Emerging Markets

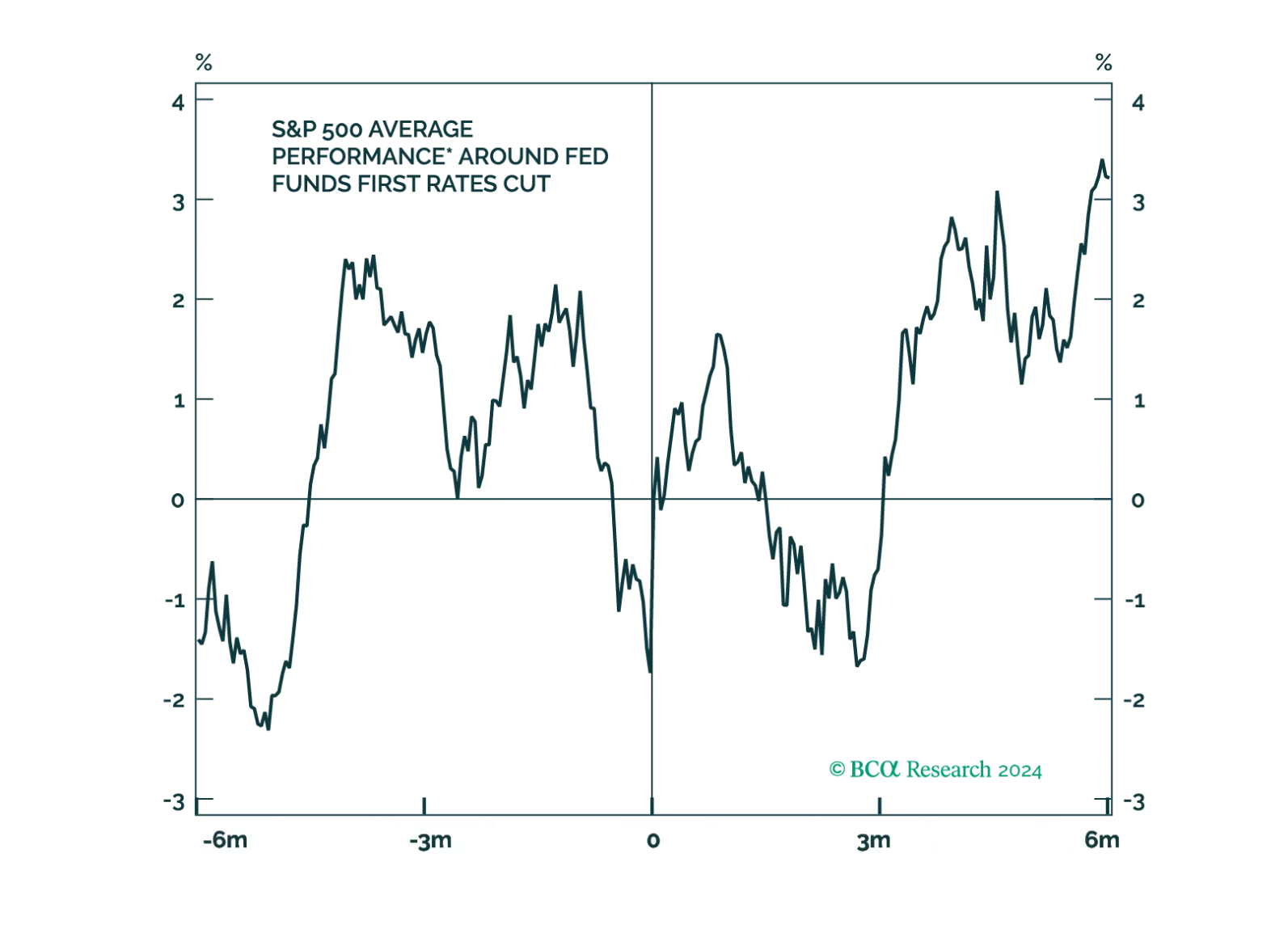

Even after the Fed cuts rates, policy will remain restrictive for some time. Moreover, in history, stocks have tended to fall around the first rate cut. We remain cautious on the outlook for the economy and risk assets.

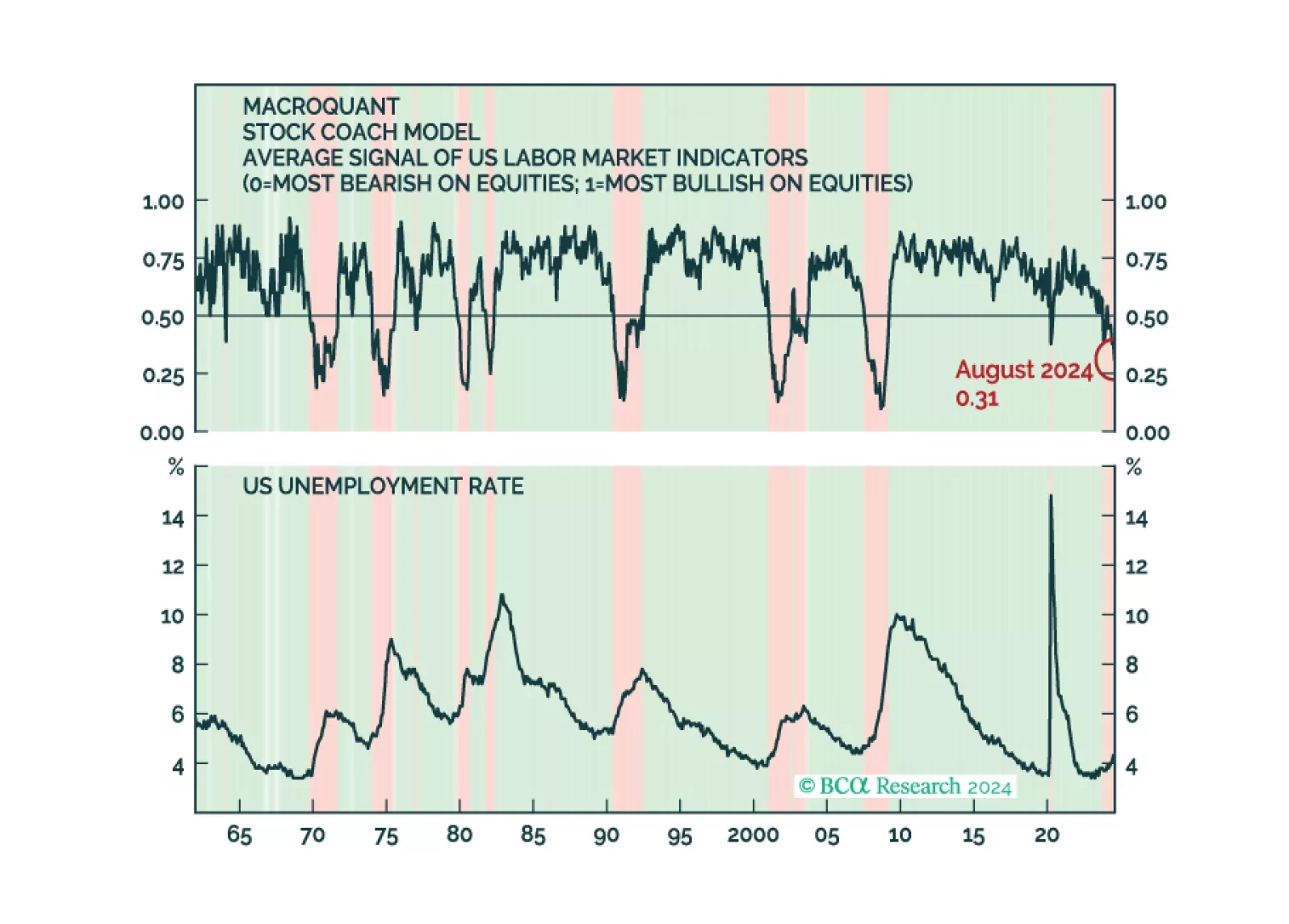

MacroQuant continues to recommend underweighting equities and overweighting bonds. This is consistent with the Global Investment Strategy Team's decision to downgrade global equities to underweight in late June.

Chinese onshore and offshore bank stocks have outperformed their respective broad markets by 26% and 24% since October. Despite deteriorating return on assets, return on equity and net interest margins, investors have sought out their high dividend yields and…

China has notably diversified its export markets over the past two decades, reducing its dependence on the US and other DM economies and strengthening trade ties with EM nations. Since 2000, shipments to the US have halved (from 30% to 16% of total…

The Asian currency index (ADXY index) rose nearly 3% from its late-July lows. While CNY/USD accounted for a large share of these gains, an equal-weighted basket of non-CNY Asian currencies surged by an even larger margin (5%) indicating that Asian currencies’…

According to BCA Research’s Commodity & Energy Strategy service, oil markets are caught in a tug-of-war that has kept oil prices in a trading range since H2 2023. Bearish demand concerns are enforcing an upper limit on the price of crude while bullish…

Chinese industrial profits rose by 4.1% y/y (3.6% YTD y/y) in July, from 3.6% (3.5%) in June. Upstream mining industries’ profits contracted 9.5% from January to July 2024, whereas downstream manufacturing sectors’ profits rose 5.0%. The NBS reported that…

Brazilian equities have largely underperformed their EM peers in USD terms since the beginning of the year. Rising public debt and inflation are the two main forces weighing on the Brazilian bourse. Our Emerging Market strategists expect public debt-to-GDP…

According to BCA Research’s Geopolitical Strategy service, the logic of pursuing one’s interest against US interests in the final hours of the election mostly applies to states that will suffer a significant loss to their strategic security if the…