Emerging Markets

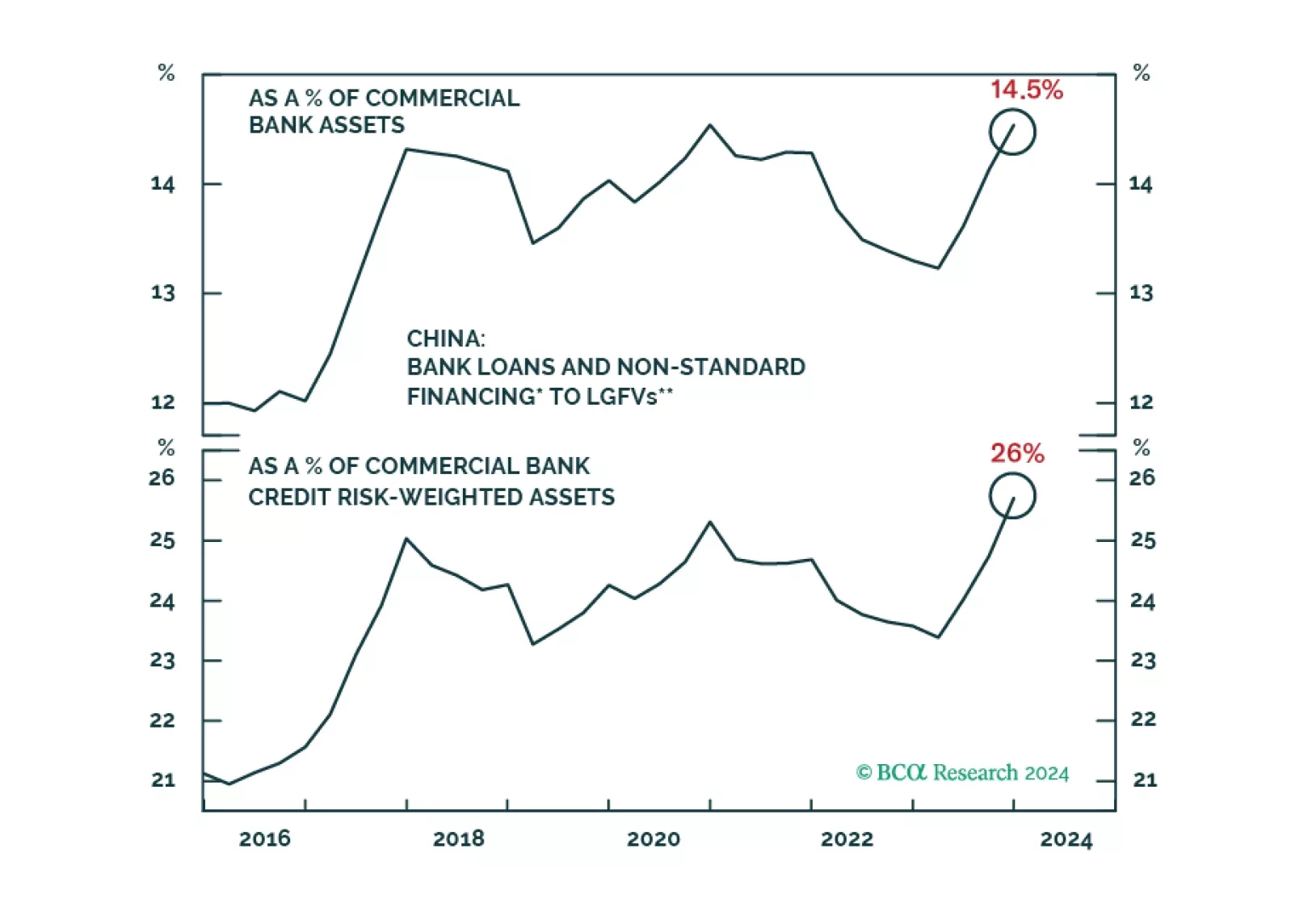

The odds of a “Minsky Moment” for the Chinese banking sector are low. They, however, will continue facing cyclical and structural headwinds, including a dismal asset quality and profit outlook. Bank stocks remain a value trap. Absolute-return investors should sell rebounds in Chinese bank stocks.

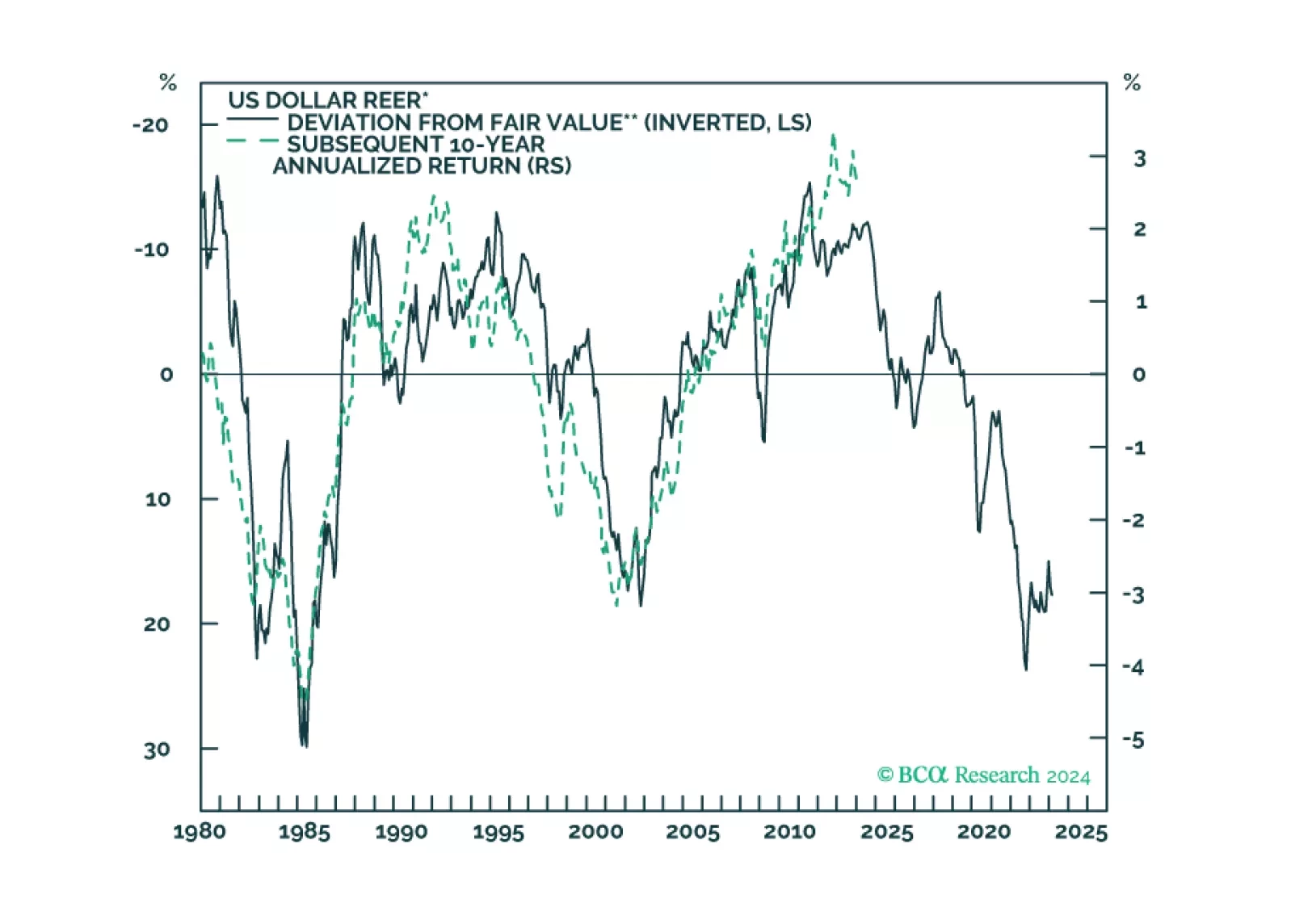

In this week’s report, we release an update to our long-term REER valuation model and expected future returns for major currencies.

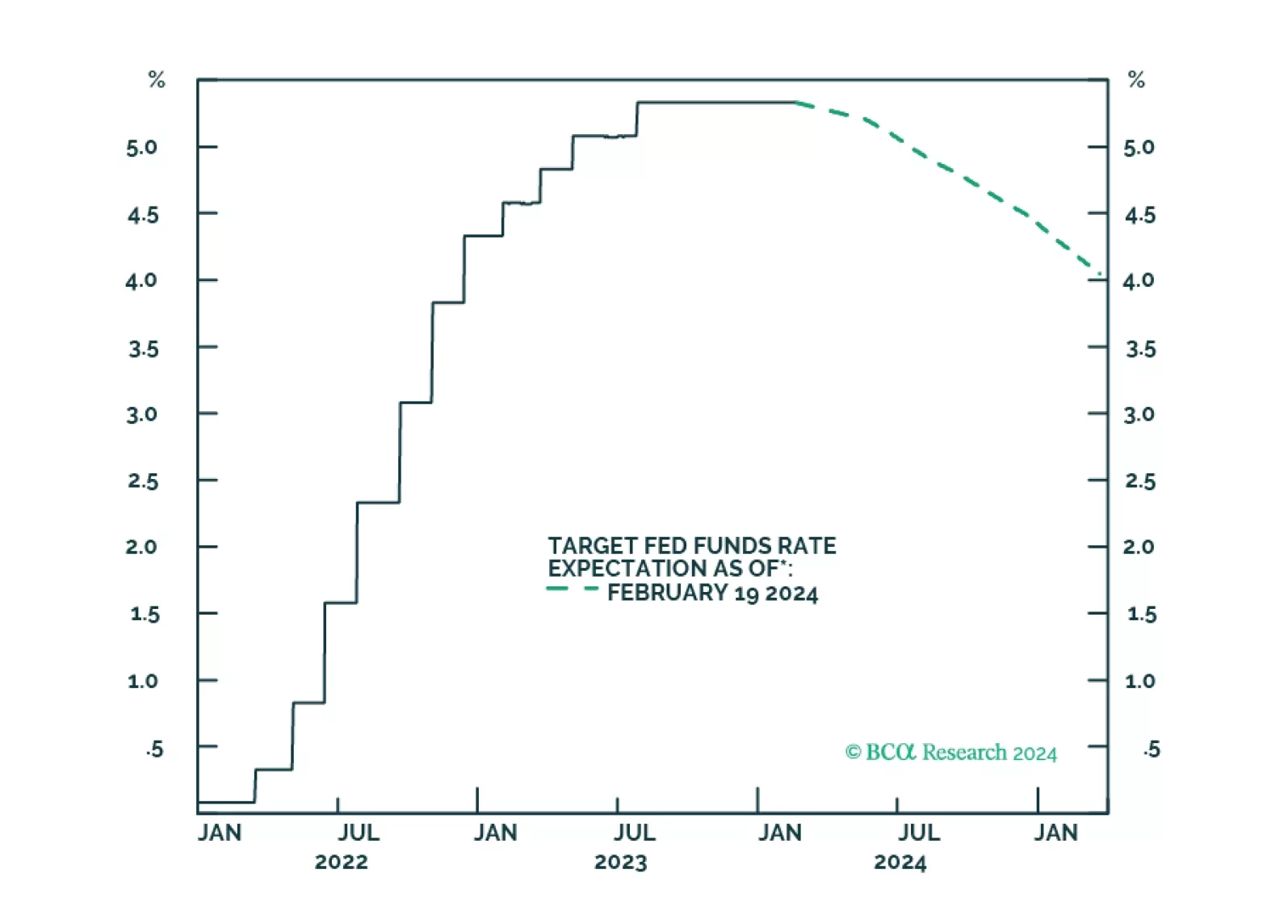

Seasonal weather and price variability in the first quarter will dissipate, which will reduce the agita caused by the recent inflation scare. This will increase the Fed’s comfort level in initiating a rate-cutting cycle in June with a 25 bp cut. With inflation well-behaved, real interest rates will move lower and gold prices will move higher. The rate-cutting cycle also will allow the USD to weaken as assets ex-US become more attractive; this will be bullish for gold. Physical demand for gold is expected to remain robust, along with safe-haven and central-bank diversification demand, due to heightened geopolitical uncertainty. We continue to expect gold to trade above $2,200/oz this year.

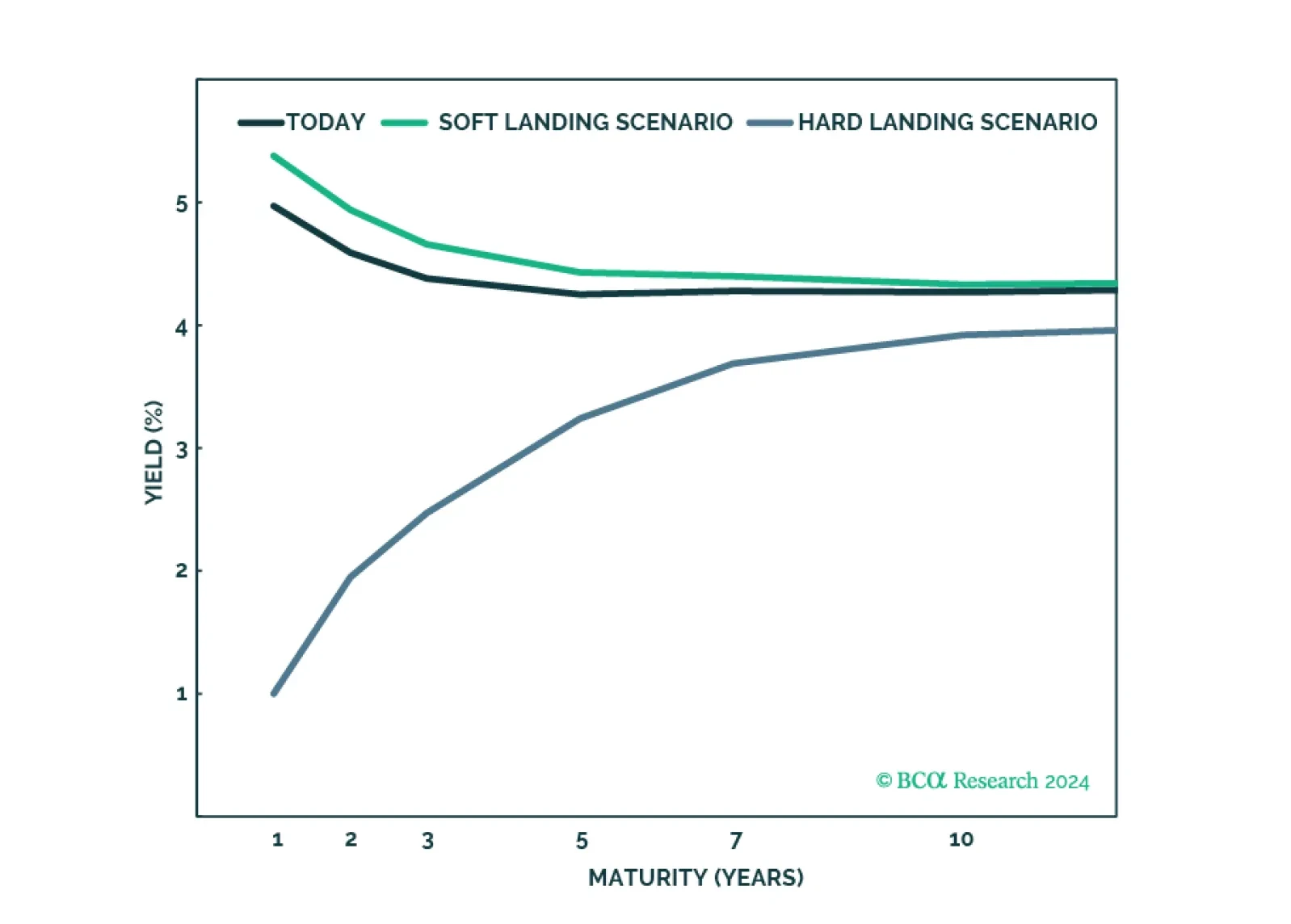

We rank the US spread sectors in terms of risk versus reward.

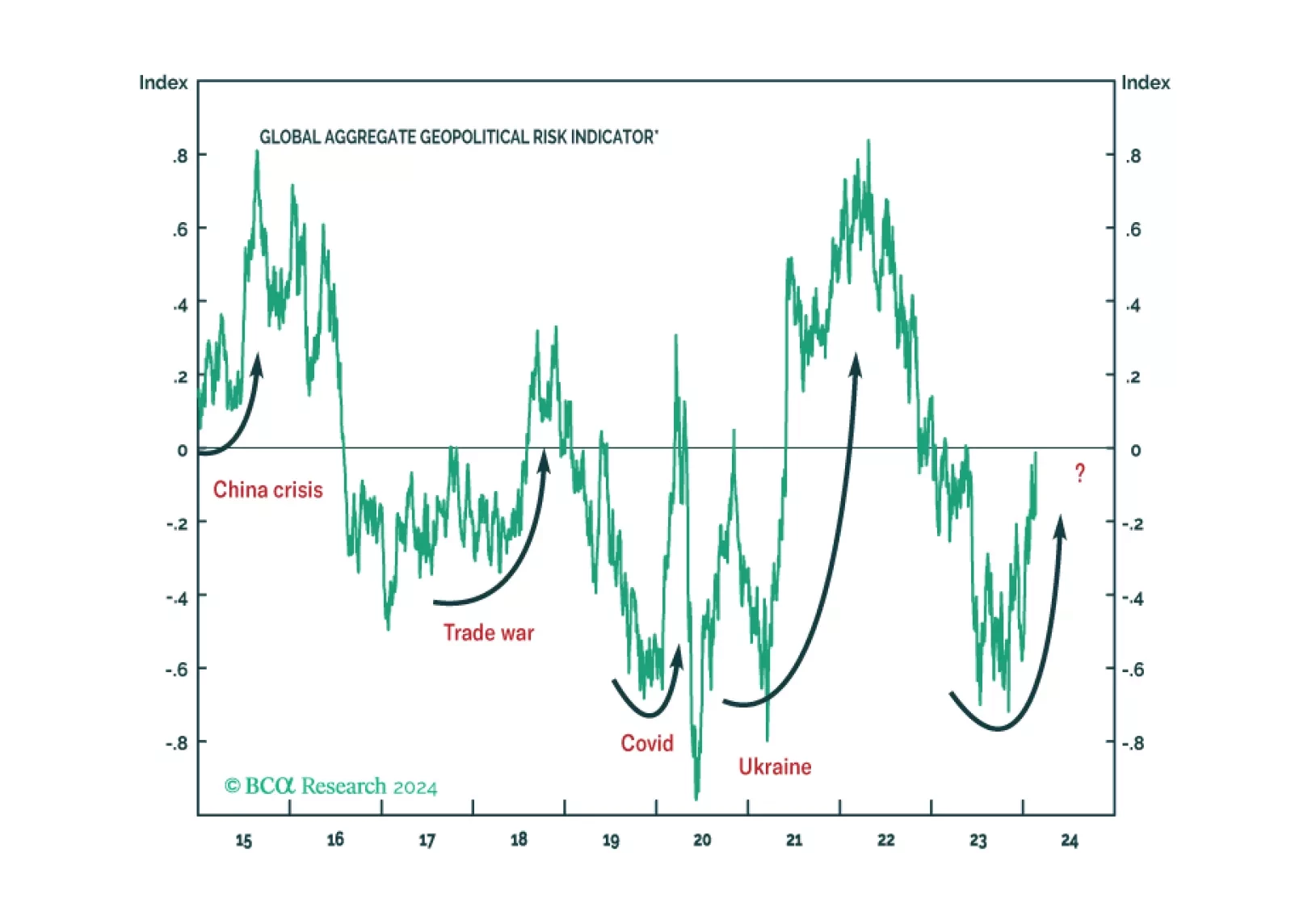

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.

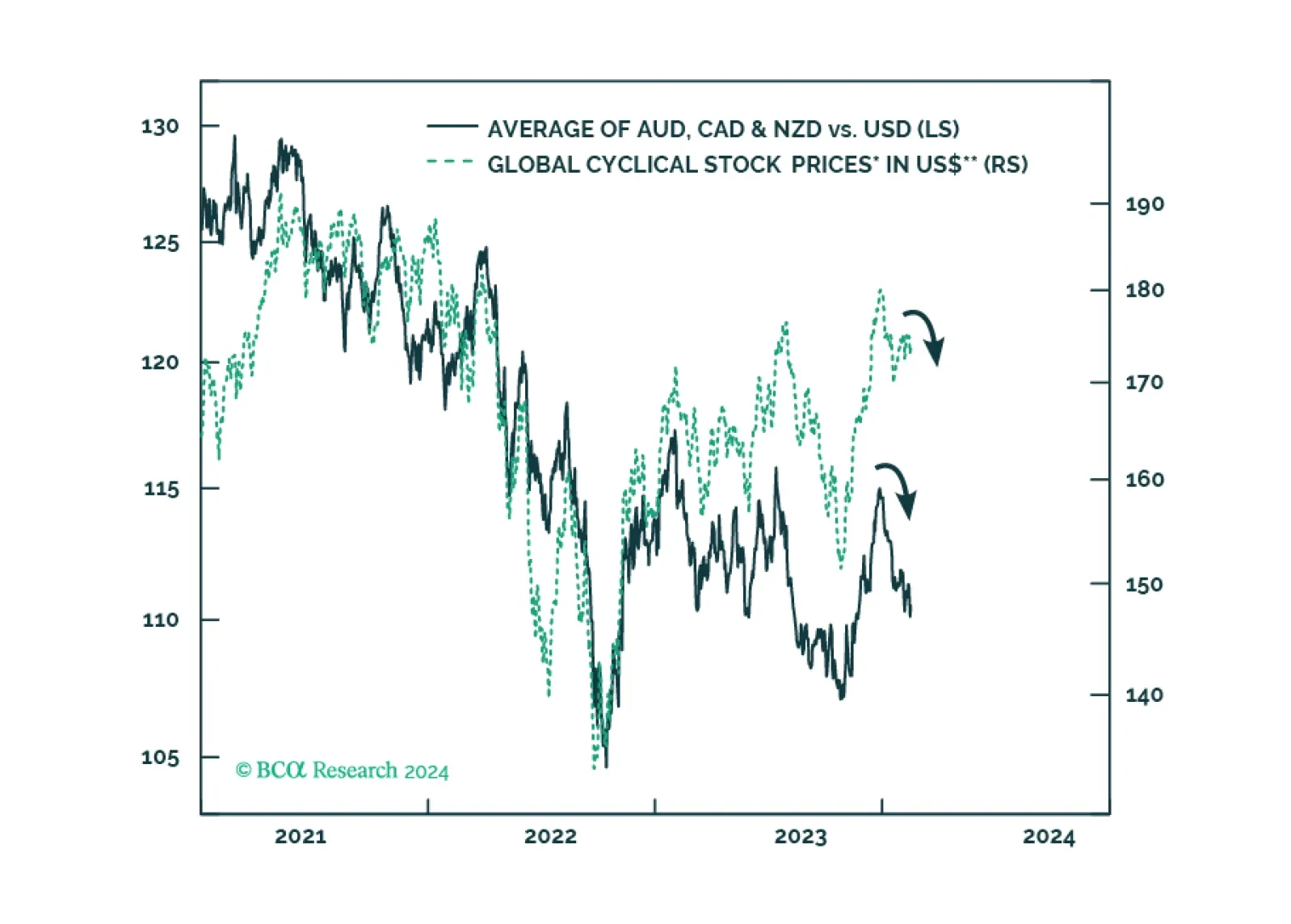

Over the next six months, the deterioration in non-US growth will occur earlier and be more pronounced than in the US. This expectation reinforces our confidence to bet on the strength of the US dollar. As usual, the flip side of the US dollar strength will be weakness in EM risk assets.