Emerging Markets

Highlights The economic and health crises since Q1 2020 have accelerated the breakdown in the US-China relationship. Although the US is in a much weaker economic position this year than in 2019, President Trump may have fewer political constraints to an escalation in the trade war. President Xi Jinping is fueling provocations with the US, adding instability and unpredictability to the geopolitical equation. The Phase One trade deal may be collapsing. We recommend a defensive stance on Chinese risk assets and the RMB during the summer. Feature The outbreak of COVID-19 this year has sparked the worst economic contraction in China and the US in decades. Economic calamities and social unrest should have tied the hands of leaders in both countries. However, as our Geopolitical Strategist Matt Gertken reminds us, this is an atypical election year in the US and some constraints that previously deterred both sides from taking aggressive actions may be diminishing.1 We agree that the economic and health crises have likely accelerated the possibility of a breakdown in the relationship between the US and China. The risk will likely reach a new height in the summer, when pressure on Trump’s election campaign intensifies leading up to the vote in November. While there is a growing bipartisan hawkish view on China in Washington, China is also playing a part in fanning the flames. The USD/CNY exchange rate will be extremely volatile during this episode of heightened geopolitical turbulence. We continue to hold a long USD-CNH position, with the expectation that the RMB will likely weaken further in the summer. Trump Facing Fewer Constraints Whether Trump’s chances of reelection increase through a strong recovery in the US stock market and economy, or decrease through an economic recession and/or weak public support, either scenario could remove constraints preventing Trump from confronting China. Trump’s current priority may be to secure a recovery in the equity market and improve his polling, which will require economic improvement. Ironically, the US stock market has been on fire despite the battered real economy. The S&P 500 Index has gone up by 44% since its trough on March 23, nearly erasing its losses for the year. The higher the market rises, the more Trump may believe that the market can sustain a shock even if he resorts to imposing tariffs on Chinese export goods - particularly if his approval rating does not rise along with the market. The market’s reaction in 2018 and 2019 provides a good example of how the US financial markets shrugged off any negative impact from a trade war between the US and China (Chart 1). If the pandemic prevents the US economy from fully reopening and/or recovering in the summer, then an equity market correction could send a negative signal about Trump’s reelection prospects. In this case, Trump may not be as enslaved by financial constraints as he would have been if the economy was in an expansionary state. A falling approval rating, coupled with domestic social unrest, would make Trump a “lame duck” President (Chart 2). Therefore, he may try to divert attention away from the economy and adopt an aggressive foreign and trade policy. China is already perceived negatively by a majority of American voters and certain political communities, thus there could be a political upside for Trump to escalate his confrontation with China. Chart 1US Stocks Kept Reaching New Highs In 2019 Despite An Ongoing Trade War

US Stocks Kept Reaching New Highs In 2019 Despite An Ongoing Trade War

US Stocks Kept Reaching New Highs In 2019 Despite An Ongoing Trade War

Chart 2Trump’s Polling Drops Below Average

Watch Out For A Second Wave (Of US-China Frictions)

Watch Out For A Second Wave (Of US-China Frictions)

All bets are off if Trump’s approval rating continues to trend downwards, regardless of whether the US equity market continues to rally and/or if the US economy is mired in recession. Our Geopolitical Strategy illustrates the scenarios as follows (Diagram 1). If Trump’s approval rating is high and the market is up, then Trump is “winning” and the only risk of a tariff hike would come from overconfidence or Chinese provocation. If his approval is up but the market falls, then he may become more inclined to use tariffs. If his approval rating is low but the market is up, then he has ammunition to get tougher on China. If his approval and the market are collapsing, then he is a “lame duck president” and all bets are off. Combined, these scenarios imply there is a 59% probability that Trump refrains from large tariffs, and a 41% chance that he reverts to large tariffs. Diagram 1Odds President Trump Will Hike Tariffs On China Before US Election

Watch Out For A Second Wave (Of US-China Frictions)

Watch Out For A Second Wave (Of US-China Frictions)

Bottom Line: All bets are off if Trump’s approval rating continues to trend downwards, regardless of whether the US equity market continues to rally and/or if the US economy is mired in recession. Both scenarios would remove financial and economic constraints that Trump faced in 2019. If Trump's polling is weak, he may spend financial ammunition to shore up his “America First” credentials. Adding China To The Geopolitical Instability Equation China itself may be an independent source of geopolitical instability and unpredictability. While President Xi Jinping does not have any electoral constraints, he needs to restore the confidence of Chinese people in the wake of the worst public health crisis and economic performance in decades. Like Trump, the pandemic gives President Xi an incentive to distract his populace from domestic crises by adopting hawkish foreign policies. This hawkish approach was demonstrated when a new Hong Kong SAR national security law was proposed and approved at this year’s National People’s Congress (NPC). The new law would give Beijing greater direct control over Hong Kong, in contravention of its promise of 50 years of substantial autonomy enshrined in the Sino-British Joint Declaration of 1984. China’s foreign policy tone recently shifted to a more combative one. This “wolf warrior diplomacy" has gained popularity among Chinese diplomats.2 During a news conference at this year’s NPC, China’s Foreign Minister Wang Yi defended the “wolf warrior diplomacy” by stating that the country will stand firm in defending its national interest and combating “smears.” Chart 3Chinese Imports Of American Goods Are Falling Far Short Of The Target Set By The Trade Deal

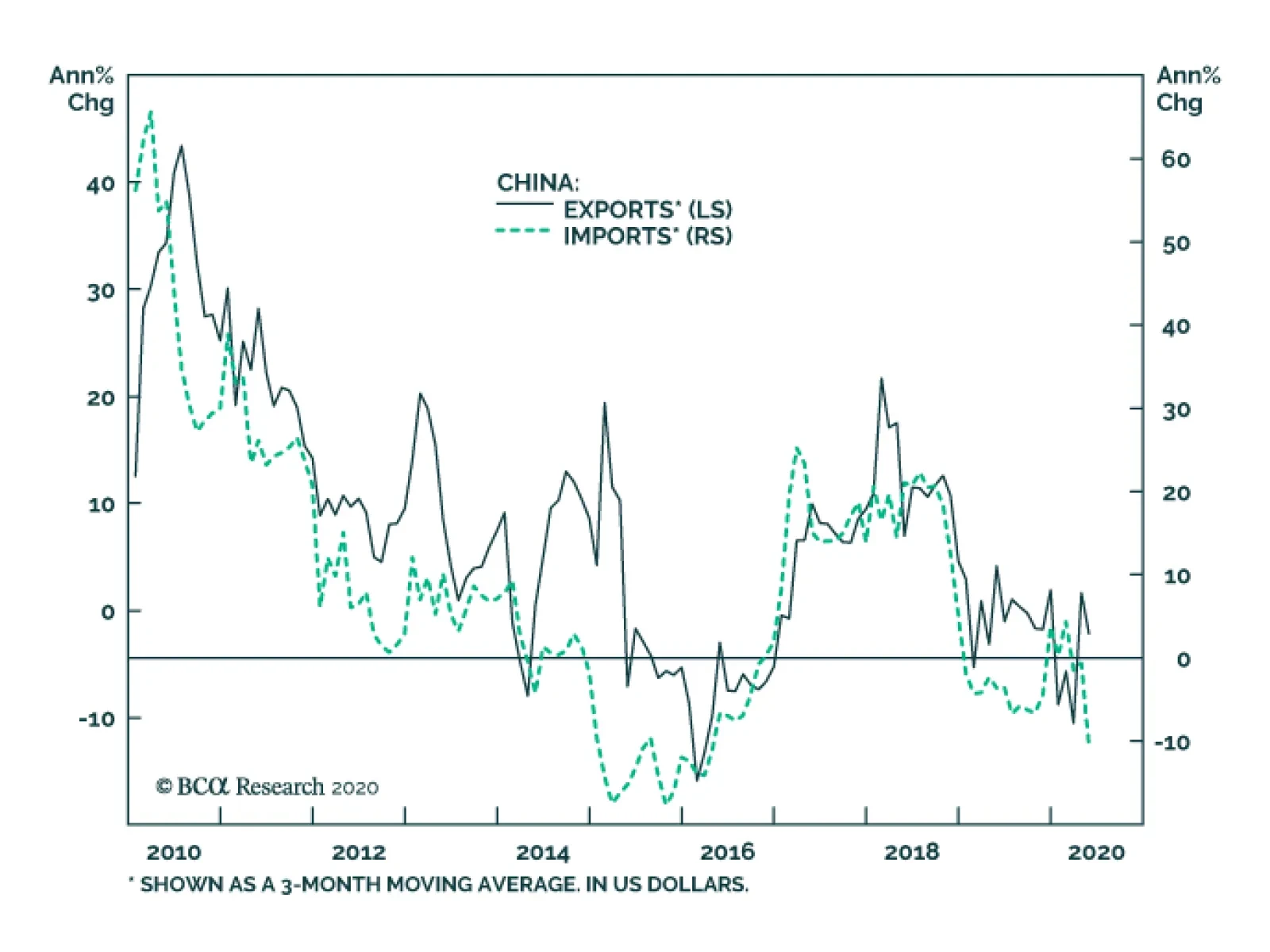

Chinese Imports Of American Goods Are Falling Far Short Of The Target Set By The Trade Deal

Chinese Imports Of American Goods Are Falling Far Short Of The Target Set By The Trade Deal

The response from the Trump administration has been lukewarm. While Secretary of State Mike Pompeo will strip Hong Kong of its autonomous status, President Trump is taking limited sanctions on mainland China and eschewing more drastic punitive measures. China may see the timid response as a sign that Trump is reluctant to take action on China and tip the bilateral relationship into an outright confrontation. This perception is, in itself, a risk that may lead to more provocation on both sides. Lastly, the Phase One trade deal is tenuous. US Trade Representative Robert Lighthizer last week stated that "China has done a pretty good job" at meeting its trade-deal quotas,3 but we have long argued China was never going to honor the commitment to its full extent.4 The latest data shows that Chinese purchases of American exports in the first four months of 2020, from manufacturing goods to agricultural produce and energy, have fallen far short of the huge expansion agreed in the deal (Chart 3). The recent depreciation in the RMB may be another sign that China is abandoning the Phase One trade deal.5 Weakness in economic fundamentals and renewed tensions between the US and China may have contributed to the RMB’s recent depreciation. However, the decline was reinforced by the PBoC’s move to set the CNY/USD fixing rate to its lowest point since 2008 (Chart 4). Given that the RMB has become an anchor for emerging market currencies, a rapid drop in the RMB would lead to selloffs in emerging Asian and Latin American currencies and, in turn, would strengthen the USD (Chart 5). The Trump administration may see a swift RMB depreciation as China is deliberately violating the Phase One trade deal, which will prompt Trump to seek retaliatory actions against China. Chinese purchases of American goods in the first four months of 2020 have fallen far short of the Phase One trade agreement. Chart 4Is The PBoC Sending A Warning Signal To Trump?

Is The PBoC Sending A Warning Signal To Trump?

Is The PBoC Sending A Warning Signal To Trump?

Chart 5The RMB Has Been The Anchor Currency In EM

The RMB Has Been The Anchor Currency In EM

The RMB Has Been The Anchor Currency In EM

Bottom Line: While China is prioritizing its own economic recovery, its foreign policy stance has decisively swung to a more combative one. Additionally, the Phase One trade deal is on the verge of collapsing. Investment Conclusions The USD/CNY exchange rate will likely be extremely volatile in the next quarter amid heightened geopolitical turbulence, with more downside risks to the RMB. As such, we continue to recommend that investors hedge their RMB exposure in Chinese stocks by holding a long USD-CNH position. We remain neutral on Chinese stocks in relative terms in view of the non-trivial, near-term vulnerability of risk assets. As in 2019, investable stocks are particularly exposed to an escalation in the US-China conflict (Chart 6). Chart 6Large Divergence In Onshore Versus Offshore Stock Performance During The Trade War

Large Divergence In Onshore Versus Offshore Stock Performance During The Trade War

Large Divergence In Onshore Versus Offshore Stock Performance During The Trade War

Chart 7Stocks In Some Domestic Demand-Oriented Sectors Are Still Relatively Safe Bets

Stocks In Some Domestic Demand-Oriented Sectors Are Still Relatively Safe Bets

Stocks In Some Domestic Demand-Oriented Sectors Are Still Relatively Safe Bets

Price corrections in both China’s onshore and offshore aggregate equity markets are likely to occur during the summer. Nevertheless, cyclical plays that closely track Chinese stimulus are relatively safe bets, especially for China’s domestic investors and in absolute terms (Chart 7). Jing Sima China Strategist jings@bcaresearch.com Footnotes 1Please see Geopolitical Strategy Weekly Report "Spheres Of Influence (GeoRisk Update)," dated May 29, 2020, available at gps.bcaresearch.com 2South China Morning Post, “Chinese Foreign Minister Wang Yi defends ‘wolf warrior’ diplomats for standing up to ‘smears’”, May 24, 2020 3Bloomberg, “Lighthizer Says He Feels ‘Very Good’ About Phase One China Deal”, June 4, 2020 4Please see China Investment Strategy Weekly Report "Managing Expectations," dated January 22, 2020, available at cis.bcaresearch.com 5The Phase One trade deal prohibits both the US and China from manipulating exchange rates to devalue their currencies for competitive purposes. Cyclical Investment Stance Equity Sector Recommendations

Highlights Egypt’s balance of payments have deteriorated materially due to both the crash in oil prices and the global pandemic. The country’s foreign funding requirements in 2020 are high and the currency is under depreciation pressures. Unless domestic interest rates are brought considerably lower, the nation’s public debt is on an unsustainable trajectory. Hence, Egypt needs to reduce local interest rates substantially and rapidly. And in so doing, the central bank cannot control or defend the exchange rate. The latter is set to depreciate. Investors should buy Egyptian local currency bonds while hedging their currency exposure. Feature The Central Bank of Egypt (CBE) is depleting its foreign exchange (FX) reserves to defend the currency (Chart I-1). As the CBE’s foreign exchange reserves diminish, so will its ability to support the currency. As such, the Egyptian pound will likely depreciate in the next 6-9 months. Interestingly, despite being a net importer of energy, many of Egypt’s critical macro parameters are positively correlated with oil prices (Chart I-2). Egypt is in fact deeply integrated in the Gulf oil-economy network via trade and capital flows. In other words, Egypt is a veiled play on oil. Chart I-1The CBE Has Been Defending The Currency

The CBE Has Been Defending The Currency

The CBE Has Been Defending The Currency

Chart I-2Egypt: A Veiled Play On Oil

Egypt: A Veiled Play On Oil

Egypt: A Veiled Play On Oil

Although oil prices have rallied sharply recently, the Emerging Markets Strategy team believes upside is limited and that oil prices will average about $40 over the next three years.1 In addition, local interest rates that are persistently above 10% are disastrous for both Egypt’s domestic demand and public debt sustainability. Egypt’s current account balance strongly correlates with oil prices because of the strong interlinkages that exist between Egypt and the oil-exporting Gulf countries. To preclude a vicious cycle in both the economy and public debt, the CBE should reduce interest rates materially and rapidly. Therefore, higher interest rates cannot be used to defend the exchange rate. Balance Of Payments Strains Egypt’s balance of payments (BoP) dynamics have deteriorated and the probability of a currency devaluation has risen: Current Account: The current account deficit – which stood at $9 billion and 3% of the GDP as of December 2019 – is widening significantly due to the plunge in oil prices this year (Chart I-2, top panel). Egypt’s current account balance strongly correlates with oil prices because of the strong interlinkages that exist between Egypt and the oil-exporting Gulf countries. The latter have been hard hit by the twin shocks of the coronavirus pandemic and the oil crash. First, Egypt’s $27 billion in annual remittances are drying up (Chart I-2, bottom panel). The majority of these transmittals come from Egyptian workers working in Gulf countries. Second, Egypt’s tourism industry – which brings in $13 billion in annual revenues or 4% of GDP – has collapsed due to the pandemic. Tourist arrivals from Middle Eastern countries – which makeup 20% of total tourist arrivals into Egypt – will diminish substantially due to both the pandemic and the negative income shock that the Gulf economies have experienced (Chart I-3). Third, Egyptian exports are in freefall (Chart I-4, top panel). Not only is this due to the freeze in global trade, but also because the country’s exports to the oil-leveraged Arab economies have taken a massive hit. The latter make up 25% of Egypt’s total goods shipments. Chart I-3Egypt: Tourism Is Linked To Oil Prices

Egypt: Tourism Is Linked To Oil Prices

Egypt: Tourism Is Linked To Oil Prices

Chart I-4Exports Revenues Swing With Oil Prices

Exports Revenues Swing With Oil Prices

Exports Revenues Swing With Oil Prices

Furthermore, since 2019 Egypt has been increasingly exporting natural gas. The collapse in gas prices has probably already wiped out a large of chunk its natural gas export revenues (Chart I-5). Chart 6 exhibits the structure of Egypt’s exports of goods and services. Energy, tourism and transportation constituted 67% of total exports in 2019. Chart I-5Gas Export Revenues Are At Risk

Gas Export Revenues Are At Risk

Gas Export Revenues Are At Risk

Chart I-6Egypt: Structure Of Goods & Services Exports

Egypt: A Veiled Oil Play

Egypt: A Veiled Oil Play

Chart I-7Exports Are Shrinking Amid Resilient Imports

Exports Are Shrinking Amid Resilient Imports

Exports Are Shrinking Amid Resilient Imports

Finally, while export revenues have plunged, imports remain resilient (Chart I-7). Critically, 26% of Egypt’s imports are composed of essential and basic items such as consumer non-durable goods, wheat and maize. Consumption of these staples and goods are less sensitive to business cycle oscillations. Therefore, the nation’s current account deficit has ballooned. A wider current account deficit needs to be funded by foreign inflows. With foreign investors reluctant to provide funds, the CBE has lately been financing BoP by depleting its foreign exchange reserves (Chart I-1, on page 1). Foreign Funding Requirements: Not only is Egypt facing a massively deteriorating current account deficit, but the country also carries large foreign funding debt obligations (FDO). FDOs are the sum of debt expiring in the next 12 months, and interest as well as amortization payments over the next 12 months. FDOs due in 2020 were $24 billion.2 In turn, Egypt’s total foreign funding requirements (FFR) – which is the sum of FDOs and the country’s current account deficit – has risen to $33 billion.3 Importantly, this FFR amount is based on the current account for 2019 and, thereby, does not take Egypt’s deteriorating current account deficit into consideration – as discussed above. Meanwhile, the central bank has net FX reserves of only $8 billion.4 If the monetary authorities continue to fund FFR of $33 billion in 2020 to prevent the pound from depreciating, the CBE will soon run out of its net FX reserves. Overall, Chart I-8 compares Egypt to the rest of the EM universe: with respect to (1) exports-to-FDO on the x-axis and (2) foreign exchange reserves-to-FFR on the y-axis. Based on these two measurements, Egypt is among the most vulnerable EM countries in terms of the balance of payments as it has the lowest FX reserves-to-FFR ratio and a low export-to-FDO ratio as well. Chart I-8Egypt Is One Of The Most Exposed EM Countries To Currency Depreciation

Egypt: A Veiled Oil Play

Egypt: A Veiled Oil Play

Chart I-9FDI Inflows Are Set To Diminish

FDI Inflows Are Set To Diminish

FDI Inflows Are Set To Diminish

Foreign Funding of Private Sector: Egypt will struggle to attract private-sector foreign inflows to meet its large FFR amid this adverse regional economic environment and the likely renewed relapse in oil prices in the months ahead. FDI inflows are set to drop (Chart I-9). The oil & gas sector has been the largest recipient of FDI inflows recently (around 55% in 2019 according to the central bank). The crash in both crude oil and natural gas prices will therefore ensure that FDIs into this sector will dry up. Besides, overall FDI inflows emanating from Gulf countries are poised to shrink substantially.5 Chart I-10The Egyptian Pound Is Once Again Expensive

The Egyptian Pound Is Once Again Expensive

The Egyptian Pound Is Once Again Expensive

Foreign Funding of Government: With FDI inflows diminishing, the Egyptian government has once again been forced to approach the IMF for assistance. The country managed to secure $8 billion in assistance from the IMF ($2.8 billion in May and $5.2 in June). This has ameliorated international investor confidence in Egypt. Indeed, the country raised $5 billion by issuing US dollar-denominated sovereign bonds in May. Egypt is now seeking another $4 billion from other international lenders. Crucially, assuming Egypt manages to get the $4 billion loan, which would allow it to raise a total of $17 billion, Egypt would still be short on foreign funding to finance its $33 billion in FFR. Therefore, the currency will come under pressure of devaluation. As we argue below, the nation’s public debt sustainability is in jeopardy unless local currency interest rates are brought down substantially. This can only happen if the currency is allowed to depreciate. Consistently, foreign investors might be unwilling to lend to Egypt until interest rates are pushed lower and the country’s public debt trajectory is placed back on a sustainable path. Finally, the Egyptian pound has once again become expensive according to the real effective exchange rate (REER) which is based on both consumer and producer prices (Chart I-10). Bottom Line: Egypt is facing sharply slowing foreign inflows due to both the crash in oil prices and the global pandemic. This is occurring amid increased FFRs. Meanwhile, the CBE’s net FX reserves are insufficient to defend the exchange rate. Public Debt Sustainability The BoP strains discussed above are forcing the CBE to keep interest rates high to prevent the currency from depreciating. Yet the country’s public debt is on a dangerous path due to elevated interest rates. In turn, without currency devaluation that ultimately allows local interest rates to drop dramatically, the sustainability of Egypt’s public debt will worsen considerably. The BoP strains discussed above are forcing the CBE to keep interest rates high to prevent the currency from depreciating. Yet the country’s public debt is on a dangerous path due to elevated interest rates. To start, Egypt’s public debt stands at 97% of GDP – local currency and foreign currency debt account for 79% and 18% of GDP respectively (Chart I-11, top panel). Chart I-12 illustrates that interest payments on public debt is already using up 60% of government revenue and stands at 10% of GDP. Chart I-11Egypt: Public Debt Profile

Egypt: Public Debt Profile

Egypt: Public Debt Profile

Chart I-12The Government's Interest Payments Are Unsustainable

The Government's Interest Payments Are Unsustainable

The Government's Interest Payments Are Unsustainable

Therefore, if the CBE keeps interest rates at the current level, then the government will continue to pay high interest on its debt. Generally, two conditions need to be met to ensure public debt sustainability in any country (i.e., to ensure that the public debt-to-GDP ratio does not to surge). Nominal GDP growth needs to be higher than government borrowing costs. The government needs to run persistently large primary fiscal surpluses. Chart I-13Egypt: Nominal GDP Growth And Government Borrowing Costs

Egypt: Nominal GDP Growth And Government Borrowing Costs

Egypt: Nominal GDP Growth And Government Borrowing Costs

Regarding the first condition, nominal GDP growth was already dangerously close to the level of Egypt’s government borrowing costs even before the pandemic hit Egypt (Chart I-13). With the pandemic, both domestic demand and exports have plunged. Consequently, nominal GDP is likely close to zero while local currency borrowing costs are above 10%. So long as nominal GDP growth remains below borrowing costs, the public debt sustainability will continue to deteriorate. As to the second condition, Egypt only started running primary fiscal surpluses in 2018 as it implemented extremely tight fiscal policy by cutting non-interest expenditures (Chart I-14). However, that was only possible because economic growth was then strong. As growth has slumped, government revenue is most likely shrinking. Chart I-14Egypt Only Recently Started Running A Primary Fiscal Surplus

Egypt Only Recently Started Running A Primary Fiscal Surplus

Egypt Only Recently Started Running A Primary Fiscal Surplus

Tightening fiscal policy amid the economic downturn will be ruinous. Cutting non-interest expenditures further will depress the already weak economy, drying up both nominal GDP and government revenues even more. This will bring about a vicious economic cycle. Needless to say, the latter option is politically unviable. The most feasible option to ensure sustainability of public debt dynamics is to bring down domestic interest rates considerably. Lower local interest rates will reduce interest expenditures on its domestic debt and will either narrow overall fiscal deficit or free up space for the government to spend elsewhere, boosting much needed economic growth. Meanwhile lower interest rates will boost demand for credit and revive private-sector domestic demand. Provided Egypt’s public debt has a short maturity profile, lower interest rates will reasonably quickly feed into lower interest payments for the government. This means that lower interest rates could reasonably quickly feed to lower interest payments for the government. Importantly, there is a trade-off between the exchange rates and interest rates. Lowering interest rates entail currency depreciation. According to the impossible trinity theory, a central bank facing an open capital needs to choose between controlling interest rates or the exchange rate, it cannot control both simultaneously. As such, if the Central Bank of Egypt opts to bring down local interest rates, while keeping the capital account reasonably open, it needs to tolerate a weaker currency amid its ongoing BoP strains. Bottom Line: Public debt dynamics are treading on a dangerous path. Egypt needs to bring down local interest rates down substantially and rapidly. And in so doing, the CBE cannot control and defend the exchange rate. Devaluation Is Needed All in all, the Egyptian authorities are facing a tight tradeoff: (1) either they continue to defend the currency at the expense of depressing the economy and worsening public debt dynamic, or (2) they tolerate a one-off currency devaluation which would allow the monetary authorities reduce interest rates aggressively. The latter will help stimulate economic growth and make public debt sustainable. Specifically, if the Central Bank of Egypt opts for defending the currency from depreciation, it will need to tolerate much higher interest rates for a long period of time. The CBE would essentially need to deplete whatever little net FX reserves it currently has to fund BoP deficits. This would simultaneously shrink local banking system liquidity, pushing domestic interbank rates higher. All in all, the Egyptian authorities are facing a tight tradeoff: (1) either they continue to defend the currency at the expense of depressing the economy and worsening public debt dynamic, or (2) they tolerate a one-off currency devaluation which would allow the monetary authorities reduce interest rates aggressively. Worryingly, not only would high interest rates devastate the already shaky Egyptian economy, but higher domestic interest rates carry major ramifications for Egypt’s public debt sustainability as discussed earlier. A one-off currency devaluation is painful and carries some political risks yet, it is still the least worst choice for Egypt from a longer-term perspective. Although inflation will spike due to pass-through from currency devaluation, it will be a transitory one-off increase (Chart I-15). Besides, the pertinent risk to the Egyptian economy currently is low inflation and high real interest rates (Chart I-16). Chart I-15Egypt: Currency-Induced Inflation Is A One-Off

Egypt: Currency-Induced Inflation Is A One-Off

Egypt: Currency-Induced Inflation Is A One-Off

Chart I-16Egypt: Real Interest Rates Are High

Egypt: Real Interest Rates Are High

Egypt: Real Interest Rates Are High

In turn, currency depreciation will ultimately provide the CBE with scope to reduce its policy rate which will help stimulate the ailing economy as well as make public debt trajectory more sustainable. Finally, odds are high that Egyptian authorities might choose to devalue the currency sooner rather than later. The basis for this is that the government’s foreign public debt is still relatively small at 18% of the GDP and 19% of the total government debt (Chart I-11, on page 8). Further, the majority (70%) of Egypt’s foreign public debt remains linked to international and bilateral government loans making it easier to renegotiate their terms than in the case of publicly traded sovereign US dollar bonds (Chart I-11, bottom panel). This means that currency depreciation will not materially deteriorate the government’s debt servicing ability. Furthermore, Egypt has experience managing and tolerating currency depreciation. The currency depreciated against the US dollar by 50% in 2016 and before that by 12% in 2013. Bottom Line: The Central Bank of Egypt will not hike interest rates or sell its foreign currency reserves for too long to defend the pound. Odds are high that it will allow the currency to depreciate and will cut interest rates materially. Investment Recommendations Chart I-17Egyptian Pound In The Forward Market

Egyptian Pound In The Forward Market

Egyptian Pound In The Forward Market

Investors should buy Egyptian 3-year local currency bonds while hedging their currency exposure. The basis is that low inflation and a depressed economy in Egypt will lead the CBE to cut rates by several hundred basis points over the next 12 months while allowing currency to depreciate. Forward markets are pricing 5% depreciation in the EGP in the next 6 months and 10% in the next 12 months (Chart I-17). We would assign a higher probability of depreciation. For now, EM credit portfolios should have a neutral allocation on Egyptian sovereign credit. While another potential drop in oil prices and the currency devaluation could push sovereign spreads wider (Chart I-18), eventually large rate cuts by the CBE will make public debt dynamics more sustainable. Absolute return investors should wait for devaluation to go long on Egypt’s US dollar sovereign bonds. Chart I-18Remain Neutral On Egypt's Sovereign Credit

Remain Neutral On Egypt's Sovereign Credit

Remain Neutral On Egypt's Sovereign Credit

Chart I-19Remain Neutral On Egyptian Equities

Remain Neutral On Egyptian Equities

Remain Neutral On Egyptian Equities

Equity investors should keep a neutral allocation on Egyptian stocks with an EM equity portfolio (Chart I-19). Lower interest rates ahead will eventually boost this stock market. Ayman Kawtharani Editor/Strategist ayman@bcaresearch.com 1 This is the view of BCA’s Emerging Markets Strategy service and it differs from the view of BCA’s Commodities and Energy Strategy service. 2 We exclude the Central Bank’s foreign liabilities due in 2020 as they are mostly deposits at the Central Bank of Egypt owed to Gulf countries. It is highly likely that Gulf lenders will agree to extend these deposits given the difficulties Egypt is experiencing. 3 Excluding the Central Bank’s foreign liabilities due in the next 12 months. Please refer to above footnote. 4 The amount of net foreign exchange reserves currently at the Central Bank – i.e. excluding the Bank’s foreign liabilities– are now low at $8 billion. 5 Gulf Co-operation Countries (GCC) are in no position to provide much financial assistance due to the pandemic and oil crash as they are under severe financial strain themselves. Also, GCC countries run strict currency pegs and need to preserve their dwindling foreign exchange reserves to defend their currency pegs to the US dollar.

Chinese economic data continue to reflect the evolution of the global economy. In USD-term Chinese exports contracted 3.3% on a year-on-year basis and imports fell 16.7%. Chinese exports remain more resilient than feared. However, exports of medical…

Highlights Our base case reflects our view that China’s strong fiscal and monetary stimulus, combined with a weaker US dollar, will provide a favorable backdrop for copper markets in 2H20. Supply factors are for the most part reflected in current copper prices. In 2H20, the speed of the demand recovery will be the determining factor for prices. Global policy uncertainty remains high. Assessing the joint effects of global monetary and fiscal stimulus, along with consumers’ willingness to spend once lockdowns are lifted will keep uncertainty at relatively high levels. A possible second wave of COVID-19 returning large economies to lockdown status looms large for copper markets, and for commodity markets generally. The combination of safe-haven demand and a continued dollar shortage for borrowers without access to US swap lines could keep the dollar well bid, suppressing foreign flows to EM economies and commodity demand at the margin. Tactically, we remain on the sidelines until the fog clears around these known and unknown unknowns. A $3/lb COMEX refined copper price is likely in 2H20, but the risks to this outlook remain high. Feature Copper prices will end the year higher vs. current levels in our base case. But uncertainty remains elevated. Copper prices will end the year higher vs. current levels in our base case. But uncertainty remains elevated. Assessing the synchronicity of EM recoveries and the joint effects of global monetary and fiscal stimulus, along with consumers’ willingness to spend once lockdowns are lifted is extremely difficult. Looming over all of these considerations: A possible second wave of COVID-19 returning large economies to lockdown status loom large. Tactically, we remain on the sidelines as the fog clears around some of these known and unknown unknowns. Importantly, our positive view rests on our expectation of a robust recovery in China’s economic activity and, to a lesser extent, in its main export destinations, which were hit later by the pandemic. A weak recovery in China would slow the rate at which the current copper supply surplus subsides. At ~ $2.50/lb, copper prices have recovered significantly since bottoming in March at $2.11/lb on the COMEX. Still, clearing the $3.30/lb double top reached in June 2018 will require either a significant increase in global demand or a sharp contraction in supply, which we do not expect. Copper markets were severely hit by the global pandemic: Prices fell 10% in January, as the case count grew in China – the largest copper-consuming market – followed by another 19% decline as the virus spread globally (Chart of the Week). The intensification of lockdowns globally pushed copper markets to a 60k MT surplus as of March – the latest data reported by the World Bureau of Metal Statistics (WBMS) – from a 20k MT deficit in 2019. Bearish sentiment moved our Tactical Composite Indicator – which captures sentiment, positioning, and momentum dynamics – to oversold territories on in March (Chart 2). Chart of the WeekCopper Prices Were Severely Hit By The Pandemic

Speed Of Demand Recovery Remains Key To Copper Prices

Speed Of Demand Recovery Remains Key To Copper Prices

Chart 2Bearish Sentiment Crushes Copper Prices

Bearish Sentiment Crushes Copper Prices

Bearish Sentiment Crushes Copper Prices

After reaching a low of $2.11/lb on March 23, COMEX copper prices surged 18% with few interruptions as the Chinese economy reopened, and global monetary and fiscal authorities supplied unprecedented economic support (Chart 3). This prompted a wave of short-covering by money managers, releasing some of the downward pressure on prices (Chart 4). Chart 3Unprecedented Fiscal Response

Speed Of Demand Recovery Remains Key To Copper Prices

Speed Of Demand Recovery Remains Key To Copper Prices

Chart 4Money Managers Neutral For Now

Money Managers Neutral For Now

Money Managers Neutral For Now

Still, hedge funds have not yet entered bullish positions on the metal. And, importantly, inventory levels are not drawing sharply. China’s Economy Bottomed, World ex-China Still Contracting Our outlook hinges primarily on our assessment of China’s policy-driven copper demand – both from domestic usage perspective, and, to a lesser extent, from copper-intensive exported goods. Since the end of the Global Financial Crisis (GFC), copper prices have mostly shadowed China’s economic cycles (Chart 5). China’s importance for copper markets now dominates that of major DM countries (Chart 5, panel 3). The influence of global supply-demand fundamentals on copper prices has declined. Prices are increasingly policy-driven with supply adjusting to demand as dictated by Chinese policymakers’ decisions on the allocation of total social financing funds in that economy. Thus, our outlook hinges primarily on our assessment of China’s policy-driven copper demand – both from domestic usage perspective, and, to a lesser extent, from copper-intensive exported goods. According to the International Copper Study Group (ICSG), around 17% of Chinese copper demand comes from exports of products containing copper.1 In “normal” times, we rely heavily on our monthly indicators to gauge economic and commodity cycles. However, the speed with which the COVID-19 pandemic evolves – and the associated fiscal and monetary responses to it – makes short-term forecasting of cyclical commodities a perilous task. Chart 5DM Consumption Pales Vs. China

DM Consumption Pales Vs. China

DM Consumption Pales Vs. China

High-frequency data suggest Chinese economic growth bottomed in March and is rapidly recovering (Chart 6). Chart 6Chinese Economy Returning To Normal

Speed Of Demand Recovery Remains Key To Copper Prices

Speed Of Demand Recovery Remains Key To Copper Prices

Meanwhile in China’s major export destinations, the number of confirmed COVID-19 cases appear to be flattening, containment measures are gradually easing, and mobility is improving (Chart 7, panel 1 and 2). Globally, the copper- and oil-to-gold ratios have stabilized, and stock prices for nine of the largest copper producers have trended up since March 23 (Chart 7, panel 3 and 4). That said, we believe it is still too early to adopt a high-conviction view about a price recovery trajectory. For one, China recently reintroduced containment measures in certain regions, as clusters of coronavirus cases were detected, highlighting the fragility of the current recovery.2 Chart 7China's Major Export Partners Could Rebound Soon

China's Major Export Partners Could Rebound Soon

China's Major Export Partners Could Rebound Soon

Chart 8Strong Domestic Demand, Weak Export Growth

Strong Domestic Demand, Weak Export Growth

Strong Domestic Demand, Weak Export Growth

Moreover, the rebound in overall Chinese demand hasn’t fully offset the collapse in its exports. As a result, the reopening of the supply side of the economy outpaced demand growth (Chart 8). Extrapolating this to its copper market: Chinese refined copper production (40% share of world output) is facing robust domestic demand but weak export demand for copper (44% and 9% of world demand), leaving its market with a supply surplus. Nonetheless, absent a severe second wave of COVID-19 cases, the infrastructure-focused stimulus and market-friendly real estate policies in the country will allow internal demand to overtake production in 2H20, despite limited external demand (more on this below). China’s Credit Growth To Drive Copper Demand Higher The key message emerging from the NPC is that policymakers are willing to do whatever it takes – including abandoning their deleveraging objectives – to reflate the economy. Markets were unimpressed by the fiscal package announced during China’s National People’s Congress (NPC) last month, which, for the first time in decades, did not contain an annual economic growth target in the Government Work Report (Table 1). Even so, the key message emerging from the NPC is that policymakers are willing to do whatever it takes – including abandoning their deleveraging objectives – to reflate the economy. Broad money and total social financing growth will accelerate relative to last year and notably exceed nominal GDP growth. Our Emerging Markets strategists expect China’s fiscal and credit impulse will reach 15.5% this year (Chart 9).3 Table 1No Economic Growth Target In The Government Work Report

Speed Of Demand Recovery Remains Key To Copper Prices

Speed Of Demand Recovery Remains Key To Copper Prices

Additionally, China pledged to stabilize employment and targeted the creation of 9 million new jobs in urban areas. This is an ambitious target amidst the massive layoffs induced by the COVID-19 pandemic this year. Chart 9Chinese Credit Growth Will Surge

Chinese Credit Growth Will Surge

Chinese Credit Growth Will Surge

Policymakers also reserved policy space to be used – without the approval of the NPC at the Politburo’s mid-year review – in the event the shock from the pandemic proves persistent.4 Past episodes of Chinese stimulus resulted in strong rallies in base metals prices. Given China now represents more than half of global copper consumption (vs. 43% in 2009 following the GFC, and 32% in 2012 following the euro area debt crisis), we expect this new round of stimulus will lead to a sharp increase in copper prices.5 By and large, refined copper prices are highly sensitive to growth in EM imports – particularly China’s – which are closely tied to income growth. The latest CPB World Trade Monitor data for March shows EM ex-China imports have been resilient suggesting the rebound in China’s economic activity might be spilling over to other EMs highly leveraged to China (Chart 10). Still, our main cyclical commodity demand indicators were declining as of April. We expect stimulus-driven EM income and investment growth will show up in our indicators in 2H20 (Chart 10). Chart 10Awaiting A Rebound In Our Cyclical Indicators

Speed Of Demand Recovery Remains Key To Copper Prices

Speed Of Demand Recovery Remains Key To Copper Prices

Stalling Primary And Secondary Supply Growth In addition to the demand implications, lockdowns also resulted in restrictions – and few complete shutdowns – in mining activities in copper-producing countries. The ICSG revised down its global mine and refined copper output by 950k MT and 1.1mm MT, respectively, for this year on the back of the COVID-19 pandemic.6 The group now expects 2020 mine supply to decline by 3% this year and refined production to remain flat y/y, for a second consecutive year. While important, these adjustments were insufficient to completely offset the large negative demand shock in 1Q and 2Q20.7 In 2H20, the supply-side outlook rests on the evolution of COVID-19 cases and associated governments’ responses in major ore and refined copper-producing countries (i.e. Chile, Peru, US, DRC, China, Russia, and Japan). So far, mining activities were mostly treated as essential and allowed to operate at reduced capacity under additional sanitary and social distancing guidelines. Confirmed cases in these countries appears to be slowing, this could allow activity to slowly return to normal (Chart 11). Chart 11Further Supply Disruptions Are Unlikely

Speed Of Demand Recovery Remains Key To Copper Prices

Speed Of Demand Recovery Remains Key To Copper Prices

Supply factors are for the most part reflected in current prices. Going forward the speed of the demand recovery will be the determining factor for copper prices. While mining and refining of copper concentrates were often classified as essential, scrap activities were not. According to the ICSG, copper scrap supplied decreased significantly as trade flows and generation, collection, and disassembling activities were disrupted by the pandemic. China’s import of scrap copper – a key input for Chinese refiners – declined 37% in 1Q20. This prompted the government to allow more scrap imports to fill the gap, but it might struggle to find suppliers. Globally, scrap makes up ~ 25% of total refined copper supply, thus, it usually plays a non-negligible role in the rebalancing of global markets. Supply factors are for the most part reflected in current prices. Going forward the speed of the demand recovery will be the determining factor for copper prices. In addition, the crisis began at an abnormally low inventory level. Thus, despite the temporary build in 1Q20, inventories are still below their 2010 to 2019 average. The rebound in demand, combined with flat supply and limited scrap availability, will move Chinese inventory down in 2H20 and offset any builds at the LMEX and COMEX warehouses, supporting copper prices this year (Chart 12). Chart 12Inventories Still Low Despite Builds In 1Q20

Inventories Still Low Despite Builds In 1Q20

Inventories Still Low Despite Builds In 1Q20

USD Depreciation Leads To EM Economic Growth Uncertainty over the duration of lockdowns globally continues to fuel safe-haven demand for USD. As the COVID-19 shock abates we expect a weaker US dollar to be more supportive to copper demand. Uncertainty over the duration of lockdowns globally continues to fuel safe-haven demand for USD (Chart 13). The shortage of USD experienced by EM debtors servicing dollar-denominated debt continues to hamper their recovery. The combination of safe-haven demand and a continued dollar shortage for borrowers without access to US swap lines is keeping the dollar well bid, suppressing foreign flows to EM economies and commodity demand at the margin (Chart 14, panel 1). Chart 13Global Financial Cycles Hurting EM Economies

Speed Of Demand Recovery Remains Key To Copper Prices

Speed Of Demand Recovery Remains Key To Copper Prices

Chart 14Uncertainty Keeps USD Well Bid

Uncertainty Keeps USD Well Bid

Uncertainty Keeps USD Well Bid

The Fed will continue to accommodate USD demand, in an ongoing attempt to reverse a tightening of global financial conditions. EM economies – the bulk of base metals demand growth – are facing dual domestic demand and global financial shocks.8 These economies have become more dependent on foreign portfolio inflows, both in debt and equity markets (Chart 14, panel 2). Thus, global financial cycles now have a significant impact on their growth. The main factors influencing these flows are risk appetite, EM exchange rates, and DM interest rates.9 We expect all factors to support inflows to emerging markets as the COVID-19 shock abates. The Fed will continue to accommodate USD demand, in an ongoing attempt to reverse a tightening of global financial conditions. A lower USD will decrease the local-currency cost of consuming commodities ex-US. Metals producers' ex-US will face higher local-currency operating costs, reducing supply growth at the margin. A depreciating USD is a necessary factor for our bullish cyclical commodities view (Chart 15). The risk to this view is a severe second wave of COVID-19 infection which would cause safe assets to spike anew. Chart 15Metals Inversely Correlated With The US Dollar

Metals Inversely Correlated With The US Dollar

Metals Inversely Correlated With The US Dollar

$3.00/lb Copper Price Likely; Geopolitical Risks Mounting Over the short term, geopolitical risks – chiefly mounting Sino-US tensions – could derail the rally in copper prices and other risk assets. For April, our copper demand model suggested prices were at equilibrium relative to underlying demand trends (Chart 16). Chart 16Copper Prices Will Rise As The USD Depreciates

Copper Prices Will Rise As The USD Depreciates

Copper Prices Will Rise As The USD Depreciates

When simulating a 10% decline in the USD and a rebound in EM import growth in 2H20, our model suggests COMEX copper prices could move 25% higher, holding everything else constant. In reality, the USD’s path and the extent of the EM import rebound are among the key known unknowns we confront in estimating a model for copper prices. We do not have a precise view on these variables, which is why we run simulations. Theory would suggest the stimulus we are seeing globally points to a lower USD and a pick-up in EM imports, however, and these factors will create a more supportive environment for metals prices. Over the short term, geopolitical risks – chiefly mounting Sino-US tensions – could derail the rally in copper prices and other risk assets. With the US election now only 5 months away, President Trump’s odds of being reelected on the back of a strong economy are fading amidst the COVID-19 pandemic. According to our Geopolitical strategists, Trump is the underdog and will need to double down on foreign and trade policies to prop-up his chances of winning. Meanwhile, China is seeking to solidify its sphere of influence.10 This is causing US-China tensions to intensify. Depending on the nature of the actions taken by the Trump administration (i.e. increasing tariffs on US imports of Chinese goods vs. cutting China’s access to foreign technology), metals prices could suffer, as was the case in 2018. With these geopolitical risks in mind, we maintain that China’s strong fiscal and monetary stimulus, combined with a falling US dollar will provide a favorable backdrop for copper markets in 2H20. Hugo Bélanger Senior Analyst Commodity & Energy Strategy HugoB@bcaresearch.com Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Commodities Round-Up Energy: Overweight Doubts about OPEC 2.0’s commitment to extending their deepest-ever production cuts expiring this month to July, perhaps August, took some of the steam out of crude-oil rally earlier in the week. In our modeling, we do not see the need to extend the massive voluntary cuts announced by the Kingdom of Saudi Arabia (KSA) and its Gulf allies: KSA’s cuts of ~ 4.5mm b/d vs. its April output level of 12mm b/d starting this month will take the Kingdom’s output to ~ 7.5mm b/d. The UAE and Kuwait also voluntarily added cuts of 100k and 80k b/d, respectively, to their agreed quotas. We continue to believe the current schedule of production cuts will result in a physical supply deficit in 3Q20, which will require OPEC 2.0 to begin raising production to keep prices from getting too high going into a US presidential election. We expect Brent prices to average $40/bbl this year and $68/bbl next year, with WTI trading $2 - $4/bbl below that (Chart 17).11 Base Metals: Neutral Iron ore prices breached $100/MT this week, as COVID-19-induced supply disruptions in Brazil – the largest exporter of high-grade ore – and South Africa leave the seaborne market open to Australian suppliers to meet higher Chinese demand as port inventories are rebuilt. FastMarkets MB, a sister company of BCA Research, reported May exports to China from Brazil were down 28% y/y to 21.5mm MT from just under 30mm MT the year prior. Iron ore exports from Australia are expected to exceed A$100 billion this year, according to government estimates reported by the Financial Times.12 Precious Metals: Neutral As we go to press, gold prices retreated to $1,700/oz from ~ $1,740/oz last week, exhibiting a positive correlation with the dollar. This is a result of rising risk appetite globally as economies exit lockdowns. In the US, interest rates are continuing to support gold. Going forward, the probability of negative rates is remains low, but the Fed will continue to buy more debt from the public and private sectors to push the shadow rate further down. This supports gold prices (Chart 18). Chart 17Crude Prices Will Rebound

Crude Prices Will Rebound

Crude Prices Will Rebound

Chart 18Fed Buying Supports Gold Prices

Fed Buying Supports Gold Prices

Fed Buying Supports Gold Prices

Footnotes 1 Please see “The Impact of the COVID-19 Pandemic on World Copper Supply,” published by the International Copper Study Group on May 21, 2020. 2 A resurgence of infection triggered renewed lockdowns over a region of 100 million people in May. Please see More than 100 million people in China's northeast back under lockdown to thwart potential second wave published by the National Post on May 19, 2020. 3 Please see BCA's Emerging Markets Strategy Weekly Report "EM Stocks Are At A Critical Resistance Level," published May 28, 2020. It is available at ems.bcaresearch.com. 4 Please see BCA's China Investment Strategy Weekly Report "Taking The Pulse Of The People’s Congress," published May 28, 2020. It is available at cis.bcaresearch.com. 5 There remains a risk global monetary stimulus fails to ignite strong consumer and business consumption. The unprecedented shock could raise precautionary savings and keep risk aversion elevated for an extended period. Based on the Quantity Theory of Money, money supply times velocity (the rate at which money changes hands) equals nominal GDP. Low confidence translates to a low velocity of money limiting the reach of monetary policy. This value is extremely difficult to forecast. 6 Please see “The Impact of the COVID-19 Pandemic on World Copper Supply,” published by the International Copper Study Group on May 21, 2020. 7 According to BGRIMM Lilan Consulting, China’s real demand for refined copper declined by ~22% in 1Q20. This implies a ~11% decline in global copper consumption. Please see footnote 6 for more details. 8 Global financial cycles capture how global financial conditions affect individual economies. The analysis of these cycles stressed the importance of common factors in global risk asset prices which are driven by risk appetite and US monetary policy. These factors are mainly explained by developments in advanced economies but have a drastic effect on emerging markets. Please see Iñaki Aldasoro, Stefan Avdjiev, Claudio Borio and Piti Disyatat (2020). “Global and domestic financial cycles: variations on a theme,” BIS Working Papers, No 864. 9 Please see Chapter 3 of the Global Financial Stability Report titled “Managing Volatile Portfolio Flows,” published by IMF. 10 Please see BCA's Geopolitical Strategy Weekly Report "Spheres Of Influence (GeoRisk Update)," published May 29, 2020. It is available at gps.bcaresearch.com. 11 Please see our May 21, 2020 report entitled US Politics Will Drive 2H20 Oil Prices for our latest view on oil fundamentals and prices, available at ces.bcaresearch.com. 12 Please see Australia’s iron ore miners exploit supply gap as Covid-19 hobbles rivals published by the Financial Times June 3, 2020. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Trade Recommendation Performance In 2020 Q1

Speed Of Demand Recovery Remains Key To Copper Prices

Speed Of Demand Recovery Remains Key To Copper Prices

Commodity Prices and Plays Reference Table Trades Closed in 2020 Summary of Closed Trades

Speed Of Demand Recovery Remains Key To Copper Prices

Speed Of Demand Recovery Remains Key To Copper Prices

Highlights Risks assets have entered a FOMO-driven mania phase that could last for a few more weeks. Markets are ignoring the particularities of this recession and are treating the post-lockdown activity snapback as a V-shaped recovery. A weaker than expected global recovery and rising geopolitical tensions between the US and China are the two primary risks that will weigh on EM risk assets after this mania phase runs out of steam. We are upgrading EM sovereign and corporate credit from underweight to neutral within a global credit portfolio. Within EM, local rates will perform well in both risk-on and risk-off phases. Feature The recovery in global risk assets has entered a fear-of-missing-out, or FOMO, mania phase. Like any mania, this one could last longer and go further than any fundamental analysis could presume. Investors who are long or cannot afford to stay on the sidelines should play this rally with tight stop points. Investors with longer time horizon should wait for a pullback in EM equities and currencies to buy. Within EM, local rates offer the best risk-reward profile. A recovery in global trade and mainland industrial sectors is necessary for EM equities and currencies to rally on a sustainable basis. The global equity rally has taken place amid a shrinking forward EPS. The top panel of Chart I-1 demonstrates that even the ever-bullish bottom-up analysts have been cutting their expectations of the level of corporate 12-month forward earnings per-share. As a result, the global forward P/E ratio has spiked to a 18-year high (Chart I-1, bottom panel). Chart I-1An Unprecedented Divergence: Surging Stocks Prices Amid Plunging Forward EPS Levels

An Unprecedented Divergence: Surging Stocks Prices Amid Plunging Forward EPS Levels

An Unprecedented Divergence: Surging Stocks Prices Amid Plunging Forward EPS Levels

Chart I-2EM Forward EPS Level Has Been Falling

EM Forward EPS Level Has Been Falling

EM Forward EPS Level Has Been Falling

Chart I-2 illustrates that the same phenomenon is true for EM equities. Their forward EPS has been contracting and their forward P/E has jumped to a decade high. Any overdrive in asset prices without supporting fundamentals can last for a while but typically ends with a crash. This FOMO-driven mania is unlikely to be any different. It is fair to say that during the March carnage, many investors operated on a “sell now, think later” principle. Since the rally began, they have switched to a “buy now, ask questions later” attitude. As this rally persists, global stocks and credit will become overbought and expensive. At that point, any negative shock could produce a sharp pullback that would likely devolve into another nasty selloff as investors shift back to a “sell now, think later” mentality. The Narratives Driving The Rally The narratives supporting this mania are simple and seem to be both accepted and embraced by a growing number of investors. We agree with some and disagree with others: Economies around the world are opening, which will ensure that an economic recovery will follow. Our interpretation: Surely as confinement policies are eased, activity will improve. However, in our opinion, this should not come as a surprise to investors. This is especially pertinent for the trend-setting US stock market. With US equity valuations not particularly cheap, the market was never pricing in extended lockdowns. Hence, it appears strange to us that markets have so exuberantly cheered the reopening of the economy. Looking forward, the key to the medium-term (six-month) equity outlook is the shape of the recovery following the initial partial normalization. The latter presently looks V-shaped because as stores and businesses reopen economic activity is bound to improve. Yet the odds are that following this initial normalization, the shape of the recovery is most likely to be U-shaped. For what it’s worth, manufacturing PMIs in export-oriented economies like Korea, Japan and Taiwan made new lows in May (Chart I-3). We are not suggesting these indicators will not improve in the months ahead; they surely will. Nevertheless, a marginal rise in diffusion indexes like PMIs from extraordinary depressed levels do not signify a profit recovery. This recession differs from previous ones as the level of business activity has dropped below breakeven points for more businesses than it did in other recessions. When a company operates below its breakeven level, a marginal rise in sales may not be sufficient to improve its debt-servicing capacity, hiring and capital spending intentions. However, it seems markets are ignoring the particularities of this recession and are treating the post-lockdown activity snapback as a V-shaped recovery. This is why we feel risk assets are in a FOMO-driven mania phase, where fundamentals do not matter. Authorities around the world are stimulating, with the US pumping enormous amounts of fiscal and credit stimulus into the economy (Chart I-4, top panel). Chart I-3Asian Manufacturing PMIs Made New Lows In May

Asian Manufacturing PMIs Made New Lows In May

Asian Manufacturing PMIs Made New Lows In May

Chart I-4An Unparalleled Global Money Boom

An Unparalleled Global Money Boom

An Unparalleled Global Money Boom

Chart I-5China Is Ramping Up Stimulus

China Is Ramping Up Stimulus

China Is Ramping Up Stimulus

China has finally embarked on aggressive stimulus. The National People’s Congress has set the monetary policy objective for 2020 as follows: Substantially accelerate the growth of broad money supply and total social financing (Chart I-4, bottom panel). Our interpretation: Indeed, government stimulus worldwide is massive. Yet, it is hard to know if it will be sufficient to produce a V-shaped recovery. The rise in money supply at the moment is being offset by the drop in the velocity of money. As a result, nominal GDP levels are extremely low. That said, last week we upgraded our growth outlook for China because of the above-mentioned aggressive policy stimulus. It is possible that China’s credit and fiscal impulse will reach about 15% of GDP before year-end (Chart I-5). What presently deters us from recommending outright long positions in China-related plays is the escalating US-China confrontation and the risk of a relapse in global stocks. Central banks around the world both in DM and EM are monetizing debt and injecting immense liquidity into the system. Our interpretation: Correct, but equally relevant is investors’ animal spirits. The latter will determine whether and when these liquidity injections leak into risk assets. For now, it seems that once again central banks’ actions have been successful in lifting asset prices, despite poor fundamentals. Equity valuations are cheap, especially outside the US. This is especially true given the low risk-free rate. Our interpretation: We agree that EM equities are cheap, something we have been highlighting since mid-March (Chart I-6). Yet valuations are not a good timing tool, as they can stay depressed so long as profits are not worsening. Meanwhile, US equities are expensive (Chart I-7). Critically, we argued in a recent report that equity multiples depend not only on the risk-free rate but also on the equity risk premium (ERP). Chart I-6EM Equities Are Cheap

EM Equities Are Cheap

EM Equities Are Cheap

Chart I-7US Stocks Are Expensive

US Stocks Are Expensive

US Stocks Are Expensive

Given the immense ambiguities investors are facing with respect to both the business cycle and economic, political and geopolitical trends, the ERP should be at the upper end of its historical range. Hence, the discount factor – the sum of the risk-free rate and the ERP – should be reasonably high. In this context, US equity valuations are rather expensive, despite the very low risk-free rate. In short, the expensive US stock market has until very recently been the locomotive of this rally. If US share prices had not rallied hard in the past two months, EM and other international bourses would not have caught a bid. The Fed’s public debt monetization is a structural, not near-term negative for the greenback. The US dollar is expensive and will depreciate a lot due to unrestrained fiscal and monetary stimulus in the US. Our interpretation: The US dollar is one standard deviation expensive (Chart I-8) and EM currencies have become cheap (Chart I-9). Chart I-8US Dollar Valuations Are Elevated

US Dollar Valuations Are Elevated

US Dollar Valuations Are Elevated

Chart I-9EM Currencies Are Cheap

EM Currencies Are Cheap

EM Currencies Are Cheap

Chart I-10EM Currencies And Stocks Correlate With Industrial Metals

EM Currencies And Stocks Correlate With Industrial Metals

EM Currencies And Stocks Correlate With Industrial Metals

We do not disagree with the view that the US dollar is vulnerable in the long term due to the Federal Reserve’s aggressive debt monetization and that the Fed will eventually fall behind the inflation curve. Yet inflation is not imminent, and the Fed’s public debt monetization is a structural, not near-term negative for the greenback. As such, these potholes for the US dollar may not be pertinent in the next several months. Critically, Chart I-10 illustrates that EM currencies move with industrial metals prices, and EM stocks correlate with global materials stocks. The common driver of all of these markets is global growth in general and China’s industrial sectors in particular. In short, a recovery in global trade and mainland industrial sectors is necessary for EM equities and currencies to rally on a sustainable basis. Investors are underinvested in global equities in general and cyclical plays in particular. Our interpretation: Indeed, we showed last week that institutional equity investors had been skeptical of this rally. What has driven or supercharged this equity rally since late March has been unsophisticated retail investors. They have been opening up broker accounts worldwide and aggressively trading since March lockdowns. We cited a few pieces of anecdotal evidence confirming this phenomenon in last week’s report. However, it seems that institutional investors in recent weeks have capitulated by raising their risk exposure in general and their exposure to cyclical plays in particular. This explains the recent surge in cyclical equities and currencies. Bottom Line: The narratives driving this rally are only partially correct. Markets are ignoring the particularities of this recession and are treating the post-lockdown activity snapback as a V-shaped recovery. A weaker than expected global recovery and rising geopolitical tensions between the US and China are the two primary risks that will weigh on EM risk assets after this FOMO-driven mania phase runs out of steam. Nuances To Beware Of There are several nuances about the market’s internals and characteristics that we would like to draw investors’ attention to: There is mixed evidence as to whether China’s economy in general and its industrial sectors in particular have entered a sustainable recovery. First, examining the Taiwanese manufacturing PMI data could help in assessing the growth outlook for both the mainland economy and for global trade. The basis is that Taiwan has done extremely well by avoiding COVID-19 outbreaks and lockdowns. Therefore, there are no domestic reasons for weak output growth. In addition, its manufacturing sector is very export-oriented, with about 40% of exports destined for mainland China. PMI export orders for Taiwan's aggregate manufacturing and its three key sectors plunged to new lows in May (Chart I-11). This includes both the electronic optical (semiconductor) and basic materials sectors. The latter correlates well with global materials stocks. There has so far not been a bullish signal from this indicator (Chart I-11, second panel). Second, China’s domestic A-share market in general and its cyclical sectors in particular have not yet broken out (Chart I-12). Given China was the first nation to exit from lockdowns, its share prices should be the first to signal a sustainable economic recovery. Yet onshore share prices have been rather subdued. China’s economy will eventually stage a recovery later this year. Our point is that global cyclicals might have run ahead of themselves by pricing in a recovery too early. Chart I-11Taiwanese Manufacturing PMIs In May: New Lows Across All Industries

Taiwanese Manufacturing PMIs In May: New Lows Across All Industries

Taiwanese Manufacturing PMIs In May: New Lows Across All Industries

Chart I-12Chinese Onshore Share Prices Are Not Flagging An Imminent Recovery

Chinese Onshore Share Prices Are Not Flagging An Imminent Recovery

Chinese Onshore Share Prices Are Not Flagging An Imminent Recovery

Equity market and sector leadership changes occur during selloffs or at the inception of rallies. Chart I-13 illustrates EM relative stock prices versus DM along with the global equity index. Over the past 25 years, there have been several major leadership changes between EM and DM. And all of them occurred during selloffs in global share prices. Chart I-13EM Versus DM Equity Leadership Rotations Took Place During Selloffs

EM Versus DM Equity Leadership Rotations Took Place During Selloffs

EM Versus DM Equity Leadership Rotations Took Place During Selloffs

Similarly, the relative performance of global growth versus value stocks experiences trend reversals during global bear markets (Chart I-14). Chart I-14Global Growth Versus Value Leadership Rotations Occurred During Bear Markets

Global Growth Versus Value Leadership Rotations Occurred During Bear Markets

Global Growth Versus Value Leadership Rotations Occurred During Bear Markets

Chart I-15EM Could Outperform DM For A Few Weeks

EM Could Outperform DM For A Few Weeks

EM Could Outperform DM For A Few Weeks

Leadership of US equities and global growth stocks did not change during the March crash nor during the following two-month rally from the bottom. Only in the past week or so have US equities and global growth stocks begun to lag EM bourses and global value, respectively (Chart I-15). In brief, the latest leadership rotation from US to EM did not occur during the selloff or at inception of the rally – i.e., it does not fit the typical profile of sustainable leadership reversal. As such, it may not be enduring. The internals of this rally are consistent with the fact that it might already be at a late stage. During rallies, laggards are the last to catch a bid. Contrarily, during selloffs, outperformers are the last to be liquidated. For example, US growth stocks were the last ones to be liquidated in both the 2015-early-2016 and 2018 selloffs. When the decade-long leaders – US growth stocks – were finally stamped out, it marked the bottom of those selloffs. We are upgrading EM sovereign and corporate credit from underweight to neutral within a global credit portfolio. The Fed’s purchases of US bonds will likely continue pushing investors into EM credit markets. Using an analogous framework for this rally, the latest extraordinary spike in the laggards such as EM, Europe and both value and cyclical stocks could be a sign of bear capitulation, and could signify the final phase of this equity rally. Bottom Line: There are several nuances to the current equity market rally, but investors seem reluctant to consider them amid a FOMO-driven mania. Investment Considerations The FOMO-driven rally could last for several more weeks. Afterwards it will be followed by a major setback. Investors who are long or cannot afford to stay on the sidelines should play this rally with tight stop points. Investors with longer time horizon should wait for a pullback in EM equities and currencies to buy. Chart I-16EM Local Rates Offer Value

EM Local Rates Offer Value

EM Local Rates Offer Value

We are making the following adjustments and changes to our strategy and trade recommendations: In regard to our EM versus DM asset allocation strategy, we are making one change: we are upgrading EM sovereign and corporate credit from underweight to neutral within a global credit portfolio. The Fed’s purchases of US bonds will likely continue pushing investors into EM credit markets. Consistently, we are closing two positions: (1) our short EM corporate and sovereign credit / long US investment-grade corporate bond trade; and (2) our long Asian investment-grade /short high-yield corporate bond trade. Within the EM credit space, we continue to favor sovereigns versus corporates – a strategy recommended on April 23. We are still reluctant to strategically upgrade EM stocks versus DM ones even though odds of EM outperforming DM stocks are high in the coming weeks. In light of the potential FOMO-driven rally, to protect profits we are closing the following two currency positions: Take profits on short BRL/long USD trade. It was initiated on November 29, 2019 and has produced a 19% gain. Book profits on short SGD/long JPY position. This recommendation has generated a 2.3% gain since its initiation on June 8, 2018. We are still maintaining shorts in the following EM currencies: CLP, ZAR, TRY, IDR, PHP and KRW. They could continue rallying in the near term but will relapse afterwards. We are also structurally short low beta currencies: the RMB and the Saudi riyal. Within EM, local rates offer the best risk-reward profile: they will perform well in both risk-on and risk-off phases. Real bond yields remain somewhat elevated in many EMs, as shown in Chart I-16. We continue to receive long-term rates in Mexico, Colombia, Russia, Ukraine, India, Pakistan, Malaysia, China and Korea, as well as 2-year rates in South Africa. Their central banks will reduce policy rates much further. In addition, several of these local bond markets will benefit from ongoing quantitative easing by their central banks. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

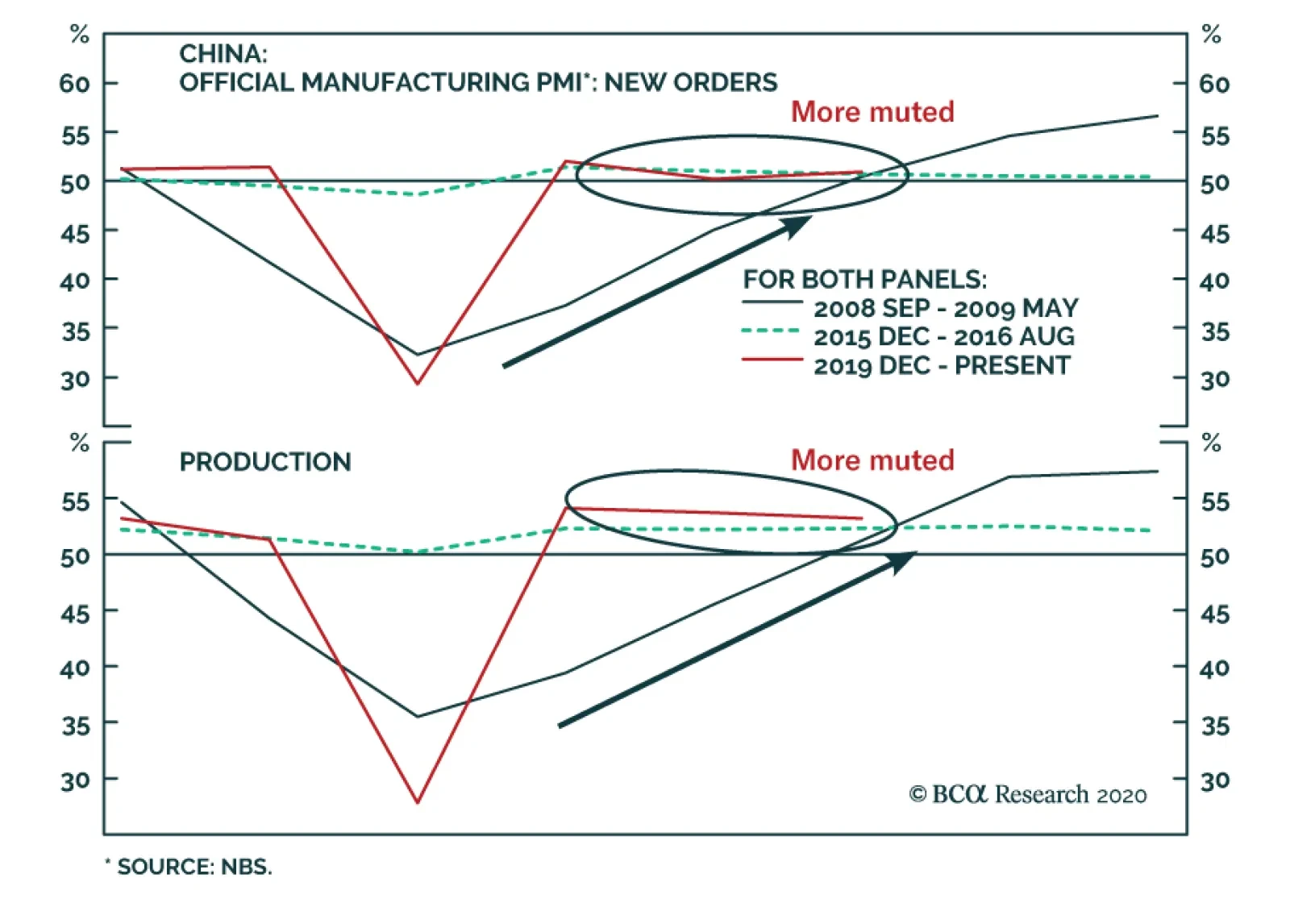

BCA Research's China Investment Strategy service shows that demand is struggling to outpace supply. China’s official manufacturing PMI slipped to 50.6 in May from 50.8 a month earlier. While the reading suggests that manufacturing activities are still in an…

Highlights The Chinese economy continues to recover, albeit less quickly than the first two months following a re-opening of the economy. The demand side of the Chinese economic recovery in May marginally outpaced the supply side, with a notable improvement concentrated in the construction sector. We are initiating two new trades: long material sector stocks versus the broad indices, in both onshore and offshore equity markets. Feature The recovery in China’s economy and asset prices has entered a “tapering phase”, in which the speed of the recovery is normalizing from a rapid rebound two months after the economy re-opened. The direction of the ultra-accommodative monetary and fiscal stance has not changed, but the aggressiveness in the stimulus impulse is abating as the recovery continues. As we highlighted in last week’s report, the announced stimulus at this year's NPC was less than meets the eye of investors.1 Chart 1A Quick Reversal In The Outperformance Of Chinese Stocks

A Quick Reversal In The Outperformance Of Chinese Stocks

A Quick Reversal In The Outperformance Of Chinese Stocks

Near-term downside risks in Chinese stocks were highlighted by last week’s quick reversal in the outperformance of Chinese equities relative to global benchmarks (Chart 1). As the US and European economies re-open and the stimulus impulse in major developed markets (DMs) is at peak intensity, Chinese stocks will underperform those in DMs, particularly US stocks. The re-escalation in Sino-US tensions will also add to the near-term volatility in Chinese equities. Therefore, we maintain our tactical (0-3 months) neutral view on aggregate Chinese equity indexes, in both domestic and offshore markets. Beyond Q2, however, our baseline view still supports an outperformance in Chinese stocks. The stepped-up stimulus measures since March should start to trickle down into the broader economy. Global business activities and demand will slowly normalize in the summer, helping to revive China’s exports. Moreover, an intensified pressure on employment, indicated in this month’s employment subcomponents in manufacturing and non-manufacturing PMIs, should prompt policymakers to roll out more growth-supporting measures in Q3. Tables 1 and 2 below highlight key developments in China’s economic and financial market performance in the past month. Table 1China Macro Data Summary

China Macro And Market Review

China Macro And Market Review

Table 2China Financial Market Performance Summary

China Macro And Market Review

China Macro And Market Review

Chart 2ASpeed Of Manufacturing Activity Recovery Has Moderated

Speed Of Manufacturing Activity Recovery Has Moderated

Speed Of Manufacturing Activity Recovery Has Moderated

China’s official manufacturing PMI slipped to 50.6 in May from 50.8 a month earlier (Chart 2A). While the reading suggests that manufacturing activities are still in an expansionary mode, the speed of the expansion has moderated compared with April and March. The supply side of manufacturing activities and employment were the biggest drags on May’s official PMI. The production subcomponent in the PMI decelerated whereas new orders increased from April (Chart 2A, bottom panel). The net result is an improved supply-demand balance in the manufacturing sector, however, the improvement is marginal. It also differs from the V-shaped recovery in 2008/09, when both new orders and production subcomponents grew simultaneously (Chart 2B). The demand side of the economy is still concentrated in the policy-driven construction sector. The rebound in construction PMI continues to significantly outpace that in manufacturing and non-manufacturing PMIs (Chart 2C, top panel). The construction employment sub-index ticked up by 1.7 percentage points in May, compared with a slowdown of 0.8 percentage points in manufacturing and 0.1 percentage points in non-manufacturing employment PMIs (Chart 2C, bottom panel). Chart 2BDemand Struggles To Outpace Supply

Demand Struggles To Outpace Supply

Demand Struggles To Outpace Supply

Chart 2CDemand Recovery Is Concentrated In Construction

Demand Recovery Is Concentrated In Construction

Demand Recovery Is Concentrated In Construction

While a buoyant construction sector should provide a strong tailwind to raw material prices and related machinery sales, a laggard recovery from other sectors means the upside potential in aggregate producer prices (PPI) will be limited in the current quarter. In May, there was a rebound in the PMI sub-indices measuring raw material purchase prices and ex-factory prices, which heralds easing in the contraction of PPI in Q2 (Chart 3). However, neither of the PMI price sub-indices has returned to levels reached in January, when PPI growth was last positive. Moreover, weaker readings in the purchases and raw material inventory subcomponents suggest that manufacturers may be reluctant to restock due to sluggish global trade and a lagging rebound in domestic demand (Chart 3, bottom panel). This month’s PMI shows that the employment subcomponents in both the manufacturing and non-manufacturing PMIs are contracting (Chart 4). Because demand for Chinese export goods remains sluggish, we expect unemployment in China’s labor-intensive export manufacturing sector to rise in Q2 and even into Q3. The intensified pressure on employment will likely prompt Chinese policymakers to roll out more demand-supporting measures. Chart 3PPI Contraction Will Ease But Upside Limited In Q2/Q3

PPI Contraction Will Ease But Upside Limited In Q2/Q3

PPI Contraction Will Ease But Upside Limited In Q2/Q3

Chart 4Employment In Trouble, A Catalyst For More Easing

Employment In Trouble, A Catalyst For More Easing

Employment In Trouble, A Catalyst For More Easing

The BCA Li Keqiang Leading Indicator rose moderately in April. A plunge in the Monetary Conditions Index (MCI) limited the magnitude of the indicator's increase, offsetting an uptick in money supply and credit growth (Chart 5). A rapid disinflation in headline consumer prices (CPI) since the beginning of this year has pushed up the real savings deposit rate, which contributed to the MCI’s nose-dive. In our view, the MCI’s sharp drop is idiosyncratic and does not signify a tightening in the PBoC’s monetary stance or overall monetary conditions. Huge fluctuations in food prices have been driving the headline CPI since March 2019, while the core CPI remains stable. While food prices historically have very little correlation with the PBoC's monetary policy actions, a disinflationary environment will provide the central bank more room for easing. Odds are high that the PBoC will cut the savings deposit rate for the first time since 2015. Chart 5Monetary Conditions Are Not As Tight As The Indicator Suggests

Monetary Conditions Are Not As Tight As The Indicator Suggests