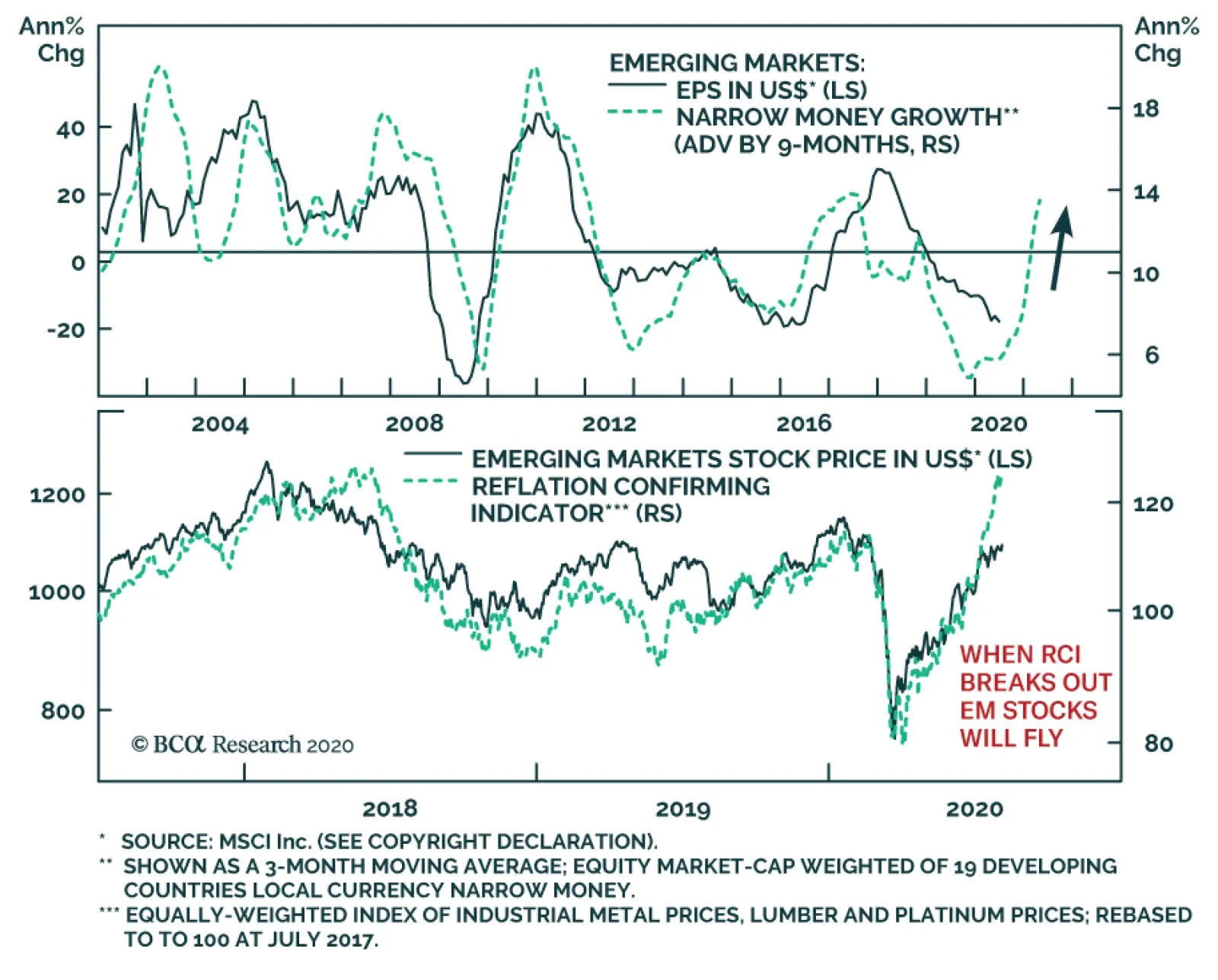

Emerging Markets

Dear Client, In lieu of our regular report next week, we are sending you a Special Report from my colleague Chester Ntonifor, Foreign Exchange Strategist. Chester will share his outlook on the Hong Kong Dollar. I hope you will find his report insightful. Please note that next week’s report will be published on Friday, August 21. Best regards, Jing Sima, China Strategist Highlights President Trump's ban of China-based apps marks a new front in the Sino-US tech war. There is no change in our strategic views. The impact on both China’s aggregate economic growth outlook and the financial markets should be limited on a cyclical basis. Consider overweight Chinese offshore ex-TMT stocks and onshore semiconductor stocks within a global equity portfolio, against a backdrop of escalating hostilities in the tech sphere. Feature Chart 1Five Chinese Companies Are Mentioned In The New "Clean Network" Initiative

Five Chinese Companies Are Mentioned In The New "Clean Network" Initiative

Five Chinese Companies Are Mentioned In The New "Clean Network" Initiative

Geopolitical risks again stirred up volatility last week in China’s equity markets. President Trump issued two executive orders to take effect in 45 days, banning US transactions with the Chinese-owned social media apps TikTok and WeChat. Shares in Tencent, the China-based Internet giant that owns WeChat, have plummeted by 11% in China’s offshore market following the ban announcement (Chart 1). The event underscores that technology is at the root of a power struggle between the US and China. The struggle will likely be exploited by Trump as the US presidential election nears and Trump’s polling numbers lag. However, we remain constructive on Chinese stocks over the next 6 to 12 months. Although the latest development remains highly fluid, the tensions should not have a material impact on the cyclical outlook for China’s aggregate economy or financial markets. This will be the case as long as the situation does not degenerate into an outright tariff increase on Chinese export goods or other strategic actions with the potential to cause major economic damage. Given rising downside risks to Chinese tech company stocks in the near term, we recommend investors hold a neutral position on Chinese tech giant company equities versus their global peers. Instead, investors should overweight Chinese “old economy” stocks as well as sectors that are greatly benefited from policy support. We initiate two trades today: long MSCI China ex-TMT versus MSCI Global ex-TMT;1 and long domestic semiconductor stocks versus global semiconductor benchmark. A New Front In Tech War It is likely that the US will implement the ordered bans in some way. Banning TikTok wasn’t a surprise because the US had amply signaled its displeasure with the app in preceding months. The social media company has rapidly gained US market share and hence access to American users’ data. Its parent company ByteDance is based in Beijing and therefore subject to China’s cybersecurity laws, a major source of bilateral tensions. The company originated in a Chinese acquisition of an American company, another irritant for the Trump administration. The US is now pressuring TikTok’s US operations to sell the app to an American-based company such as Microsoft. Regarding Trump’s executive order on WeChat and Tencent, it is not clear what “transactions” with Tencent will be disallowed from the US market.2 Additionally, US officials later appeared to backpedal and limit the scope of the executive order on Tencent to only the WeChat app. We have a few preliminary observations on the evolving situation: It is unknown how far the executive action will go regarding Tencent. The Internet titan gets less than 5% of its revenues from outside China, according to its 2019 financial statement. However, Tencent has many prominent investments in the US gaming and music industries. The US Commerce Department has 45 days to interpret and enforce the directive. The vague language in the executive order provides the US with enough legal space to deprive Tencent of US technologies in those sectors, and would severely curtail Tencent’s online gaming business, which is its main engine of growth. The bans underscore the US administration’s intention to extend tech hostilities with China by denying Chinese tech companies the access to compete and expand globally. Last week, Secretary of State Mike Pompeo announced a five-pronged “Clean Network” initiative that would scrub Chinese companies from US telecommunications networks entirely.3 China, for its part, has been progressively banning US social media giants since 2009. China has not announced any retaliatory actions since the executive orders were issued. Top Chinese policymakers seem to have shifted gears from a tit-for-tat retaliation to a carefully calibrated diplomatic reaction that does not ramp up tensions further. Moreover, there is a sizeable contingent of top Chinese policymakers pushing for reconciliation with the US. We think that China’s senior leaders prefer to dial down the current conflict and take a wait-and-see approach until after the US presidential election in November. Nevertheless, the next two to three months will be unpredictable as the election nears and Trump’s polling numbers lag behind his rival Joe Biden. Bottom Line: China’s leading Internet and tech companies are embroiled in a US-China feud. Pressures will likely intensify with other tech companies potentially also targeted. For now, stay neutral on leading Chinese tech company stocks within a global equity portfolio. Stick With The Knowns Chinese tech company stock prices will likely be extremely volatile in the short run. Nevertheless, we are staying the course with our constructive cyclical view on overall Chinese stocks and we do not recommend any one-way bets on the market during the next two to three months. China’s financial markets have been shaken by negative surprises relating to frictions with the US. However, investors cheer on even the slightest easing of tensions between the two countries. Last Friday’s volatile trading was a good example: initial confusion over the ban’s scope in Trump’s order led to a more than 10% plunge in Tencent stock during morning trading in the Hong Kong market, but the losses were cut in half after the US indicated the ban only affected the WeChat app. Chart 2Chinese Tech Company Stocks Rallied Through Most Of The Trade War

Chinese Tech Company Stocks Rallied Through Most Of The Trade War

Chinese Tech Company Stocks Rallied Through Most Of The Trade War

Economic policy support from the Chinese government and “national team” can also distort the short-term price trend in tech equities. These stocks have risen by more than 20% in both the onshore and offshore markets since the beginning of 2018, despite the deteriorating US-China relationship (Chart 2). While we are neutral on tech company stocks, we recommend overweight Chinese “old economy” stocks and remain constructive on domestic sectors that are beneficiaries of government policy support. We are initiating two trades: long MSCI China ex-TMT versus MSCI Global ex-TMT; and long domestic semiconductor stocks versus global semiconductor benchmark. The reflationary efforts since early this year facilitated a strong rebound in China’s industrial sector activities and profits (Chart 3). In turn, China’s ex-tech "old economy" stocks have outperformed relative to their global peers. Even though the handful of tech titans account for roughly 35% of the investable market capitalizations, MSCI China stock prices excluding tech titans have decisively broken out of their 200-day moving average, which suggests there is still sufficient support to our constructive view on the overall investable index (Chart 4). Chart 3Investors Have Been Focusing On China's Stimulus And Economic Recovery

Investors Have Been Focusing On China's Stimulus And Economic Recovery

Investors Have Been Focusing On China's Stimulus And Economic Recovery

Chart 4Chinese "Old Economy" Stocks Have Prevailed Of Late

Chinese "Old Economy" Stocks Have Prevailed Of Late

Chinese "Old Economy" Stocks Have Prevailed Of Late

Our cyclical overweight view on China’s domestic stocks also remains unchanged. The domestic market is much more sensitive to the trend in monetary conditions, credit growth and economic cycles than the investable market. As we pointed out in last week’s report,4 monetary conditions are accommodative and credit and economic growth remain in an uptrend. This underscores that China’s domestic stocks have more upside potential than investable stocks, even in an escalating geopolitical risk environment. Chart 5Chinese Semis Are On Fire

Chinese Semis Are On Fire

Chinese Semis Are On Fire

Lastly, more pressure from the US and the West to curb the advancement of Chinese technology will only encourage the leadership to double down on supporting state-led technology programs. This argues for a more bullish view on Chinese tech companies that focus on the domestic market, at least on a cyclical basis (Chart 5). Last week the State Council updated its policy, supporting two strategically important sectors: integrated circuits and software. The central government has had policies in place to support these two sectors since 2000 and updates its support policies every decade or so. Last week's updated version will allow chip companies to enjoy even more tax exemptions and favorable financing than the first set of support policies. China has clearly stepped up its promotion of self-sufficiency and redoubled its efforts to thwart any pressures meant to restrain its technological progress. As pointed out by our Geopolitical Strategy team,5 the U.S. and its allies control 95% of the global semiconductor market (Chart 6). Nonetheless, China is the world’s largest importer, accounting for about one-third of global semiconductor sales, making it the largest consumer of semiconductors (Chart 7). Chart 6China’s Chip Makers Are Still Small Fry

Sticking With Chinese “Old Economy” Stocks In A Widening Tech War

Sticking With Chinese “Old Economy” Stocks In A Widening Tech War

Chart 7China Accounts For 60% Of Global Semiconductor Demand

Sticking With Chinese “Old Economy” Stocks In A Widening Tech War

Sticking With Chinese “Old Economy” Stocks In A Widening Tech War

Chart 8Made In China 2025 Targets

Sticking With Chinese “Old Economy” Stocks In A Widening Tech War

Sticking With Chinese “Old Economy” Stocks In A Widening Tech War

In brief, China relies a lot on imported semiconductors and is working to mitigate this dangerous vulnerability. The Made in China 2025 program estimates that China will produce 70% of its demand for integrated circuits by 2030 (Chart 8). Bottom Line: China’s domestic industrial sector will continue to recover in the next 6 to 12 months. The nation’s semiconductor industry will get a boost from recently shored-up government policy supports. Overweight these sectors in the face of expanding tensions from the US tech war against China. Jing Sima China Strategist jings@bcaresearch.com Footnotes 1TMT stocks include information technology prior to December 2018, and include media & entertainment and internet & direct marketing retail sectors after December 2018. 2Please see the orders: https://www.whitehouse.gov/presidential-actions/executive-order-addressing-threat-posed-tiktok/ and https://www.whitehouse.gov/presidential-actions/executive-order-addressing-threat-posed-wechat/ 3https://www.state.gov/announcing-the-expansion-of-the-clean-network-to-safeguard-americas-assets/ 4Please see China Investment Strategy Weekly Report "China Macro And Market Review," dated August 5, 2020, available at cis.bcaresearch.com 5Please see China Investment Strategy Special Report "U.S.-China: The Tech War And Reform Agenda," dated December 12, 2018, available at cis.bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

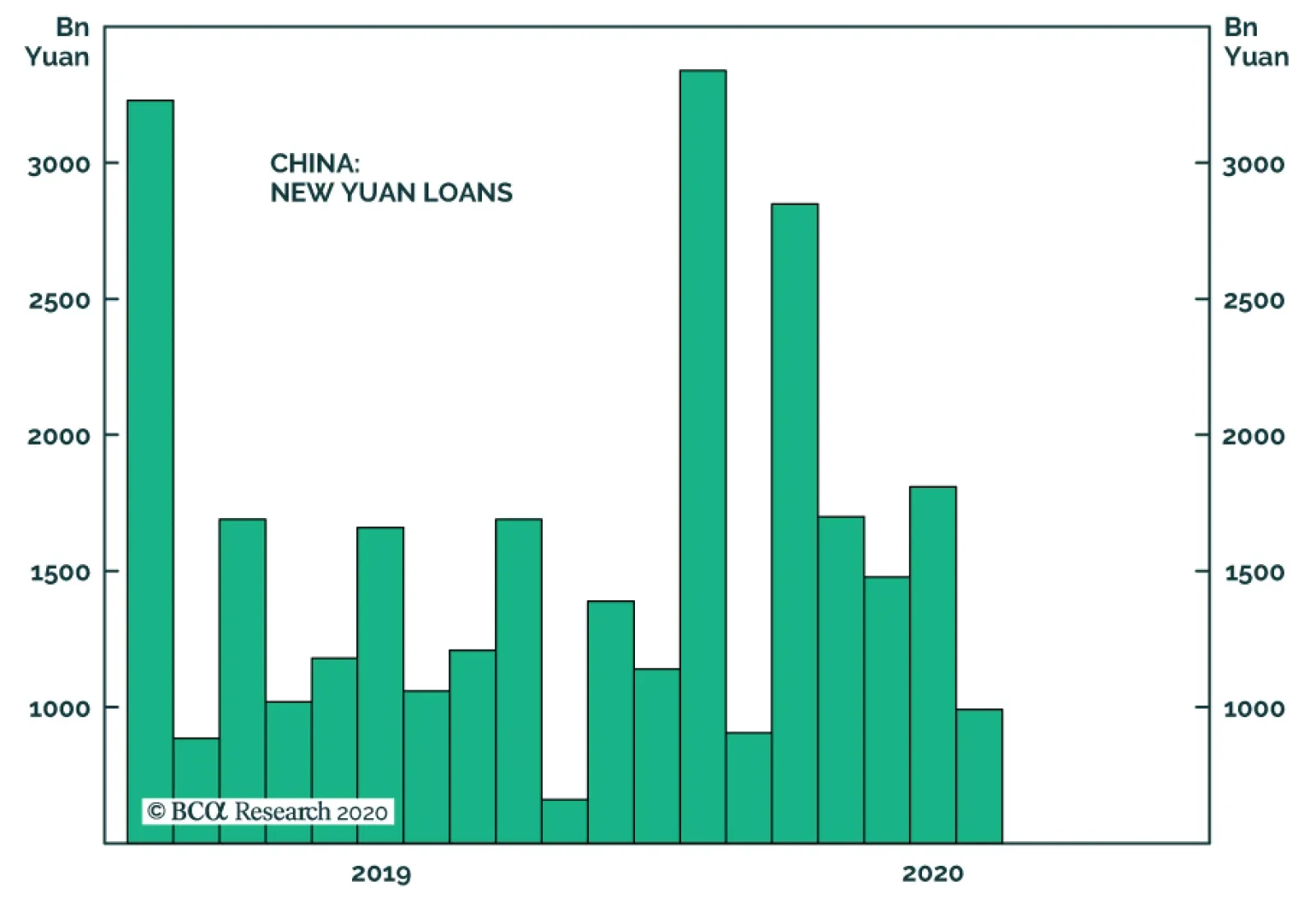

New Yuan loans in China came in at only CNY 992.7 billion in July, well below levels seen since policymakers opened the stimulus floodgates in March. However, it would be premature to suggest that this dip in lending signals a shift toward a more…

The biggest developments overnight Sunday were geopolitical. President Donald Trump signed an executive order to provide more relief to Americans. Then China fired a new salvo in the geopolitical war with the US. In a nutshell, both parties are aggressively…

China’s trade data for July released last Friday was mixed. On the positive front, export growth in USD terms accelerated to 7.2% from 0.5% as economic re-opening among trade partners continues to boost the demand from Chinese goods. Exports to the US,…

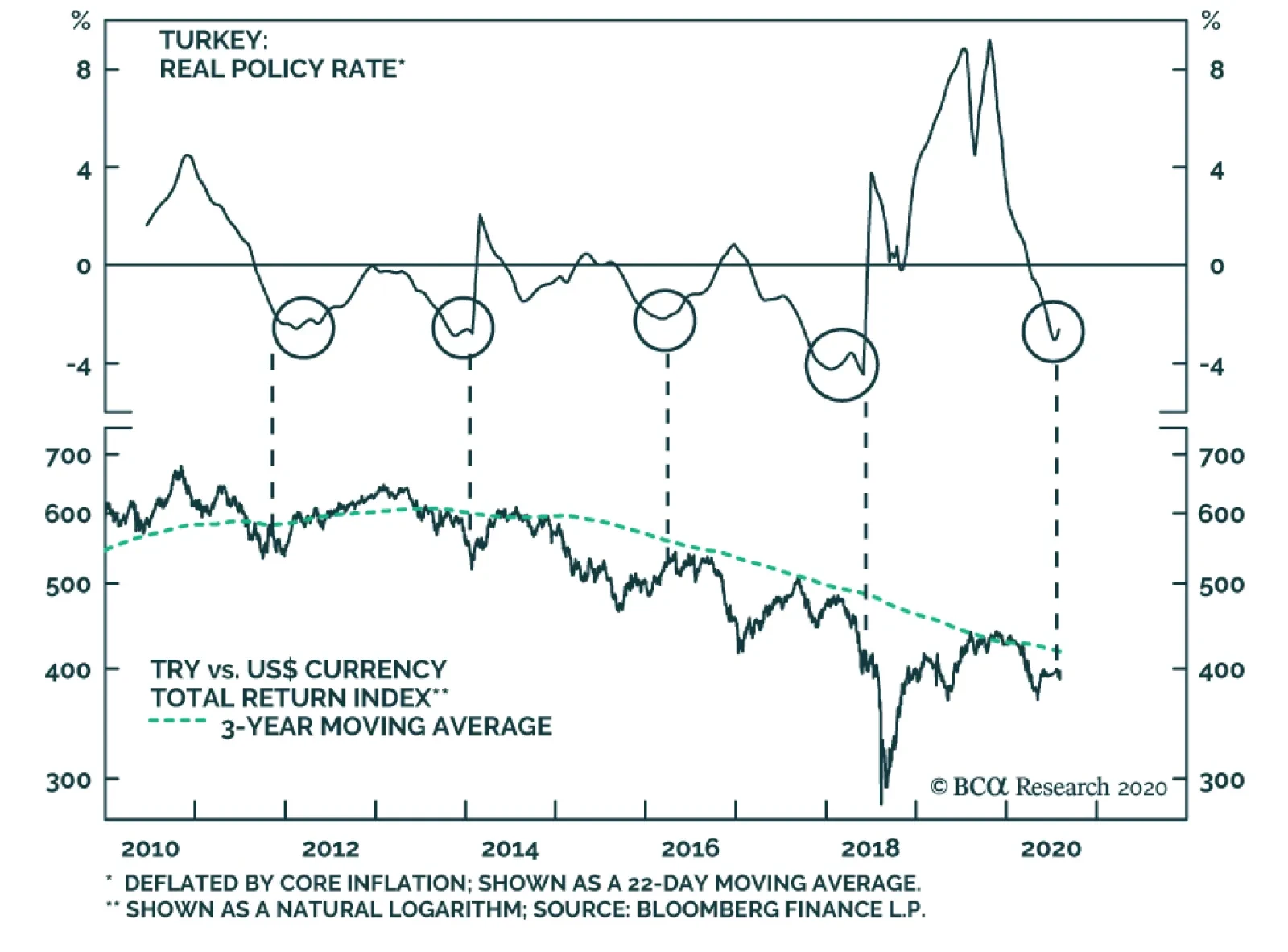

Even after the recent selloff in the TRY, BCA Research's Emerging Markets Strategy service remains negative on Turkish stocks, local currency bonds and credit markets relative to their EM counterparts. Turkey is facing another currency turmoil. At the core…

China: The Recovery And Equity Dichotomy China’s economic recovery has been gathering steam, and policymakers have become reasonably confident about the growth outlook. In fact, transaction activity in the property market has recovered to year-ago levels, auto sales and construction starts have bottomed following a 18 to 20-month contraction (Chart I-1). In line with this economic revival, authorities issued a statement following last week’s Politburo meeting contending that monetary policy should aim “to maintain adequate growth of money supply and credit.” This statement is a change in the monetary policy stance in May when the stated objective was to “significantly accelerate the growth rate of broad money supply and total social financing relative to last year.” This change in language highlights that authorities have become more comfortable with the recovery and are now becoming a bit concerned about amplifying credit and property market excesses. There will be no additional stimulus forthcoming, but policy tightening is not in the cards. In short, there will be no additional stimulus forthcoming, but policy tightening is not in the cards. Policymakers will therefore be in a wait-and-see mode for now, monitoring how economic conditions improve as the enacted stimulus works its way into the economy. Odds are high that the business cycle recovery will continue in China for now. Chart I-2 shows that the amount of credit and fiscal stimulus has been considerable, and that broad money and bank assets impulses remain in uptrend. All these should support the recovery into early next year. Chart I-1China: A Cyclical Recovery Is Underway

China: A Cyclical Recovery Is Underway

China: A Cyclical Recovery Is Underway

Chart I-2China: The Stimulus Will Continue Working Its Way Into Economy

China: The Stimulus Will Continue Working Its Way Into Economy

China: The Stimulus Will Continue Working Its Way Into Economy

As to the risks to Chinese growth emanating from depressed demand in the rest of the world, they are not substantial. First, global demand has already bottomed. Second, China’s total exports account for 17% of GDP, while investment expenditures and consumer spending account for 42% and 38% of GDP, respectively (Chart I-3). Hence, rising capital expenditures and household spending will offset the drag from exports. Finally, China exports many household and medical goods that are currently in very high demand worldwide due to the lockdowns and the pandemic. As a result, Chinese exports have recently done a bit better than global shipments in volume terms (Chart I-4). Chart I-3China Is Not Very Reliant On Exports

China Is Not Very Reliant On Exports

China Is Not Very Reliant On Exports

Chart I-4Chinese Exports Are Doing A Better Than Global Shipments

Chinese Exports Are Doing A Better Than Global Shipments

Chinese Exports Are Doing A Better Than Global Shipments

As to domestic growth drivers, output has been rising faster than consumer demand. Furthermore, capital spending and production by state-owned enterprises has been much stronger than that of private enterprises. However, with the stimulus in full force, both consumer demand and private investment will pick up in the second half of this year. An Equity Market Dichotomy Chart I-5Dichotomy Between Old And New Economy Stocks

Dichotomy Between Old And New Economy Stocks

Dichotomy Between Old And New Economy Stocks

On the surface, the strong rally in Chinese equity indexes has validated the economic recovery thesis. However, a closer examination of the equity performance of various equity sectors reveals that the rebound in cyclical sectors has been rather tame and that the large gains in the equity indexes have been primarily due to tech and new economy businesses, benefiting from working and shopping from home, and to health care stocks (Chart I-5). Chart I-6 illustrates that industrials, materials, autos and real estate stocks are only modestly above their March lows. More importantly, large bank stocks trading in Hong Kong are reaching new lows in absolute terms (Chart I-6, bottom panel). Chart I-6China: Cyclicals Stocks And Banks

China: Cyclicals Stocks And Banks

China: Cyclicals Stocks And Banks

Is such lackluster performance by Chinese cyclical stocks a warning sign to its business cycle recovery? Not necessarily. In our opinion, poor performance of cyclical stocks and banks in China reflects the long-term ramifications of repeated episodes of credit frenzy. A credit-driven growth recovery is always a double-edged sword for both borrowers and creditors. Companies that borrow and invest in new projects accumulate debt. Critically, it is unclear whether these investments will produce new recurring cash flows that would allow the debtors to service their debt. Hence, many companies that take on more debt and invest in financially non-viable projects undermine shareholder value. China has again doubled down on the same policies it has been deploying since the 2008 Lehman crisis. Namely, it has encouraged another boom in money and credit creation, as well as in infrastructure investment. Another outcome of this is that excess money creation leaks into the property market, further fueling the real estate bubble. As for banks, if debtors are unable to service their debt, bank shareholders will be at risk too. This does not mean that banks will be liquidated, but that their shareholders will be diluted. It is critical to put this round of stimulus into perspective: it comes amid already elevated debt levels, following a decade-long credit frenzy and a two decade-long capital spending boom (Chart I-7). Therefore, we doubt that the latest round of investments will be able to substantially increase shareholder value. On the whole, we believe the rally in Chinese stocks outside secular growth plays – such as Alibaba, Tencent – is cyclical not structural. The basis is that while more credit produces a cyclical recovery, it often undermines shareholder value. Chart I-6 on page 4 illustrates that Chinese cyclical stocks and bank share prices have been flat-to-down in the past 10 years despite recurring stimulus. Finally, the near-term risks for Chinese stocks do not stem from the domestic economy, but from geopolitics and a correction in US FAANG stocks. President Trump may escalate the confrontation with China in order to “rally the nation behind the flag” if his polling does not improve ahead of the November elections. Chart I-8 illustrates that the Americans’ view of China has deteriorated significantly in recent years. This might be exploited by President Trump to boost his re-election chances. A heightened confrontation could produce a correction in Chinese stocks. Chart I-7China Credit Excesses Are Getting Larger

China Credit Excesses Are Getting Larger

China Credit Excesses Are Getting Larger

Chart I-8Americans’ Perception Of China Has Deteriorated In Recent Years

China, Indonesia And Turkey

China, Indonesia And Turkey

Also, if the FAANG mania is either paused or reversed, then Chinese tech and mega-cap stocks will correct, pulling down the broad Chinese equity indexes. Bottom Line: The current round of stimulus in China has made the credit, money and property excesses even larger. As we have written over the years, easy money and credit generally fuel a misallocation of capital. Ultimately, this slows productivity growth on the macro level and destroys shareholder value on the company level. Small banks, not large ones, have been leading the massive money and credit boom for the past 10 years. Nevertheless, given that the cyclical recovery in China will endure for now, we continue overweighting Chinese investable stocks within an EM equity portfolio. Finally, we are closing our short CNY/long USD position given the change in our USD outlook on July 9. This position has produced a 4.2% loss since its initiation on December 9, 2015. A Stress Test For Bank Stocks Chart I-9China: Small and Medium Banks Versus Large 5 Ones

China: Small and Medium Banks Versus Large 5 Ones

China: Small and Medium Banks Versus Large 5 Ones

Small banks, not large ones, have been leading the massive money and credit boom for the past 10 years. Chart I-9 demonstrates that the risk-weighted assets of smaller banks have risen much faster, and are presently larger, than those of large banks. We have performed a new stress test for both the Big Five and small & medium listed banks. Concerning large banks, our base-case scenario calls for risk-weighted non-performing assets to rise to 13% of total. Accordingly, their equity will be diluted by 46% if they were to provision for these losses (Table I-1). Consequently, the true (adjusted) price-to-book (PBV) ratio will be 1.1. Assuming that the fair value of these large banks corresponds to a PBV ratio of one, then Big Five banks remain moderately (10%) overpriced. For small banks, our baseline scenario assumes a risk-weighted non-performing asset ratio of 13%. If these banks were to provision for these write offs, their equity will be diluted by 61%, pushing the adjusted PBV ratio to 2 (Table I-2). If we use a PBV fair value ratio of 1.3, then small and medium listed banks are substantially overpriced. Table I-1Stress Test Of 5 Large Banks

China, Indonesia And Turkey

China, Indonesia And Turkey

Table I-2Stress Test Of The Other 25 Listed Medium & Small Banks

China, Indonesia And Turkey

China, Indonesia And Turkey

Chart I-10Favor Large 5 Banks Over Small And Medium Ones

Favor Large 5 Banks Over Small And Medium Ones

Favor Large 5 Banks Over Small And Medium Ones

Bottom Line: Chinese banks stocks could rebound, but their structural outlook has deteriorated further following another round of credit binge. Among banks stocks, we reiterate our strategy of favoring large banks over smaller ones (Chart I-10). Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Lin Xiang, CFA Research Analyst linx@bcaresearch.com Indonesia: Struggling To Recover Indonesian stocks and the rupiah have rebounded in line with global risk assets. However, the rebound might be waning. The rupiah has begun weakening anew against the US dollar despite a major weakness in the latter. Relative to EM, Indonesian equities are underperforming again (Chart II-1). Chart II-1Indonesian Stocks Are Underperforming EM Again

Indonesian Stocks Are Underperforming EM Again

Indonesian Stocks Are Underperforming EM Again

Crumbling Economic Activity And Insufficient Stimulus Indonesia is experiencing its worst recession since the Asian Crisis in 1997. Consumer income has dwindled and consumer confidence collapsed (Chart II-2, top panel). In turn, passenger car and truck sales have contracted by 90% and 84%, respectively, from a year ago (Chart II-2, second and third panel). Meanwhile, domestic cement consumption plunged by 17% (Chart II-2, bottom panel). In the meantime, the Coronavirus pandemic is not subsiding and will continue weighing on the Indonesian economy. The authorities have been attempting to prop up domestic demand. Yet the total fiscal stimulus announced so far – which amounts to $48 billion or 4.3% of GDP – is unlikely to be enough, given the harsh nature of this recession. For instance, the commercial banks loan impulse has already dipped to -2.7% of GDP (Chart II-3, top panel). Provided that demand for credit stays weak and banks continue to be reluctant to lend, the credit impulse will drop even further. As a result, the negative credit impulse will offset the fiscal thrust. Chart II-2Indonesia: Domestic Demand Collapsed

Indonesia: Domestic Demand Collapsed

Indonesia: Domestic Demand Collapsed

Chart II-3Indonesia: Lending Rates Are High

Indonesia: Lending Rates Are High

Indonesia: Lending Rates Are High

On the monetary policy front, Bank Indonesia (BI) has been aggressively cutting its policy rate and injecting banking system liquidity into the market. The BI has been also purchasing government bonds on the secondary and primary markets, de facto conducting quantitative easing. Still, the ongoing monetary easing has not translated into lower lending rates for the real economy. In particular, although the BI lowered its policy rate by 200 basis points since July 2019, bank lending rates have only fallen by 100 basis points (Chart II-3, middle panel). This is a major sign that the monetary transmission mechanism is broken. Furthermore, the commercial banks’ lending rate, in real (inflation-adjusted) terms, remains elevated (Chart II-3, bottom panel). This is severely hurting credit demand (Chart II-3, top panel). The deflationary pressures on the Indonesian economy are intensifying. As a result, the deflationary pressures on the Indonesian economy are intensifying. The top panel of Chart II-4 shows that the GDP deflator is flirting with deflation. Meanwhile, both core and headline inflation have undershot the central bank’s target (Chart II-4, bottom panel). Bottom Line: Very low inflation and crumbling real growth have caused nominal GDP growth to drop below borrowing rates (Chart II-5). This is hitting borrowers’ ability to service their debt and is leading to swelling non-performing loans (NPLs). Chart II-4Indonesia Is Facing Very Low Inflation

Indonesia Is Facing Very Low Inflation

Indonesia Is Facing Very Low Inflation

Chart II-5Indonesia: Nominal GDP Growth Is Well Below Lending Rates

Indonesia: Nominal GDP Growth Is Well Below Lending Rates

Indonesia: Nominal GDP Growth Is Well Below Lending Rates

Bank Stocks Remain At Risk The outlook for bank stocks that make up 48% of the Indonesia MSCI equity index is bleak. Chart II-6 shows that non-performing loans and special-mention loans (which are composed of doubtful loans) were rising before the pandemic shock. This has forced commercial banks to boost their bad loans provisioning, which has hurt their profitability. Additionally, Indonesian commercial banks’ net interest margins (NIM) have been falling sharply (Chart II-7). This has occurred because, on the revenues side, interest earnings have mushroomed as debtors have halted their interest payments while, on the expenditures side, commercial banks were forced to keep on paying interests to depositors. To protect their profitability, commercial banks have kept their lending rates stubbornly high. However, doing so will end up backfiring – as elevated lending rates punish borrowers and end up causing NPLs to rise, leading to more profit weakness. Chart II-6Indonesia: Bad Loans Are On The Rise

Indonesia: Bad Loans Are On The Rise

Indonesia: Bad Loans Are On The Rise

Chart II-7Indonesia: Banks' Net Interest Margins Are Falling

Indonesia: Banks' Net Interest Margins Are Falling

Indonesia: Banks' Net Interest Margins Are Falling

Crucially, Bank Central Asia and Bank Rakyat – which now account for a whopping 37% of the Indonesia MSCI market cap – are vulnerable. Both commercial banks are heavily exposed to state-owned enterprises (SOE) and small and medium (SME) companies. Particularly, 40% of Bank Central Asia’s loan book is linked to SOEs and government-led projects across electricity, ports, airports and cement among other sectors. Meanwhile, 68% of Bank Rakyat’s loan book is leveraged to the SME sector and 20% to large companies, including SOEs. Worryingly, both SOEs and SMEs have been undergoing stress. Their profitability and debt servicing ability were questionable even before the COVID-19 pandemic. State-Owned Enterprises (SOEs): The debt servicing ability for these companies has deteriorated. The debt-to-EBITDA ratio has risen considerably while the EBITDA coverage of interest expenses is set to fall from already low levels (Chart II-8). Small & Medium Enterprises (SME): The debt serviceability of the top 40% of the MSCI-listed small cap stocks is also deteriorating. The top panel of Chart II-9 shows that these companies’ debt-to-EBITDA has risen substantially, and that the EBITDA-to-interest expense ratio has plunged (Chart II-9, bottom panel). Chart II-8Indonesian SOEs: Weak Debt Servicing Capacity

Indonesian SOEs: Weak Debt Servicing Capacity

Indonesian SOEs: Weak Debt Servicing Capacity

Chart II-9Indonesian SMEs: Weak Debt Servicing Capacity

Indonesian SMEs: Weak Debt Servicing Capacity

Indonesian SMEs: Weak Debt Servicing Capacity

Chart II-10Indonesia Equities: Banks, Non-Financials And Small Caps

Indonesia Equities: Banks, Non-Financials And Small Caps

Indonesia Equities: Banks, Non-Financials And Small Caps

All in all, both Bank Central Asia and Bank Rakyat are set to experience a considerable new NPL cycle emanating from the poor profitability of SOEs and SMEs. Importantly, Bank Central Asia and Bank Rakyat’s respective NPLs at 1.3% and 2.6% were relatively low at the start of this year and have much room to rise. Neither are their valuations appealing. At a price-to-book value of 4.4 Bank Central Asia is expensive. As for Bank Rakyat while its multiples are not as high as Bank Central Asia’s (which is trading at a price-to-book value of 1.8), it is not particularly cheap either, considering its enormous exposure to Indonesia’s struggling SME sector. Bottom Line: The outlook for bank stocks is murky (Chart II-10). Apart from banks, the rest of the Indonesian stock market has been performing very poorly and there is no obvious evidence that this will change (Chart II-10, bottom two panels). Investment Conclusions Continue underweighting the Indonesian stock market. Bank stocks remain at risk. Moreover, there is evidence that retail investors have been active in the stock market as of late. When the stock market does relapse, retail investors will likely rush to sell their holdings, thereby magnifying the equity selloff. Dedicated EM local currency bonds and credit portfolios should continue underweighting Indonesia. Investors in Indonesia’s corporate US dollar bonds should tread carefully as the largest issuers are those SOEs that have experienced deteriorating creditworthiness. Chart II-11Return On Capital Drives EM Currencies

Return On Capital Drives EM Currencies

Return On Capital Drives EM Currencies

If the US dollar continues to depreciate, the rupiah could stabilize and rebound but it will underperform other EM and DM currencies. Return on capital (ROC) is the ultimate driver of EM currencies. Given the magnitude of the recession Indonesia is in and the slow recovery it will experience, its ROC will remain weak. This will weigh on the rupiah (Chart II-11). We continue shorting the rupiah against an equally weighted basket of the euro, Swiss franc and Japanese yen. Ayman Kawtharani Editor/Strategist ayman@bcaresearch.com Turkey: The Ramifications Of A Money Plethora Turkey is facing another currency turmoil. At the core of significant currency depreciation pressures is an overflow of money. Chart III-1 demonstrates that narrow money (M1) and broad money (M3) are booming at 90% and 50%, respectively, from a year ago. These measures exclude foreign currency deposits. Bank loan annual growth has surged to 45% and commercial bank purchases of government bonds are skyrocketing (Chart III-2). Chart III-1Turkey's Money Overflow

Turkey's Money Overflow

Turkey's Money Overflow

Chart III-2Rampant Credit Creation By Commercial Banks

Rampant Credit Creation By Commercial Banks

Rampant Credit Creation By Commercial Banks

In turn, the Central Bank of Turkey’s (CBRT) funding of commercial banks has surged (Chart III-3). By providing ample liquidity the CBRT has enabled commercial banks to engage in a credit frenzy and levy of government debt. The latter has capped local currency bond yields at a time when the private sector and foreign investors have been reluctant to finance the government bond given its current yields. At the core of significant currency depreciation pressures is an overflow of money. Consistent with this expanding money bubble, inflation in Turkey remains in a structural uptrend (Chart III-4). Core and service sector consumer price inflation is close to 12% and will rise even further due to the overflow of money in the economy. Besides, residential property prices are already soaring, in local currency terms, as residents are fleeing from liras. Chart III-3Central Bank's Funding Of Banks

Central Bank's Funding Of Banks

Central Bank's Funding Of Banks

Chart III-4Structurally Rising Inflation

Structurally Rising Inflation

Structurally Rising Inflation

Still, the central bank refuses to acknowledge these inflationary pressures and to tighten its policy stance. Monetary authorities remain well behind the inflation curve. The policy rate, in real terms (deflated by core CPI), is -2%. In the past, when real policy rates have dropped to this level, the exchange rate has often tumbled, as in 2011, 2013, 2015 and 2018 (Chart III-5). Chart III-5Numerous Headwinds For The Lira

Numerous Headwinds For The Lira

Numerous Headwinds For The Lira

In regard to balance of payments, the current account deficit is widening again due to the plunge in exports and tourism revenues and the recovering imports (Chart III-5, bottom panel). Historically, a widening current account deficit has weighed on the currency. Lastly, the central bank is not in the position to defend the exchange rate much longer. Not only has it depleted its own reserves but it has also used up $70 billion of commercial banks deposits and entered a $55 billion foreign exchange swap. Hence, its is massively short on US dollars. Bottom Line: As part of our broader currency strategy, on July 9, we replaced our short Turkish lira versus the US dollar position with a short in TRY versus a basket of the euro, CHF and JPY. This switch has proved to be very profitable and we continue recommending it. Consequently, investors should continue underweighting Turkish stocks, local currency bonds and credit markets relative to their EM counterparts. Fixed-income investors should consider betting on higher inflation expectations, i.e. going long domestic inflation adjusted yields and shorting nominal yields. Andrija Vesic Associate Editor andrijav@bcaresearch.com Footnotes Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

The wave of COVID-19 continues to spread across EM economies, but the outlook for EM assets has improved significantly. EM equities and currencies trade at valuation levels consistent with long-term bottoms. While depressed valuations do not necessarily…

BCA Research's China Investment Strategy service concludes that a buildup in industrial inventory may temporarily slow down China’s commodity imports over the next month or two. Both the production and demand subcomponents of the PMI improved in July, but…

Highlights A buildup in industrial inventory may temporarily slow down China’s commodity imports over the next month or two. Last week’s Politburo meeting stated that policy supports will remain in place for 2H20, despite a rising policy rate. We think the policy rate normalization will not imminently reverse the credit impulse; strong bank lending growth will be sustained and fiscal support will likely accelerate through Q3. The liquidity-driven hype in Chinese equities may be waning, but improving economic fundamentals should support a continued bull run (in both absolute and relative terms) for the rest of this year. Feature July’s official PMI indicates that China's economic recovery remains two-tracked, with a rebound in the supply side outpacing demand and investment outpacing consumption. This uneven improvement in the economy may lead to some inventory buildup in July and August. Nevertheless, both production and demand have grown steadily and should continue to pick up in the rest of the year, ahead of other major economies.1 The annual mid-year Politburo meeting last week indicates that the monetary and fiscal policies will remain accommodative through the end of 2020. Chinese policymakers also emphasized the importance of reviving domestic demand and consumption in H2. While we have seen a rising interbank rate since late April, the current growth in credit should be sustained at least through Q3. Moreover, we expect fiscal spending to accelerate in H2 and boost infrastructure investment growth even higher. The authorities’ stringent regulations on equity margin lending may curb speculation in the financial markets. However, stronger economic fundamentals in the second half of 2020 bodes well for China’s equity performance, particularly for cyclical stocks on a 6-12 month time horizon. Tables 1 and 2 present key developments in China’s economic and financial market performance over the past month, and we highlight several developments below: Table 1China Macro Data Summary

China Macro And Market Review

China Macro And Market Review

Table 2China Financial Market Performance Summary

China Macro And Market Review

China Macro And Market Review

Chart 1Export Growth Has Been Beating Expectations (And Our Model)

Export Growth Has Been Beating Expectations (And Our Model)

Export Growth Has Been Beating Expectations (And Our Model)

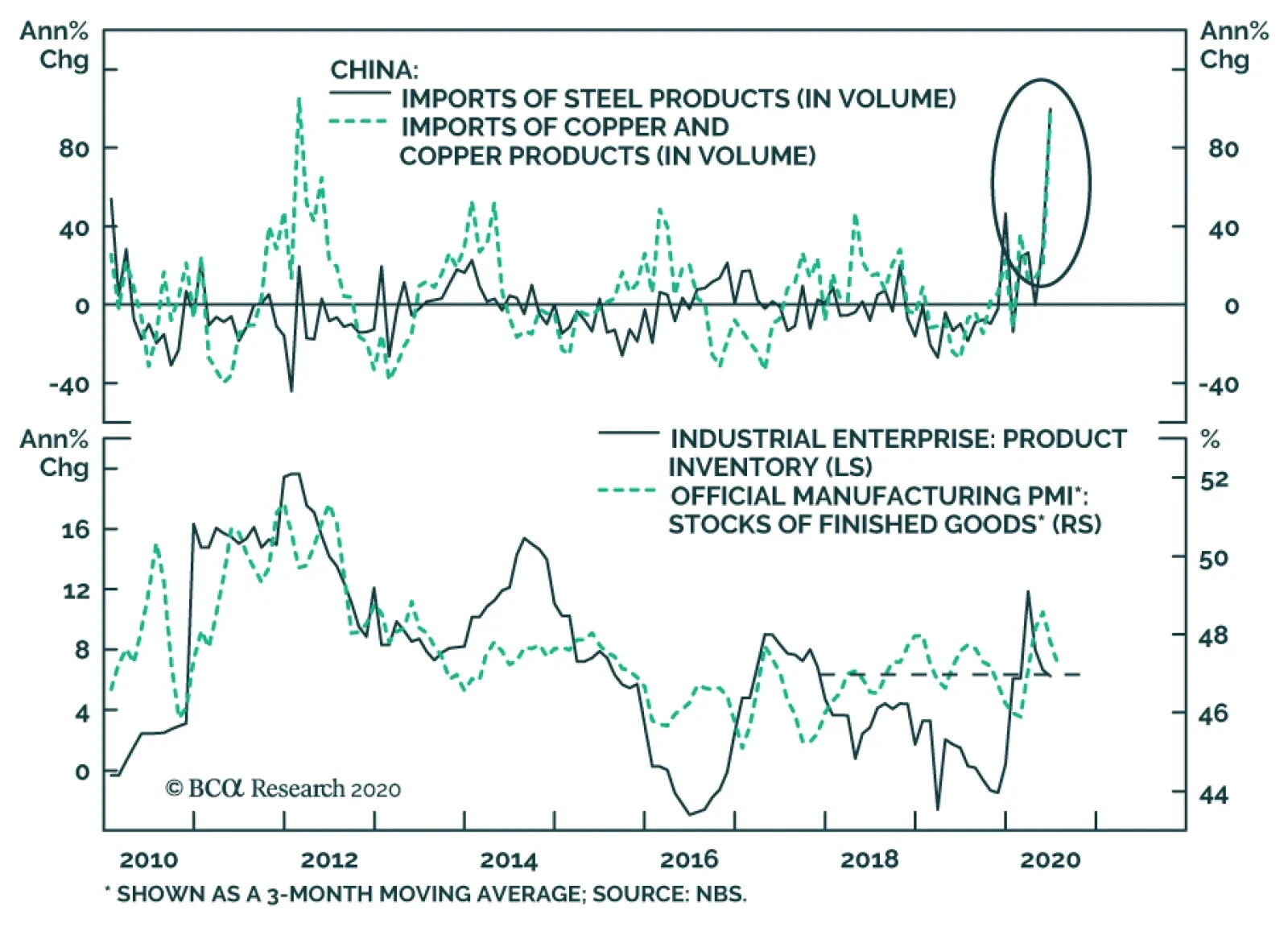

China’s official manufacturing PMI rose to 51.1 in July, beating the market consensus. The export order subcomponent of the PMI rebounded substantially last month, although it remains below the 50 percent boom-bust threshold (Chart 1). Recent high-frequency data in the US suggests that America’s economic and consumption recovery may be stalling.2 While weak economic improvement in major global economies will be a drag on external demand for consumer and capital goods, we expect that China’s export growth will continue to be supported by the pandemic-related need for medical supplies. Both the production and demand subcomponents of the PMI improved in July, but the demand side was outpaced by the supply side. This has led to a significant uptick in the finished-goods inventory subcomponent, which is the first advance in four months (Chart 2). The acceleration in post-lockdown construction activity in Q2 and exceptionally low commodity prices have driven up China’s imports of major commodities, such as steel, copper and crude oil. In turn, industrial inventories remained at their highest levels since late 2017 (Chart 3). This suggests that an inventory destocking and delay in construction activity in the flood-stricken southern part of China may hold back commodity import growth in August and possibly September. Chart 2Faster Production Rebound Leads To A Pickup In Inventory

Faster Production Rebound Leads To A Pickup In Inventory

Faster Production Rebound Leads To A Pickup In Inventory

Chart 3High Product Inventories May Curb Commodity Imports In Q3

High Product Inventories May Curb Commodity Imports In Q3

High Product Inventories May Curb Commodity Imports In Q3

Chart 4Chinese Demand For Commodities Remains Strong

Chinese Demand For Commodities Remains Strong

Chinese Demand For Commodities Remains Strong

Despite this, any moderation in China’s imports should be temporary. Industrial profit growth sprung back sharply in June. Rejuvenated growth in China’s industrial profits is crucial for fixed-asset investment and demand for durable goods, which would allow imports of commodities to remain robust in most of H2 this year (Chart 4). Statements from the mid-year Politburo meeting highlighted that “monetary policy will be more flexible and targeted in 2H20; and that the PBoC will focus on guiding the loan primary rate (LPR) lower to reduce financing costs for enterprises, particularly to the manufacturing sector and the SMEs.” Since late April, the 3-month SHIBOR (the de facto policy rate) has been rising, though it remains at a historic low. Our take is that the authorities intend to normalize liquidity conditions in the interbank system, at least for the time being, to curb financial institutions’ speculative activities (Chart 5). Even though the rising policy rate has pushed up both government and corporate bond yields, it does not necessarily lead to an imminent tightening in credit growth. Instead, we expect bank lending and fiscal spending to accelerate. Even if the 3-month SHIBOR decisively bottomed in April, the momentum in credit growth should continue through Q3 and possibly peak in October (Chart 6). Our view is based on the following: Chart 5Policymakers May Be Trying To Curb "Animal Spirits"...

Policymakers May Be Trying To Curb "Animal Spirits"...

Policymakers May Be Trying To Curb "Animal Spirits"...

Chart 6...Without Stopping Capitals From Flowing To The Real Economy

...Without Stopping Capitals From Flowing To The Real Economy

...Without Stopping Capitals From Flowing To The Real Economy

The rising policy rate and corporate bond yields do not seem to affect the amount of corporate bonds being issued. Moreover, corporate bond issuance as a share of total social financing has been flat since 2016 and remains small relative to bank lending (Chart 7, top and middle panels) On the other hand, the local government bonds’ share of total social financing has been rising since 2016 (Chart 7, middle panel). Since the amount of local government bonds issued is set at the annual National People’s Congress, a rising policy rate and bond yields have little effect on this segment of total social financing. Last week’s Politburo meeting called for local governments to speed up their special purpose bonds (SPB) issuance and complete the 3.75 trillion yuan annual quota by the end of October. The government bond issuance in July was dominated by special COVID-19 relief treasury bonds (STB), therefore, the SPB issuance will be concentrated in August to October. Based on our estimates, the average SPB issuance may reach 500 billion yuan per month in August through October, a more than 30% increase from the average monthly issuance in H1 this year. The largest share in total social financing is bank lending, which has not correlated with the policy rate since 2016 (Chart 7, bottom panel). Instead, bank loan growth and lending rates are affected by the LPR, which rate policymakers vow to guide further downwards (Chart 8). Additionally, the PBoC signaled that bank lending in 2020 is targeted at 20 trillion yuan. This leaves the second half of 2020 with a minimum of 40% of the target, or 8 trillion yuan of newly increased bank lending. To complete this annual target, according to our calculations, the growth rate of bank lending in 2H20 will need to reach at least 13% on an annual basis. This would equal to the annual growth in bank lending seen in H1. Chart 7Fiscal Support Will Accelerate

Fiscal Support Will Accelerate

Fiscal Support Will Accelerate

Chart 8Bank Loans Should Accelerate Too When Lending Rates Are Lower

Bank Loans Should Accelerate Too When Lending Rates Are Lower

Bank Loans Should Accelerate Too When Lending Rates Are Lower

China’s domestic and investable stocks dropped by 2% and 4%, respectively, from their peaks in early July, a technical correction that was mainly driven by market concerns that Chinese policymakers will withdraw stimulus too soon. China’s policymakers have indeed tightened interbank liquidity conditions and adopted more stringent measures to curb speculative behavior in the financial markets. However, we think the strong credit growth and fiscal stimulus will continue in the second half of the year, and will provide substantial support to boost China’s economic growth. As shown in Chart 9 (top panel), there has not been a steady correlation between China’s policy rate and equity performance. Rather, economic fundamentals are still the main driver for stock performance on a cyclical basis (6-12 month) (Chart 9, bottom panel). The multiples in Chinese stocks are not too elevated compared with their global peers (Chart 10A,10B, and 10C). Moreover, Chinese cyclical stocks have outperformed defensives, enhancing our cyclical bullish view on stocks in both absolute and relative terms (Chart 11). Chart 9Chinese Equity Performances Are More Correlated With Economic Fundamentals Than Policy Rate

Chinese Equity Performances Are More Correlated With Economic Fundamentals Than Policy Rate

Chinese Equity Performances Are More Correlated With Economic Fundamentals Than Policy Rate

Chart 10AChinese A Shares Are Not Too Decoupled From Economic Fundamentals

Chinese A Shares Are Not Too Decoupled From Economic Fundamentals

Chinese A Shares Are Not Too Decoupled From Economic Fundamentals

Chart 10BChinese Offshore Stocks Are More Driven By Multiple Expansions...

Chinese Offshore Stocks Are More Driven By Multiple Expansions...

Chinese Offshore Stocks Are More Driven By Multiple Expansions...

Chart 10C...But Still Not As Much As Their Global Peers

...But Still Not As Much As Their Global Peers

...But Still Not As Much As Their Global Peers

Chart 11Cyclical Stocks Are Having The Upper Hand

Cyclical Stocks Are Having The Upper Hand

Cyclical Stocks Are Having The Upper Hand

Qingyun Xu, CFA Senior Analyst qingyunx@bcaresearch.com Jing Sima China Strategist jings@bcaresearch.com Footnotes 1Please see Global Investment Strategy Outlook "Third Quarter 2020 Strategy Outlook: Navigating The Second Wave," dated June 30, 2020, available at gis.bcaresearch.com 2Please see Daily Insights "A Bumpy Recovery, But Stocks Have Room To Run," dated July 31, 2020, available at bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

Highlights Global Bond Yields: The growing divide between falling negative real bond yields and rising inflation expectations in the US and other major developed economies may be a sign of investors pricing in slower long-run potential economic growth in the aftermath of the COVID-19 recession – and, thus, lower equilibrium real interest rates. Stay overweight inflation-linked bonds versus nominal equivalents. Currency-hedged spread product: A broad ranking of currency-hedged global spread product yields, adjusted for volatility and credit quality, shows that the most attractive yields (hedged into USD, EUR, GBP and JPY) are on offer in emerging market USD-denominated investment grade corporates and high-yield company debt in the US and UK. Feature Global bond yields are testing the downside of the narrow trading ranges that have persisted since May. As of last Friday, the yield on the Bloomberg Barclays Global Treasury index was at 0.41%, only 3 basis points (bps) above the 2020 low seen back in March. The 10-year US Treasury yield closed yesterday at 0.56%, only 6bps above the year-to-date low. Chart of the Week

A Massive Shock To Growth ... And Interest Rates

A Massive Shock To Growth ... And Interest Rates

Concerns about global growth, with the number of new COVID-19 cases still surging in the US and new breakouts occurring in countries like Spain and Australia, would seem to be the logical culprit for the decline in yields. The first reads on global GDP data for the 2nd quarter released last week were historically miserable, with declines of -33% (annualized) in the US and -10% in the euro area (non-annualized). That represents a very deep hole of lost output, literally wiping out several years of growth. Even with the sharp improvements seen recently in cyclical indicators like global manufacturing PMIs, especially in China and Europe, a return to pre-pandemic levels of global economic output is many years away. Central banks will have no choice but to keep policy rates near 0% for at last the next couple of years, as is the current forward guidance provided by the Fed, ECB and others. Lower global bond yields may simply be reflecting the reality that it will take a long time to heal the economic wounds from the pandemic. However, there may be a more insidious reason why bond yields are falling. Investors may be permanently marking down their expectations for long-term potential economic growth, and equilibrium interest rates, in response to the devastation caused by the COVID-19 recession. Last week, Fitch Ratings lowered its estimates for long-term potential GDP growth, used to determine sovereign credit ratings, by 0.5 percentage points for the US (now 1.4%), 0.5 percentage points for the euro area (now 0.7%) and 0.7 percentage points in the UK (now 0.7%).1 These are declines similar in magnitude to the plunge in the OECD’s potential growth rate estimates seen after the 2009 Great Recession (Chart of the Week). Bond yields in the US and Europe witnessed a fundamental repricing in response, with nominal 5-year yields, 5-years forward breaking 200bps below the 4-6% range that prevailed in the US and Europe during the decade prior to the Great Recession. A similar re-rating of global bond yields to structurally lower levels may now be happening, with investors now believing that central banks will have difficulty raising rates much (if at all) in the future - even after the pandemic has ended. The Message From Declining Negative Real Bond Yields Chart 2The Real Rate/Breakevens Divergence Continues

The Real Rate/Breakevens Divergence Continues

The Real Rate/Breakevens Divergence Continues

The typical signals about economic growth from government bond yields are now less clear because of the aggressive policy responses to the COVID-19 crisis. 0% policy rates, dovish forward guidance on the timing of any future rate increases, large scale asset purchases (QE), and more extreme measures like yield curve control to peg bond yields, have all acted to suppress the level and volatility of nominal global bond yields. Within those calm nominal yields, however, the dynamic that has been in place since May - rising inflation breakevens and falling real bond yields – is growing in intensity. The 10-year US TIPS real yield is now at a new all-time low of -1.02%, while the 10-year TIPS breakeven is now up to 1.58%, the highest since February before the pandemic began to roil financial markets (Chart 2). Similar trends are evident in most other major developed economy bond markets, with the gap between falling real yields and widening breakevens growing at a notably faster pace in Canada and Australia. More often than not, longer-term real yields tend to move in the same direction as inflation expectations when economic growth is improving. The former responds to faster economic activity, often with an associated pick up in private sector credit demand. At the same time, rising inflation expectations discount higher economic resource utilization (i.e. lower unemployment) and confidence that inflation will start to pick up. A deeply negative correlation between longer-term real yields and inflation expectations is unusual, but not unprecedented. A deeply negative correlation between longer-term real yields and inflation expectations is unusual, but not unprecedented. In Chart 3, we show the range of rolling three-year correlations between 10-year inflation-linked (real) government bond yields and 10-year inflation breakevens in the US, Germany, France, Italy, the UK, Japan, Canada and Australia for the post-crisis period. The triangles in the chart are the latest three-year correlation, while the diamonds are a more recent measure showing the 13-week correlation. There are a few key takeaways from this chart: Chart 3Negative Real Yield/Breakevens Correlations Are Not Unprecedented

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

All countries shown have experienced a sustained period of negative correlation between real yields and inflation breakevens; The correlation has mostly been positive in Australia and has always been negative in Japan; Most importantly, the deeply negative correlations seen over the past three months – with rising breakevens all but fully offsetting falling real yields – are at or below the range of historical experience for all countries shown. Chart 4TIPS Yields May Stay Negative For Some Time

TIPS Yields May Stay Negative For Some Time

TIPS Yields May Stay Negative For Some Time

In the current virus-stricken world, where many businesses that have closed during the pandemic may never reopen, there will be abundant spare global economic capacity for several years. In the US, measures of spare capacity like the unemployment gap (the unemployment rate minus the full-employment NAIRU rate) have been a reliable leading directional indicator of the long-run correlation between real TIPS yields and TIPS breakevens over the past decade (Chart 4). The surge in US unemployment seen since the spring, which has pushed the jobless rate into double-digit territory, suggests that the current deeply negative correlation between US real yields and inflation breakevens can persist over the next 6-12 months. Given the large increases in unemployment seen in other countries, the negative correlations between real yields and inflation breakevens should also continue outside the US. As for inflation expectations, those remain correlated in the short-run to changes in oil prices and exchange rates in all countries. On that front, there is still some room for breakevens to widen to reach the fair value levels implied by our models.2 A good conceptual way to think about inflation breakevens on a more fundamental level, however, is as a “vote of confidence” in a central bank’s monetary policy stance. If investors perceive policy settings to be too tight, markets will price in slower growth and lower inflation expectations, and vice versa. Every developed market central bank is now setting policy rates near or below 0% - and promising to keep them there until at least the end of 2022. Thus, the trend of rising global inflation breakevens can continue as a reflection of very dovish central banks that will be more tolerant of increases in inflation and not tighten policy pre-emptively. Currently, real 10-year inflation-linked bond yields are below the New York Fed’s estimates of the neutral real short-term rate, or “r-star”, in the US and the UK (Chart 5), as well as in the euro area and Canada (Chart 6).3 In the US and euro area, real yields have followed the broad trend of r-star, but the gap between the two is relatively moderate with r-star estimated to be only 0.5% in the US and 0.2% in the euro zone (where the ECB is setting a negative nominal interest rate on European bank deposits at the central bank – a policy choice that the Fed has been very reluctant to consider). Chart 5Negative Real Bond Yields Are Below R* In The US & UK ...

Negative Real Bond Yields Are Below R* In The US & UK ...

Negative Real Bond Yields Are Below R* In The US & UK ...

Chart 6... As Well As In The Euro Area & Canada

... As Well As In The Euro Area & Canada

... As Well As In The Euro Area & Canada

A more interesting study is in the UK where 10yr inflation-linked Gilt yields have fallen below -2.5%, but without the Bank of England implementing any negative nominal policy rates. In the UK, inflation expectations have been relatively high – running in the 2.5-3% range prior to the COVID-19 recession – as the Bank of England has consistently kept overnight interest rates below actual CPI inflation since the 2008 financial crisis. Thus, nominal Gilt yields have stayed relatively low for longer, as real yields and inflation expectations have remained negatively correlated for a long period with the Bank of England maintaining a consistently negative real policy rate. Chart 7Spillovers From Negative TIPS Yields Into Other Assets

Spillovers From Negative TIPS Yields Into Other Assets

Spillovers From Negative TIPS Yields Into Other Assets

If the Fed were to do the same in the US, keeping the funds rate very low even as inflation rises, then a similar dynamic could take place where real TIPS yields continue to fall and TIPS breakevens continue to rise as the market prices in a sustained negative real fed funds rate. That may already be happening, with Fed Chair Jerome Powell hinting last week that the Fed is in the process of completing its inflation strategy review – with a shift towards rate hikes occurring only after realized inflation has sustainably increased to the Fed’s 2% target. A forecast of inflation heading to 2% because of falling unemployment will no longer be enough.4 Other factors may be at work depressing real bond yields while boosting inflation expectations, such as the massive QE bond buying programs of the Fed, ECB and other central banks. Yet even QE programs are essentially an aggressive form of forward guidance designed to drive down longer-term bond yields by lowering expectations of future interest rates. In sum, it is increasingly likely that the current phase of negative global real bond yields may become longer lasting if markets believe that equilibrium real policy rates are now negative. Bond investors will expect central banks to sit on their hands and do nothing in that environment, even if inflation starts to increase. This not only has implications for bond markets, but other asset classes as well based on what is happening in the US. The steady decline in the in the 10-year US TIPS yield has boosted the valuation of assets that typically have been considered inflation hedges, like equities and gold (Chart 7). The fall in TIPS yields also suggests that more weakness in the US dollar is likely to come over the next 6-12 months – another reflationary factor that should help lift global inflation expectations and boost the attractiveness of inflation-linked bonds. The current phase of negative global real bond yields may become longer lasting if markets believe that equilibrium real policy rates are now negative. Bottom Line: The growing divide between falling negative real bond yields and rising inflation expectations in the US and other major developed economies may be a sign of investors pricing in slower long-run potential economic growth in the aftermath of the COVID-19 recession – and, thus, lower equilibrium real interest rates. Stay overweight inflation-linked bonds versus nominal equivalents. Searching For Value In Global Spread Product Last week, we looked at the impact of currency hedging on the attractiveness of government bond yields across the developed markets.5 We concluded that US Treasuries still offered superior yields to most other countries’ sovereign bonds, even with the US dollar in a weakening trend and after hedging out currency risk. We also presented a cursory look at the relative attractiveness of the major global spread product categories in that report, but without factoring in any considerations on the relative credit quality or volatility between sectors. This week, we will look at the relative value of global spread products hedged into USD, GBP, EUR and JPY, but after controlling for those credit and volatility risks. We conducted a similar analysis in early 2018,6 ranking the currency-hedged yields for a wide variety of global spread products by the ratio of yields to trailing volatility. This time, instead of looking at the just that simple valuation metric, we use regression models to make a judgment on how under- or over-valued spread products are relative to their “fair value”. To recap the methodology of this analysis, we take the Bloomberg Barclays index yield-to-maturity (YTM) for each spread product category, hedged into the four currencies used in this analysis, and divide it by the annualized trailing volatility of those yields over both short-term (1-year) and long-term (3-year) windows. In order to hedge the yields into each currency, we used the annualized differentials between spot and 3-month forward exchange rates, which is the all-in cost of hedging. We then compare those currency-hedged, volatility-adjusted yields to two measures of risk: the index credit rating and duration times spread (DTS) for each spread product. Table 1 summarizes the attractiveness of each product when hedged into different currencies. The rank is based on the average of four different valuation measures.7 The higher the rank, the more attractive the sector is in terms of yield relative to risk measures such as both short-term and long-term volatilities, credit ratings, and DTS. Table 1Ranking Currency-Hedged, Risk-Adjusted Global Spread Product Yields

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

A few interesting points come from the table: Emerging market (EM) USD-denominated investment grade (IG) corporate debt ranks at or near the top of the rankings, for all currencies; the opposite holds true for EM USD-denominated sovereign bonds Almost all European spread products rank poorly for non-euro denominated investors US & UK high-yield (HY) rank highly for all currencies US real estate related assets (MBS and CMBS) also rank well for all investor groups In general, US products are more attractive than European credit sectors. This is mainly because US spread products offer higher yields than European ones even after accounting for volatility and the weakening US dollar. Almost all European spread products rank poorly for non-euro denominated investors. Chart 8 shows the unhedged YTM on the x-axis and the option-adjusted spread (OAS) on the y-axis (Table 2 contains the abbreviations used in this chart and all remaining charts in this report). Unsurprisingly, the YTM and OAS follow a very tight linear relationship. However, when yields are hedged into different currencies and risk measures are factored in, the result changes. Chart 8Global Spread Product Yields & Spreads

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Charts 9A to 12B show the details of spread product analysis with different currency hedges and risk factors. To limit the number of charts shown, we show only currency-hedged yields adjusted by long-term trailing volatility (the rankings do not change significantly when using a shorter-term volatility measure). The y-axis in all charts shows the volatility-adjusted yields, while the x-axis shows credit ratings and DTS. Sectors that are close to upper-right in each chart are more attractive (undervalued), while spread products that are close to bottom-left are less attractive (overvalued). Chart 9AGlobal Spread Product Yields, Hedged Into USD, Adjusted For Credit Quality

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 9BGlobal Spread Product Yields, Hedged Into USD, Adjusted For Duration-Times-Spread

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 10AGlobal Spread Product Yields, Hedged Into EUR, Adjusted For Credit Quality

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 10BGlobal Spread Product Yields, Hedged Into EUR, Adjusted For Duration-Times-Spread

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 11AGlobal Spread Product Yields, Hedged Into GBP, Adjusted For Credit Quality

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 11BGlobal Spread Product Yields, Hedged Into GBP, Adjusted For Duration-Times-Spread

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 12AGlobal Spread Product Yields, Hedged Into JPY, Adjusted For Credit Quality

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 12BGlobal Spread Product Yields, Hedged Into JPY, Adjusted For Duration-Times-Spread

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Table 2Global Spread Products In Our Analysis

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

An interesting result is that when comparing the three major high-yield products (US-HY, EMU-HY and UK-HY), US-HY is the most attractive in USD terms, but UK-HY is more attractive when hedged into GBP, EUR, and JPY. Another observation is that higher quality bonds such as government-related and agency debt in the US and euro area are overvalued and less attractive given how low their yields are, regardless of their low volatility. The results from this analysis may differ from our current recommendations. For example, we currently only have a neutral recommendation on EM corporates, but based on this analysis, EM corporates offer the most attractive return in USD terms. This analysis is purely based on YTM and traditional risk factors without considering other concerns that could make EM assets riskier such as the spread of COVID-19 in major EM countries. However, these rankings do line up with our major spread product call of overweighting US IG and HY corporate debt versus euro area equivalents. Based on this analysis, EM corporates offer the most attractive return in USD terms. Bottom Line: A broad ranking of currency-hedged global spread product yields, adjusted for volatility and credit quality, shows that the most attractive yields (hedged into USD, EUR, GBP and JPY) are on offer in emerging market USD-denominated investment grade corporates and high-yield company debt in the US and UK. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Ray Park, CFA Research Analyst ray@bcaresearch.com Footnotes 1https://www.fitchratings.com/research/sovereigns/coronavirus-impact-on-gdp-will-be-felt-for-years-to-come-27-07-2020 2 Please see BCA Global Fixed Income Strategy Weekly Report, "How To Play The Revival Of Global Inflation Expectations", dated June 23, 2020, available at gfis.bcaresarch.com. 3 We use the French 10-year inflation-linked bond as the proxy for the entire euro area, as this is the oldest inflation-linked bond market in the region and thus has the most data history. 4https://www.wsj.com/articles/fed-weighs-abandoning-pre-emptive-rate-moves-to-curb-inflation-11596360600?mod=hp_lead_pos6 5 Please see BCA Research Weekly Report, “What A Weaker US Dollar Means For Global Bond Investors”, dated July 28, 2020, available at gfis.bcaresarch.com. 6 Please see BCA Global Fixed Income Strategy Weekly Report, "Policymakers Are Now Selling Put Options On Volatility, Not Asset Prices", dated March 6, 2018, available at gfis.bcareseach.com. 7 Hedged YTM/Short-term trailing volatility vs. Credit Rating; Hedged YTM/Long-term trailing volatility vs. Credit Rating; Hedged YTM/Long-term trailing volatility vs. Duration; Hedged YTM/Long-term trailing volatility vs. Duration. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns