Emerging Markets

BCA Research's China Investment Strategy & Emerging Markets Strategy services recommend going long Chinese insurance stocks in absolute terms. They also recommend accumulating and overweighting Chinese healthcare stocks on a 15% correction. China’s…

Highlights China’s healthcare expenditure is projected to rise due to the increasing affluence and rapid aging of its population. The desire to access healthcare services beyond the basic coverage provided by the public health insurance will increasingly prompt people to purchase health insurance products from private insurers. We recommend going long Chinese insurance stocks in absolute terms. We also recommend accumulating and overweighting Chinese healthcare stocks on a 15% correction. Feature The aging population and the rapidly expanding middle class in China entail that healthcare expenditures will remain on a secular growth trajectory. The COVID-19 outbreak will function as a catalyst for the rapid transformation of China's healthcare system. In fact, many game changing trends in global healthcare systems will probably be attributed to the COVID-19 pandemic. Healthcare Expenditures: Still Low Health expenditures per capita in China grew substantially over the same period of time, but their level is still below those in most countries. Chart 1Chinese Healthcare Expenditure Will Grow 10% CAGR

Chinese Healthcare Expenditure Will Grow 10% CAGR

Chinese Healthcare Expenditure Will Grow 10% CAGR

Health expenditures in China have grown considerably since the economic reforms started in 1978. Between 1978 and 2018, total health expenditures in China grew at a compound annual growth rate (CAGR) of 17% in nominal terms, higher than the 15% growth in nominal GDP (Chart 1, top panel). Notwithstanding the rapid expansion of China’s healthcare market, expenditures remained at a modest 6.4% of China’s GDP in 2018 (Chart 1, bottom panel), far below the OECD average of 9%. Health expenditures per capita in China grew substantially over the same period of time, but their level is still below those in most countries. In 2017, health expenditures per capita in China were $841 in PPP (purchasing power parity) terms, ranking 92nd worldwide. Japan, by comparison, ranks 18th with $4,550, and Korea ranks 31th with $3,000, both in PPP terms (Chart 2). Chart 2China Ranks Low In Health Expenditure Per Capita Worldwide

China: Healthcare Now And Beyond

China: Healthcare Now And Beyond

Healthcare Capacity And Healthy China 2030 Chart 3China Healthcare Capacities Are Rising Fast

China Healthcare Capacities Are Rising Fast

China Healthcare Capacities Are Rising Fast

Access to adequate healthcare is crucial to social and economic development, as healthy human capital fosters productivity and economic growth. In China, healthcare capacity is still subdued. After the pandemic, authorities will divert resources to this sector to ensure it expands quickly. In 2018, the number of physicians and nurses per 1000 Chinese people was 2.6 and 2.9, respectively (Chart 3), far below the OECD average of 3.5 physicians and 8.8 nurses per 1,000 people. Hospital beds per 1000 people is 4.3 in China, compared to an average of 4.7 across OECD countries. In Japan and Korea, the measure is much higher, at 13.1 and 12.3 beds per 1,000 people, respectively (Chart 3, bottom panel). China released the Healthy China 2030 (HC 2030) blueprint in 2016, covering public health services, environmental management, the medical industry, and food and drug safety. The five specific goals of this blueprint are to improve the population’s health, control against major risks, increase the capacity of healthcare services, grow the scale of the healthcare industry, and improve the health service system generally. This program has set targets for health service capacity, including an increase in the number of doctors, nurses and beds per 1,000 people to 3, 4.7 and 6, respectively, by the year 2030. The blueprint also aims to further ease the financial burden imposed on the population by the cost of healthcare and medical treatments. Currently, in China, 29% of health costs are paid by individuals; HC 2030 recommends a reduction to 25%. We will discuss these objectives in the next section. Healthcare Financing: A Looming Funding Crunch The aging population, along with its rising income, will drive up health expenditures in the years to come. Chart 4China Elderly Population Will Rise Significantly

China Elderly Population Will Rise Significantly

China Elderly Population Will Rise Significantly

There are currently more than 167 million people over the age of 65 in China. By this measure, China is already the largest eldercare market in the world in terms of the absolute number of elderly people. What is more, China’s elderly population is growing rapidly and is expected to reach almost 200 million by 2025 (Chart 4). The aging population, along with its rising income, will drive up health expenditures in the years to come. As health expenditures grow, so will investment opportunities. Global healthcare systems can generally be classified into the three categories shown in Table 1. China’s health insurance system more closely resembles Germany’s national social health insurance system than the US commercial health insurance model. China’s healthcare system and insurance scheme is illustrated in Table 2. Table 1Overview Of Major Healthcare Systems Worldwide

China: Healthcare Now And Beyond

China: Healthcare Now And Beyond

Table 2Main Features Of China's Three Basis Social Health Insurance Schemes

China: Healthcare Now And Beyond

China: Healthcare Now And Beyond

In 2000, just over 20% of Chinese citizens had healthcare coverage. The SARS outbreak in 2003 was a wake-up call for Chinese leaders. Thanks to heavy government subsidies and political commitments, China achieved universal health insurance coverage in 2011, when nearly 95% of its 1.4 billion people had health insurance. This represents the largest and fastest expansion of insurance coverage in human history. Chart 5Individuals Health Expenditures Remain High

Individuals Health Expenditures Remain High

Individuals Health Expenditures Remain High

However, the government-sponsored health insurance plan provides for only basic coverage. Government budgetary spending accounted for 28% of total health expenditures in 2018 and the population’s out-of-pocket costs amounted to 29%, such that the remaining 43% was covered by the public social health insurance contributions (Chart 5). China’s health insurance is supervised at the national level and guided by the principle that all citizens are entitled to receive basic healthcare. Nevertheless, local governments are ultimately responsible for funding and offering these health services. This leads to unevenly distributed healthcare capacities across different provinces, as more resources are concentrated in wealthier jurisdictions. People can only receive a reimbursement for healthcare costs from their province of residence, as indicated on their hukou registration documents. Migrant urban professionals and laborers have to return to the place of their household registration to access healthcare. Chinese policy makers have been working on reforming the reimbursement system now for many years. As of the end of 2019, 3.95 million people have benefited from inter-provincial health insurance settlements. Relying heavily on local government contributions to healthcare expenditures is the primary reason why government spending on healthcare is relatively low, at only 1.7% of GDP and 7% of total general (central and local) government spending1 (Chart 6). Government expenditures on social security (which includes contributions to social health insurance, pension, unemployment and work injury insurance) make up 12% of overall government spending.1 The outbreak of COVID-19 sounded the alarm across Chinese society. Building a comprehensive and effective healthcare system with adequate capacity will become one of the most important priorities over the coming decade. The people’s well-being will be critical to social stability as its increasingly affluent population is asking for better healthcare services. Chart 6Government Spending In Healthcare

Government Spending In Healthcare

Government Spending In Healthcare

Chart 7China: A Rapidly Aging Population

China: A Rapidly Aging Population

China: A Rapidly Aging Population

However, the overall sustainability of the current healthcare financing scheme is questionable. Chart 7 shows the old age-dependency ratio, defined as the ratio of older dependents (people over the age of 64) to the working-age population (25 to 64-year old). The ratio is expected to increase from the current 19% to 30% in 2030. This means a decreasing contribution to social insurance budgets from the working population and an increase in healthcare spending on seniors. What makes the situation worse is the opacity of the National Social Security Fund (SSF). The SSF manages money reserved for pension and insurance disbursements related to medical, unemployment and injury needs for future use. Of the 2.6 trillion RMB under SSF management, at the end of 2019, over 90% are invested domestically. The fund’s average 10-year investment return is close to 6%, which is lower than the average nominal GDP growth rate of 11%, over the same period. With declining revenues from workforce contributions and rising healthcare costs, the ability of the social security system to finance proper healthcare service provisions is endangered. Furthermore, the replenishing of the SSF, so far, has depended on central government contributions and asset transfers from state-owned enterprises to the SSF. Bottom Line: As demand for healthcare services increases, the current public scheme for financing healthcare is going to be increasingly unable to cover the costs. Private Health Insurance Private health insurance offers a more extensive level of protection than the state-based coverage. Currently, most private health insurance plans provide supplementary insurance products to complement public health insurance plans. Supplementary insurance and critical illness products are the most popular because the public insurance systems cannot fully cover the cost of catastrophic illnesses. The private health insurance industry has been thriving in recent years and is expected to continue growing because of increased consumer awareness. The written premiums attributed to health insurance registered a compound annual growth rate of 36% between 2013 and 2019 (Chart 8). However, penetration into China’s health insurance market remains far behind that of more developed markets, signaling huge growth potential. One measure of insurance industry penetration is insurance depth. It is defined as the percentage of the GDP attributed to the total written premium for insurance. China’s insurance depth is currently 0.7% for health insurance and 4.2% for overall insurance (Chart 9), whereas the overall insurance depth is 11% in South Korea, 9% in Japan, and 7% in the US. Chart 8Health Insurance Premiums Are Skyrocketing

Health Insurance Premiums Are Skyrocketing

Health Insurance Premiums Are Skyrocketing

Chart 9China: Health Insurance Penetration

China: Health Insurance Penetration

China: Health Insurance Penetration

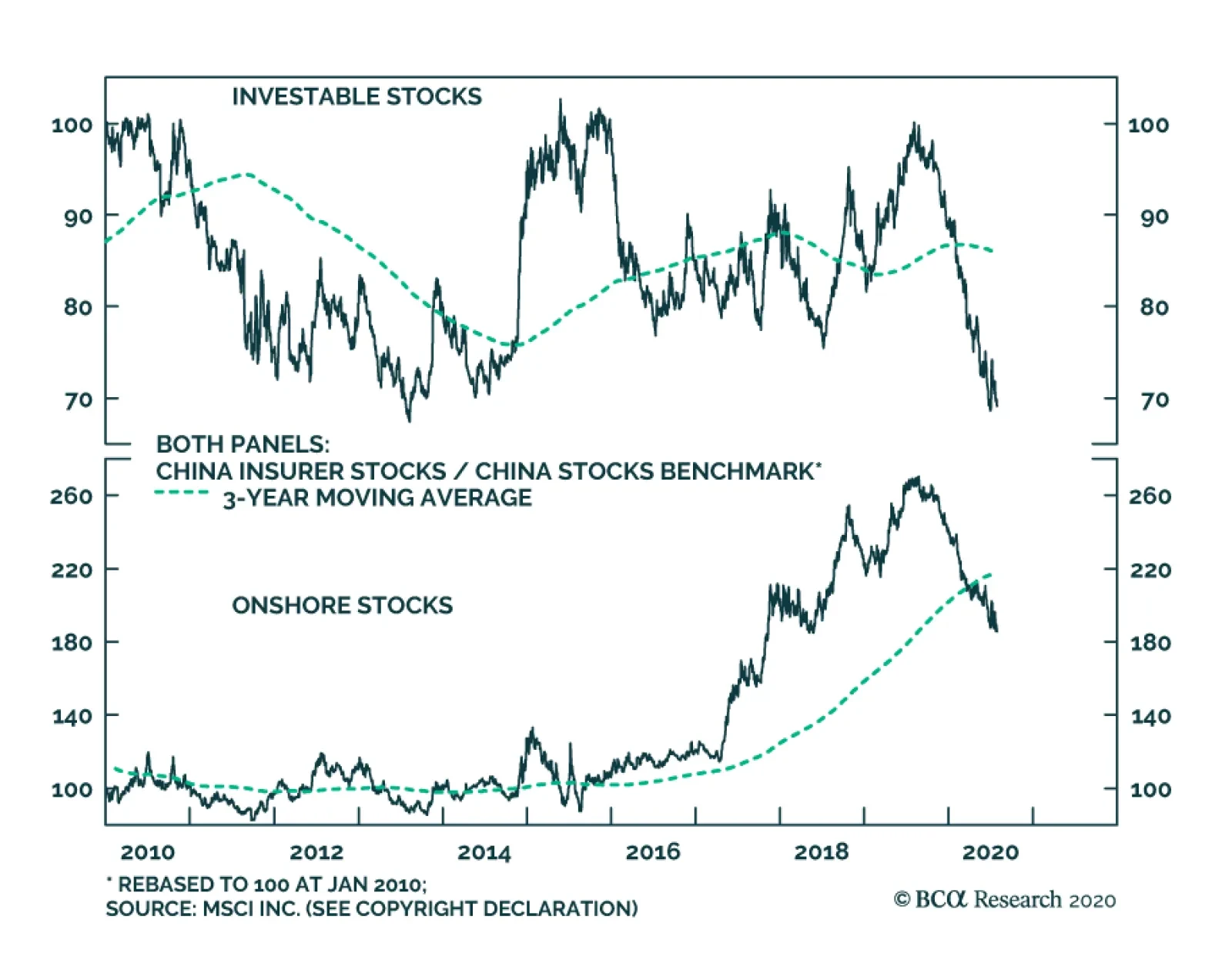

Faced with financial strains and a growing demand for healthcare services, the government is supporting private healthcare providers by relaxing regulatory restrictions and offering tax incentives to Chinese consumers when they buy health insurance. Private health insurance offers the growing middle-income class a more extensive level of protection than the state-based coverage. In regard to insurance companies’ asset management, the regulators raised the equity investment cap for all insurers earlier this month from 30% to 45% of total assets. In May of this year, regulators also allowed insurers to invest in the secondary capital bonds issued by banks, as well as in perpetual bonds. This expanded investment opportunity should help insurers diversify their investment portfolios and therefore increase the efficacy of their asset/liability management (ALM). Bottom Line: Private health insurance offers the growing middle-income class a more extensive level of protection than the state-based coverage. This underdeveloped private insurance market presents substantial opportunities. Investment Conclusions As China’s population ages, incomes rise and private healthcare services expand, investment opportunities will also increase. In short, the growth trajectory of China’s healthcare sector warrants investors’ attention. To play on this healthcare theme in China, we are initiating two strategic investment positions: First, go long Chinese insurance companies in absolute terms. Chinese insurer stocks have rallied in absolute terms since March lows, but then lagged relative to the benchmark (Chart 10 & 11); Chart 10Chinese Insurance Stocks: Rising In Absolute Terms...

Chinese Insurance Stocks: Rising In Absolute Terms...

Chinese Insurance Stocks: Rising In Absolute Terms...

Chart 11…But Underperforming The Benchmark

...But Underperforming The Benchmark

...But Underperforming The Benchmark

Double-digit CAGR of insurance premiums entails a steady asset expansion (Chart 8 on page 8). High and steady growth at a time of a low discount factor warrants high equity multiples. The private insurance industry’s gross profit margin proxy, calculated as insurance premiums minus insurance payments, divided by insurance premiums, amount to a whopping of 67%, with health insurance at 65% and life insurance at 87% (Chart 12). The equity valuations are reasonable. Unlike the tech and media sectors of the new economy, that have sky-high multiples, the trailing price to earnings ratio for insurers is still 8.8, 45% lower than the 10-year average. (Chart 13). Chart 12Chinese Insurance Companies: Outstanding Gross Profit Margins

Chinese Insurance Companies: Outstanding Gross Profit Margins

Chinese Insurance Companies: Outstanding Gross Profit Margins

Chart 13Attractive Valuations

Attractive Valuations

Attractive Valuations

Insurance company assets will be better managed going forward due to the new asset/liability management (ALM) requirements imposed by the regulators. The ALM requirements were announced in March 2018 and then fully implemented in July 2019. The rules introduced quantitative risk-adjusted measurements to help insurers more accurately capture the risk of duration mismatch, negative spread and liquidity strain. The CBIRC regularly evaluates and ranks the competence of insurers’ ALM against peers. The key risk to shareholders of insurance companies is the credit risk of their portfolio. 39% of insurance sector portfolios are invested in other investments, which include long-term equity investments, project-based debt schemes, trust plans and asset management (Chart 14). Credit risks stemming from credit claims and asset management products warrant careful investor consideration. Chart 14Investment Portfolio Of The Insurance Industry

China: Healthcare Now And Beyond

China: Healthcare Now And Beyond

Chart 15Healthcare Stocks Have Rallied Massively...

Healthcare Stocks Have Rallied Massively...

Healthcare Stocks Have Rallied Massively...

Second, accumulate Chinese healthcare stocks on a 15% correction in absolute terms (Chart 15). While we believe that healthcare stocks are in a secular bull market, they have already rallied a lot since recent lows, and they are pricing in a lot of short-term good news. Chinese investable healthcare stocks registered 55% returns since the outbreak of COVID-19. The trailing P/E ratio reached 51, a decade high since 2010 (Chart 16). We are reluctant to buy and overweight this sector now and would wait for a better entry point. Chart 16...And Are Now Too Expensive

...And Are Now Too Expensive

...And Are Now Too Expensive

Lin Xiang, CFA Research Analyst LinX@bcaresearch.com Footnotes 1Does not include quasi-fiscal (off-balance sheet) government spending.

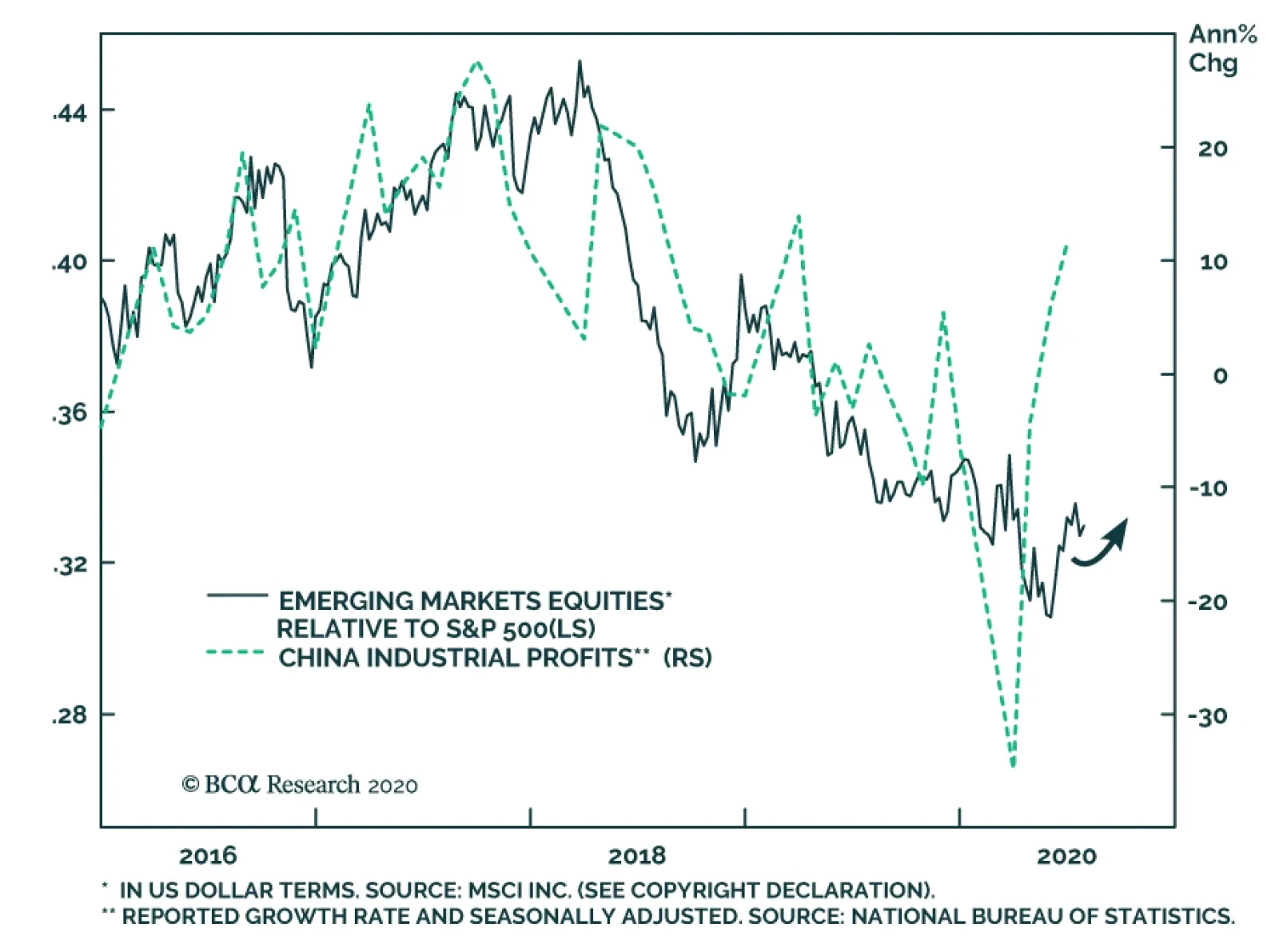

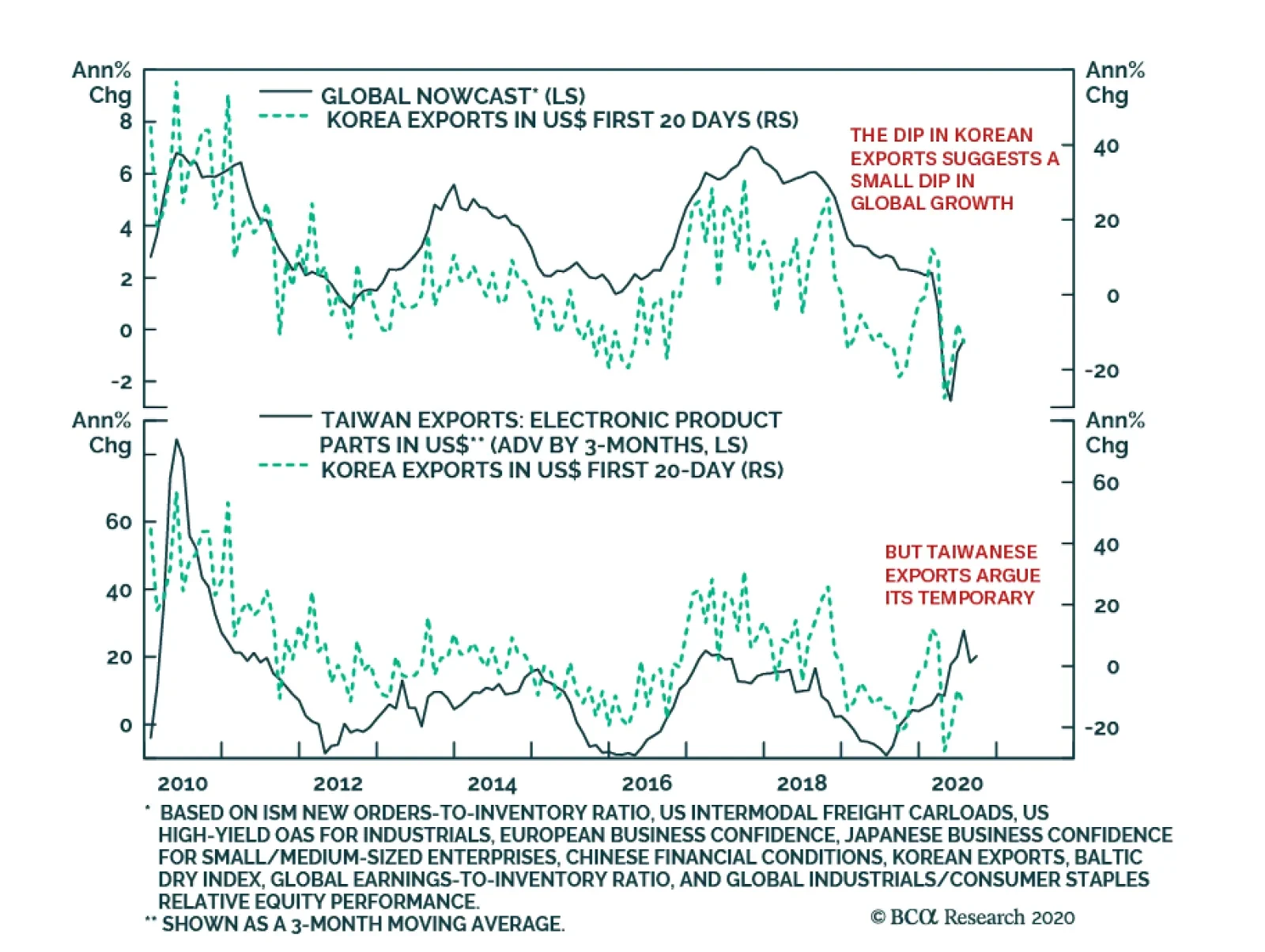

In June, China’s industrial profits growth continued to recover, rising from a 6% annual pace to an 11.5% one. For the past four and a half years, strengthening Chinese industrial profits growth aligns with an outperformance of EM equities relative to US…

Highlights The epicenter of the new Middle East crisis is the Shia Crescent, which threatens global oil supply. However, the escalation of conflict in the Mediterranean is also relevant to global investors. The crises in Libya and the Eastern Mediterranean are escalating as President Erdogan makes a last attempt to benefit from his relationship with Trump before US elections in November. A breakup between Turkey and NATO is not our base case, but European sanctions against Turkey are likely. Turkish risk will rise. A revival in Libyan oil production would not be a meaningful risk to the recovery in oil markets. Stay strategically long Brent crude oil. Libya could become a “Black Swan” for market participants exposed to southern Europe, Turkey, and North Africa. We remain short our EM Strongman Currency Basket versus other emerging market currencies. Feature Dear Clients, This week we present to you a special report on Turkey by my colleague Roukaya Ibrahim, Editor, Geopolitical Strategy. Roukaya argues that President Erdogan is at a crossroads in which he will confront major military and economic constraints to his foreign policy adventurism. On Monday, July 27 you will receive a special report that I co-wrote with Anastasios Avgeriou, chief strategist of our US Equity Strategy. In this report we continue our analysis of the equity sector implications of the upcoming US election. Anastasios also provides analysis of two cyclical sectors that you may find of interest. On Friday, July 31 we will send you our regular monthly GeoRisk Update, which surveys our proprietary, market-based geopolitical risk indicators and what they imply for your portfolio. We trust you will enjoy these reports and look forward to your feedback. All very best, Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Chart 1Shia Crescent' Flailing Under Maximum Pressure And COVID-19

Shia Crescent' Flailing Under Maximum Pressure And COVID-19

Shia Crescent' Flailing Under Maximum Pressure And COVID-19

The Middle East is suffering a wave of instability after the COVID-19 crisis just as it did in the years after the 2008 financial crisis. The crises in Libya, Syria, and Yemen were never resolved and now new crises are emerging from Egypt and Turkey to Iran and Iraq. By contrast with the “Arab Spring” of 2011, the epicenter of the political earthquake this time around is likely to be the “Shia Crescent,” i.e. Iran, Iraq, eastern Saudi Arabia, Syria, and Lebanon. The US policy of maximum pressure on Iran, which is intensifying in the lead-up to the US election, has weakened Iran and its sphere of influence (Chart 1). Chart 2Dominant Arab States Also Face Struggles

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

Meanwhile the pandemic and collapse in oil prices have destabilized the predominantly Arab states (Chart 2). Authoritarian regimes like Egypt and Saudi Arabia that consolidated power after the Arab Spring are more stable than they were but still vulnerable to external and internal forces. These cyclical developments are occurring against the backdrop of structural changes like the US’s energy independence and strategic pivot to Asia, which have created a power vacuum in the Middle East. The pivot to Asia is rooted in US grand strategy and has proceeded across partisan administrations, so it will continue. Indeed US-China tensions are escalating rapidly in 2020 despite the financial market’s lack of interest. Turkey and Russia are scrambling to take advantage of the US’s withdrawal and gain greater influence through regional proxy wars. This year has seen a marked escalation of their involvement in Libya, where the war is re-escalating and drawing in Egypt, Europe, and Gulf Arabs. At minimum a Mediterranean conflict could affect oil prices as well as Turkish, Russian, and other regional financial assets. At maximum it could affect European assets, which are exposed to geopolitical risk in Turkey and North Africa. The Shia Crescent is the crisis’s epicenter, but Libya is also investment relevant. Bottom Line: The epicenter of the new Middle East crisis is the Shia Crescent, which threatens global oil supply. However, the escalation of conflict in the Mediterranean is also relevant to global investors, primarily through its potential to impact European assets. Re-Escalation In Libya The Libyan crisis has been escalating since the beginning of the year and is on the verge of turning into a major multilateral conflict. The risk now is that Egypt, another regional power, will intervene in Libya against Turkey in a battle for North African hegemony (Map 1). Map 1Libya Could Become A "Black Swan" Event

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

Several incidents since we outlined Egypt’s red lines on the Libyan conflict suggest that Cairo and Ankara will clash in Libya (Table 1). Table 1Egypt And Turkey Up The Ante In Libya

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

While Egypt has declared Sirte and al-Jufra as red lines, threatening military intervention if crossed, Turkey is calling for the Libyan National Army’s (LNA) withdrawal from these regions as a precondition for a ceasefire (Map 2). Egypt is allied with General Khalifa Haftar’s Libyan National Army, which is based in Benghazi and holds parliament in Tobruk. Map 2Libya’s Battlefront Is Closing In On The Oil Crescent

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

The next move is now in Turkey’s hands. The escalation depends on whether it insists on moving forward toward Egypt’s red line. Turkey’s recent movements do not suggest it is backing down. True on July 21, and again on July 22, top officials from Turkey’s foreign ministry referred to a political solution as being the only solution in Libya. However, these statements were made while Turkey held diplomatic meetings with Niger and Malta that could be aimed at establishing airbases there.1 At its core, the conflict in Libya is a clash between the two dominant geopolitical forces in the Middle East. On the one hand, Turkey and Qatar are independent economic forces to Saudi Arabia and supporters of political Islam. On the other hand, Saudi Arabia, the UAE, and Egypt form an economic bloc and support Saudi religious authority and political authoritarianism. Bottom Line: The crisis in Libya is heading toward an Egypt-Turkey confrontation. Be ready for an escalation. Egypt Has More To Lose Than Turkey In Libya Both Egypt and Turkey are nearing a point of no return in Libya. A last-minute change of heart from either side would be increasingly more humiliating, both domestically and regionally. Chart 3Defeat In Libya Would Accelerate Erdogan’s Decline

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

While Egypt’s geographic proximity to Libya makes it more interested in what goes on there and will give it a home advantage in any military confrontation, Egypt’s military may be overstretched as it is also at risk of conflict with Ethiopia over water resources.2 For Egypt, a victory would resuscitate its position as a regional power, bringing about a new era of greater Egyptian regional leadership. It would silence domestic skeptics who argue Egyptian President Abdel Fattah al-Sisi’s rule is based on the illegitimate ousting of Egypt’s only democratically elected leader. It would squash any prospect of a revival of the Muslim Brotherhood in Egypt and validate authoritarian rulers in the region. It could also annul the recent Libya-Turkey maritime demarcation agreement – a positive for Egypt’s natural gas ambitions. A loss would be a wake-up call for Egypt’s military, which has been spending scarce funds on costly equipment. It may also result in a change in leadership in Egypt or at the very least weaken al-Sisi’s domestic power and Egypt’s regional clout. The regime would persist over the short and medium term, but it would suffer a loss of legitimacy and the underground domestic opposition would intensify, creating a long-term threat. A complete defeat of LNA forces would pose a major security risk. Haftar’s LNA acts as a buffer between Egypt and unfriendly militias in Western Libya. Turkey does not have a vital national strategic interest in Libya and therefore the constraint pushing against on a protracted conflict is stronger than it is for Egypt. Given that Turkey is a democracy, President Recep Tayyip Erdogan has more to lose in the case of a military defeat. It would accelerate the decline in his popular support and that of his Justice and Development Party (AKP) (Chart 3). A conflict with Egypt is therefore a gratuitous gamble. However, victory would vindicate Erdogan’s efforts to create a strongman regime and revive memories of the great Ottoman empire.3 Such an accomplishment could mark a major turning point for Erdogan. His domestic blunders would be forgiven and he would be able to claim that he is one of the great leaders of Turkey. Given that Turkey lacks strategic necessity in Libya, and a defeat could dislodge Erdogan in 2023, one should expect Turkey not to cross Egypt’s red lines. However, Erdogan’s rule has been characterized by hubris, nationalism, and foreign assertiveness to distract from domestic economic mismanagement. Therefore we cannot have a high conviction that Turkey will bow to its political and military constraints. The risk of a large conflict is underrated. Bottom Line: Egypt has greater national interests at stake in Libya than Turkey. The implication is that Turkey should recognize Egyptian red lines. However, Turkey’s decision to intervene in Libya suggests that Erdogan could overreach. Libya could become a “Black Swan” for market participants exposed to southern Europe, Turkey, and North Africa. Will Turkey Break With NATO? Since signing the maritime and military cooperation agreements with Libya on November 27, Turkey has raised its stakes in Libya. Ankara has sent more armed drones, surface-to-air missile defense systems, naval frigates, a hundred officers, and up to 3,800 Syrian fighters. It has rolled back all of the strategic gains that the Libyan National Army made in 2019. The timing of the recent escalation is significant. The US election cycle offers Erdogan a chance to increase Turkey’s foreign assertiveness with minimal US retaliation. US-Turkish relations have been icy for years. Turkey is an ascendant regional power that is pursuing an increasingly independent national policy, while the US is no longer as dominant of a global hegemonic power capable of enforcing discipline among minor allies. The US alliance with the Kurds in Syria and Iraq has alienated Turkey. The 2016 Turkish coup attempt also increased the level of distrust between the two states. However, President Trump’s personal and political affinity for President Erdogan has resulted in a permissive policy toward Turkey. Trump seeks to distance the US from conflicts in Syria and Libya inherited from his predecessor. He has little commitment to the Kurds. More broadly he has embraced geopolitical multipolarity and avoided telling Erdogan what to do. The Trump administration has not retaliated against Turkey for purchasing Russia’s S400 missile defense system or for pursuing expansive maritime-territorial claims near Cyprus. Even though the Turkish arms purchase makes it eligible for sanctions under the Countering America’s Adversaries Through Sanctions Act (CAATSA), the Trump administration has yet to impose sanctions. Senator Lindsey Graham, who is close to the Trump administration, suggested in July 2019 that sanctions could be avoided if Turkey did not activate the system.4 Turkey, for its part, has yet to activate the system three months after the April target date for activation. Turkey blames the delay on COVID-19. With regard to Libya, the Trump administration has remained largely on the sidelines. It has promised to reduce American commitment to overseas conflicts and has criticized the Obama administration’s intervention in Libya in 2011 to bail out the European allies. Officially the US is aligned with Fayez al-Sarraj’s UN-backed Government of National Accord (GNA), but so far its role has been minimal, refraining from providing any military support. Moreover, Washington’s key allies in the region – Egypt, Saudi Arabia, the UAE, even France – support the Libyan National Army. Libya could become a “Black Swan” event. It is Haftar’s other main backer – Russia – that would present an incentive for greater American involvement. The US African Command reports that two thousand Russian mercenaries from the Kremlin-backed Wagner Group have fought in Libya. The US also reported in June that at least 14 MiG29 and Su-24 Russian warplanes were sent to Libya via Syria, believed to be located in the al-Jufra airbase. Moreover, the US State Department has accused Russia of printing billions of fake Libyan dinars to fund Haftar’s forces.5 The Trump administration has been permissive toward Russia as well as Turkey, letting them work out deals with each other, but US electoral politics could prompt Trump to make shows of strength against Russia to fend off criticism. Thus the months in the lead up to the US elections offer the Turkish leader what may be a closing opportunity to increase the country’s foreign assertiveness with minimal US retribution. If Trump loses, Erdogan may face a less sympathetic Washington. By contrast France, also a NATO ally, has taken a stronger position against Ankara over its involvement in Libya. Relations with other eastern Mediterranean countries have also been rocky due to Turkey’s exclusion from gas deals in the region and drilling in disputed waters near Cyprus and Greece. France has a commercial interest in Libya’s oil industry and backs Haftar’s Libyan National Army to some extent.6 Citing aggressive behavior by Turkish warships after an encounter in the Mediterranean, France suspended its involvement in NATO’s Operation Sea Guardian on July 1.7 France has also demanded EU sanctions against Turkey – both for its drilling activities around Cyprus as well as for its role in Libya.8 Still, Europeans have little appetite for direct intervention in Libya. The leaders of France, Italy and Germany have threatened sanctions against foreign states that violate the arms embargo in Libya. This warning comes after EU foreign ministers agreed to discuss the possibility of another set of sanctions against Turkey in their August meeting if Turkey persists in converting the Hagia Sophia from a museum to a mosque. Despite the fracturing within NATO, the alliance will not break up. Turkey’s geographic proximity to Russia, large number of troops, and military strength make it an essential member of the defense treaty (Chart 4). Chart 4NATO Will Not Break With Turkey

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

Instead, the Europeans will retaliate against Erdogan’s foreign adventurism through sanctions, while maintaining the NATO alliance. This acts as a cyclical rebuke without damaging the secular relationship. Europe will use sanctions to retaliate against Turkey’s provocations. The Europeans will be particularly rattled if Turkey succeeds in its North African endeavor and amasses significant regional power as a result. Victory in Libya would make Turkey the gatekeeper to two major migrant entry points to the European continent, providing Ankara with leverage in its negotiations with Europe (Chart 5). It would also increase the likelihood that Turkey increases its assertive behavior in the Eastern Mediterranean, where Israel, Egypt, Greece, Cyprus, and Italy are seeking to develop a natural gas hub. Chart 5Turkish Victory In Libya Would Rattle Europe

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

Although Erdogan shows no signs of backing down, constraints suggest that Erdogan may pull back from being perceived as overly provocative. The Turkish economy is highly dependent on Europe in trade and capital flows (Chart 6). Thus unlike American sanctions, which have little bearing on the Turkish economy short of radical financial measures, European sanctions suppress any chance of an economic recovery. Chart 6European Sanctions Would Reverse Turkey's Recovery

European Sanctions Would Reverse Turkey's Recovery

European Sanctions Would Reverse Turkey's Recovery

Chart 7Erdogan Risks Popularity By Overstepping In Libya And East Med

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

Turkey’s frail economy and crackdown on opposition parties could weigh on Erdogan’s approval, which is losing its COVID-induced bounce (Chart 7). Thus, as in the case of Egypt, Erdogan should recognize these constraints and reduce his foreign assertiveness. If he does not, then he will hit up against material constraints that will harm the Turkish economy. Bottom Line: The Libyan crisis is escalating as Erdogan makes a last attempt to benefit from his relationship with Trump before US elections in November. Washington’s detached stance in Libya highlights that its foreign policy priorities lie elsewhere – in Asia and Iran. Meanwhile, Europe is divided over Libya. A breakup between Turkey and NATO is not our base case, but new European sanctions against Turkey are not unlikely. A Turkish victory in Libya would lead to a significant escalation in tensions between Turkey and the West. Investment Implications Turkish geopolitical risk is set to rise in the lead up to the November US elections as Turkey becomes increasingly embroiled in foreign conflicts – in Libya, Syria, Iraq, and most recently in the Azerbaijan-Armenia conflict (Chart 8). Ankara’s more provocative stances raise the risk of sanctions from the US and more significantly from the EU. This would hurt Turkish risk assets at a time of already heightened vulnerability. If Turkey manages to secure a victory in Libya, it would benefit economically from construction and energy contracts there. However, it would also result in a significant uptick in geopolitical tensions in the Middle East as the West and the West’s regional allies will be disturbed by Ankara’s expanding influence. Stay short our EM Strongman Currency Basket composed of the Turkish lira, Philippine peso, and Brazilian real versus other emerging market currencies. Even though the lira is already cheap against the US dollar, it faces more downside due to the risks highlighted in this report and the massive growth in money supply in Turkey. Similarly, the prospect of a military confrontation will raise the equity risk premium priced in Egyptian stocks. Egypt will continue underperforming emerging markets as long as it remains invested in an unsettled conflict in Libya (Chart 9). Chart 8Turkish Risk Will Rise

Turkish Risk Will Rise

Turkish Risk Will Rise

Libyan oil exports are unlikely to stage a major revival anytime soon (Chart 10). Although the Libyan National Oil Company lifted force majeure on July 10, Haftar’s Libyan National Army reintroduced the blockade a day later. Clashes are also occurring near oil facilities in the Brega region where Syrian, Sudanese, and Russian Wagner Group mercenaries currently have a presence. Chart 9Egyptian Risk Assets Will Underperform

Egyptian Risk Assets Will Underperform

Egyptian Risk Assets Will Underperform

Chart 10Libyan Oil Handicapped By Haftar’s Blockade

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

Chart 11Stay Bullish Euro Over The Long Run

Stay Bullish Euro Over The Long Run

Stay Bullish Euro Over The Long Run

Even in the best-case scenario, in which force majeure is promptly lifted, the blockade damaged both the reservoirs and oil and gas infrastructure, preventing a resurgence of exports to pre-January levels. The Libyan National Oil Company warned that unless oil production restarts immediately, output will average 650,000 barrels per day in 2022. This is significantly less than the over 1 million barrels per day just prior to the blockade, and the 2.1 million barrels per day Libya had planned to produce by 2024. In any case these figures pale in comparison to the production curtailments currently in place by OPEC 2.0, which are set to decrease to 8.3 million barrels per day beginning in August from 9.6 million barrels per day now. Given OPEC 2.0’s demonstrated commitment to production discipline, a revival in Libyan oil production is not a meaningful risk to the recovery in oil markets. We remain strategically long Brent crude oil, which is up 78% since inception in March. This trade could experience near-term volatility due to any hiccups in global economic stimulus or risk-off events from geopolitical risks. But over a 12-month time frame we expect oil prices to rise higher. BCA Research’s Commodity & Energy strategists expect Brent prices to average $44/bbl in 2H2020, and $65/bbl in 2021. The recent rise in the euro is rooted in global macro and structural factors but a major Mediterranean crisis and/or other geopolitical risks we have highlighted surrounding the US election cycle could create headwinds in the short term. Over the long run we are bullish euro (Chart 11). Roukaya Ibrahim Editor/Strategist Geopolitical Strategy RoukayaI@bcaresearch.com Footnotes 1 In Niger, Turkish Foreign Minister Mevlut Cavusoglu met with his Nigerien counterpart and stated the two states’ willingness to boost bilateral relations in agriculture, mining, energy, industry, and trade. A day earlier, Turkey and Qatar’s defense ministers met with Libya’s minister of interior in Ankara to discuss the situation in Libya. And on July 20, a trilateral meeting was held between Turkey’s defense minister, Libya’s interior minister, and Malta’s minister of home affairs and national security. The inclusion of Malta – located just north of Libya in the Mediterranean – is perplexing. The three discussed defense cooperation and efforts toward regional stability and peace. These recent meetings could suggest that Turkey is negotiating agreements to fortify its strategic approaches to Libya. This could involve greenlighting airbases in Niger and Malta in exchange for economic support and Qatari funding. 2 The latest developments suggest that the Egypt-Ethiopia conflict is de-escalating. On July 21, Ethiopian Prime Minister Abiy Ahmed tweeted that Egypt, Ethiopia and Sudan had reached a “common understanding on continuing technical discussions on filling.” But Ethiopia will have an opportunity if Egypt becomes embroiled in Libya. 3 The Turks ruled Tripolitania from the mid-1500s until Italy’s 1912 victory in the Italo-Turkish War. Surveys conducted by Metropoll reveal that the share of Turks with a positive perception of Turkey’s active role in Libya shot up to 58% in June from 35% in January. 4 Senate Majority Whip John Thune has even proposed using the US Army’s missile procurement account to buy the Russian missiles from Turkey, thus reducing tensions between the two NATO allies. This is unlikely to occur because it would look politically weak in the US, while Turkey would face Russian pressure. The US suspended Turkey from the F35 Joint Strike Fighter program, banning it from purchasing F35s, and removing it from the aircraft’s production program. US Secretary of Defense Mark Esper stated that the US would only consider allowing Turkey back into the F35 Joint Strike Program if the Russian defense system were moved out of the country. The Turkish purchase of the Russian defense system was partly driven by the need to work with Russia and partly driven by Erdogan’s desire to reduce the risk of another coup attempt. Ankara was indefensible against the Turkish Air Force’s F-16s during the 2016 coup attempt since its military relies heavily on US built missile defense. 5 Moscow has denied all allegations of involvement in Libya. 6 US-made javelin missiles purchased by France were found at the pro-Haftar base in Gharyan in June last year, raising suspicion that France was backing Haftar’s offensives. 7 On June 10, French frigate Courbet approached a Tanzanian-flagged ship heading to Libya in suspicion that it was violating the UN arms embargo. France accused three Turkish vessels that were escorting the Tanzanian vessel of harassment by targeting the Courbet’s fire control radars. Turkey denied harassing the Courbet and maintains that the Tanzanian vessel was transporting humanitarian aid to Libya. A NATO investigation into the incident was inconclusive. 8 The EU agreed to impose sanctions on two Turkish oil company officials in February in protest against Turkish drilling activity in the Eastern Mediterranean. However these sanctions are mostly just political symbolism.

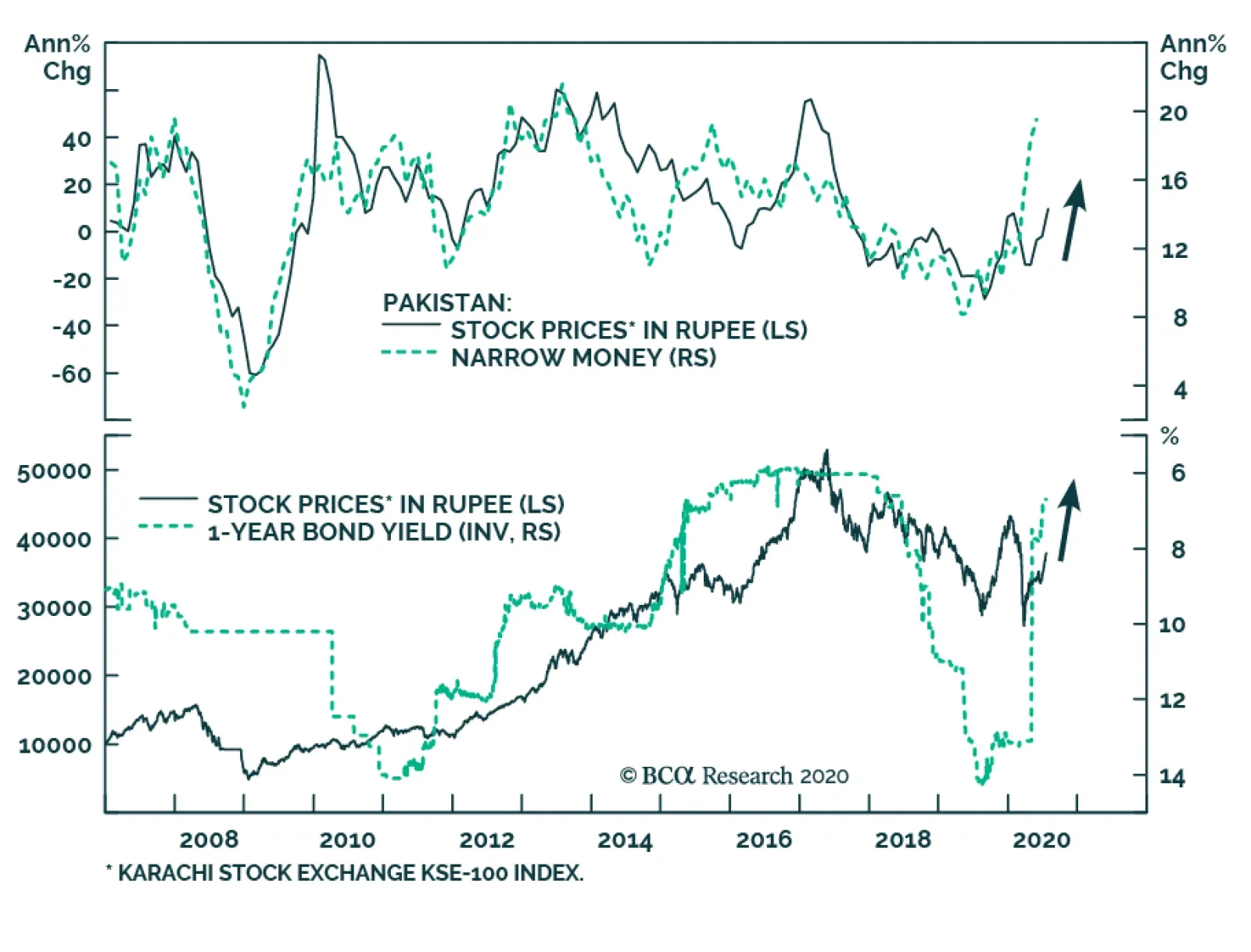

BCA Research's Emerging Markets Strategy service recommends buying Pakistani equities in absolute terms and overweighting this bourse within the emerging markets space. Pakistani stock prices in US dollar terms are currently 20% lower than their January…

Highlights The EU’s €750 billion fiscal package, along with another round of US stimulus likely exceeding $1 trillion, will support global oil demand. On the supply side, OPEC 2.0’s production discipline likely holds, and US shale output will remain depressed. These fundamentals, along with a weakening USD, will continue to support Brent prices, which are up 129% from their lows in April. China’s record-setting crude-oil-import surge during the COVID-19 pandemic – averaging 12.7mm b/d in 1H20, up 28.5% y/y – is at risk of slowing in 2H20, as domestic storage fills. Supply-side risks are acute: Massive OPEC 2.0 spare capacity – which could exceed 6mm b/d into 2021 – will tempt producers eager to monetize these to boost revenue. On the demand side, COVID-19 infection rates are surging in the US. Progress on vaccines notwithstanding, politically intolerable public-health risks in big consuming markets could usher in demand-crushing lockdowns again. Economic policy uncertainty remains elevated globally, but the balance of risks continues to favor the upside: We expect 2H20 Brent prices to average $44/bbl, and 2021 prices to average $65/bbl, unchanged from last month’s forecast. Feature We are marginally lifting our forecast of average 2020 Brent prices to $43/bbl, with 2H20 expected to average $44/bbl, and $65/bbl next year, unchanged from June. Marginal improvements to preliminary supply and demand estimates earlier in the COVID-19 pandemic support the thesis that fundamentals will not derail the massive oil-price rally that lifted Brent 129% from its April 21 low of $19.30/bbl. A weakening US dollar, and the expectation this trend will continue, also is supportive to commodities in general, oil in particular. As a result, we are marginally lifting our forecast of average 2020 Brent prices to $43/bbl, with 2H20 expected to average $44/bbl, and $65/bbl next year, unchanged from June (Chart of the Week). The three principal oil-market data providers – the US EIA, IEA and OPEC – raised demand estimates at the margin for 1H20, particularly for 2Q20, the nadir for global oil consumption. The EIA’s estimate for 2Q20 demand shows an upward revision of 550k b/d from last month’s estimate. On the supply side, the EIA estimates global output fell -8.1mm b/d in 2Q20, a -300k b/d downward revision vs. its estimate from last month (Chart 2). Chart of the WeekOil Price Rally Remains Intact

Oil Price Rally Remains Intact

Oil Price Rally Remains Intact

Chart 2OPEC 2.0, US Shale Production Cuts Deepen

OPEC 2.0, US Shale Production Cuts Deepen

OPEC 2.0, US Shale Production Cuts Deepen

We continue to expect the drawdown in storage levels to flatten – and then backwardate – the forward curves for Brent and WTI. After accounting for this better-than-expected fundamental performance, we now expect global supply to fall 5.9mm b/d in 2020 and to increase 4.2mm b/d in 2021. On the demand side, we now expect 2020 demand to fall 8.1mm b/d vs. 8.9mm b/d last month, and for 2021 demand to rise 7.8mm b/d vs 8.5mm b/d in June (Chart 3). This will keep the physical deficit we’ve been forecasting for 2H20 and 2021 in place, allowing OECD storage to fall to 3,026mm barrels by year-end and to 2,766mm barrels by the end of next year (Chart 4). Chart 3Supply-Demand Balances Tighten ...

Supply-Demand Balances Tighten ...

Supply-Demand Balances Tighten ...

Chart 4... Leading To Deeper Storage Draws ...

... Leading To Deeper Storage Draws ...

... Leading To Deeper Storage Draws ...

We continue to expect the drawdown in storage levels to flatten – and then backwardate – the forward curves for Brent and WTI (Chart 5). One caveat, though: We are watching floating storage levels closely, particularly in Asia: The current structure of the Brent forwards does not support carrying floating inventory, but it’s been slow moving lower (Chart 6). This could reflect a slowing in China’s crude-oil import surge, which hit record levels in May and June. Chart 5... And More Backwardation In Brent And WTI Forwards ...

... And More Backwardation In Brent And WTI Forwards ...

... And More Backwardation In Brent And WTI Forwards ...

Chart 6… Even As Floating Storage In Asia Remains Elevated

Balance Of Oil-Price Risk Remains To The Upside

Balance Of Oil-Price Risk Remains To The Upside

China’s Crude-Import Binge Ending? There is a non-trivial risk China’s crude-buying binge during the COVID-19 pandemic, which supported prices during the brief Saudi-Russian market-share war in March and the collapse in global demand in 2Q20, may have run its course (Chart 7).1 At the depths of the global pandemic in 2Q20, China’s year-on-year (y/y) crude imports surged 15%. According to Reuters, China’s crude oil imports totaled 12.9mm b/d in June, a record level for the second month in a row.2 Much of this was converted to refined products – chiefly gasoline and diesel fuel – as China’s demand recovered from the global pandemic (Chart 8). China’s 208 refineries can process 22.3mm b/d of crude, according to the Baker Institute at Rice University in Houston.3 Refinery runs in June were estimated at just over 14mm b/d by Reuters. Chart 7China's Crude Import Binge Stalls

China's Crude Import Binge Stalls

China's Crude Import Binge Stalls

Chart 8China's Refiners Lift Runs As Imports Surge

China's Refiners Lift Runs As Imports Surge

China's Refiners Lift Runs As Imports Surge

A reduction in China’s crude imports would force barrels to either remain on the water until refiners find a need for it, or demand for refined products increases in the region. China imports its oil into 59 port facilities, which can process ~ 16mm b/d. Storage is comprised of 74 crude oil facilities holding ~ 706mm barrels, and 213 refined-product facilities with capacity to hold ~ 357mm barrels of products (Map 1). By Reuters’s count, ~ 2mm b/d of crude went into storage in the January-May period, while close to 2.8mm b/d was stored in June. Official storage data is a state secret, so it is not possible to determine whether China’s crude and product storage is full. However, if crude oil imports remain subdued – and floating storage in Asia remains elevated – we would surmise the Chinese storage facilities are close to full. Additionally, any sharp and sustained increase in refined product exports would indicate storage is brimming. Map 1Baker Institute China Oil Map

Balance Of Oil-Price Risk Remains To The Upside

Balance Of Oil-Price Risk Remains To The Upside

A reduction in China’s crude imports would force barrels to either remain on the water until refiners find a need for it, or demand for refined products increases in the region. We expect the latter condition to obtain, in line with our expectation of a global recovery in demand, even though China remains out of sync with the rest of the world presently. China was the first state to confront the pandemic and first to emerge out of it; its trading partners still are in various stages of recovery (Chart 9). Chart 9China's Demand Recovery Likely Will Be Choppy

China's Demand Recovery Likely Will Be Choppy

China's Demand Recovery Likely Will Be Choppy

OPEC 2.0’s Remains Sensitive To Demand Fluctuations OPEC 2.0’s leaders – the Kingdom of Saudi Arabia (KSA) and Russia – also managed to secure additional “compensation” cuts from members that have missed their targets in previous months. The asynchronous recovery in global oil demand poses a unique problem for OPEC 2.0 this year and next. OPEC 2.0 will be easing production curtailments to 7.7mm b/d beginning in August from 9.6mm b/d in July, on the advice of its Joint Ministerial Monitoring Committee (JMMC). This is a decision that will be closely monitored, amid rising concern over the speed of demand recovery in the US and EM economies, due to mounting COVID-19 cases (Chart 10). The surge in US infections relative to its trading partners is of particular concern, given the size of US oil demand (Chart 11). In 2H20, we expect US demand will account for close to 20% of global demand, much the same level it was prior to the pandemic (Table 1). Chart 10COVID-19 Infections Surge In The US

Balance Of Oil-Price Risk Remains To The Upside

Balance Of Oil-Price Risk Remains To The Upside

Chart 11US COVID-19 Infections Are A Risk To Global Commodity Demand

Balance Of Oil-Price Risk Remains To The Upside

Balance Of Oil-Price Risk Remains To The Upside

Table 1BCA Global Oil Supply - Demand Balances (MMb/d, Base Case Balances)

Balance Of Oil-Price Risk Remains To The Upside

Balance Of Oil-Price Risk Remains To The Upside

OPEC 2.0’s leaders – the Kingdom of Saudi Arabia (KSA) and Russia – also managed to secure additional “compensation” cuts from members that have missed their targets in previous months, bringing the actual increase in production closer to 1-1.5mm b/d. Together, Iraq, Nigeria, Kazakhstan, and Angola, over-produced versus their May and June targets by ~ 760k b/d. In our balances estimates, as is our normal practice, we haircut these estimates and use a lower compliance level that those stated in the official OPEC 2.0 agreement. In the case of these producers, we assume they will compensate for ~ 70% of their overproduction, bringing the adjusted cuts to ~ 8.3mm b/d. This should be sufficient to maintain the current supply deficit in oil markets that continues to support Brent prices above $40/bbl. However, the reliance on laggards’ extra cuts to balance markets adds instability. There is a lot of supply on the sidelines from the OPEC 2.0 cuts and the restart of the Neutral Zone shared by Saudi Arabia and Kuwait. The JMMC is continually assessing supply-demand balances and remains focused on making sure the totality of the cuts does not fall on a small group of countries. It reiterated its position that “achieving 100% conformity from all participating Countries is not only fair, but vital for the ongoing rebalancing efforts and to help deliver long term oil market stability.” In June, OPEC 2.0’s overall compliance was 107% – mostly reflecting over-compliance from KSA, the UAE, and Kuwait.4 There is a lot of supply on the sidelines from the OPEC 2.0 cuts and the restart of the Neutral Zone shared by Saudi Arabia and Kuwait. The US EIA estimates that within the original OPEC cartel spare capacity will average close to 6mm b/d this year, the first time since 2002 that it has exceeded 5mm b/d. On top of this, there’s the looming downside risk of a new Iran deal if Democrats win the White House and Congress in US elections in November, and a possible restart of Libyan exports this year. Watch The DUCs In The US With WTI prices averaging $41/bbl so far in July, we continue to expect part of previously shut-in US production to come back on line in July, August and September. Nonetheless, the negative effect of the multi-year low rig count will be felt heavily in 4Q20 and 1Q21 and will push production lower. The rig count appears to be bottoming but is not expected to increase meaningfully until WTI prices move closer to $45-50/bbl. On average it takes somewhere between 9-12 months for the signal from higher prices to result in new oil production flowing to market in the US. As the rig count moves back up in 2021, its effect on production will be apparent only in late-2021. However, the massive inventory of drilled-but-uncompleted (DUC) wells in the main US tight-oil basins will provide a source of cheaper new supply, if WTI prices remain above $40/bbl. DUCs are 30-40% cheaper to complete compared to drilling a new well from start. We expect DUCs completion will begin adding to US crude output in 1Q21, and that this will continue to be a source of supply beyond 2021. Bottom line: Global economic policy uncertainty remains elevated, albeit off its recent highs (Chart 12). We expect this uncertainty to continue to wane, which will allow the USD to continue to weaken. This will spur global oil demand, and will augment the fiscal and monetary stimulus to the COVID-19 pandemic undertaken globally. Chart 12Global Policy Uncertainty Remains High, Which Could Support USD Demand

Balance Of Oil-Price Risk Remains To The Upside

Balance Of Oil-Price Risk Remains To The Upside

Nonetheless, the global recovery remains out of sync, which complicates OPEC 2.0’s production management, and markets’ estimation of supply-demand balances. Uneven success in combating the pandemic keeps the risk of lockdowns on the radar in the US. Policy is driving oil production at present, and, given the temptation to monetize spare capacity, the supply side remains a risk to prices. We continue to see upside risk dominating the evolution of prices and are maintaining our expectation Brent prices will average $44/bbl in 2H20 – lifting the overall 2020 average to $43/bbl – and $65/bbl next year. Our expectation WTI will trade $2-$4/bbl below Brent also remains intact. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Hugo Bélanger Associate Editor Commodity & Energy Strategy HugoB@bcaresearch.com Fernando Crupi Research Associate Commodity & Energy Strategy FernandoC@bcaresearch.com Commodities Round-Up Energy: Overweight Canadian oil production averaged 4.6mm b/d in 2Q20 vs. 5.5mm b/d in 2Q19, based on EIA estimates. The lack of demand from US refiners – crude imports from Canada fell by 420k b/d y/y during the quarter – and close to maxed-out local storage facilities pushed prices below cash costs, forcing the shut-ins of more than 1mm b/d of crude production. Canadian energy companies started releasing their 2Q20 earnings this week and analysts expect the results to be one of the worst ever recorded, reflecting the extent of the pain producers felt during the COVID-19 shock. Base Metals: Neutral High-grade iron ore prices (65% Fe) were trading above $120/MT this week, on the back of forward guidance from the commodity’s top exporter, Brazilian miner Vale, which suggested exports will be lower than had been previously estimated this year, according to Fastmarkets MB, a sister service of BCA Research. This is in line with an Australian Department of Industry, Science, Energy and Resources analysis in June, which noted, “The COVID-19 pandemic appears to have affected both sides of the iron ore market: demand disruptions have run up against supply problems localised in Brazil, where COVID-19-related lockdowns have derailed efforts to recover from shutdowns in the wake of the Brumadinho tailings dam collapse” (Chart 13). Precious Metals: Neutral Our long silver position is up 17.5% since it was recommended July 2. We are placing a stop-loss on the position at $21/oz, our earlier target, given the metal was trading ~ $22/oz as we went to press. The factors supporting gold prices – chiefly low real rates in the US, a weakening dollar and global monetary accommodation, also support silver prices. However, silver also will benefit from the recovery in industrial activity and incomes we anticipate in the wake of global fiscal and monetary stimulus, which will drive demand for consumer products (Chart 14). Ags/Softs: Underweight Lumber prices have more than doubled since April lows. The uncertainty brought by the COVID-19 health emergency altered the perception of future housing demand and, by extension, lumber demand, to the point that mills responded by substantially decreasing capacity utilization rates. However, in the wake of global monetary and fiscal stimulus, housing weathered the storm better than expected. Furthermore, a surge in DIY projects from individuals working from home at a time of reduced supply contributed to the current state of market shortage. Chart 13Lower Supply Supports Iron Ore Prices

Lower Supply Supports Iron Ore Prices

Lower Supply Supports Iron Ore Prices

Chart 14Silver Favored Over Gold

Silver Favored Over Gold

Silver Favored Over Gold

Footnotes 1 In our reckoning, a non-trivial risk is something greater than Russian roulette odds – i.e., a 1-in-6 chance of an event occuring. Re the ever-so-brief Saudi-Russian market-share war, please see KSA, Russia Will Be Forced To Quit Market-Share War, which we published March 19, 2020. It is available at ces.bcaresearch.com. 2 Please see COLUMN-China's record crude oil storage flies under the radar: Russell published by reuters.com July 20, 2020. 3 The Baker Institute’s Open-Source Mapping of China's Oil Infrastructure was last updated in March 2020. The map is “a beta version and is likely missing some pieces of existing infrastructure. The challenge of China’s geographic expanse — it is roughly the same area as the U.S. Lower 48 — is compounded by a lack of transparency on the part of China’s government,” according to the Baker Institute. 4 In our supply-side estimates, we used IEA estimates of cuts for June this month. This doesn’t change the overall estimate of cuts from our earlier analysis; however, it slightly changes how the 9.7mm b/d was split between OPEC 2.0 members. the official eased cuts are 7.7mm b/d from 9.7mm b/d in May-June-July, but it actually is closer to 8.3mm b/d accounting for the compensation from the countries mentioned above. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Trade Recommendation Performance In 2020 Q2

Balance Of Oil-Price Risk Remains To The Upside

Balance Of Oil-Price Risk Remains To The Upside

Commodity Prices and Plays Reference Table Trades Closed in 2020 Summary of Closed Trades

Balance Of Oil-Price Risk Remains To The Upside

Balance Of Oil-Price Risk Remains To The Upside

Last Friday, my colleague Dhaval Joshi and I held a webcast discussing investment strategies. The topics of discussion included global equity valuations, mega-cap stocks leadership and the outlook for EM stocks, fixed-income and currencies. You can listen to the webcast recording by clicking here. An Opportunity In Pakistani Equities And Bonds Pakistani stock prices in US dollar terms are currently 20% lower than their January high and 56% lower than their 2017 high (Chart I-1, top panel). Meanwhile, the government projected a contraction in real GDP during the fiscal year 2019-20 (ending on June 30), the first in 68 years. We believe stock prices have already priced in plenty of negatives, and that Pakistani equities are likely to move higher over the next six months. Strengthening the balance of payments (BoP) position and continuing policy rate cuts will increase investors’ confidence and benefit its stock market (Chart I-2). We also expect the Pakistani bourse to outperform the EM equity benchmark (Chart I-1, bottom panel). Chart I-1Pakistani Equities: More Upside Ahead

Pakistani Equities: More Upside Ahead

Pakistani Equities: More Upside Ahead

Chart I-2Monetary Easing Will Help Pakistani Equities

Monetary Easing Will Help Pakistani Equities

Monetary Easing Will Help Pakistani Equities

Chart I-3The Current Account Deficit Is Set To Shrink Further

The Current Account Deficit Is Set To Shrink Further

The Current Account Deficit Is Set To Shrink Further

Balance Of Payments Position Pakistan’s BoP position is set to improve. First, its trade deficit will shrink further, as Pakistan’s export will likely improve more than its imports (Chart I-3). The country’s total exports declined 6.8% year-on-year in June, which is a considerable improvement as compared to the massive 54% and 33% contractions that occurred in April and May, respectively. The country was on a strict lockdown for the whole month of April, which was then lifted in early May. As the number of daily new cases and deaths are falling, the country is likely to remain open, lowering the odds of a domestic supply disruption. In addition, as DM growth recovers, the demand for Pakistani products will improve as well. Europe and the US together account for about 54% of Pakistan’s exports. The government is keen to boost the performance of the domestic textile sector, which accounts for nearly 60% of the country’s total exports. The government will likely approve the industry’s request for supportive measures, including access to competitively priced energy, a lower sales tax rate, quick refunds, and a reduction of the turnover tax rate. Moreover, the government has prepared an incentive package for the global promotion of the country’s information technology (IT) sector, aiming to increase IT service exports from the current level of US$1 billion to US$10 billion by 2023. Currently, over 6,000 Pakistan-based IT companies are providing IT products and services to entities in over 100 countries worldwide. Regarding Pakistan’s imports, low oil prices will help reduce the country’s import bill year-on-year over the next six months. Second, remittance inflows – currently at 9% of GDP – have become an extremely important source of financing for Pakistan’s trade deficit. Even though about half of the remittances sent to Pakistan are from oil-producing regions like Saudi Arabia, UAE, Oman and Qatar, low oil prices may only have a limited impact on Pakistan’s remittance inflows. For example, when Brent oil prices fell to US$40 in early 2016, remittances sent to Pakistan in the second half of that year declined by only 1.9% on year-on-year terms. Over the first six months of this year, the remittances received by Pakistan still had a year-on-year growth of 8.7%. At the same time, the government has planned various measures to boost remittances. For example, a “national remittance loyalty program” will be launched on September 1, 2020, in which various incentives would be given to remitters. Strengthening the balance of payments (BoP) position and continuing policy rate cuts will increase investors’ confidence and benefit its stock market. Third, Pakistan will receive considerable financial inflows this year, probably amounting to over US$12 billion1 from multilateral and bilateral sources. This will be more than enough to finance its current account deficit, which was at US$11 billion over the past 12 months. In April, the International Monetary Fund (IMF) approved the disbursement of about US$1.4 billion to Pakistan under the Rapid Financing Instrument designed to address the economic impact of the Covid-19 shock. The World Bank and the Asian Development Bank have also pledged around US$ 2.5 billion in assistance. The IMF and the Pakistani government are in talks about the completion of the second review for the Extended Fund Facility (EFF) program. If completed in the coming months, the IMF will likely disburse about US$1 billion to Pakistan in the second half of this year. In April, G20 countries also awarded Pakistan a suspension of debt service payments, valued at US$ 1.8 billion, which will be used to pay for Pakistan’s welfare programs. In early July, the State Bank of Pakistan (SBP) received a US$1 billion loan disbursement from China. This came after Beijing awarded Pakistan a US$300 million loan last month. The authorities plan to raise US$1.5 billion through the issuance of Eurobonds over the next 12 months. Other than the funds borrowed by the Pakistani government, net foreign direct inflows, mainly driven by phase II of the China-Pakistan Economic Corridor (CPEC), are set to continue to increase over the remainder of this year, having already grown 40% year-on-year during the first six months of this year. About 63% of that increase came from China. Meanwhile, as we expect macro dynamics to improve in the next six months, net portfolio investment is also likely to increase after having been record low this year (Chart I-4). In addition, as the geopolitical confrontation between the US and China is likely to persist over many years, both Chinese and global manufacturers may move their factories from China to Pakistan.2 Bottom Line: Pakistan’s BoP position will be ameliorating in the months to come. Lower Inflation And Monetary Easing Continuous monetary easing is very likely and will depend on the extent of the decline in domestic inflation. Both headline and core inflation rates seem to have peaked in January (Chart I-5). Significant local currency depreciation last year had spurred inflation in Pakistan. Then, early this year, supply disruptions and hoarding behaviors attributed to the pandemic have contributed to elevated inflation. Chart I-4Net Portfolio Investment Inflows Are Likely To Increase

Net Portfolio Investment Inflows Are Likely To Increase

Net Portfolio Investment Inflows Are Likely To Increase

Chart I-5Both Headline And Core Inflation Rates Will Likely Fall Further

Both Headline And Core Inflation Rates Will Likely Fall Further

Both Headline And Core Inflation Rates Will Likely Fall Further

A closer look at the inflation subcomponents shows that recreation and culture, communication, and education have already fallen well below 5% in the last month. Transport inflation came in negative at 4.4% in June. The inflation of non-perishable food items was still stubbornly high at 14.9% last month. Increasing the food supply and reducing hoarding will help ease that. This, along with a stable exchange rate and a negative output gap will cause a meaningful drop in inflation. As inflation drops, interest rates will be reduced to facilitate an economic recovery. While the current 7% policy rate is lower than headline inflation, and on par with core inflation, Pakistani interest rates remain much higher than those in many other emerging countries. Investment Recommendations We recommend buying Pakistani equities in absolute terms and continuing to overweight this bourse within the emerging markets space. The stock market will benefit from a business cycle recovery following the worst recession in history, worse than during the 2008 Great Recession (Chart I-6). Fertilizer and cement producers, which together account for nearly 30% of the overall stock market, will benefit from falling energy prices, a significant cut in interest rates and supportive government measures. The government recently approved subsidies to encourage fertilizer output. In the meantime, the country’s construction stimulus package and its easing of lockdown orders will help lift demand for cement over the second half of 2020. As a result, both fertilizer and cement output are set to increase (Chart I-7). Besides, a cheapened currency will limit fertilizer imports and help cement producers export their output, which will benefit their revenue. Chart I-6Manufacturing Activity In Pakistan Will Soon Rebound

Manufacturing Activity In Pakistan Will Soon Rebound

Manufacturing Activity In Pakistan Will Soon Rebound

Chart I-7Both Fertilizer And Cement Output Are Set To Increase

Both Fertilizer And Cement Output Are Set To Increase

Both Fertilizer And Cement Output Are Set To Increase

Banks account for about 22% of the overall stock market. Our stress test on the Pakistani banking sector shows it is modestly undervalued at present (Table I-1). Even assuming the worst-case scenario for non-performing loans (NPL), where the NPL ratio would rise to 17.5% from the current 6.6%, the resulting adjusted price-to-book ratio will be only 1.6. Table I-1Stress Test On Pakistani Banking Sector

Pakistani, Chilean & Czech Markets

Pakistani, Chilean & Czech Markets

Both in absolute terms, and relative to EM valuations, Pakistani stocks appear attractive (Charts I-8 and I-9). Finally, foreign investors have bailed out of Pakistani stocks and local currency bonds since 2018, as illustrated in Chart I-4 on page 4. Ameliorating economic conditions will lure foreign investors back. Chart I-8Pakistani Equities: Valuation Measures Are Attractive In Both Absolute Terms…

Pakistani Equities: Valuation Measures Are Attractive In Both Absolute Terms...

Pakistani Equities: Valuation Measures Are Attractive In Both Absolute Terms...

Chart I-9…And Relative To The EM Benchmark

...And Relative To The EM Benchmark

...And Relative To The EM Benchmark

For fixed-income investors, we recommend continuing to hold the long Pakistani local currency 5-year government bonds position, which has produced a 12% return since our recommendation on December 5th 2019. We expect interest rates to drop another 100 basis points (Chart I-5, bottom panel, on page 5). Ellen JingYuan He Associate Vice President ellenj@bcaresearch.com Chile: Not Out Of The Woods Copper prices have staged an impressive rally in the past four months, but the performance of Chilean markets remains lackluster (Chart II-1). While the red metal has broken above its January highs, Chile’s equities and currency are still trading 25% and 5% below their January peak, respectively. The government’s mismanagement of the pandemic has reignited and heightened the existing socio-political discontent, thus increasing the fragility of the situation. We therefore recommend that investors maintain a cautious stance on Chilean assets. As for dedicated EM portfolios, we recommend moving this bourse from neutral to underweight: First, the lockdowns resulting from the pandemic have revealed the precarious financial condition of low and middle-class households. The lack of savings among these groups prevented workers from self-isolating for more than a couple of weeks. The urge for them to return to work enabled the outbreak to escalate in May. Consequently, these social groups have suffered from infections, and Chile has rapidly become one of the worst affected countries in the world in terms of per-capita COVID-19 cases and deaths. Chart II-2 shows that, as a share of total population, Chile tops the region in terms of cummulative cases and deaths. Moreover, Chile has the eighth highest COVID-19 infections per capita in the world, even though its testing rate per capita is lower than that of Europe and the US. Chart II-1Chilean Markets Have Been Much Weaker Than Copper

Chilean Markets Have Been Much Weaker Than Copper

Chilean Markets Have Been Much Weaker Than Copper

Chart II-2The Pandemic Has Hit Chile Hard

The Pandemic Has Hit Chile Hard

The Pandemic Has Hit Chile Hard

Chart II-3The Economy Is In The Doldrums

The Economy Is In The Doldrums

The Economy Is In The Doldrums

Given the wide spread of the virus, Chile has implemented harsher quarantine measures than the rest of the region, which means that the economic reopening and recovery will start from a lower level of activity. The inability of President Pinera’s administration to protect low and middle-class households from being exposed to the virus has renewed a nation-wide distrust in the government. According to Cadem, one of the country’s most cited polling companies, President Pinera’s approval rating has fallen back to just 17%, not far from the lows seen during last year’s violent social unrest. In sum, these recent events have confirmed our major theme for Chile, discussed in our December Special Report. It reads as follows: Chile’s political elite has been greatly underestimating the depth and gravity of the popular frustration and has been reluctant to address the issue in a meaningful way. Consequently, Chile is set to experience a renewal in protests and a rise in political volatility as the date of the referendum on the Constitution, which is scheduled to take place in October, nears. Second, Chile is experiencing its worst recession in modern history. Chart II-3shows that the economy was already in a slump at the beginning of the year, and the economic lockdown has caused double-digit contractions in many sectors. Further, business confidence never fully recovered from last year’s social protests and has been plummeting deeper since the start of the pandemic (Chart II-3, bottom panel). Chart II-4Banks' NPLs Are Set To Rise

Banks' NPLs Are Set To Rise

Banks' NPLs Are Set To Rise

While President Pinera’s decision to prioritize small and medium-sized businesses (SMEs) has been popular among the middle class, the reality is that Chile remains a highly oligopolistic market, dominated by large companies. The failure to support these businesses will prevent a revival in business sentiment, hiring and investment and, hence, prolong the economic downtrend. This unprecedent economic contraction has caused a rapid surge in non-performing loans (NPLs), which will hurt banks’ capital profits and tighten lending standards. NPLs will rise much further given the record depth of this recession (Chart II-4). Moreover, bank stocks compose 25% of the MSCI Chile index, so a hit to banking profitability will exert downward pressure on the equity index. Third, even though fiscal and monetary stimuli have been large and were implemented rapidly, they are probably insufficient to produce a quick recovery. The government first announced a fiscal plan between March 19 and April 8 worth US$ 17 billion (or 6% of GDP), the third largest in the region. However, it is still quite small compared to that of OECD members. Excluding liquidity provisions for SMEs and tax reductions, the size of new government spending in 2020 is only 3.5% of GDP. On June 14, the government devised another fiscal plan, worth US$ 12 billon (or 5% of GDP). However, it will be spread out over the next 24 months – only 1.5% of GDP of additional stimulus will be injected over the next 12 months. This extra kick in spending seems too small given the depth of the recession. In terms of monetary policy, the Chilean central bank has already reached the limits of its orthodox toolkit. The monetary authorities have cut the policy rate by 125 basis points since November of last year, but they have reached the constitutional technical minimum of 0.5%. The central bank is now using alternative tools to stimulate the economy, such as offering cheap lending to SMEs and a US$ 8 billion quantitative easing program for buying financial institutions’ bonds, as the Constitution forbids the purchasing of government and non-financial corporate debt. In a nutshell, the overall efficiency of these monetary policies will be subdued as the main drags on the economy are downbeat business and consumer confidence stemming from ongoing socio-political tensions, not high interest rates. Chile is shrouded in a cloud of political uncertainty. Monetary policy has reached its limits, and fiscal stimulus is insufficient for now. Fourth, higher copper prices will help on the margin, but will not bail out the Chilean economy. Even with the latest rally in copper prices, Chilean copper exports will continue contracting in US$ terms. The latest increase in prices will be more than offset by output cuts caused by social distancing rules and reduced staff in mines all over the country. Bottom Line: Chile is shrouded in a cloud of political uncertainty. Monetary policy has reached its limits, and fiscal stimulus is insufficient for now. Investment recommendations Chart II-5Our CLP vs. USD Trade

Our CLP vs. USD Trade

Our CLP vs. USD Trade

Continue shorting the CLP relative to a basket of the CHF, EUR and JPY. We closed our short CLP/USD on July 9th with a 29% profit (Chart II-5) and began shorting it versus an equal-weighted basket of the CHF, EUR and JPY. Within an EM equity portfolio, downgrade Chilean stocks from neutral to underweight. An ailing economy and political uncertainty will divert capital from the country despite attractive equity valuations. For an EM local bond portfolio, we are also downgrading Chile from neutral to underweight, as the risk of renewed currency depreciation is too large to ignore and downside in yields is limited due to the zero bound. Juan Egaña Research Associate juane@bcaresearch.com The Czech Republic: Pay Rates And Go Long The Currency An opportunity to bet on higher longer-term interest rates and on a stronger currency has emerged in the Czech Republic (Chart III-1). Consumer price inflation is above the central bank’s 2% target and will continue to rise, which will necessitate higher interest rates (Chart III-2). The latter will lead to currency appreciation. Chart III-1Pay Rates And Go Long CZK vs. USD

Pay Rates And Go Long CZK vs. USD

Pay Rates And Go Long CZK vs. USD

Chart III-2Inflation Is Above The CB Bands

Inflation Is Above The CB Bands

Inflation Is Above The CB Bands