Equities

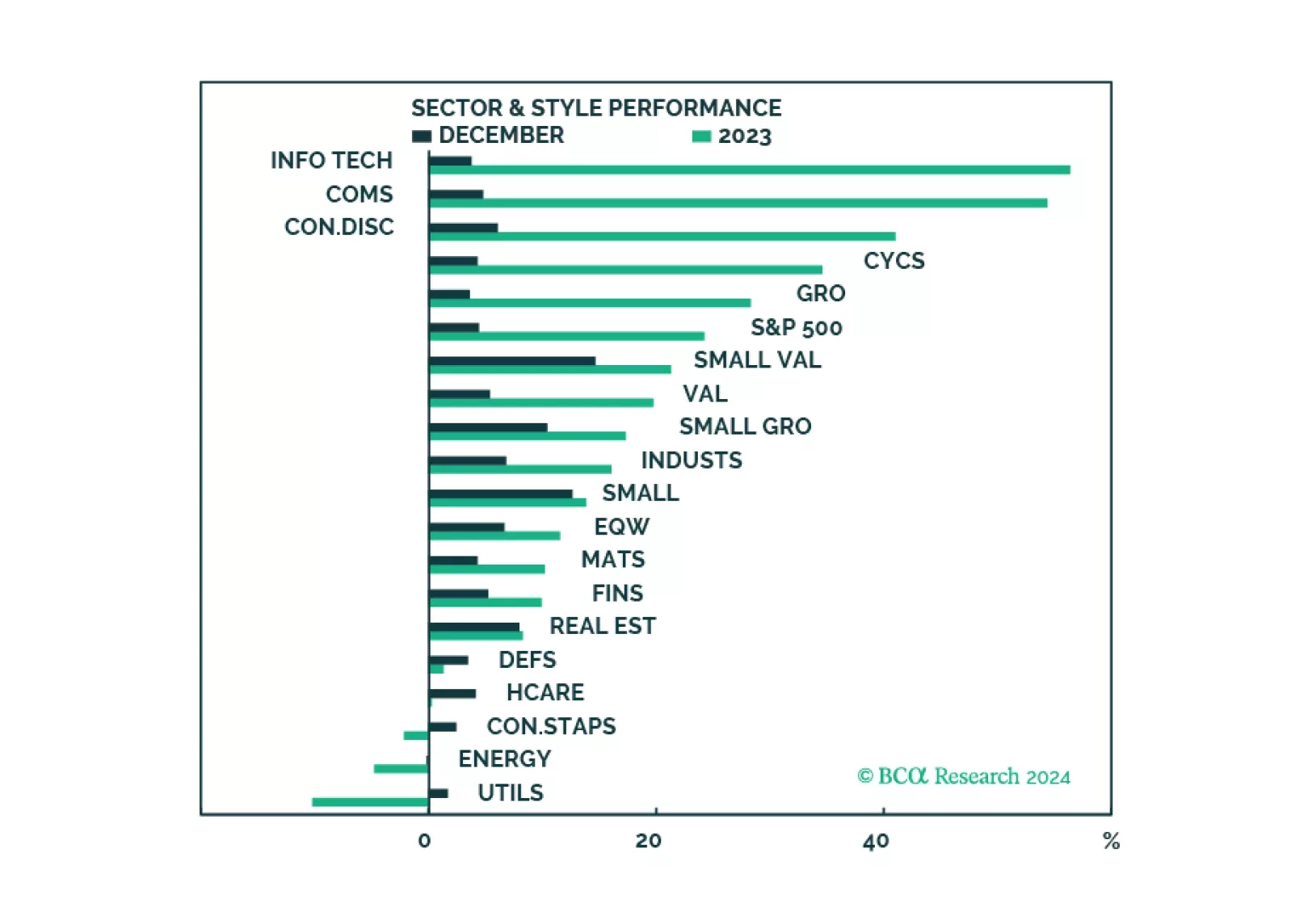

The Santa Claus rally has been fueled by investors optimism about a soft landing which is the least likely macro outcome in 2024. A pullback in the market is imminent as the probability of "too hot" or "too cold" will get priced in. We are downgrading Software and Services on a tactical basis to take profits but maintaining a strategic overweight in the same trade.

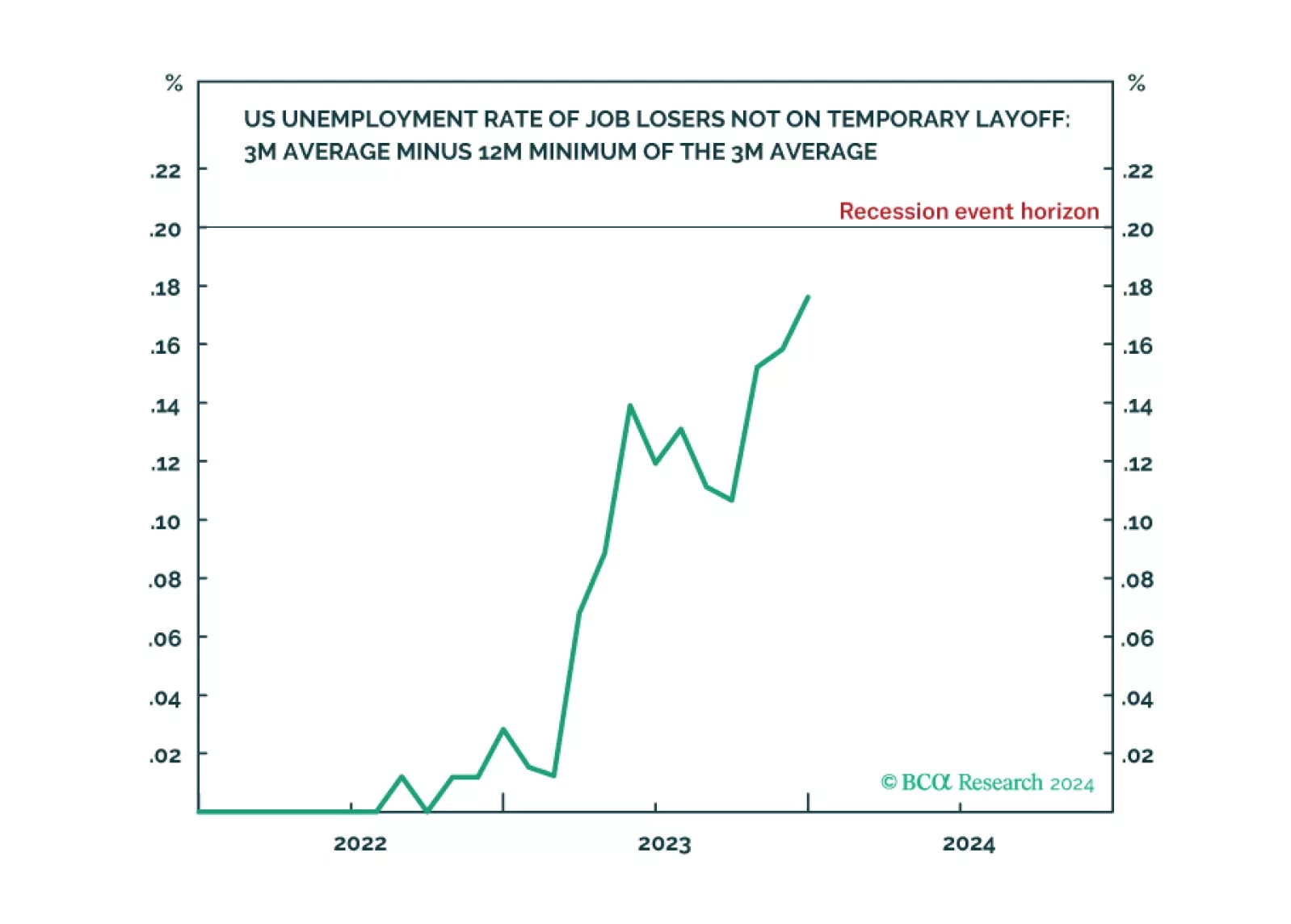

Following today’s US jobs data release, the Joshi rule real-time US recession indicator inched up to 0.18 and is now just a whisker from its recession event-horizon of 0.20.

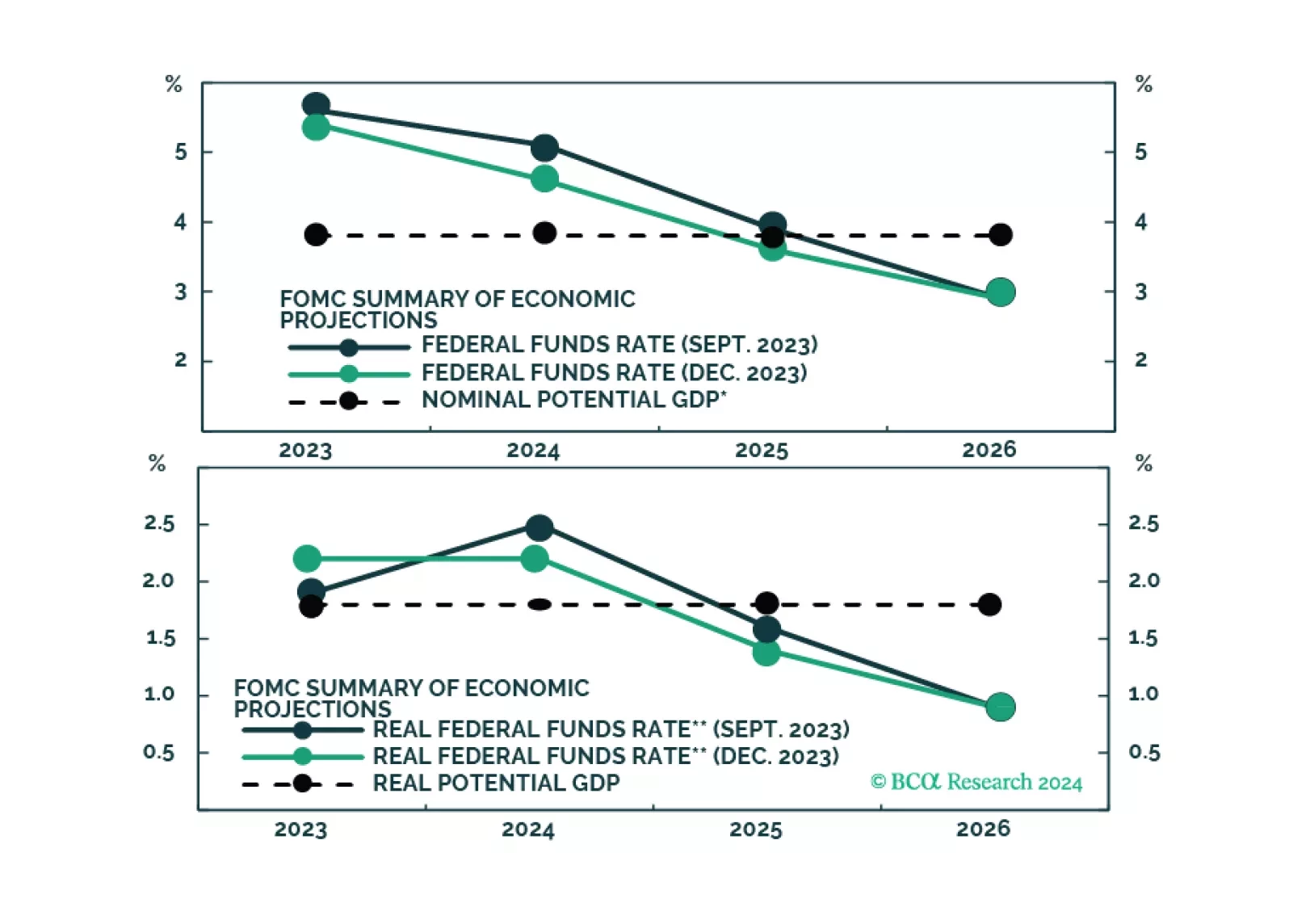

A soft landing can be achieved but not maintained. We are cutting our tactical recommendation on stocks from overweight to neutral and scaling back our long-duration stance.

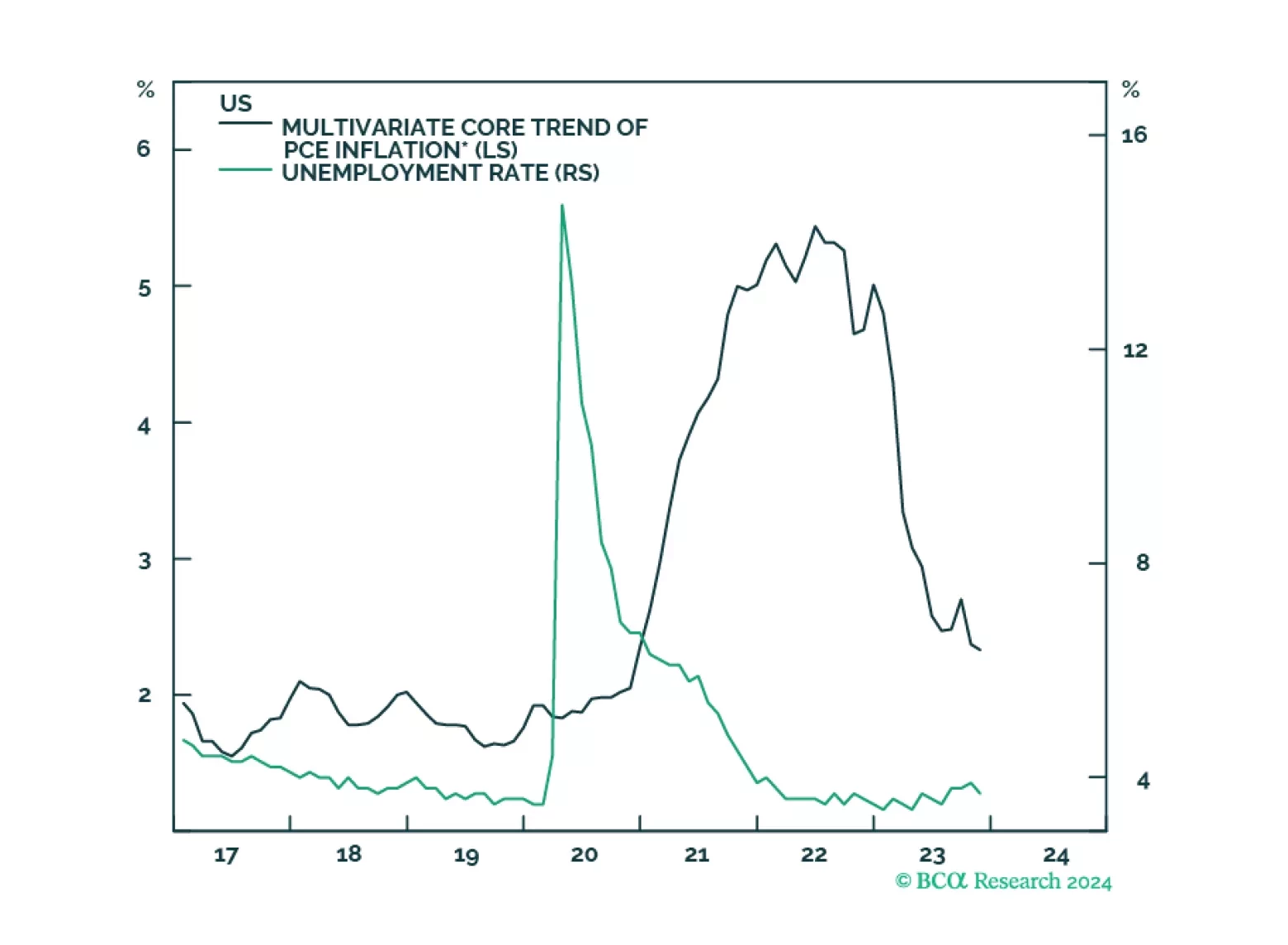

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?

In this final note for the year, we take profits and close several long-term investment positions: Overweights in Insurance and Commercial Services, and underweights in Utilities, and Retail and Commercial REITs.