Emerging Markets

We assess where emerging markets debt is on a strategic and cyclical basis. We find it has benefited from local central banks boosting their inflation-fighting credentials and governments improving financial stability. As a result, EM debt is behaving less like a risk-on asset, changing the role it plays in a global portfolio. We also expand our asset allocation playbook by assessing how the asset class behaves across the business cycle. While EM debt is more than a risk-on play, we suggest investors stay cautious on a cyclical horizon.

Our Portfolio Allocation Summary for March 2024.

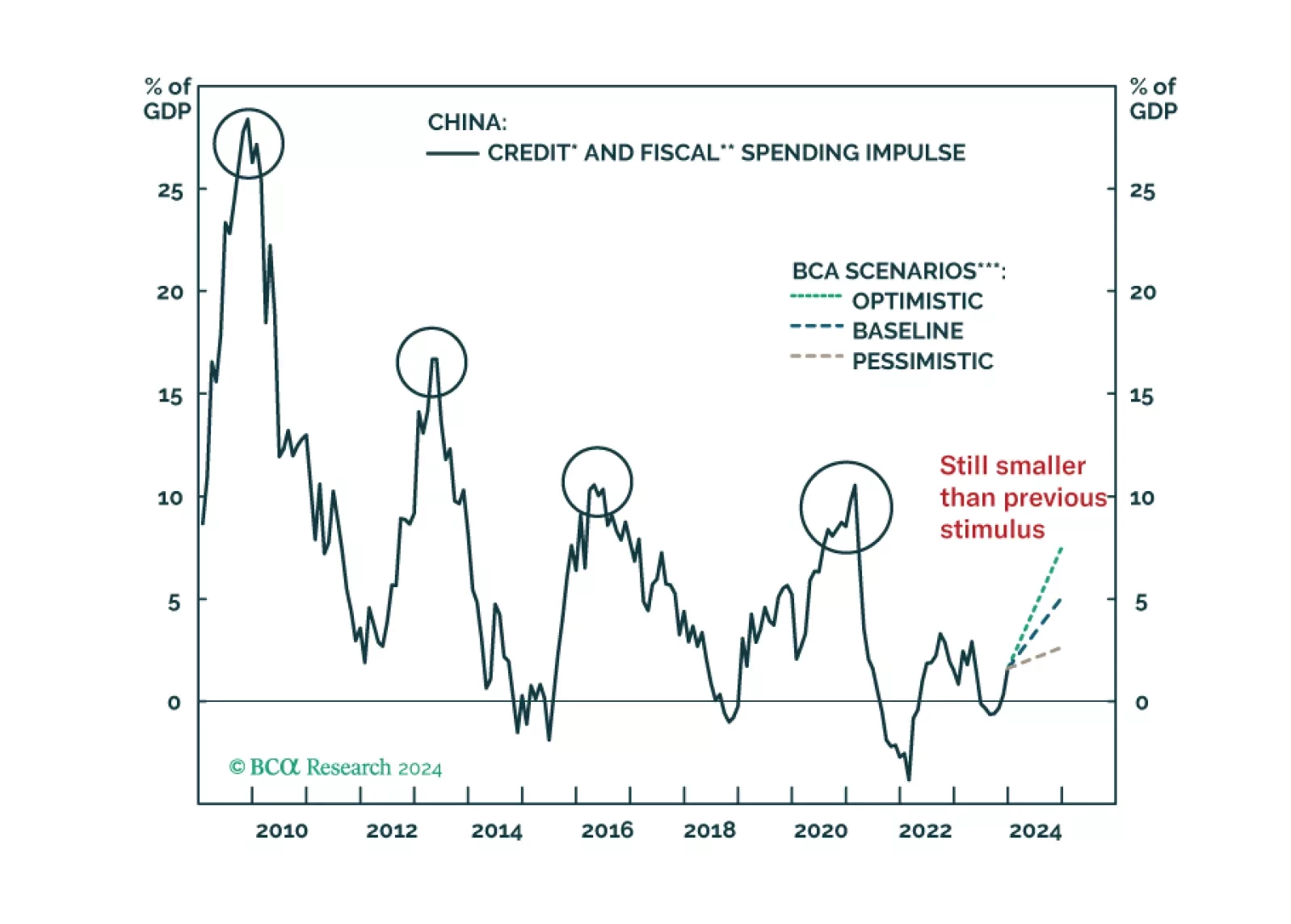

The stimulus measures announced at last week's NPC were not a game changer. As in 2023, we expect aggregate government spending will fall short of the budgeted amount again this year.