a central plank of Abenomics (Chart 9) and an area of success. It will come through in Kishida’s policies as well. But the ultimate outcome will depend on how tight the labor market gets in the upcoming economic cycle. Similarly Kishida can be expected to encourage, or at least not roll back, women’s participation in the labor force, as labor markets tighten (Chart 10). As the pandemic wanes it is also likely that he will reignite Abe’s loose immigration policy, which saw the number of foreign workers triple between 2010 and 2020. This inflow is perhaps the surest sign of any that insular and xenophobic Japan is changing with the times to meet its economic needs. Chart 9Kishidanomics To Build On Abe's Wage Growth

Kishidanomics To Build On Abe's Wage Growth

Kishidanomics To Build On Abe's Wage Growth

Chart 10Women Off To Work But Fertility ##br##Relapsed

Women Off To Work But Fertility Relapsed

Women Off To Work But Fertility Relapsed

The only substantial difference between Kishidanomics and Abenomics is that Abe compromised his reflationary fiscal efforts by insisting on going forward with periodic hikes to the consumption tax. Kishida is under no such expectation. Instead he is operating in a global political and geopolitical context in which ambitious public investments are positively encouraged even at the expense of larger budget deficits (Chart 11). Yet interest rates are still low enough to make such investments cheaply. The stage is set for fiscal largesse. Chart 11Fiscal Largesse To Continue

Fiscal Largesse To Continue

Fiscal Largesse To Continue

Kishida can be expected to promote large new investments in supply-chain resilience, renewable energy, and military rearmament. The US and EU may exempt climate policies from traditional budget accounting – Japan may do the same. Even more so than China and Europe, Japan has a national interest in renewable energy since it is almost entirely dependent on foreign imports for its fossil fuels. The green transition in Japan is lagging that of Germany but the Japanese shift away from nuclear power has gone even faster, creating an import dependency that needs to be addressed for strategic reasons (Chart 12). Monetary-fiscal coordination began under Abe and can increase under Kishida. What is clear is that public investment is the top priority while fiscal consolidation is not. Military spending is finally starting to edge up as a share of GDP, as noted above. For many years Japanese leaders talked about military spending but it remained steady at 1% of GDP. Now, at the onset of the US-China cold war, the Japanese are spending more and say the ratio will rise to 2% of GDP (Chart 13). Tensions with China, especially over Taiwan, will continue to drive this shift, though North Korea’s weapons progress is not negligible.

Chart 12

Chart 13

The Biden administration is prioritizing US allies and the competition with China, which makes the Japanese alliance top of mind. Tokyo’s various attempts to talk with Beijing in recent years have amounted to nothing, with the exception of the Regional Comprehensive Economic Partnership, which is far from ratification and implementation. Japan’s relations with China are driven by interests, not passing attitudes and emotions. If Biden proves too dovish toward China – a big “if” – then it will be Japan pushing the US to take a more hawkish line rather than vice versa. Japan will take various strategic, economic, technological, and military actions to defend itself from the range of external threats it faces. These actions will intimidate and provoke China and other neighbors, which will help to entrench the “security dilemma” between the US and China and their allies. For example, Japan will eagerly participate in US efforts to upgrade its military and its regional alliances and partnerships, including via the Quadrilateral Security Dialogue with India and Australia. The Biden administration might force Japan to play nice with South Korea and patch up their trade war. But that is a price Japan can pay since American involvement also precludes any shift by South Korea fully into China’s camp. If China should invade Taiwan – which we cannot rule out over the long run – Japan’s vital supply lines and national security would fall under permanent jeopardy. Japan would have an interest in defending Taiwan but its willingness to war with China may depend on the US response. However, both Japan and the US would have to draw a stark line in defense of Japanese territory, not least Okinawa, where US troops are based. Both powers would mobilize and seek to impose a strategic containment policy around China at that point. Until The Next Earthquake … For Japan to abandon its post-1990 strategy, it would need to see a series of shocks to domestic and international politics. If China’s economy collapsed, Korea unified, or the US abandoned the Asia Pacific region, then Tokyo would have to reassess its strategy. Until then the status quo will prevail. At home Japan would need to see a split within the Liberal Democrats, or a permanent break between the LDP and their junior partner Komeito, combined with a single, consolidated, and electorally viable opposition party and a charismatic opposition leader. This kind of change would follow from major exogenous shocks. Today it is nowhere in sight – the last two shocks, in 2011 and 2020, reinforced the LDP regime. Theoretically some future Japanese government could adopt a socialist platform that relies entirely on public debt rather than trying to reboot private debt. It could openly embrace debt monetization and modern monetary theory rather than trying to raise taxes periodically to maintain the appearance of fiscal rectitude. But if it tried to distance itself from the United States and improve relations with Russia and China, such a strategy would not go very far. It would jeopardize Japan’s grand strategy. For the foreseeable future, Japan’s economic security and national security lie in maintaining the American alliance and continuing an outward investment strategy focused on emerging markets other than China. Macroeconomic Developments The key message from an economic context is that fiscal stimulus is likely to be larger in Japan than the market currently expects. The IMF is penciling in a fiscal deficit of around 2% of potential GDP next year, which will be a drag on growth (Chart 14). More likely, Kishida will cobble together a slightly larger package to implement most of the initiatives he has proposed on the campaign trail. Meanwhile, a large share of JGBs are about to mature over the next couple of years, providing room for more issuance, which the BoJ will be happy to assimilate (Chart 15). Chart 14More Fiscal Stimulus In Japan Likely

More Fiscal Stimulus In Japan Likely

More Fiscal Stimulus In Japan Likely

Chart 15Lots Of JGBs Mature In The Next Few Years

Lots Of JGBs Mature In The Next Few Years

Lots Of JGBs Mature In The Next Few Years