Equities

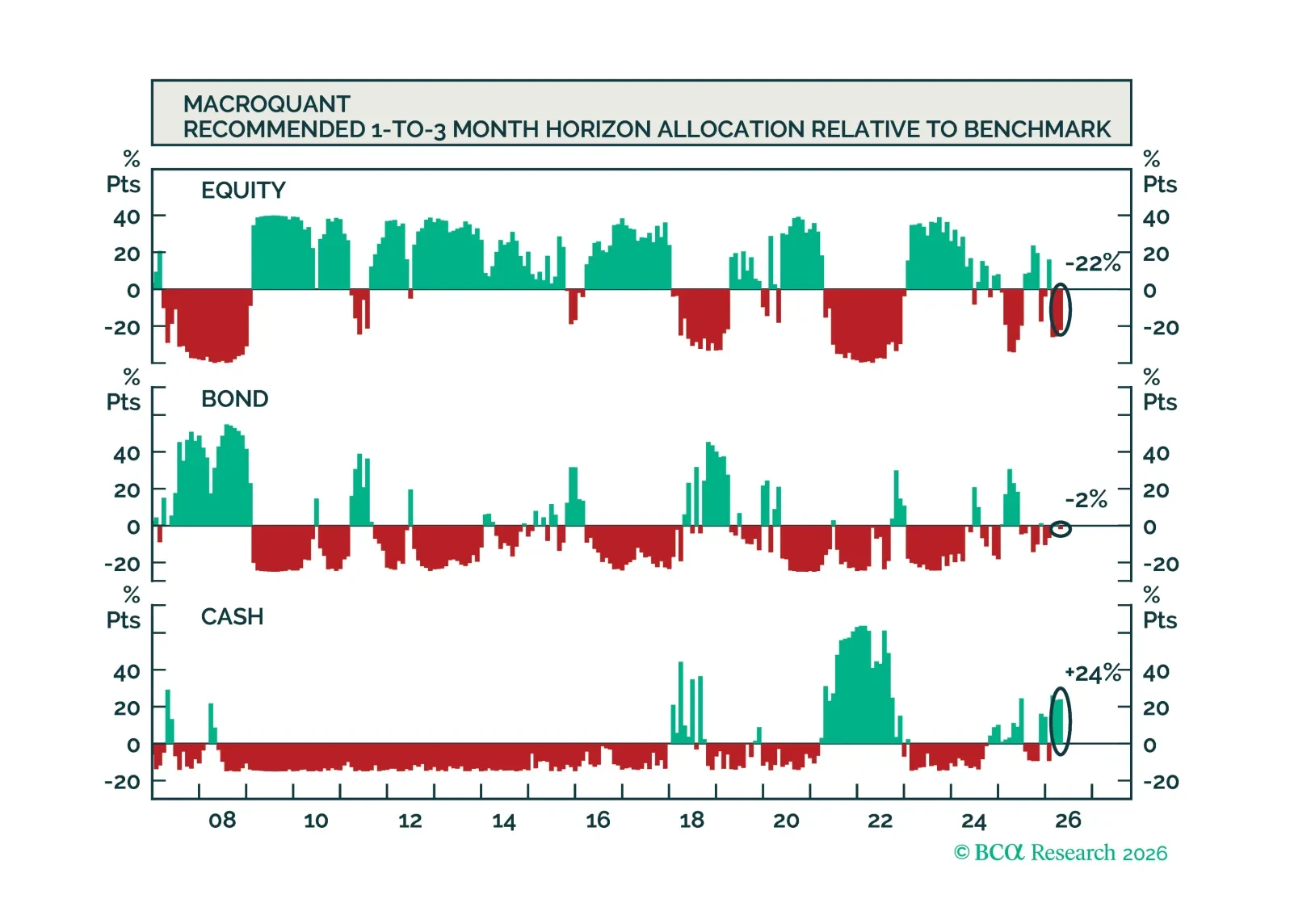

MacroQuant recommends a slight underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is very positive on the US dollar, downgrades gold to underweight, upgrades copper to overweight, and remains very bullish on oil.

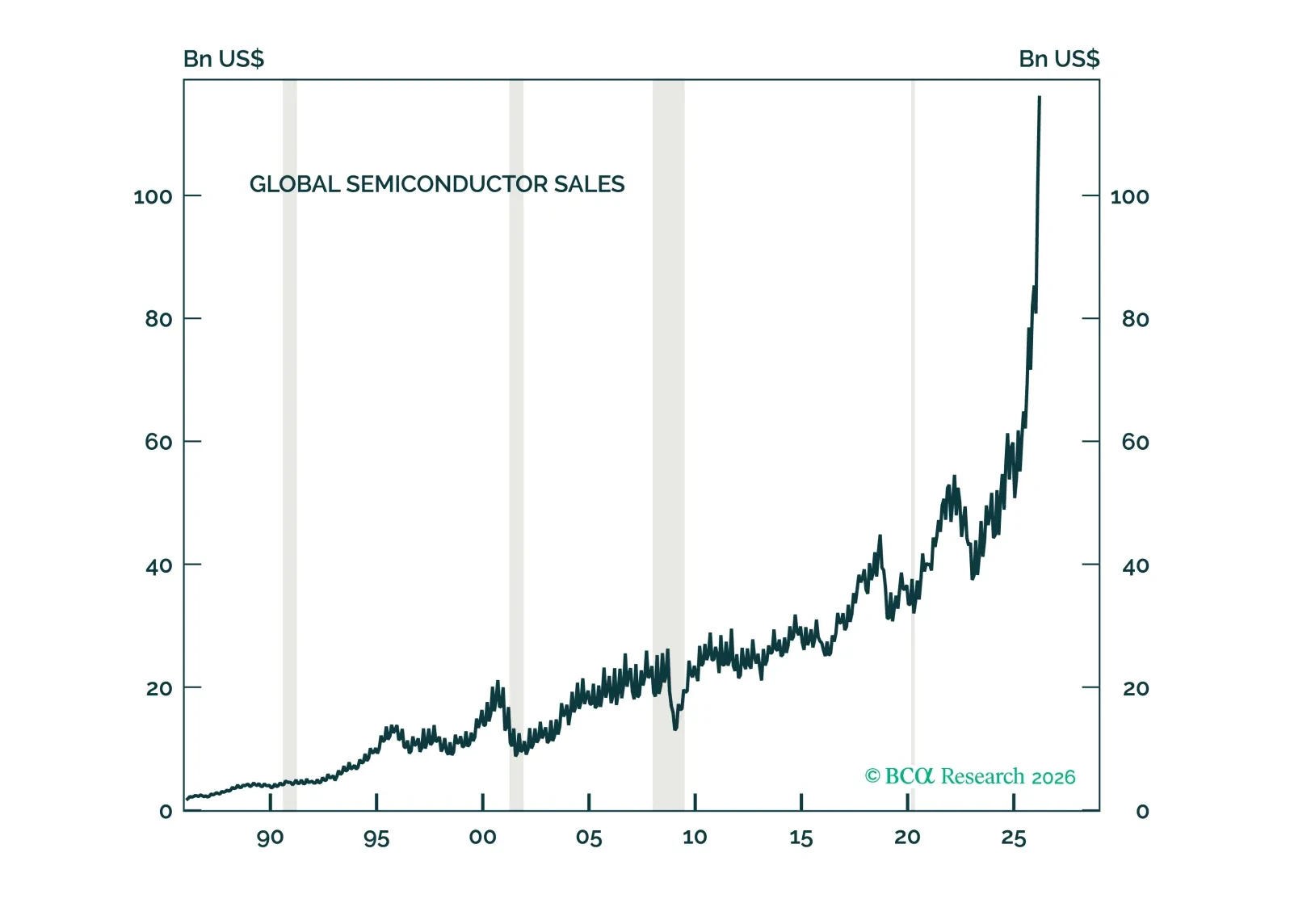

The AI bubble is a different type of bubble. It is primarily an earnings bubble rather than a valuation bubble. Like all bubbles, the AI bubble will burst. For now, however, our AI demand indicators do not suggest that this is imminent.

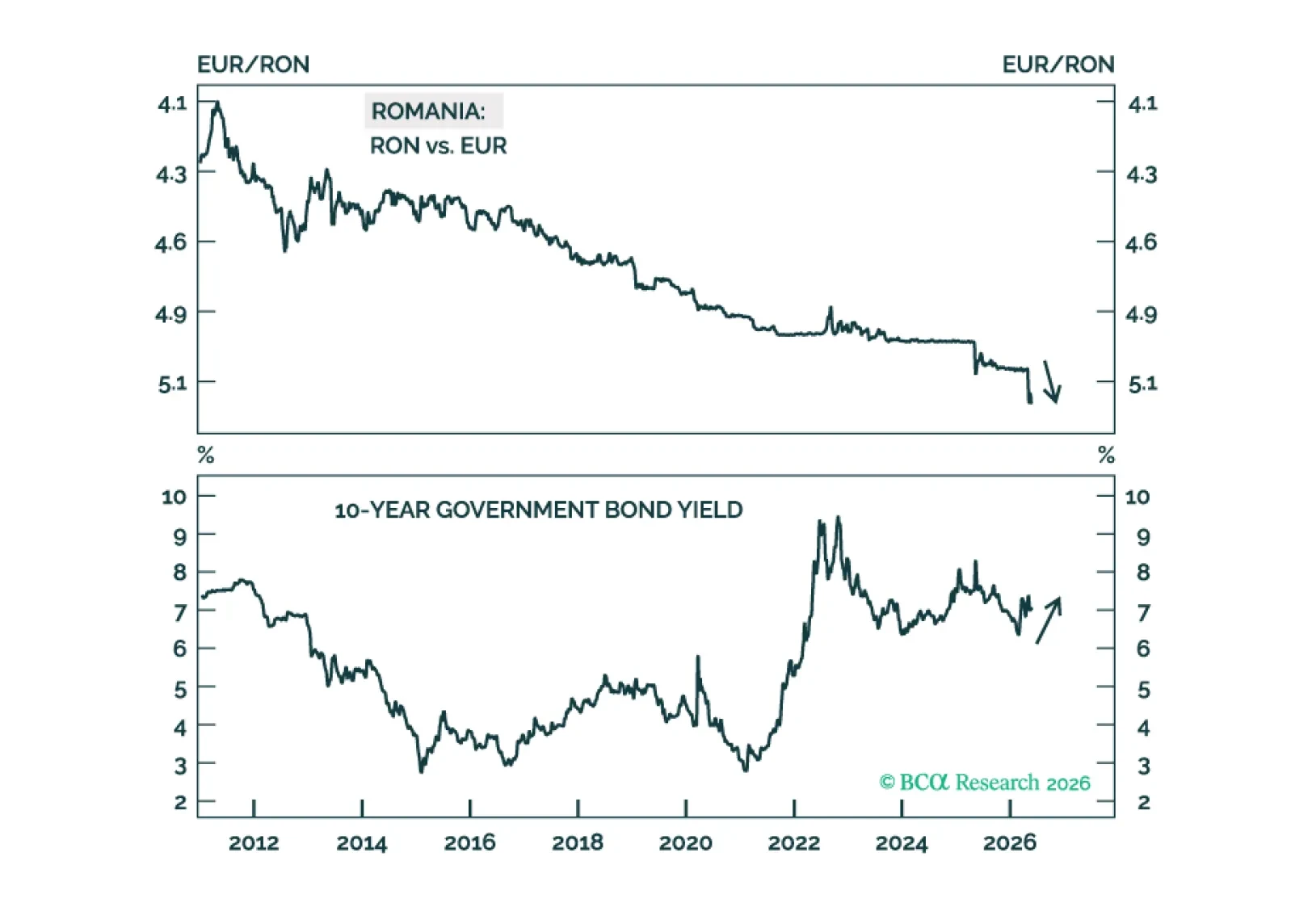

In Romania, large fiscal and current account deficits, high inflation, negative real rates, an overvalued exchange rate, and deteriorating growth point to budding currency devaluation. Investors should short the Romanian currency versus the euro and underweight Romanian local bonds, equities, and sovereign credit.

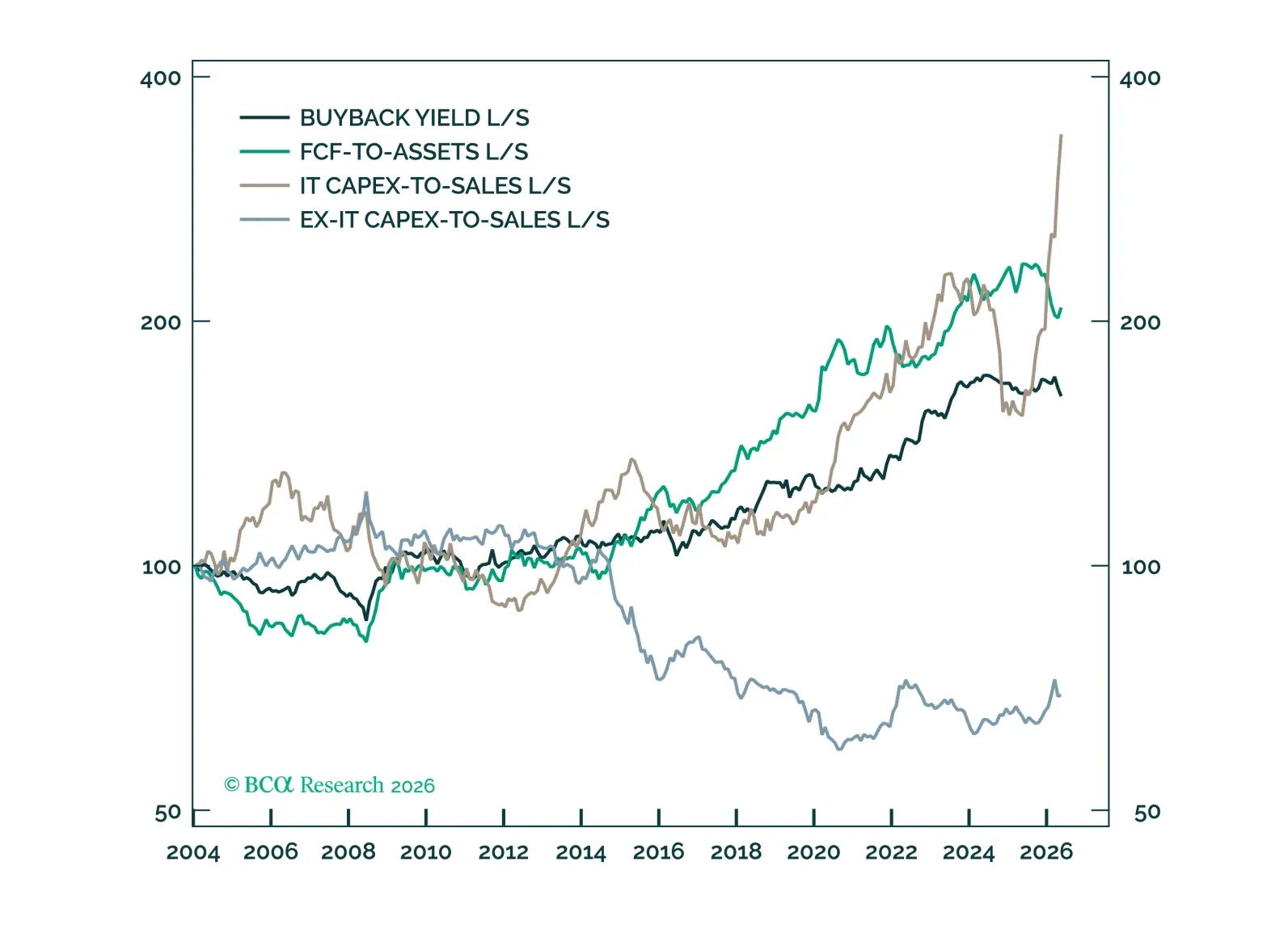

Tech, and increasingly the market, is moving from a cash-return regime to a reinvestment regime. After the GFC, investors rewarded companies that returned cash to investors. In the AI cycle, they are rewarding companies that put that cash back to work. This is not just a story of falling free cash flow; it is the mirror image of a market rewarding reinvestment. Tech has defined both regimes, revealing the old cash-flow “stars” as sector bets masquerading as alpha.

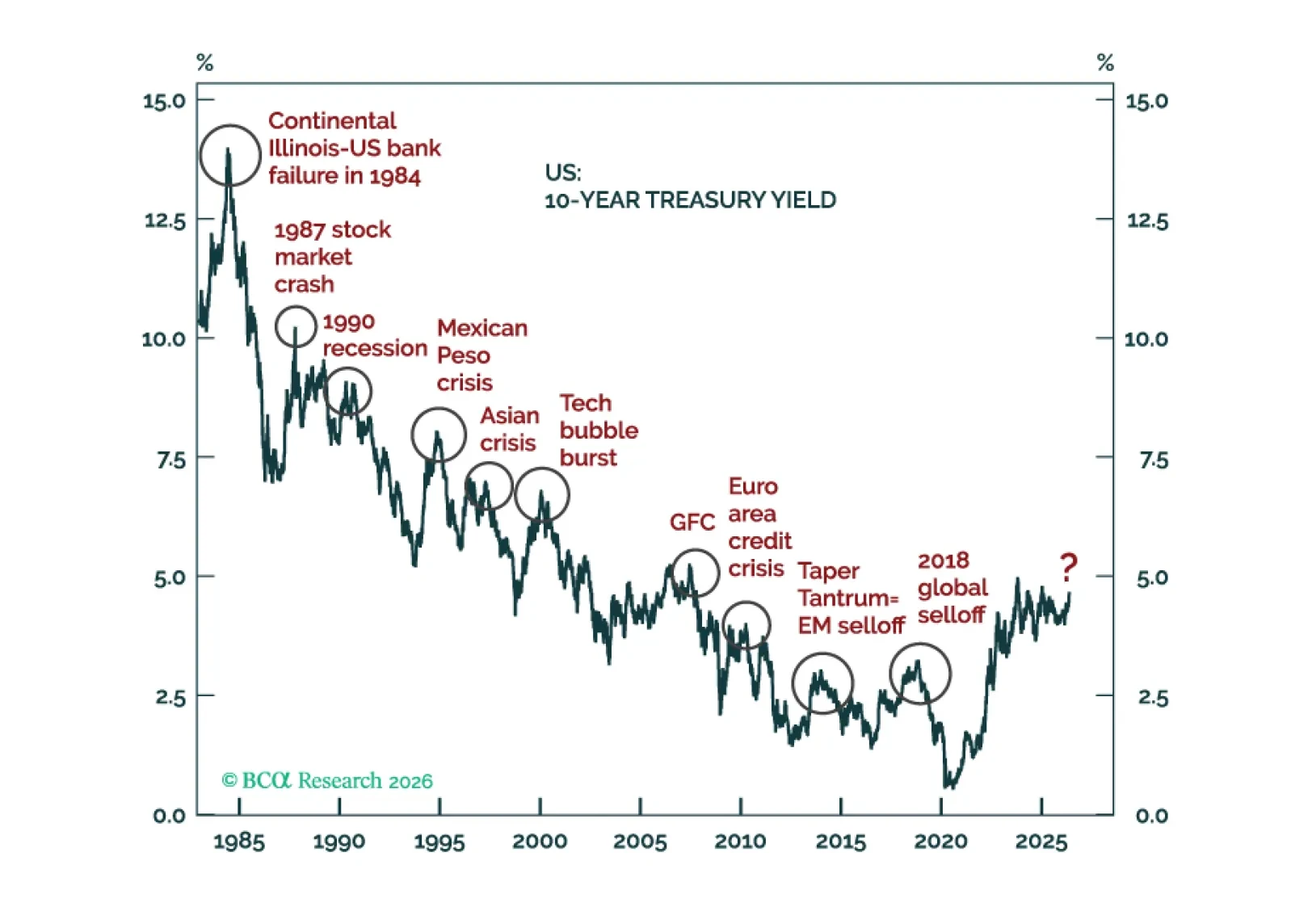

US stocks and bonds are on a collision course. Only a meaningful equity selloff is likely to pull bond yields considerably lower. Global equity risk-reward looks poor. The dollar will stay firm near term, but its medium- and long-term outlook remains bearish.