Equities

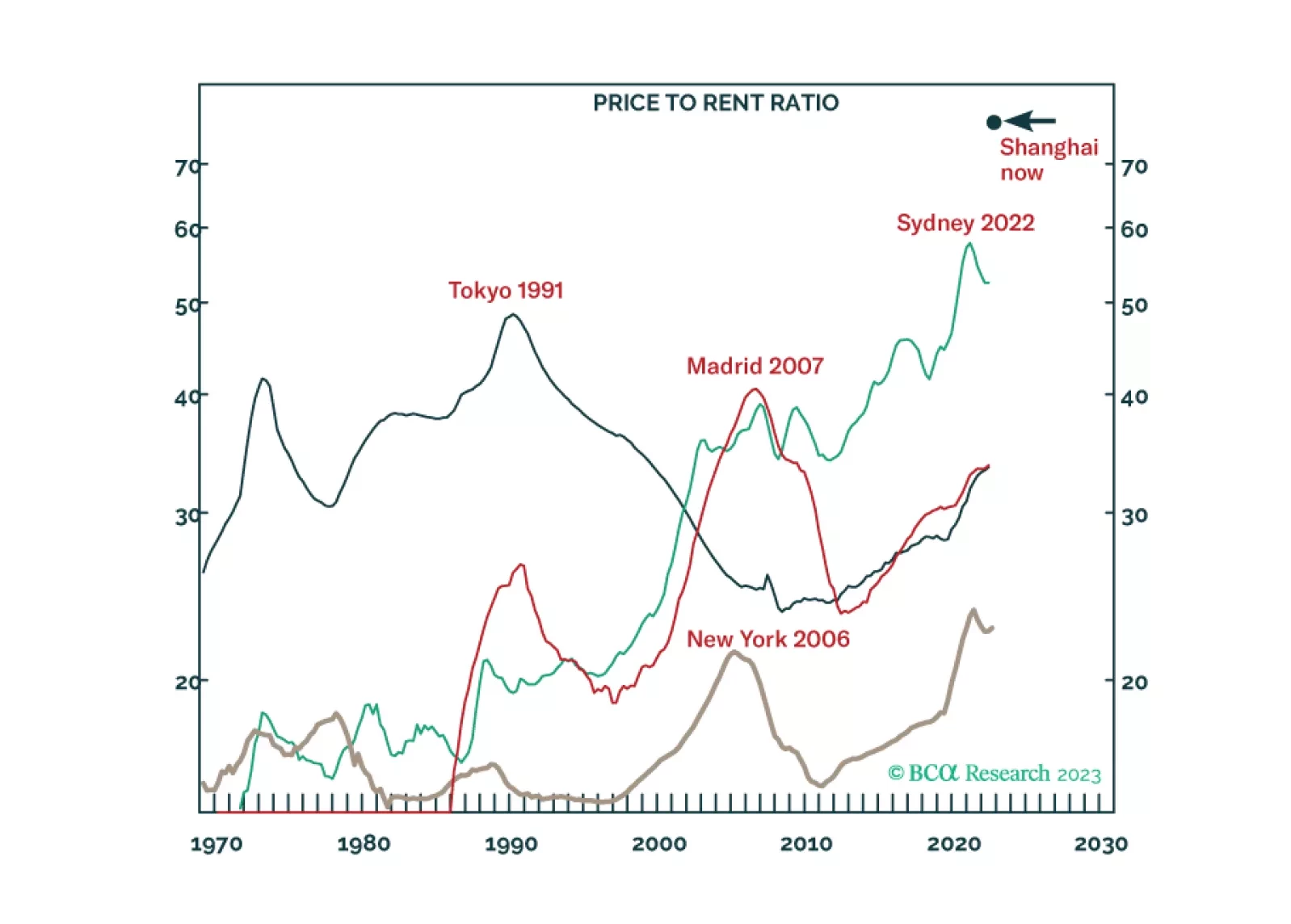

Our 2024 outlook can be encapsulated into just 39 words and three key views. Key view 1: The end of China’s housing boom means the end of the world’s main growth engine. Key view 2: If the Fed and ECB don’t kill the economy, they won’t kill inflation. Key view 3: The AI gold rush will struggle to find any gold. We go through the investment implications for the year ahead.

Our recommendations for blogs and X’s (on the economy, financial markets, asset allocation, bonds, quants, energy, real estate, geopolitics, and specific countries and regions) to try over the holidays.

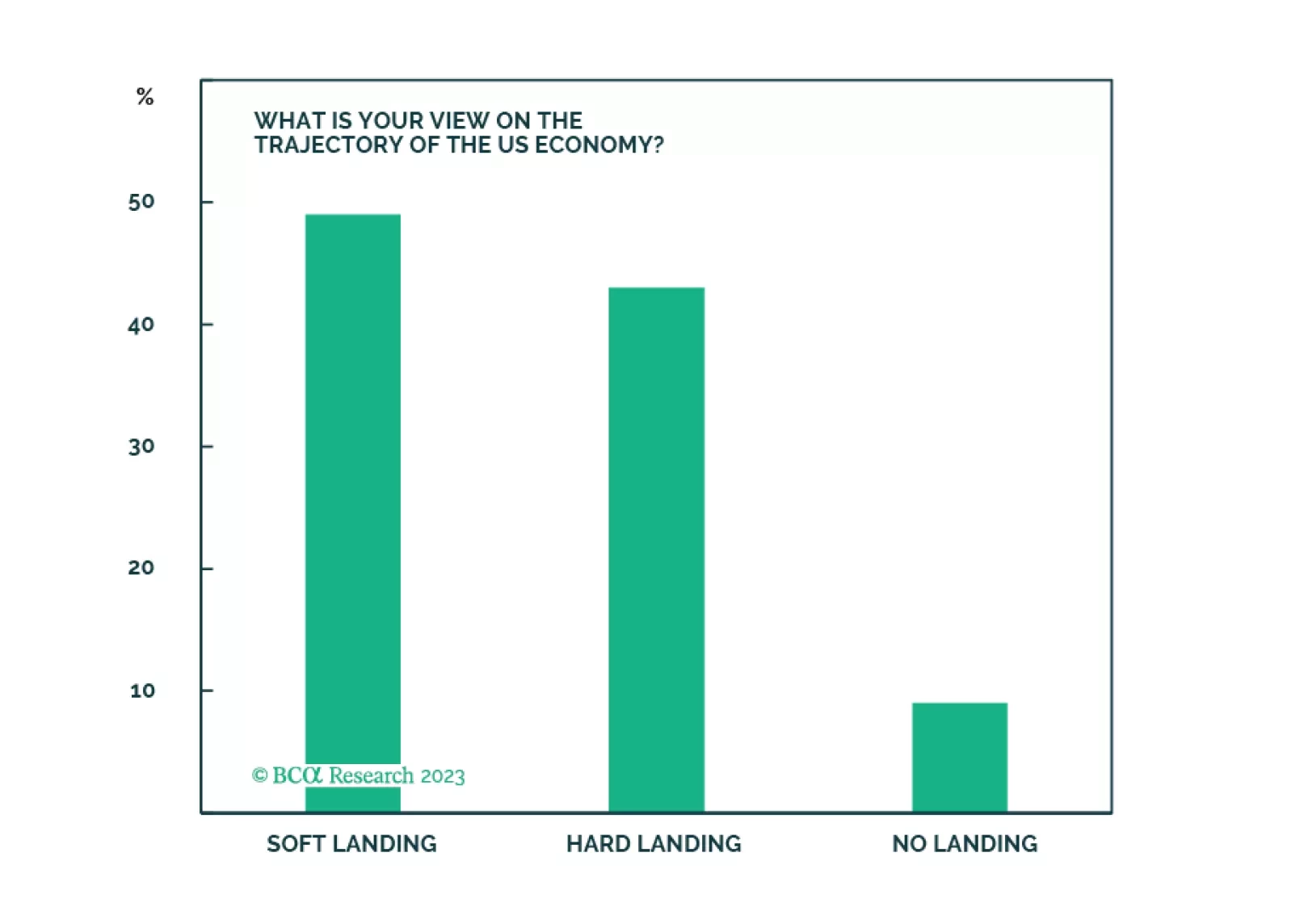

The Santa Claus rally is a repricing of the "soft landing" scenario as a likely economic outcome. Yet, many investors remain cautious, and harbor significant cash balances. Next year, repricing of various scenarios will continue, and volatility will be elevated. We remain in a "hard landing" camp and recommend defensive stance on a strategic investment horizon.

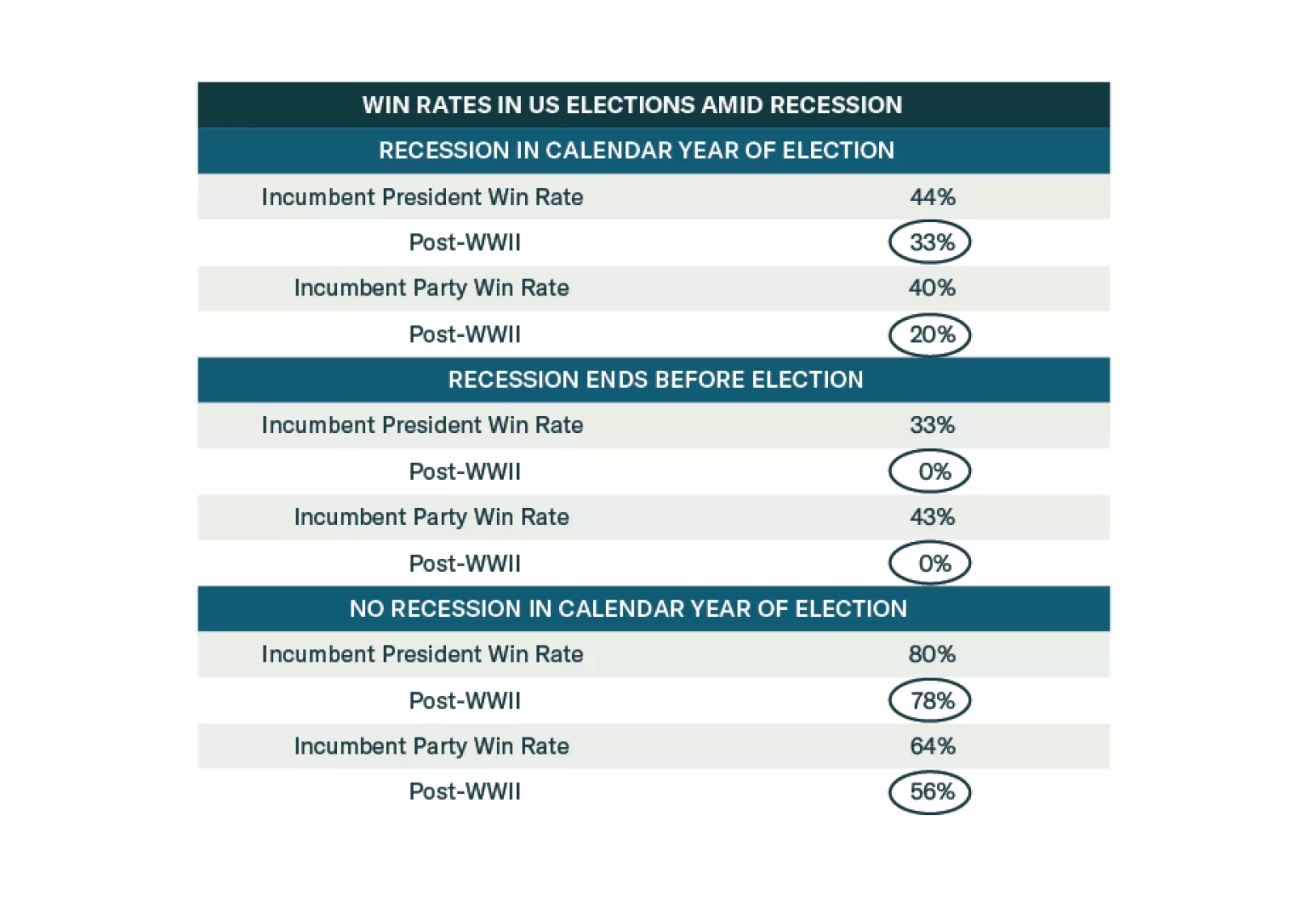

Democrats are favored to win the election until recession materializes. But recession risks are high. Investors should adopt a defensive and conservative strategy in 2024 amid extreme US policy uncertainty.